Compounder Fund: Portfolio Update (January 2022) - 12 Jan 2022

Jeremy and I intend to share frequent but non-scheduled updates on how Compounder Fund’s portfolio looks like. The last time we shared an update on this was for Compounder Fund’s portfolio as of 10 October 2021.

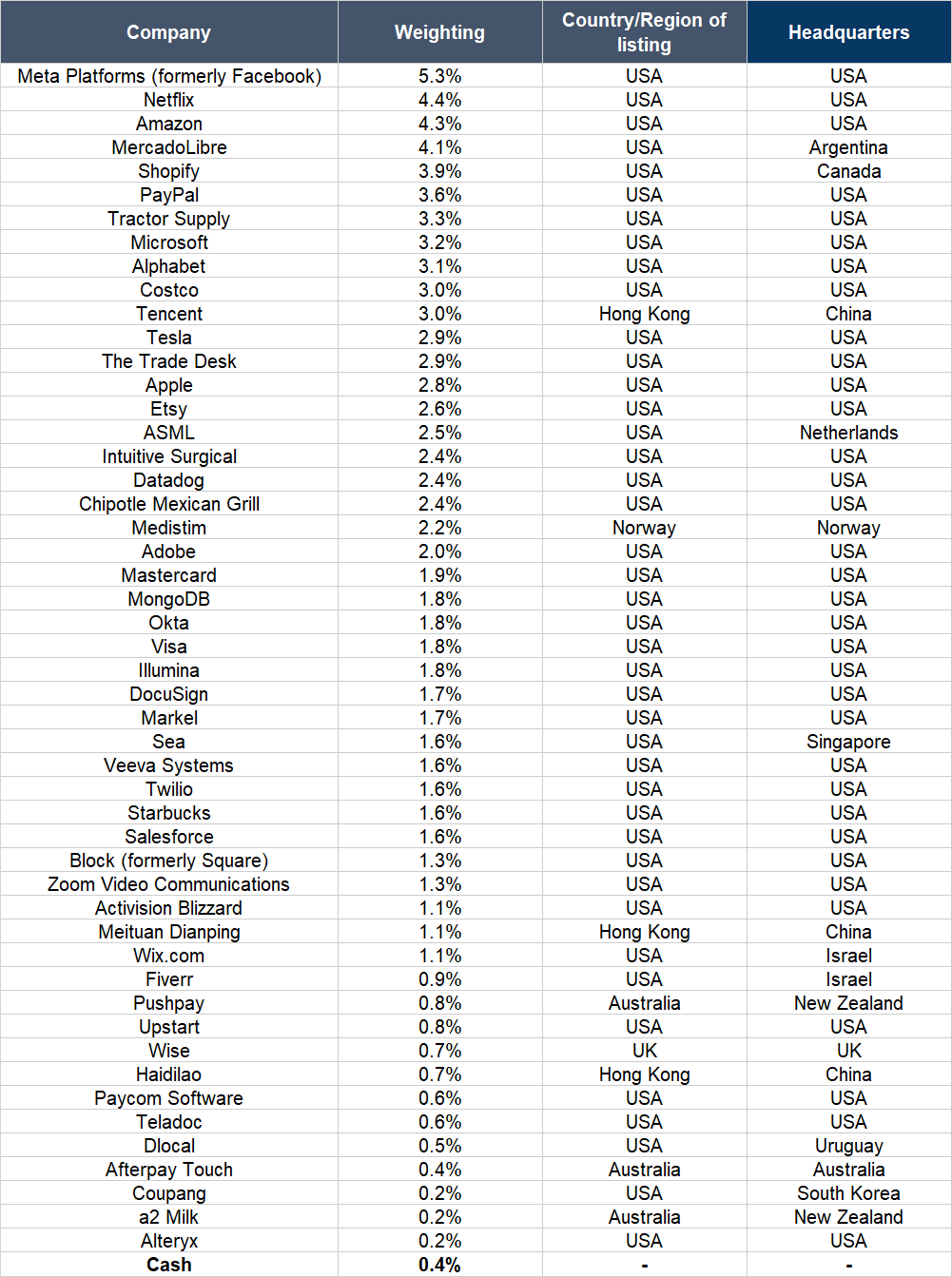

In the update, I shared all 50 holdings in the fund’s portfolio. As of the date of this update, the portfolio contains the same 50 holdings, and there are no new stocks added. As a reminder, Compounder Fund is supposed to have between 30 and 50 companies in its portfolio at any point in time. But two companies in the portfolio – Afterpay and Square (now known as Block) – will become one entity soon (we discussed this development in detail in the aforementioned update). So we think it is more appropriate to see Compounder Fund as having 49 holdings instead of 50.

In late-November 2021, Jeremy and I used a portion of Compounder Fund’s small cash position of around 1.9% back then to add to our positions in nine of the fund’s existing holdings. They are (in alphabetical order): Datadog, dLocal, MercadoLibre, MongoDB, Teladoc, The Trade Desk, Twilio, Upstart, and Zoom.

As you may know, Compounder Fund is able to accept new subscriptions once every quarter with a dealing date that falls on the first business day of each calendar quarter. In the middle of December 2021, Jeremy and I successfully closed Compounder Fund’s fifth subscription window since its initial offering period (which ended on 13 July 2020). This new capital was deployed quickly in the days after the last subscription window’s dealing date of 3 January 2022. Jeremy and I invested most of the new capital in nine existing Compounder Fund holdings. These companies are (in alphabetical order): Alphabet, DocuSign, MercadoLibre, MongoDB, Sea, Tesla, Twilio, Upstart, and Zoom.

As of this update’s publication, we have released our investment theses on all 50 companies that are currently in Compounder Fund’s portfolio and they can be found here. In the future, if and when we add new companies to the portfolio or completely exit any of the 50 companies, we will be publishing our theses for these actions.

In Compounder Fund’s Owner’s Manual, we mentioned that “if Compounder Fund receives new capital from investors, our preference when deploying the capital is to add to our winners and/or invest in new ideas.” Not all of the nine existing holdings in Compounder Fund’s portfolio that we added capital to have seen their stock prices rise strongly after we initially invested in them. But all of them have executed brilliantly in recent times and produced excellent results as you’ll soon see in the “Wonderful businesses” section of this letter. They are winners, according to our definition. Here’s how Compounder Fund’s portfolio looks like as of 9 January 2022:

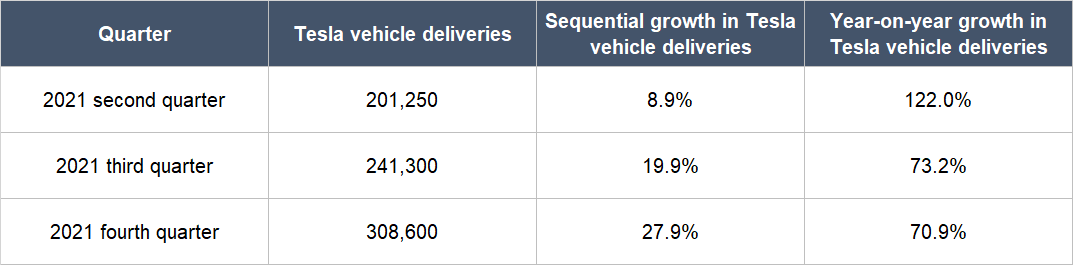

Our biggest addition in early-January 2022 was to electric vehicle pioneer, Tesla. In our investment thesis for the company, we wrote that “because of the power of Tesla’s brand, we believe that the real bottleneck for Tesla is not a lack of demand, but its production capacity.” The company has made impressive improvements to its manufacturing over the course of 2021. Our investment thesis mentioned that Tesla’s vehicle deliveries for the first quarter of the year was 184,800. This represented a pleasing increase of 2.3% sequentially (from the fourth quarter of 2020) and 109.0% year-on-year (from the first quarter of 2020). Table 7 shows the continued strong growth in Tesla’s vehicle deliveries for the second, third, and fourth quarters of 2021. As Tesla continues to ramp up its vehicle deliveries, we think the company becomes less risky as an investment opportunity. This is because the company is proving that it can grow its manufacturing rate and that consumer demand for its vehicles is healthy.

Source: Tesla announcements

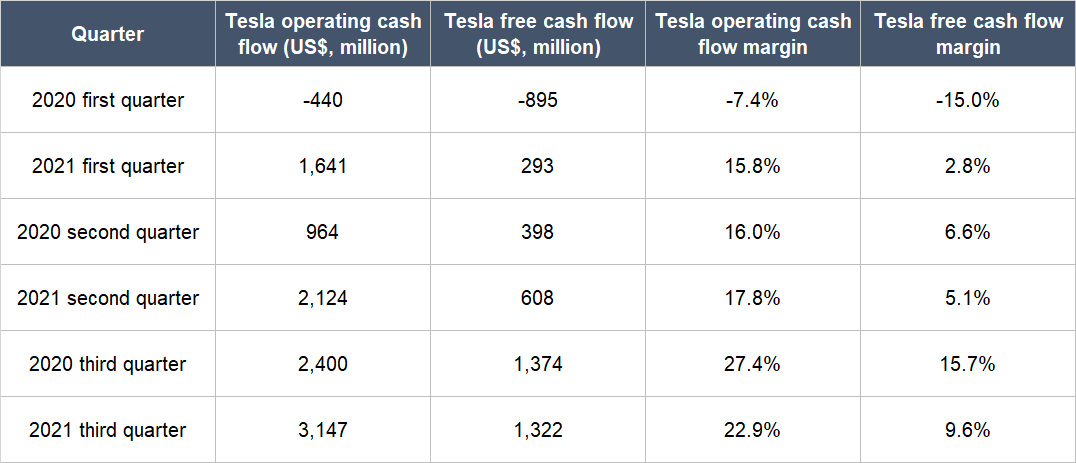

At the same time, Tesla’s cash flow situation continues to look bright. In the first three quarters of 2021, Tesla’s operating cash flow improved substantially in each quarter from their respective year-ago periods. The company also either maintained or grew its free cash flow in each quarter (from a year ago) for the same time period. If there’s one thing about Tesla’s cash flows we would criticise, it would be the declines in the margins seen in the second quarter of 2021 (for the free cash flow margin) and the third quarter (for both the operating cash flow and free cash flow margins). These are all shown in Table 8. But it’s still encouraging to see the growth in the two important cash flow numbers, as well as the mid-teens to mid-twenties percentage range for the operating cash flow margin. There is also a good reason for the fall in Tesla’s free cash flow margins: The company has been ramping up its capital expenditures, primarily for its new factories (in Texas, USA, and Berlin, Germany) and to increase capacity in its factory in Shanghai, China.

Source: Tesla earnings updates

Two of Compounder Fund’s holdings – Facebook and Square – changed their names recently. Facebook assumed its new identity of Meta Platforms in late-October to reflect its aim to be an important force in the development of the metaverse. As part of his metaverse-commitment, Meta Platforms’ co-founder and CEO, Mark Zuckerberg, recently announced that the company would be investing at least US$10 billion annually on technology infrastructure that’s related to the metaverse. Jeremy and I described what the metaverse is and how it could be an intriguing growth opportunity for Meta Platforms in our investment thesis for the company. Meta Platforms will be pouring billions in capital to, in the words of Zuckerberg, “help the metaverse reach 1 billion people and hundreds of billions of dollars of digital commerce a day.” At the same time, the company is continuing to improve its core social media platforms (Facebook, Instagram etc.), which are still growing healthily. There’s no guarantee that Meta Platforms’ metaverse-related investments would be successful. But we’re happy to see the company attempt to develop a new pillar of growth while still paying attention to its core businesses.

Meanwhile, Square’s name-change to Block happened in December. Block’s leaders wanted a name with a stronger association with the company’s growing interest in blockchain technology. The Square name will now refer to one of the company’s core services, the merchant-focused Seller Ecosystem (our investment thesis for Block has a detailed description of its various businesses). As part of its blockchain ambitions, Block launched a business arm named TBD, which is building an open developer platform for blockchain-related financial services (primarily focused on Bitcoin), in the second quarter of 2021. Block’s core services – the consumer-focused Cash App and Square – are both still growing rapidly. During the third-quarter of 2021, Cash App’s non-Bitcoin related revenue grew by 33% year-on-year while Square’s revenue was up by 44%. In a similar manner to Meta Platforms, we’re happy to see Block attempt to build a new business with high-growth potential while continuing to invest in its current core growth-drivers.

Tencent, a Compounder Fund holding, announced last month that it will distribute 86.4% of its JD.com stake to its shareholders. Tencent shareholders will receive 1 JD.com share for every 21 Tencent shares that they own in March this year. Compounder Fund owns 7,000 Tencent shares, so it will become a direct owner of 333 JD.com shares soon (7,000 divided by 21 is 333.33, but there will be no fractional shares of JD.com distributed – Compounder Fund will instead receive cash-in-lieu for any would-be fractional shares of JD.com). JD.com is an e-commerce company that is based in China. Its roots can be traced to 1998, when Richard Liu Qiangdong set up a bricks-and-mortar retail company in the country. Liu, who remains as chairman and CEO of JD.com today, closed the physical store in 2004 to transition his retail business from the physical world to the internet. Today, JD.com is China’s largest online retailer by revenue with an impressive logistics footprint. The company’s approximately 1,300 warehouses have a total gross floor area of 23 million square metres and its network of 200,000 delivery personnel covers nearly all the counties and districts in China. Jeremy and I are deciding what we want to do with the JD.com shares that Compounder Fund will soon receive and we will inform all of you about our decision in due course (keep in mind that there are effectively 49 holdings in Compounder Fund’s portfolio at the moment, not 50). In the meantime, we have a few thoughts on the implications of Tencent’s distribution of its JD.com shares:

- We have no insight on the actual motivation of Tencent’s management behind this distribution. From our vantage point, there are three possible reasons for the move: (1) it is driven by the wishes of the Chinese government to reduce Tencent’s sway in China’s technology sector; (2) it is an isolated manoeuvre by Tencent’s management to unlock value from the company’s JD.com shares after first making the investment more than seven years ago in 2014; and (3) it is the start of a coherent strategy by Tencent’s management to unlock the value of the company’s massive portfolio of investments.

- Implications that come with the first reason: If true, this would be troubling. Tencent could be forced in the future to offload or spin off its investment portfolio in ways that are harmful for its shareholders – for example, Tencent could be pushed to sell a minority investment when its stock price is temporarily depressed. In the “Investing thoughts: Investing in China” section of Compounder Fund’s 2021 third-quarter letter, I discussed the recent flurry of regulatory changes to China’s business landscape and how Jeremy and I can’t tell what the key intention of the Chinese government is behind these changes (one of the possible intentions I brought up is the Chinese government’s desire to consolidate power). Tencent’s distribution of its JD.com shares could be related to the regulatory changes that were discussed in our 2021 third-quarter letter. We will be watching developments with Tencent’s investment portfolio as it could contain clues on how the Chinese government thinks about the country’s large private-sector companies.

- Implications that come with the second reason: If true, then there’s nothing to see here.

- Implications that come with the third reason: If true, we see it as a positive development for our Tencent investment. Large conglomerates often carry a “holding discount,” where the sum of the intrinsic values of each of a conglomerate’s various holdings outweighs the conglomerate’s overall market capitalisation. It’s possible that the market is applying a holding discount to Tencent’s investment portfolio. Coherent attempts by Tencent to unlock the value of its portfolio of investments should do no harm to its core businesses’ growth, in our opinion. So it’s a move that would be neutral at-worst or positive at-best. We like these odds.

- All told, we can’t tell which possible reason is true. There may even be a combination of any two of the reasons in Tencent’s decision to distribute its JD.com shares. We’re adopting a watch-and-learn stance with Tencent. There’s still much to like about its core businesses (WeChat and digital gaming) and relatively nascent businesses (such as cloud computing), and this is why it still has a place in Compounder Fund’s portfolio.

We’re sharing all this information with the public and with the fund’s investors for two reasons. First, we believe deeply in investor education and want Compounder Fund’s return and actions to be a source for people to learn about investing. Second, we believe that this transparency will help investors of Compounder Fund develop comfort with our investing process over time, which is great; in turn, this will also free us from the time-consuming activity of dealing with questions on how we invest, and thus give us more to invest better for our investors.

And here’s an important disclaimer: None of the information or analysis presented is intended to form the basis for any offer or recommendation; they are merely our thoughts that we want to share. Holdings are subject to change at any time.