FAQ

Am I the right type of investor for Compounder Fund?

From a regulatory standpoint, Compounder Fund can only accept accredited investors. Accredited investors are individuals who meet any of the following criteria: (1) net assets of at least S$2 million, of which a maximum of S$1 million can come from the primary residence; (2) an annual income of at least S$300,000; and (3) net financial assets of at least S$1 million.

From an investing standpoint, the right investor for Compounder Fund will be someone who:

- Believes in the stock market’s ability to create long-term wealth

- Can handle stock market volatility (declines of 50% are not uncommon) in a calm manner

- Can invest for at least five years

- Understands that the stock market can make them rich, with patience

- Believes that a company’s business performance over the long run governs its stock price movement

- Believes in Compounder Fund’s mission

We understand that not everyone fits the bill above. But we hope we can help change some minds here. If you…

- Don’t believe in the stock market’s ability to create long-term wealth, note that stocks from developed economies have returned 8.2% per year for more than 100 years from 1900 to 2018, while stocks from emerging economies have gained 7.2% annually.

- Cannot handle stock market volatility well, know that even the biggest winners in the stock market have been incredibly volatile, as you’ll see later.

- Cannot invest for at least five years, then you really shouldn’t! To lower the risk of investing, we think that investors should only be investing money that they know they wouldn’t need for at least five years.

- Expect the stock market to make you rich overnight, then know that the magic of compounding takes time to work.

- Don’t believe that a company’s business performance over the long run governs its stock price movement, then know that from 1965 to 2018, Berkshire Hathaway’s book value per share (assets per share less liabilities per share) grew by 18.7% annually; over the same period, its stock price increased by 20.5% per year.

- Don’t believe in Compounder Fund’s mission, that is perfectly okay too! We just want to do our part to grow the wealth of Singaporeans and enrich society.

What does Compounder Fund invest in?

We will invest Compounder Fund’s capital solely in stocks. Over the past 120 years, stocks have outperformed bonds, bills, currency, and inflation around the world, according to Credit Suisse Research Institute’s Credit Suisse Global Investment Returns Yearbook 2020. The stocks we’re investing in for Compounder Fund can come from any stock market in the world (although we will be focusing on stock markets that are in developed economies) as well as from any economic sector. We may also invest in exchange-traded funds (ETFs) that are made up of stocks with similar traits that we’re looking for in individual stocks.

Compounder Fund is a long-only investment fund, meaning we are buying stocks with the view that they will appreciate in price over time.

Here are the constraints we have placed on Compounder Fund:

- The fund’s portfolio will hold 30 to 50 stocks/ETFs at any point in time

- No individual stock or ETF will make up more than 20% of the fund’s AUM

- The fund will not be shorting (to short is to invest with the view that a stock’s price will fall over time)

- The fund will not hedge its positions or use any form of currency hedging

- The fund will not use leverage in any form

- The fund will not invest in financial derivatives

- The fund will have no geographical concentration limit, meaning that up to 100% of Compounder Fund’s capital can be invested in stocks listed in one country’s stock market

- The fund will have no sector concentration limit, meaning that up to 100% of Compounder Fund’s capital can be invested in stocks from just one economic sector

Simply put, Compounder Fund is an investment fund that will be investing only in stocks and/or ETFs around the world. We harbour no illusion that we have any skill in hedging, or currency movements, or leveraging, or financial derivatives. So we do not want to engage in any of these activities and incur unnecessary costs (yes, these activities all cost money!) for Compounder Fund’s investors.

Is now a good time to invest in stocks?

It’s nearly always a good time to invest in stocks if you have a long-term perspective (and we do!). According to the Credit Suisse Global Investment Returns Yearbook 2019, stocks from developed economies have returned 8.2% per year for more than 100 years from 1900 to 2018, while stocks from emerging economies have gained 7.2% annually. Let’s not forget that those 118 years included two world wars! Download the Credit Suisse report here and look at that beautiful chart at the bottom of page 11 – it shows the majesty of long-term investing. If we run dry of investment ideas for Compounder Fund, we will not allow new subscriptions or top-ups, and if needed, we will return capital to investors.

We are long-term optimists on the stock market. There are 7.8 billion individuals in our globe today, and the vast majority of people will wake up every morning wanting to improve the world and their own lot in life. This is ultimately what fuels the global economy and financial markets. Miscreants and Mother Nature will occasionally wreak havoc. But we have faith in the collective positivity of humankind. If there’s any mess, humanity can clean it up. To us, investing in stocks is ultimately the same as having faith in the long-term positivity of humankind. We will be long-term optimistic on stocks so long as we continue to have this faith – the exception is when there are ridiculously high valuations in stocks, such as Japan in the late 1980s/early 1990s when stocks there were worth nearly 100 times their 10-year average inflation-adjusted earnings.

What kind of returns can I get with Compounder Fund?

There are no guarantees in the financial markets – we only deal with probabilities. We cannot guarantee any return, but our goal is to deliver a long-term annual return of 12% or more, net of all fees. But a word of caution is necessary here: The stock market is volatile. If the market falls, we fully expect Compounder Fund to decline by a similar magnitude or more. But we believe in the long-term potential of the stock market. Historically, it has been the best asset-class in generating wealth. And by finding great companies – what we call Compounders – we believe we can do very well for Compounder Fund’s investors over a multi-year period.

Is 12% too aggressive?

We think it’s achievable (based on experience and history) and we’re happy to tell you why we think so. And remember, we’re not going to borrow money to invest.

Is there a lock-up period?

Yes. We have a soft lock-up period of three years. A small early withdrawal penalty (3% of the withdrawn capital in the first year, 2% in the second year, and 1% in the third year) will be charged to investors who wish to redeem their capital before the soft lock-up period ends. The penalty fee goes to Compounder Fund. We can apply discretion on a case-by-case basis to waive the early withdrawal penalty.

The reason for implementing a soft lock-up is because long-term investing is the crux of Compounder Fund’s investment philosophy. Moving your investments in and out of a fund can severely impact your returns. The lock-up period serves to promote a long-term investing mindset.

Peter Lynch is the legendary manager of Fidelity Magellan Fund in the US. Lynch managed the fund from 1977 to 1990 and posted an incredible annual return of 29%, nearly double what the S&P 500 achieved in the same period. But amazingly, the average investor in Lynch’s fund earned only 7% per year. That’s because the investors chased the fund when it was performing well, and bailed when it temporarily declined.

Having a good fund manager is only one part of the puzzle – staying invested with the manager completes the puzzle. As such, only invest in Compounder Fund with money you do not need for at least five years. A successful fund requires like-minded investors.

Compounder Fund has an early withdrawal penalty for the first three years. As an investor, how do I reap the target annualised return of at least 12% with my capital “locked up” for three years?

Let’s talk about our 12% target first.

We’re targeting an annual return of at least 12% over the long run (a five to seven-year period, or longer) for Compounder Fund’s investors, net of all fees. A 12% annual return will double your money every six years. It will also likely be a market-beating return. From January 1970 to February 2020, the MSCI World Index – a collection of stocks across 23 developed markets – produced an annual return of 8.6% in US-dollar terms, including dividends.

It’s important to note that the target annual return of at least 12% does not mean that we’re trying to earn 12% every year – it means that over the long run, the starting value and ending value of Compounder Fund for a particular measurement period, after deduction of all fees, will work out to be at least 12% annualised.

Now, let’s discuss how you can reap the return.

If we’re successful in meeting our 12% target for Compounder Fund, it means that the value of your investment will also have grown when you eventually do decide to redeem from the fund. That’s how you can reap your return.

Aren’t stocks risky?

Stocks are very risky if you (1) invest in companies you don’t understand, (2) invest with borrowed money, and (3) invest with money you know you need within a short time frame. Stocks are volatile, meaning they move up and down fiercely over short timeframes, sometimes without good reason. But risk to us is the permanent or near-permanent loss of capital; we describe how we mitigate investing risk in our Owner’s Manual.

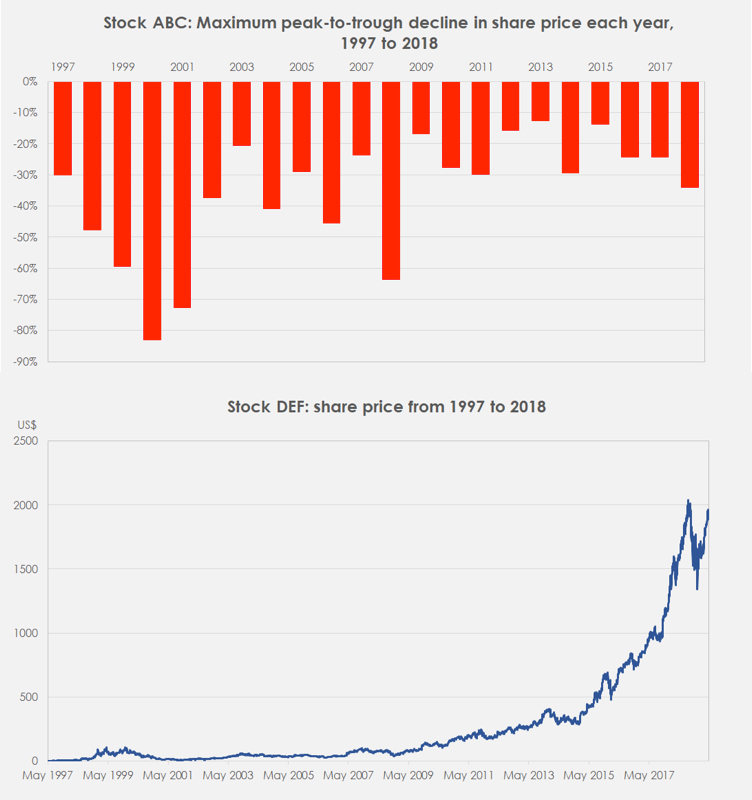

Even the biggest winners in the stock market have gone through severe periods of volatility. Let’s take a quiz. Stock ABC and Stock DEF both got listed in 1997. From 1997 to 2018, the top-to-bottom decline for ABC in each year ranged from 12.6% to 83.0%, meaning to say that ABC had experienced a double-digit peak-to-trough fall every year. Over the same period, DEF saw its stock price climb from $1.96 to $1,501.97, for an astonishing gain of over 76,000%. With this information, would you choose to invest in ABC or DEF if you could take a time machine and go back to 1997?

Source: S&P Global Market Intelligence

Well, it’s a trick quiz, because ABC and DEF are the same company – they are Amazon.com! This goes to show how critical it is that investors have the stomach to withstand volatility, enroute to big long-term gains. Peter Lynch once said that in investing, “the key organ in your body is your stomach, it’s not your brain.”

If we eschew the use of borrowed money, and if we only invest with long-term capital, we can ensure that we will never become forced-sellers in the stock market. And if we never have to become forced sellers, we have the luxury to ride out volatility and profit from the long-term values generated by growing businesses.

Why are stocks volatile?

When the late Hyman Minsky was alive, he was an obscure economist. But he became more well-known after the Great Financial Crisis of 2007-09. That’s because he had a framework for understanding why economies go through boom-bust cycles. According to Minsky, stability is destabilising. If an economy does not suffer a recession for a long time, people feel safe. This causes people to take on more risk, such as borrowing more, which leads to the system becoming fragile. Literally, the lack of a recession plants the seed for a recession.

Minsky was talking about economies, but his ideas can be applied to stocks too. Let’s assume that stocks are guaranteed to grow by 9% per year. What would happen? The logical response from investors would be to keep buying them, till the point where stocks become too expensive to continue returning 9%, or where the system becomes too fragile to handle shocks. If you knew stocks were guaranteed to produce a 9% annual return, why would you bother to earn meagre interest from bank deposits? In such a scenario, investors would pay up for stocks till their returns match those of ultra-safe bank deposits. But there are no guarantees in the world. Bad things happen from time to time. And when stocks are priced for perfection, any whiff of bad news will lead to tumbling prices.

Wharton finance professor Jeremy Siegel once said, “volatility scares enough people out of the market to generate superior returns for those who stay in.” Don’t be scared off by volatility!

Can you run away with my money?

No, we can’t. In Compounder Fund’s set-up, investors’ capital are held in the fund’s bank account with OCBC; the shares the fund invests in are bought through Interactive Brokers and are custodised with Interactive Brokers; the fund’s returns and subscriptions/redemptions are handled by the third-party fund administrator NAV Fund Administration Group; and the fund is audited by third-party auditor Baker Tilly.

When investors place capital with Compounder Fund, the capital goes to the fund’s OCBC bank account. Any use of Compounder Fund’s capital is triggered by NAV Fund Administration Group. When an investor redeems capital from Compounder Fund, a cheque is written in the investor’s name.

Compounder Fund is managed under Galilee Investment Management Pte Ltd. Galilee Investment Management is a fund management company with a Capital Markets Services Licence from the Monetary Authority of Singapore (MAS).

How do you handle currency risks given that Compounder Fund invests in global stocks?

The short answer is that we do not manage currency risks. We let the currency movements take care of themselves. We believe that the share price gains from growing companies will triumph over any currency depreciation. We also aim to invest mostly in stock markets that are based in countries with relatively stable political regimes and respect for the rule of law. So we think that the risk of severe currency depreciation – against the Singapore dollar – will be low. We want to only partake in financial activities that we understand well. We understand stocks, but we’re not experts in currencies. So, hedging currencies will be a detractor to Compounder Fund’s long-run performance.

How are your interests aligned with investors in Compounder Fund?

First, we – the co-founders of Compounder Fund – are invested in the fund together with our families.

Second, the management fee we charge at the Compounder Fund will fall as our assets under management (AUM) grows. Under this model, the bulk of our remuneration will come from Compounder Fund’s performance fee. And this performance fee is designed to (1) kick in only if Compounder Fund can generate a compound annual return of at least 6% for its investors, and (2) be charged only on the excess return over this 6% hurdle. Let’s not forget, we’ll be dropping the performance fee too as Compounder Fund’s AUM grows. See here for a detailed discussion of our fees. Funds that charge a performance fee without a hurdle will still earn the performance fee even if they generate poor annual returns of say, just 1%.

Third, Compounder Fund has no sales charges, no subscription fees, and no redemption fees. In other words, we earn only from the fund’s management fee and performance fee – and remember, the bulk of our remuneration is designed to come from Compounder Fund’s performance fee!

What is the worst thing that can happen?

The worst case scenario is Compounder Fund’s value falling to zero. It’s a theoretical possibility that all the companies in Compounder Fund’s portfolio can go bankrupt. But is it probable? No it isn’t.

The worst thing that can happen to an investor is if he/she invests with a short-term mindset, trying to jump in and out of the market. Compounding requires time to work. Give yourself the time for compounding to work for you.

Can I invest more money in Compounder Fund over time?

Yes you can. Compounder Fund can take in quarterly subscriptions for now. The very first subscription has to take place at the Singapore-dollar-equivalent of US$100,000. But subsequent subscriptions can take place at a minimum of S$10,000 (this is Singapore-dollars) without any charges.

We intend for Compounder Fund to be nearly fully invested at all times, so when additional capital comes in, it will be put to work. If we run dry of investment ideas for Compounder Fund, we will not allow new subscriptions or top-ups, and if needed, we will return capital to investors.

What kind of communication can I expect from you?

You will get an official monthly report from Compounder Fund’s fund administrator, Crowe Horwath First Trust, which will show you the total amount of your investment in terms of the number of units and the NAV (net asset value) per unit.

As the manager of Compounder Fund, we intend to provide the following on Compounder Fund’s website:

- A quarterly investors’ letter

- Monthly updates on the value/performance of Compounder Fund

- All of Compounder Fund’s holdings

- Our investment theses for the fund’s holdings

- Commentary on how we build and maintain the portfolio

All the above materials will be available to the general public as well. In our communications, we’ll generally steer clear of commentary on politics, the economy, and the stock market. We think these topics are a distraction for investors from the key drivers of Compounder Fund’s performance – the long run business performances of the companies it owns shares of. Besides, we can’t forecast these things accurately and we don’t think anyone can, either. We intend for our communications to have a focus on the business developments of the companies the fund owns.

(And just to be clear, we will not be revealing Compounder Fund’s trades before they are executed.)