Compounder Fund: Portfolio Update (October 2021) - 12 Oct 2021

Jeremy and I intend to share frequent but non-scheduled updates on how Compounder Fund’s portfolio looks like. The last time we shared an update on this was for Compounder Fund’s portfolio as of 20 August 2021.

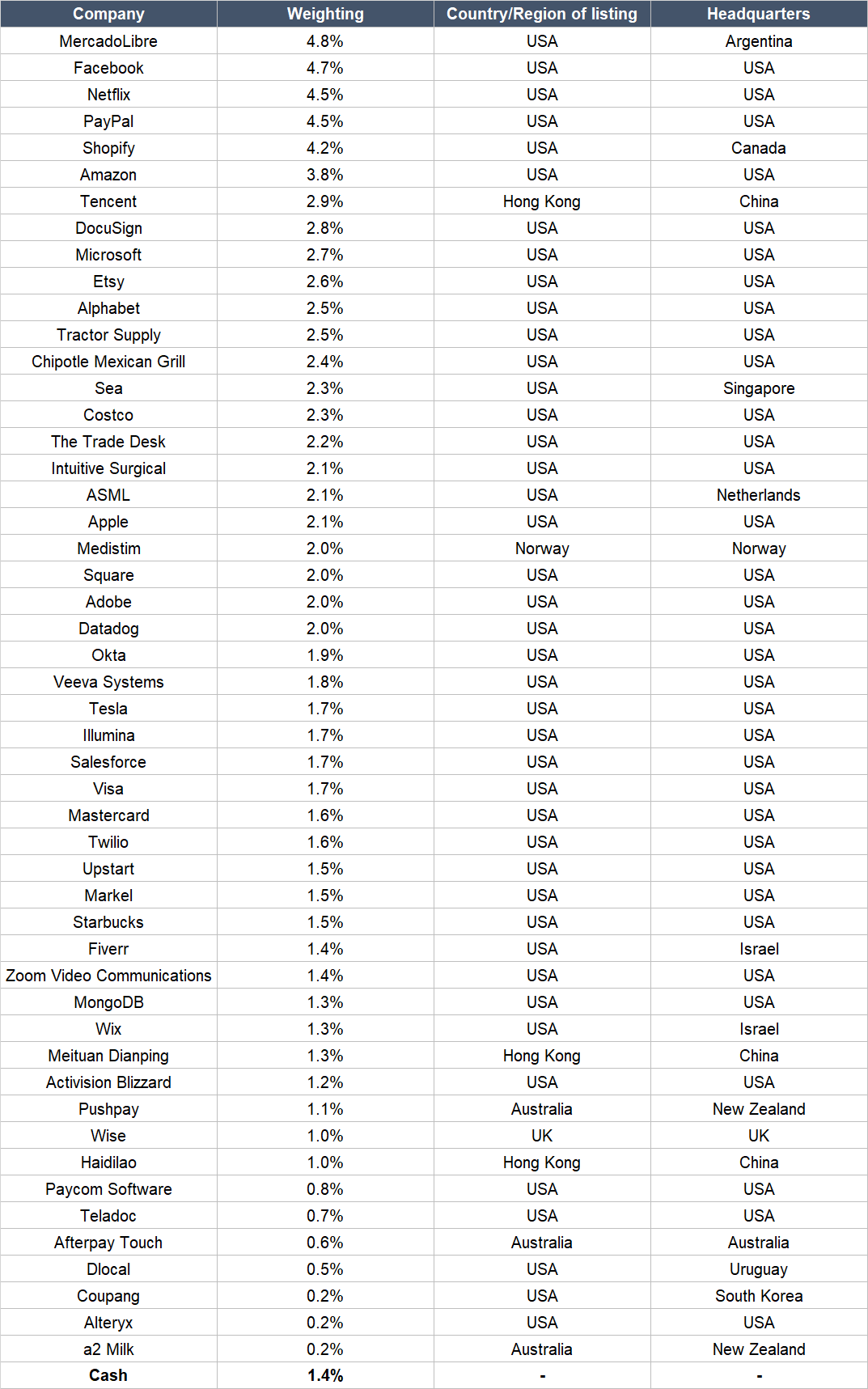

In the update, I shared all 47 holdings in the fund’s portfolio and also mentioned that a new company – Upstart – was added in early-August. As of the date of this update, the portfolio contains the same 48 holdings, plus two new companies. At first glance, this brings the total number of companies in Compounder Fund’s portfolio to 50. As a reminder, Compounder Fund is supposed to have between 30 and 50 companies in its portfolio at any point in time. But two companies in the portfolio – Afterpay and Square – will become one entity soon (we will discuss this development later). So we think it is more appropriate to see Compounder Fund as having 49 holdings instead of 50.

As you know, Compounder Fund is able to accept new subscriptions once every quarter with a dealing date that falls on the first business day of each calendar quarter. In the middle of September 2021, Jeremy and I successfully closed Compounder Fund’s fourth subscription window since its initial offering period (which ended on 13 July 2020).

This new capital was deployed quickly in the days after the last subscription window’s dealing date of 1 October 2021. Jeremy and I invested the new capital in one existing Compounder Fund holding, which is Upstart. The two new companies that we invested in are dLocal and Wise. A few quick words on the new duo:

- Headquartered in Uruguay, dLocal was listed only in June this year. Handling online payments in emerging markets can be a complicated affair as banking penetration rates are low (less than 20% in some cases). Moreover, according to dLocal, “local card, bank transfer-based payment methods, digital wallet, and cash-like payments, such as using Boleto in Brazil or UPI in India, and making payments at Oxxo in Mexico, are the predominant payment methods for end users” in emerging markets. To help global merchants deal with this complexity when operating in these markets, dLocal provides a fully cloud-based software platform for payments (which merchants can access through one direct API) that reaches 30 emerging markets and is connected with more than 600 local payment methods. Through dLocal’s platform, global merchants can safely and efficiently accept and make payments for both cross-border and local transactions in emerging markets. dLocal’s platform appears to have struck a chord with global merchants. From 2019 to the 12 months ended 30 June 2021, the total payment volume processed by dLocal has grown at an astounding annualised rate of 102.5%, from US$1.29 billion to US$3.71 billion. Over the same period, dLocal’s revenue has increased from US$55.3 million to US$164.7 million, which is an equally remarkable growth rate of 107.0% per year. What’s even more impressive is that dLocal has grown this quickly while generating substantial free cash flow. In 2019 and 2020, dLocal produced free cash flow margins (free cash flow as a percentage of revenue) of 52.5% and 81.2%, respectively. There’s still plenty of room for dLocal to grow, with more than US$1.2 trillion in total e-commerce-related payment volume taking place in 2020 in most of the countries the company operates in.

- Wise is another incredibly customer-centric company in Compounder Fund’s portfolio. The company, which is based in the UK, has its core business in facilitating cross-border money transfers. Wise’s customer-centricity can be found in its mission to (emphasis is ours) “build money without borders: instant, convenient, transparent, and eventually free.” International money transfer is a huge market, with £9 trillion being moved by SMBs (small/medium businesses) and individuals in 2020. But the user experience is poor. According to Wise’s July 2021 IPO prospectus, consumers are typically charged a fee of 3% to 7% by traditional banks and the vast majority of consumers don’t even know how much they’re actually paying. Moreover, the transfers are slow, taking between two to five business days in general. In contrast, Wise charges a much lower fee of around 0.7%, is transparent with its fees, and moves money really quickly (38% of Wise money transfers arrive instantly, and 83% of transfers arrive within 24 hours). With a drastically better product, it’s no surprise that Wise has experienced strong growth in its business. The company’s number of active customers grew by 82% from 3.3 million in FY2019 (financial year ended 31 March 2019) to 6.0 million in FY2021, with the volume of money transfers doubling from £27.1 billion to £54.4 billion over the same period. This has helped to propel Wise’s excellent revenue growth of 53.8% per year from £177.9 million in FY2019 to £421.0 million in FY2021. Wise has not just grown quickly – it has done so while consistently generating profits and free cash flow. From FY2019 to FY2021, Wise’s profit and free cash flow grew at impressive annual rates of 73.2% (from £10.3 million to £30.9 million) and 524.8% (from £2.9 million to £113.2 million), respectively.

In Compounder Fund’s Owner’s Manual, we mentioned that “if Compounder Fund receives new capital from investors, our preference when deploying the capital is to add to our winners and/or invest in new ideas.” Upstart’s share price had increased by 46% from our first purchase to the time we deployed our new capital in the latest subscription window. But this is not why we think Upstart has been a winner. The company is a winner because its business performance has been brilliant over the longer term as well as in recent quarters. You can find out more about Upstart’s business performance in our investment thesis for the company. Here’s how Compounder Fund’s portfolio looks like as of 10 October 2021:

When we first invested in Upstart, it had a weighting of only 0.6% in Compounder Fund’s portfolio. We wrote in our thesis that “we appreciate all the strengths we see in Upstart’s business, but our enthusiasm is currently tempered by the company’s high valuation and the fact that the company’s AI models have yet to prove itself in a prolonged recession for the US economy.” Our concerns on Upstart’s valuation and AI models remain. But we still decided to increase our allocation to Upstart because we wanted more exposure to a company that is not just growing rapidly, but doing so while generating healthy profit and free cash flow margins. As of 10 October 2021, Upstart makes up 1.5% of Compounder Fund’s portfolio, which can still be considered to be a small position.

Coming to Afterpay and Square, the two companies announced in August 2021 that the latter would be acquiring the former. Square would be buying Afterpay in its entirety and it would pay for each Afterpay share with 0.375 Square shares. Based on Square’s share price when the acquisition was announced, Afterpay was valued at A$39 billion (US$29 billion). The deal is expected to be completed in the first quarter of 2022.

Square’s announcement to acquire Afterpay surprised us. We think Afterpay is a company with tremendous room for growth (see our investment thesis), so we’re disappointed that we can no longer directly participate in its future developments once it becomes a part of Square. But there are aspects of the deal that we do like:

- First, we think acquiring Afterpay makes great strategic sense for Square. Square’s current business has millions of merchants in its Seller Ecosystem (we have a detailed description of Square’s business in our investment thesis on the company) and more than 70 million consumers in its Cash App ecosystem. But there’s so far no connective tissue that can bind and strengthen both ecosystems. This is where Afterpay comes into the picture. Afterpay’s core BNPL (buy now, pay later) service, which also includes merchant discovery functions, can be directly integrated into Cash App. This improves Cash App’s consumer engagement. Meanwhile, Square’s Seller Ecosystem becomes even more attractive to merchants with the addition of a BNPL function that already has 16 million active users (number of active Afterpay users as of 30 June 2021).

- Second, Afterpay’s economic structure could potentially improve by joining Square’s family. Currently, Square’s Cash App enables consumers to store money. When Afterpay is integrated with Square, Square could potentially allow consumers to pay for their purchases with Afterpay directly with the money they’ve stored in Cash App and bypass existing payment rails altogether, leading to better profit margins for Afterpay.

- Third, Afterpay’s co-founders and current co-CEOs – Anthony Eisen and Nick Molnar – will join Square and continue running Afterpay’s business when the acquisition is completed. In our Afterpay thesis, we said that we “rate Eisen and Molnar highly when it comes to execution and innovation.” So we’re pleased that Afterpay will continue to have them leading the charge. We also think it’s a positive signal on the growth prospects of Square + Afterpay that Eisen and Molnar accepted an all-stock offer from Square and will both be joining the company.

Our current intention – which is subject to change depending on developments with Square/Afterpay and the stock market in general – is for Compounder Fund to hold onto its Afterpay shares and have them be automatically converted into Square shares once the acquisition is completed. In this way, we save on unnecessary trading fees. We’re eager to observe the growth of the combined entity and are happy to see Square’s weighting in Compounder Fund increase because of its acquisition of Afterpay.

We’re sharing all this information with the public and with the fund’s investors for two reasons. First, we believe deeply in investor education and want Compounder Fund’s return and actions to be a source for people to learn about investing. Second, we believe that this transparency will help investors of Compounder Fund develop comfort with our investing process over time, which is great; in turn, this will also free us from the time-consuming activity of dealing with questions on how we invest, and thus give us more to invest better for our investors.

And here’s an important disclaimer: None of the information or analysis presented is intended to form the basis for any offer or recommendation; they are merely our thoughts that we want to share. Holdings are subject to change at any time.