Compounder Fund: Square Investment Thesis - 07 Oct 2020

Data as of 5 October 2020

Square (NYSE: SQ) is one of the 40 companies in Compounder Fund’s initial portfolio. This article describes our investment thesis for the company.

Company description

Square was founded in 2009 by Jim McKelvey and Jack Dorsey to enable any business to accept card payments. The company started with a little white square-shaped device which can be attached to a smartphone. This device, shown below, enabled merchants (Square calls them sellers) to accept card payments easily.

Source: Wikimedia Commons

Today, Square provides a comprehensive suite of services and software for sellers to accept payments and run their businesses; Square calls these its Seller Ecosystem. The company also has a mobile wallet for individuals called Cash App (unfortunately it is not available in Singapore yet) that enables users to access a range of financial services; these services are known as the Cash App Ecosystem.

Seller Ecosystem

The Seller Ecosystem consists of over 30 distinct software, hardware, and financial services products for sellers. Square monetises these products through a combination of transaction, subscription, and service fees.

The software products are cloud-based and are designed to be self-serve and intuitive for fast and easy set-up. They consist of:

- Square Point of Sale: A general-purpose point of sales software that can be downloaded to an iOS or Android mobile device.

- Square Virtual Terminal: A web-based point of sale software for use on computers.

- Square Appointments: Helps sellers in the services industry manage bookings, retail sales, invoices and payments. It is also integrated with Square Assistant, an artificial intelligence-enabled automated messaging tool that responds to buyers directly, saving sellers time.

- Square for Retail: Provides support for retailers in inventory management; accounting for cost of goods; customer profiling; vendor management and more.

- Square for Restaurants: Helps full-service restaurants with revenue and cost reporting as well as to manage tables, orders, courses, and tickets.

- Square Invoices: A digital invoicing solution that also accepts online payments.

- Square Online Store: Helps sellers to easily design and build their own online stores as well as sell on Instagram and Facebook.

- Square Loyalty, Marketing, and Gift Cards: Help sellers engage with their buyers through integrated loyalty programs and targeted marketing campaigns that are informed by combining customer- and transaction-data.

- Square Dashboard: Provides sellers with real-time data and insights about their business.

- Developer platform: Square provides APIs (application programming interfaces) and SDKs (software development kits) to enable external developers to build software that integrates with Square’s ecosystem.

Square’s hardware products in the Seller Ecosystem enable sellers to accept all major forms of card payments including magnetic stripe via a swipe, chip, or NFC (near-field communication) via a tap. Some of Square’s hardware products are:

- Square Stand: A device that enables an Apple iPad to become a payment terminal or full point of sale solution.

- Square Register: All-in-one device combining Square’s hardware, point of sale software, and payments technology.

- Square Terminal: A portable payments device that enables payments to be made anywhere in a store.

Lastly, there are financial services within the Seller Ecosystem. These consist of:

- Managed Payments: Sellers pay a transaction fee for the Managed Payments offering which include next day settlements, payment dispute management, data security, and PCI (Payment Card Industry) compliance. Sellers can onboard to Managed Payments in minutes and once onboarded, can accept payments from customers in person or online.

- Instant Transfer: For a 1.5% fee, sellers can receive funds from their payments instantly or later on the same day.

- Square Card: A free business prepaid debit card that enables sellers to spend their proceeds as soon as they make a sale. Proceeds from a sale go immediately and automatically into a seller’s Square stored balance and this money can be spent with the Square Card or withdrawn from an ATM. Square earns interchange fees when sellers make purchases with Square Card.

- Square Capital: Through a partnership with an industrial bank, Square facilitates loans to qualified Square sellers.

- Square Payroll: Makes it easier for sellers to hire, onboard, and offer benefits to employees, as well as pay wages and taxes.

Cash App Ecosystem

Cash App is offered only in the USA and in the UK. Here are the services that Cash App offers and how Square monetises them:

- Storing, sending, and receiving funds: Individuals can set up a Cash App account and engage in peer-to-peer funds transfer with other users of Cash App. Cash App users can also apply for a free Cash Card, which is a debit card that is linked to a customer’s Cash App balance. Cash App users can store money in their accounts by (1) receiving funds from other Cash App users, (2) transferring money from a bank account, and/or (3) depositing money directly from their paycheck if they have a Cash Card. Funds in a Cash App account can be sent to other Cash App users; spent with Cash Card in any location that accepts card payments; withdrawn from an ATM using Cash Card; and transferred to a bank account. It takes three to five days for a free transfer from Cash App to a bank account, but Square charges a fee for an instant transfer.

- Spending: Individuals can spend money on their Cash App by using the Cash Card. Square earns interchange fees when individuals use the Cash Card to make purchases. Cash Card also offers users a Cash Boost instant rewards program at certain businesses.

- Investing: Through Cash App, individuals can invest in Bitcoin as well as US-listed stocks and exchange-traded funds using their funds in Cash App or from a linked debit card.

Business and revenue breakdown

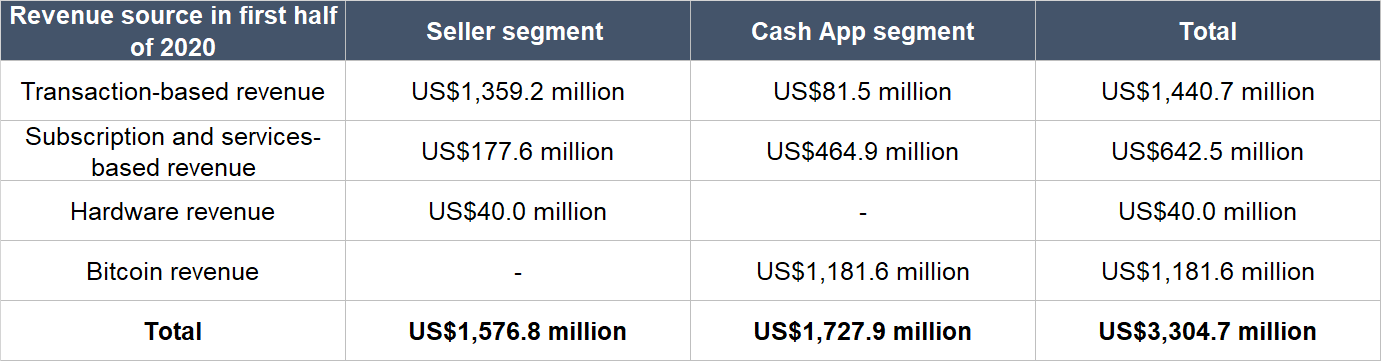

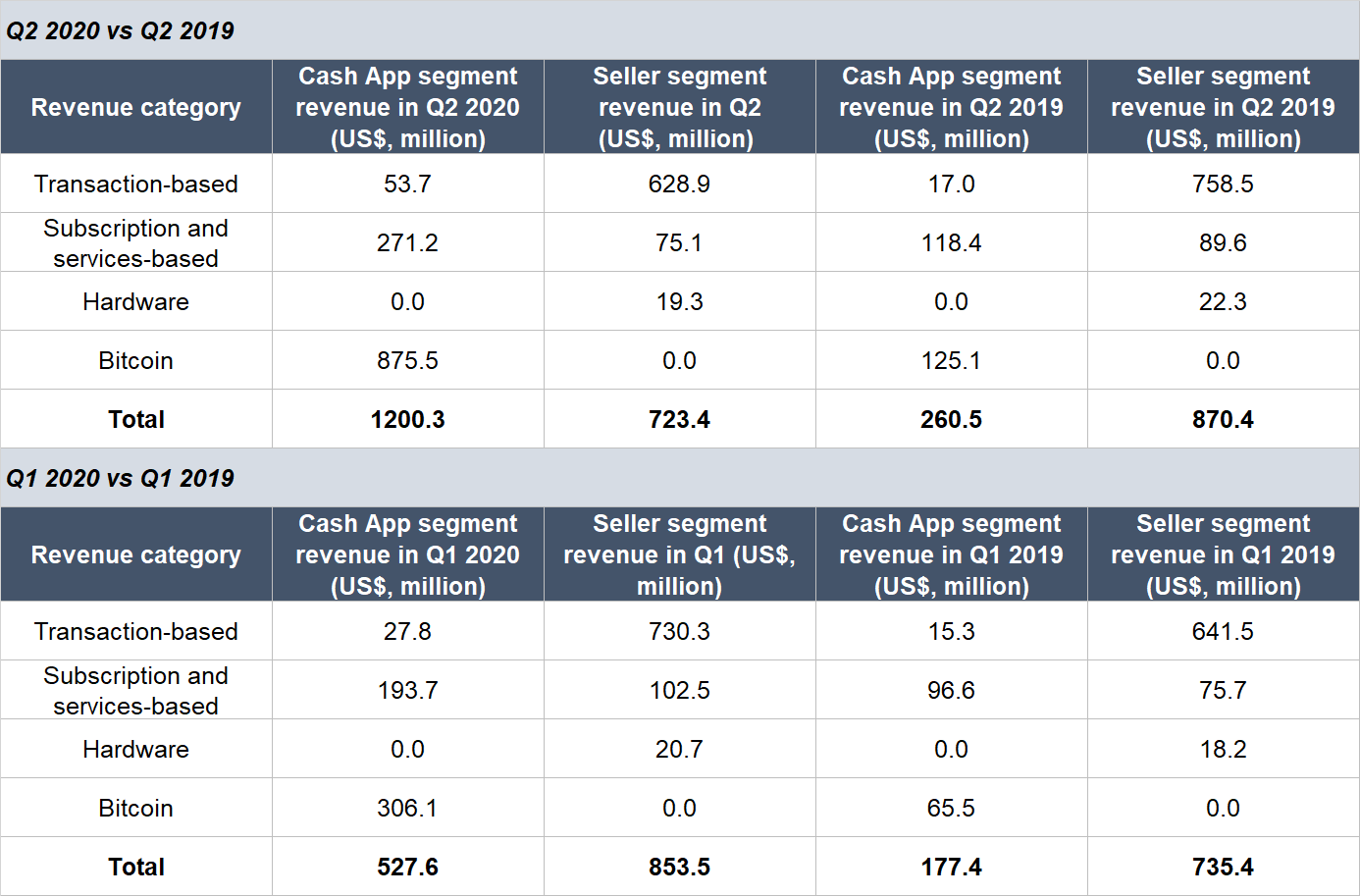

In the second quarter of 2020, Square began reporting its revenue in two segments: (1) Seller and (2) Cash App. The first segment reflects the Seller Ecosystem products while the second segment is for the services within the Cash App Ecosystem. Here’s a segmental breakdown of Square’s revenue in the first half of 2020:

Source: Square quarterly earnings update

Square recognises the entire value of Bitcoin transactions on Cash App as revenue, and then records the cost of acquiring the Bitcoin prior to transferring the cryptocurrency to customers’ accounts as cost of revenue. As Square’s gross profit and gross margin from facilitating bitcoin investments on Cash App are low (US$8.2 million and 1.6% in 2019; and US$24.1 million and 2.0% in the first half of 2020), it’s worth looking at the gross profit contributions from Square’s two business segments:

Source: Square quarterly earnings update

Within each segment, Square also provides a detailed breakdown of the various revenue sources. This is shown in the following table:

Source: Square quarterly earnings update

You can see that from a revenue perspective, Cash App is more important to Square. But if Bitcoin revenue is backed out, then the Seller segment becomes the more prominent business for Square by revenue. Moreover, it’s also clear that the Seller segment generates more gross profit, although the ex-Bitcoin gross profit margin for the Cash App segment is higher compared to the Seller segment.

Square is a USA-centric business, with 96% of its total revenue in the first half of 2020 coming from the country. The remaining 4% are from international markets that include Australia, Canada, Japan, and the UK.

Investment thesis

We have laid out our investment framework in Compounder Fund’s website. We will use the framework to describe our investment thesis for Square.

1. Revenues that are small in relation to a large and/or growing market, or revenues that are large in a fast-growing market

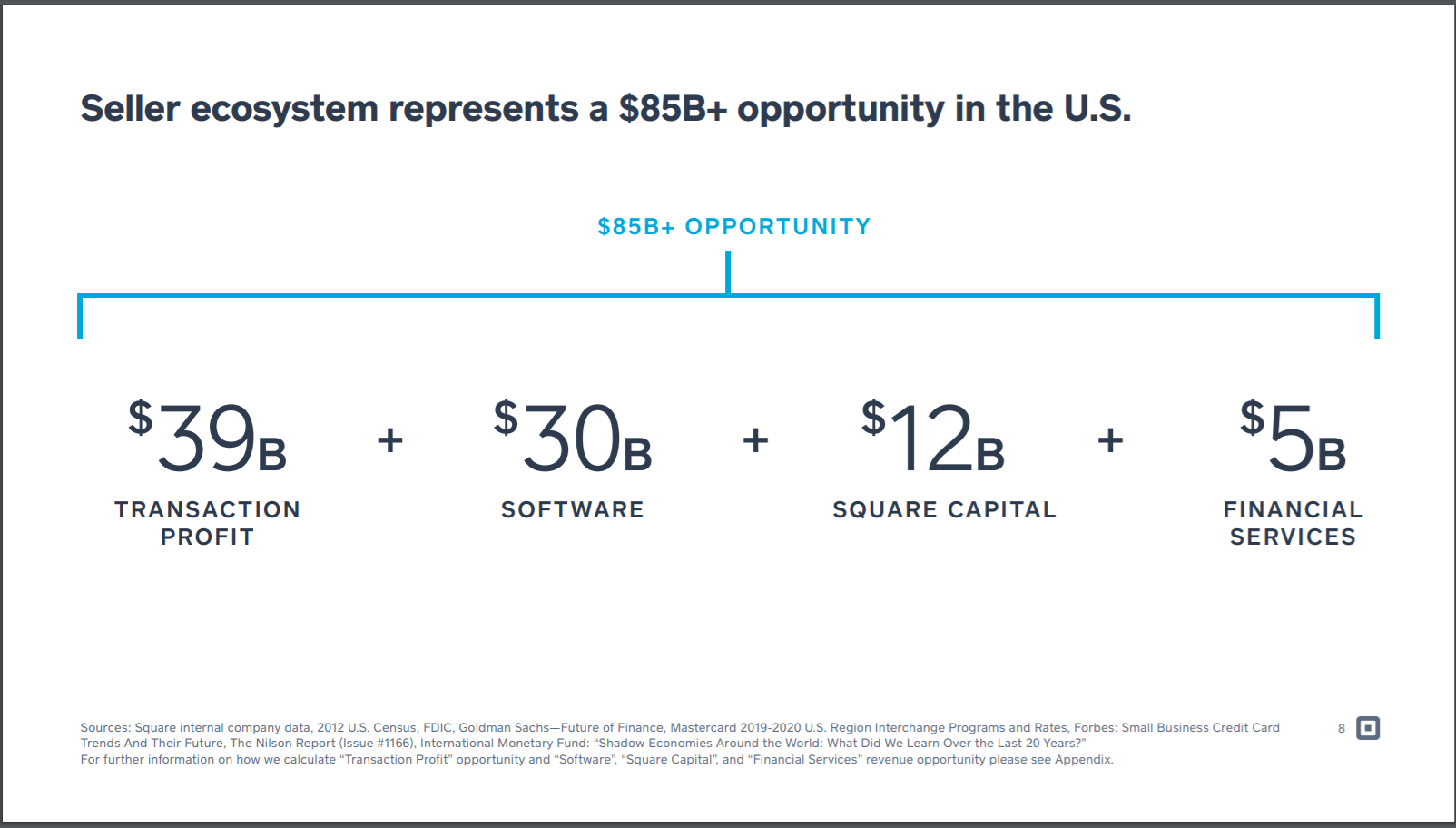

Square believes that its Seller business segment has a US$85 billion market opportunity in the US alone. It can be broken down into the following categories: US$39 billion from transaction profit, US$30 billion from software, US$12 billion from Square Capital, and US$5 billion from financial services.

Source: Square investor presentation

Square calculates the market opportunity for each category in the Seller business segment by applying a typical revenue or take rate to the relevant volume of business activities in each category.

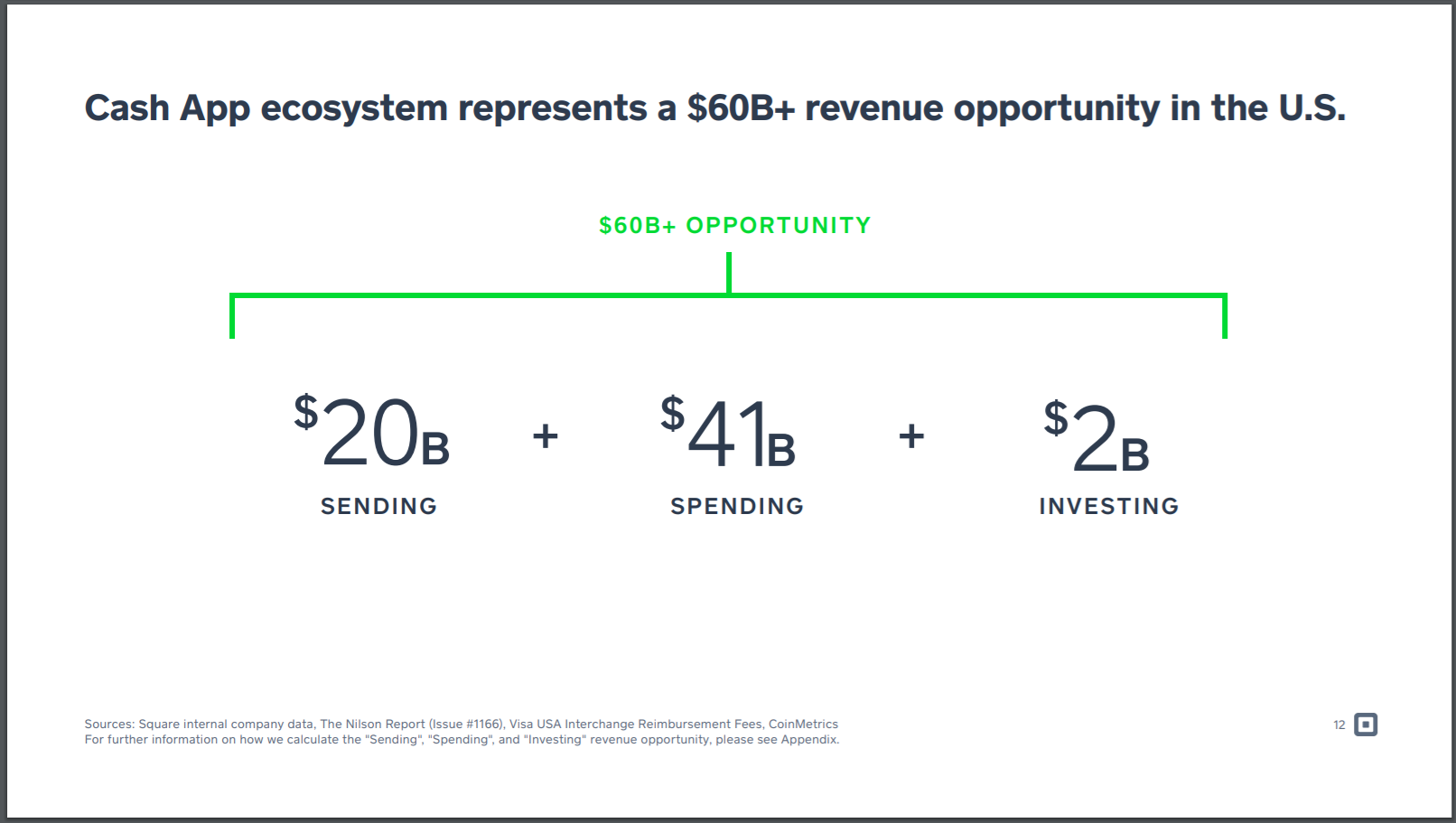

For the Cash App segment, Square believes that it has a market opportunity that’s north of US$60 billion in the USA. This can be broken down into US$20 billion in peer-to-peer sending, US$41 billion in spending, and US$2 billion in investing (the investing market opportunity is gross profit). The figures for the various market opportunities are based on the potential take rate in each activity and the overall volume of transactions that are happening in the USA (US$4 trillion in peer-to-peer sending, US$2 trillion in spending, and US$3 trillion in investing).

Source: Square investor presentation

For perspective, Square’s total revenue in the first half of 2020 was ‘just’ US$3.30 billion. An annualised revenue figure will still only represent a low single-digit percentage of Square’s overall market opportunity of more than US$145 billion in the USA alone.

And we have not even included the potential for international expansion (only 4% of Square’s revenue today comes from outside the USA), new products, and new use cases. Square is highly innovative (more on the company’s innovative spirit later) and its total addressable market has increased over time. For instance, in a May 2018 investor presentation, Square’s market opportunity was given as US$70 billion, significantly lower than what it is today.

2. A strong balance sheet with minimal or a reasonable amount of debt

Square exited the first half of 2020 with US$2.69 billion in cash and short-term investments, and US$1.78 billion in total debt. This is a strong balance sheet with a net cash position of US$910 million.

It helps too that Square had been generating positive free cash flow for a number of years prior to the onset of the COVID-19 pandemic in early-2020 (more on this later).

3. A management team with integrity, capability, and an innovative mindset

On integrity

Square is led by co-founder Jack Dorsey, who has been CEO since the company’s birth in 2009. We appreciate the fact that Dorsey has more than a decade of leadership experience with Square despite his young age of just 43.

The compensation structure for Square’s leadership team demonstrates integrity, in our view. Here are a few points we want to highlight:

- Dorsey’s total compensation in 2017, 2018, and 2019 was just US$2.75 each year (yep, no missing decimals or missing “million”) at his own request. He thinks he’s already well rewarded because of his large ownership stake in Square.

- In 2019, Square’s other key leaders enjoyed total compensation of between US$4.5 million and US$13.1 million each. These look like reasonable sums when compared to the scale of Square’s business. More importantly, the sheer majority of each of their compensation (88% to 93%) came from stock awards and options that typically vest over four years. We tend to frown upon compensation plans that are linked to a company’s short-term stock price movements. In Square’s case, the compensation for its key leaders (except Dorsey) is tied to multi-year changes in the company’s stock price, which in turn is driven by the company’s business performance. So we think this aligns the interests of Square’s leaders with its other shareholders.

And speaking of alignment of interest, Dorsey controlled 59.3 million Square shares as of 31 March 2020. Based on Square’s share price of US$170 on 5 October 2020, Dorsey’s stake is worth more than US$10 billion.

We want to highlight that all of Dorsey’s Square shares are of the Class B variety. Square has two share classes: (1) Class B, which are not traded and hold 10 voting rights per share; and (2) Class A, which are publicly traded and hold just 1 vote per share. As a result, Dorsey controlled 51.3% of Squaare’s voting power (as of 31 March 2020) despite holding only 13.5% of Square’s total shares. A manager having virtually complete control over the company can potentially be bad for shareholders. This concentration of Square’s voting power in the hands of Dorsey means that we need to be comfortable with him at the company’s helm. We are.

Although Dorsey’s personal philanthropic actions are not directly-related to investing, we think they do shine a positive light on the character of Square’s co-founder and CEO. In April this year, Dorsey publicly committed to donating US$1 billion of his Square equity – or 28% of his net worth at that time – to fund global COVID-19 relief efforts and other causes related to girl’s health, education, and universal basic income. He even set up a public Google Sheets to display how much he has given and where the money is being donated to. We applaud Dorsey’s commendable actions on making the world a better place not just through the creation of Square, but also by sharing the immense wealth he has built from the company.

On capability and ability to innovate

We think Jack Dorsey shines brightly in terms of his capability and ability to innovate and there are a few things we would like to discuss.

The first is Dorsey being CEO of not one but two companies. If you use the social messaging service Twitter, then you’ve experienced the work of Dorsey’s other company. He co-founded Twitter in 2006, was ousted in 2008, and returned to lead the company in 2015. Dorsey continues to be the CEO of Twitter. Square was founded In 2009, shortly after Dorsey left Twitter. Running one multibillion-dollar company is already a tough job, much less two publicly listed multibillion-dollar companies (as of 5 October 2010, Twitter and Square have market capitalisations of US$36 billion and US$75 billion, respectively). But we think Dorsey has done great work at Square so far.

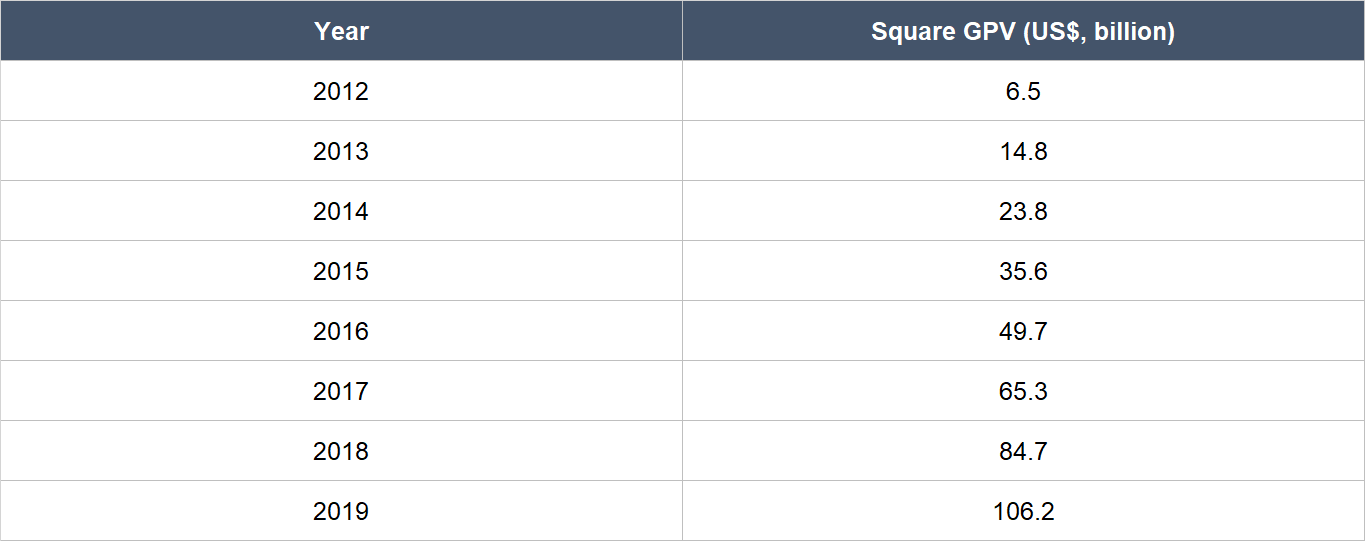

Second is Square’s robust growth in gross payment volume (GPV) processed across its products. In the first half of 2020, more than 68% of Square’s ex-Bitcoin revenue came from transaction-based services. This underscores the importance of the GPV metric for Square. The table below shows Square’s GPV from 2012 to 2019. In that period, GPV grew in each year and expanded at an impressive annual rate of 49%; 2019’s GPV growth was still strong at 25%.

Source: Square annual reports and IPO prospectus

Third, Square has a long track record of introducing successful new products. As already mentioned, Square started its corporate life with a simple square-shaped card reader that could be attached to a mobile device, but there’s so much more to Square’s business today. Here’s a sample of the various products and services Square has launched over time:

- Square Stand in 2013

- Square Cash in November 2013 (now called Cash App)

- Square Capital in May 2014

- Square Register in the fourth quarter of 2017

- Square for Restaurants in the second quarter of 2018

- Square Terminal in the fourth quarter of 2018

- Square Card in the first quarter of 2019

We want to highlight Square Capital and Cash App because we’re excited about their prospects.

Let’s discuss Square Capital first. Through Square Capital, Square offers loans to sellers on its platforms who are under-banked. Square is managing Square Capital’s risks and growth intelligently through two key ways and we credit Dorsey and his team for their innovative thinking. First, Square makes clever use of the real-time payment and point-of-sale data on its sellers to assess loan suitability. Square Capital is able to approve loans at a much faster pace and also make small loans that traditional banks typically avoid. Generally, loan repayment occurs automatically with Square taking a fixed percentage of each of the seller’s card-transactions. The loans are also sized to be less than 20% of a seller’s annual gross payment volume, and thus sellers can typically repay their loans in eight to nine months simply by running their business. Second, funds for Square Capital’s loans are mostly supplied by third-party institutional investors who purchase the loans. Besides lowering risks for Square, this funding arrangement significantly increases the speed at which Square Capital can grow.

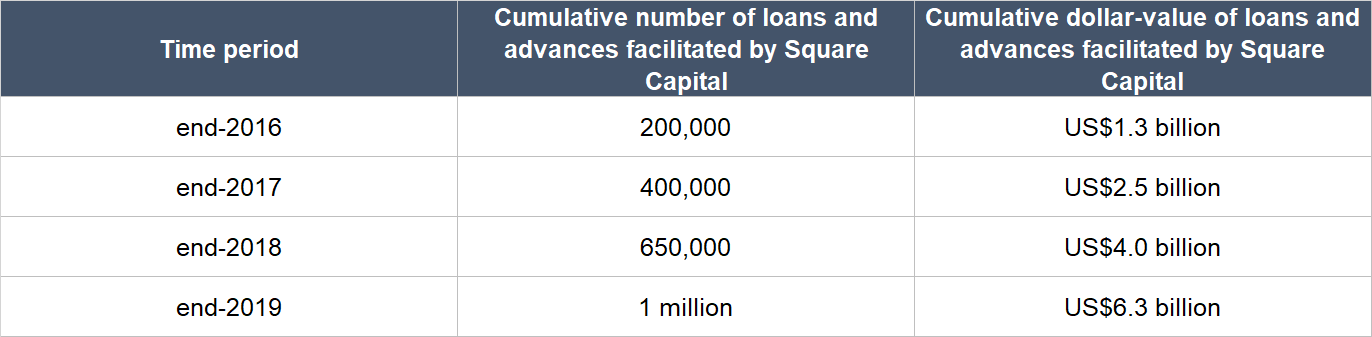

Right now, Square Capital’s market opportunity is US$12 billion. This is based on the USA’s annual volume of small business loans under US$250,000 (US$232 billion as of end-2019) and an estimated revenue rate for small business loans of 4% to 6%. We won’t be surprised to see this market opportunity expand in the future as Square improves Square Capital’s features. For example, Square Capital could facilitate higher loan amounts over time as it understands the loan business better or small businesses that were previously unable to take any bank loans could rely on Square Capital for financing. The following table shows the impressive growth in cumulative loans and advances that Square Capital has facilitated for different points in time since its launch in May 2014:

Source: Square annual reports

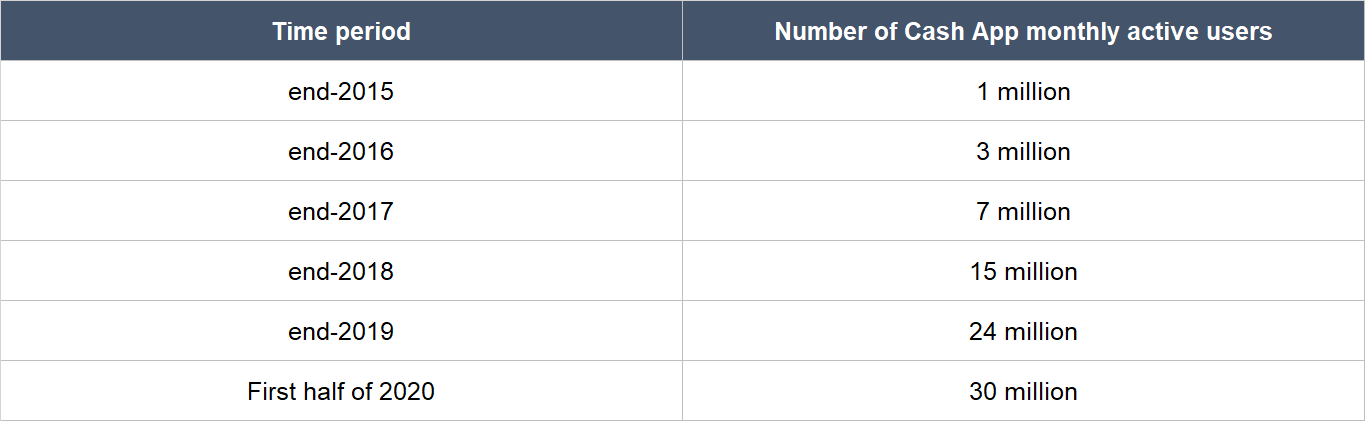

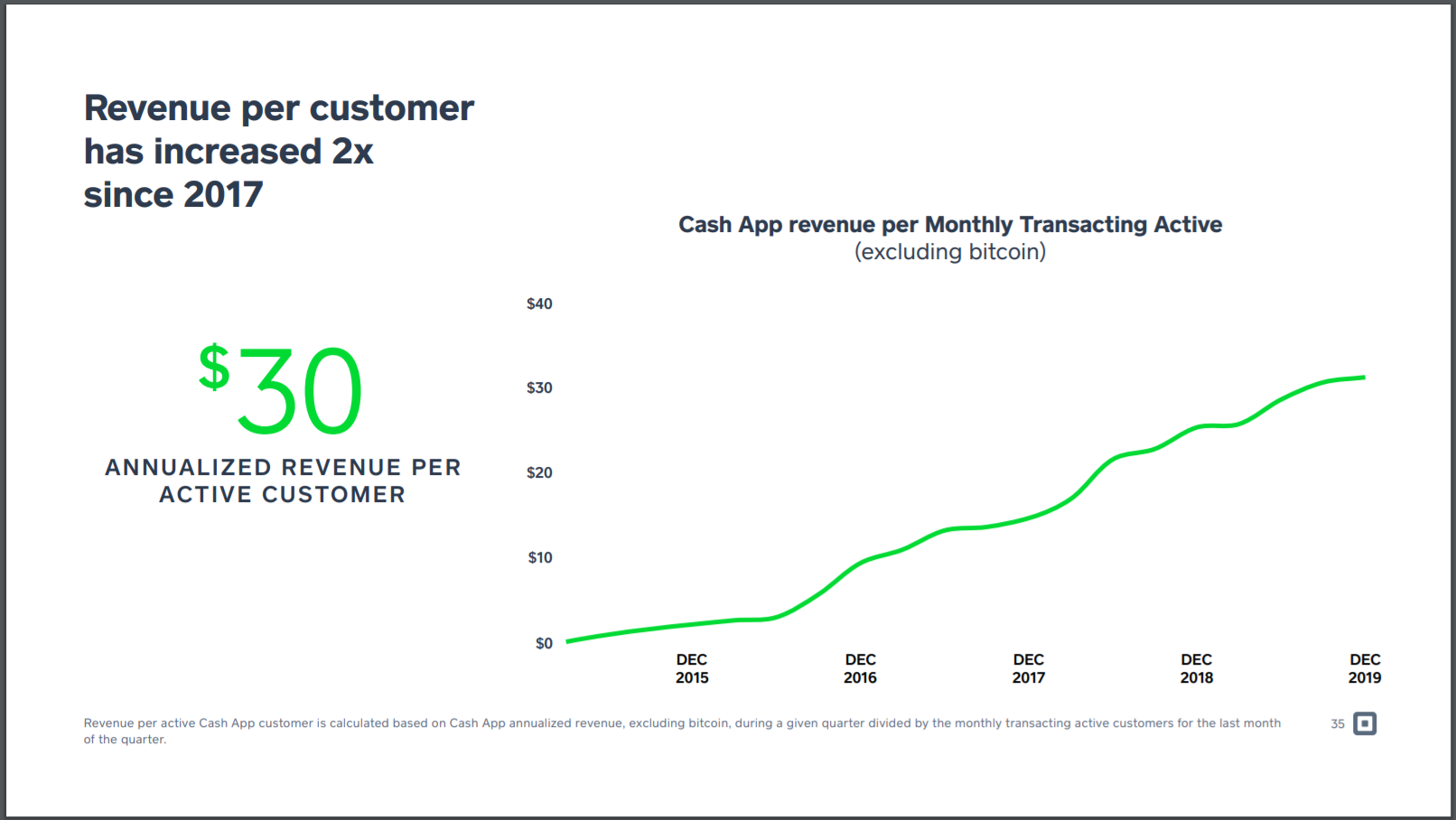

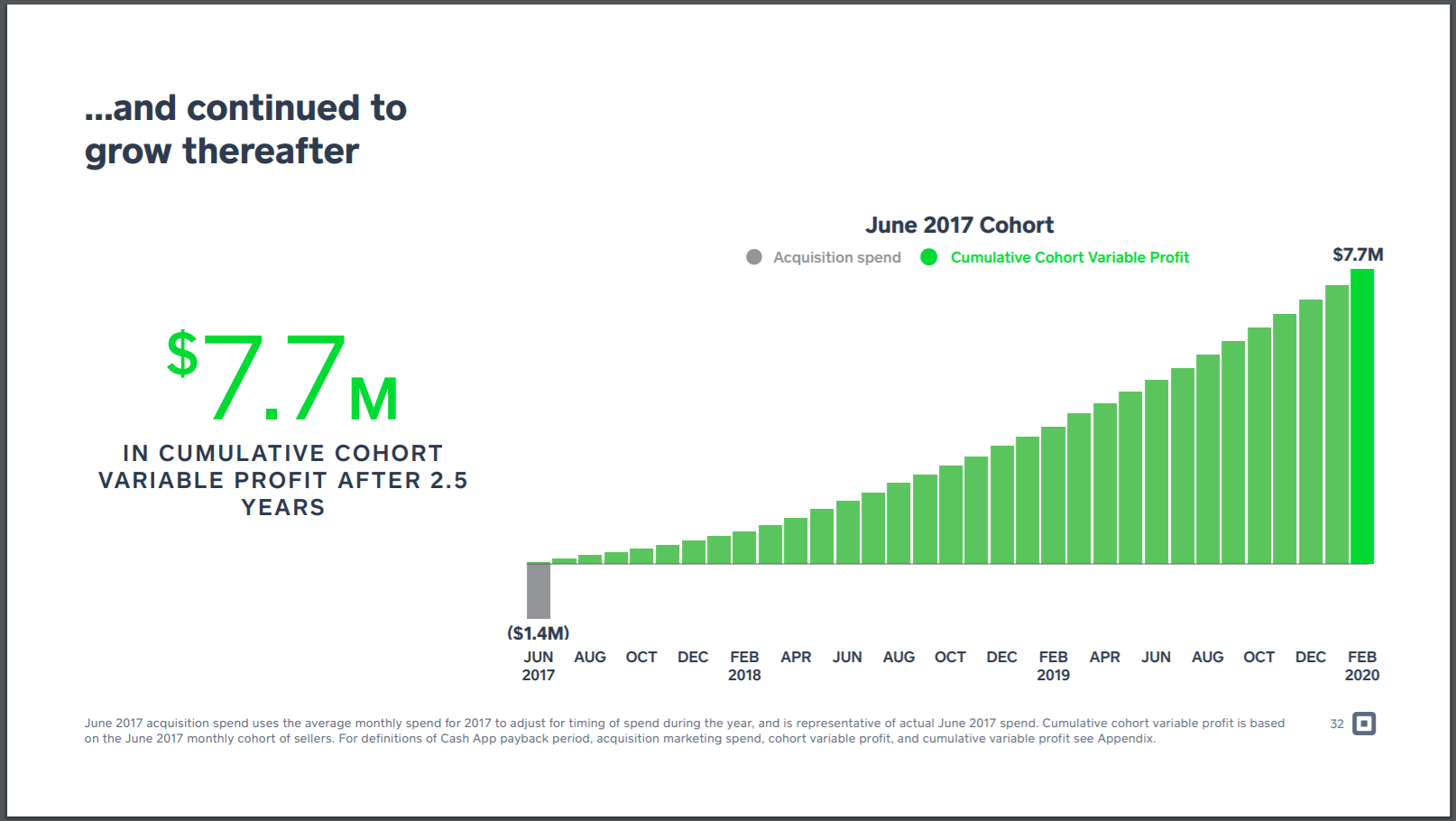

Coming to Cash App now, to the credit of Square’s management team, the financial services app has experienced (1) tremendous growth in the number of monthly-active users in the past few years, (2) a big jump in revenue per user, and (3) incredible unit economics. The table below illustrates the surge in Cash App users from 2015 to the first half of 2020 while the three charts that follow immediately illustrate Cash App’s revenue growth per user and unit economics. Here are what the charts are saying:

- First chart: The green line shows Cash App’s revenue per monthly active user (ex-Bitcoin) in the five years ended December 2019.

- Second chart: The green bars show the cumulative gross profit at each point in time that is generated by the cohort of users that first joined Cash App in June 2017. You can see that from June 2017 to February 2020, the June 2017 user-cohort had generated cumulative gross profit of US$7.7 million. Crucially, the June 2017 Cash App user-cohort had cost Square only US$1.4 million to acquire (the grey bar).

- Third chart: It shows the growth of the total gross profit Square earned from each year’s Cash App user-cohort from 2016 to 2019. The bar for each user-cohort fattens each year, showing that each annual cohort is collectively generating more business for Cash App in each year after they are acquired.

Source: Square investor presentations and earnings update

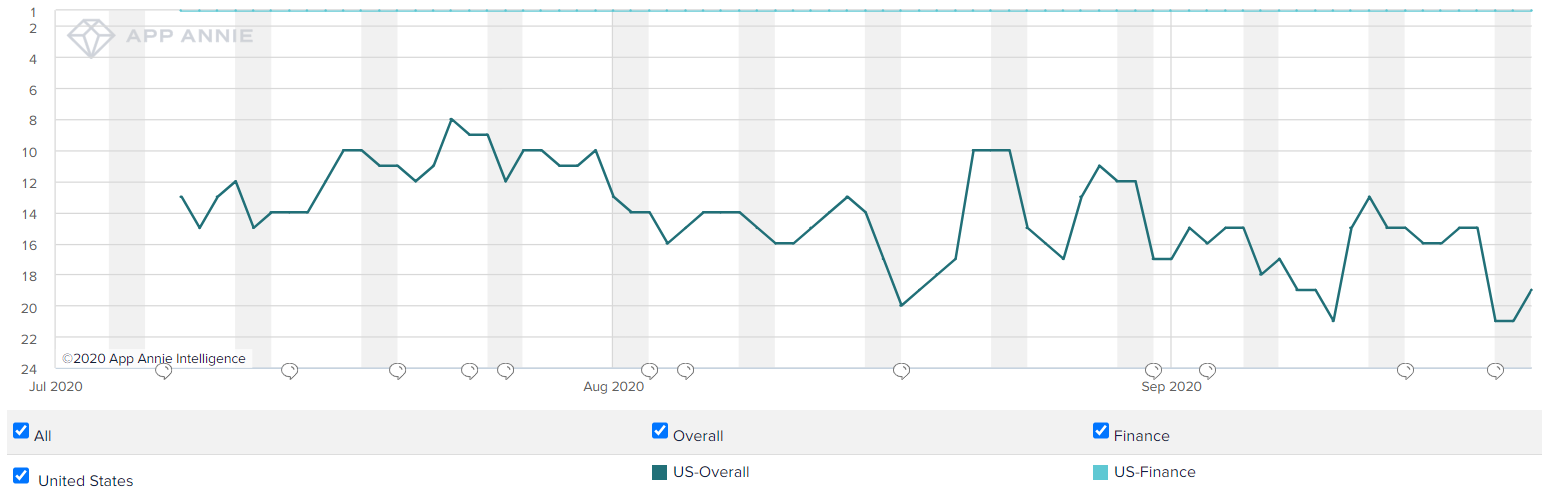

Cash App is also currently one of the top finance apps in the US. When we did a quick search on App Annie, Cash App came up as the top downloaded finance app in the USA every day for the last three months. Cash App was also consistently within the top 21 downloaded apps in the USA for the same period. The chart below is from App Annie and shows Cash App’s overall ranking in the iOS app store by downloads over the past three months.

The fourth thing we want to discuss about Jack Dorsey involves Square’s culture. Part of Square’s creation myth centers on the experience of Square’s other co-founder, Jim McKelvey, who lost the opportunity to sell a piece of art he had created for a few thousand dollars because he was unable to accept credit card payments (McKelvey sits on the board of Square today). This experience eventually led McKelvey and Dorsey to taste firsthand how exclusionary the financial system was. It drove them to create Square, to create a company that could democratise economic opportunities for society by making it easier for people to access financial services. To this point, here are some excerpts from Dorsey’s inspirational investors’ letter found in Square’s IPO prospectus:

“We started Square because Jim McKelvey, our co-founder and my second boss (after my mother!), couldn’t accept a credit card for his art.

Setting up a merchant account was painful. The application process required lots of paperwork and took months. Banks asked for multiple credit checks and years of financial history. And when we were finally approved to accept cards, we couldn’t decipher the rates we were paying. Then our first deposit was held. The entire process was exclusionary and unfair.

Square was born out of our experience. We built a working prototype: a mobile credit card reader that plugged into the audio jack of an iPhone and an app to enter an amount and process the payment. But it took us a year to convince the financial industry to allow us to make Square broadly available. The problem was not with the technology, but with the system.

We decided to make the entire system faster, more affordable, and more accessible. We gave the card reader and software away for free. We settled funds next business morning, which required us to advance money to sellers faster than we received it. We abstracted away the byzantine maze of interchange pricing to offer a simple fixed rate per swipe, which forced us to find ways to lower our costs immediately. Every one of those decisions carried existential risks that we trusted we’d be able to overcome with time. And we have!

Creating more inclusion and greater equality in the global economy is both a social need and a huge business opportunity. We’ve made it our purpose: empower people with beautifully simple tools that give them an advantage where they previously and unfairly had none. Our strategy to realize that purpose is straightforward: grow our payments service, extend payments into financial services, and extend payments into marketing services…

…The strength of this business is more than the money it generates. The collective power of our millions of sellers sustains a scale from which we can build valuable financial services and marketing services, creating reinforcing and virtuous cycles back to our core business of payments. We’ve made getting capital as easy as tapping a button. We replaced pen and paper accounting with real-time insights into sales patterns and customer trends. Everything works together seamlessly to help our sellers make smart decisions for their businesses. When they succeed, we succeed.

By making our services accessible to everyone, we can build a more fair and productive system that serves instead of rules. This is both good for Square and the right thing to do. We’re off to a strong start.”

Today, the homepage of Square’s website states that “No one should be left out of the economy because the cost is too great or the technology too complex.” The company, because of Dorsey, has a clear purpose beyond profit and we appreciate this. We think it is a strength. Dorsey also appears to have built a great culture at Square. Here are two data points:

- Glassdoor is a platform that allows employees to rate their companies anonymously. Currently, 80% of Square-raters on Glassdoor will recommend the company to a friend. Meanwhile, Dorsey has an 87% approval rating as CEO, far higher than the average Glassdoor CEO rating of 69%.

- Comparably is a competitor to Glassdoor. Square also rates highly there. It had a score of 83/100, placing it in the top 5% of companies in the US with 1,001 to 5,000 employees.

Lastly, we want to discuss Square’s excellent execution and admirable actions during this current COVID-19 pandemic that the world is experiencing. A few examples:

- Within two weeks of the first shelter-in-place measures in the USA, Square accelerated the launch of features within the Square Online Store software product to help sellers to continue serving their customers. Examples of new features include the addition of curbside pickup and self-managed delivery options.

- Square provided a massive lifeline to small businesses in the USA by helping to distribute PPP (Paycheck Protection Program) loans through Square Capital, starting in April. The PPP loans are part of the US government’s stimulus package to support the country’s economy; the loans are forgivable if businesses use at least 75% of the loan on payroll costs. As of 10 June 2020, Square Capital had facilitated more than US$820 million in PPP loans (this sum had increased to US$873 million by the end of 2020’s second quarter). Square commented in a June 2020 press release that “Compared to the Square Capital program’s 2019 business loan origination volume, which was [US]$2.3 billion, we did 4.5 months worth of volume in just 6 weeks.”

- To focus on distributing the PPP loans, Square Capital paused the facilitation of its core loan product for the entire second quarter of 2020. This caused Square Capital’s revenue to be “down significantly” for the quarter compared to a year ago. Square also waived all software subscription fees for sellers in April, and gave sellers the option in May to pause their paid subscriptions for up to three months. In addition, during the second quarter of 2020, Square offered promotional pricing for its hardware that supports contactless payments, since these products are important for sellers. These actions hurt Square’s business results in the short run. But we believe they are the right things for Square to do, as they could help build enduring customer-goodwill.

- In April, Square published a microsite and FAQs to help Cash App users understand the US government’s stimulus programs and how they can easily receive payouts from the government with Cash App. This helped to significantly increase Cash App’s popularity.

- Square is going on the offensive by continuing to invest in areas of its business that it believes will drive “attractive long-term returns.” For example, Square is currently focusing on investments to acquire new sellers for its Seller Ecosystem and to drive customer acquisition and the launch of new products for Cash App.

4. Revenue streams that are recurring in nature, either through contracts or customer-behaviour

In the “Company Description” section of this article, we showed that Square’s total revenue of US$3.30 billion in the first half of 2020 came from the following categories:

- Transaction-based revenue of US$1.44 billion

- Subscription and services-based revenue of US$642.5 million

- Hardware revenue of US$40.0 million

- Bitcoin trading revenue of US$1.18 billion

It’s clear that the lion’s share of Square’s ex-Bitcoin revenue comes from subscriptions as well as transactions and payment activities that happen perhaps everyday. These look like recurring revenue streams to us. As long as sellers and individuals keep using Square’s products and services to process payments, make payments, and move money around, Square will be able to continue earning transaction-based as well as subscription and services-based revenues. For perspective, consider the following: (a) Square’s GPV of US$106.2 billion in 2019 came from 2.3 billion card payments; (b) in the same year, Square’s Seller Ecosystem had over 180 million buyer profiles); and (c) Cash App has 30 million monthly-active users right now.

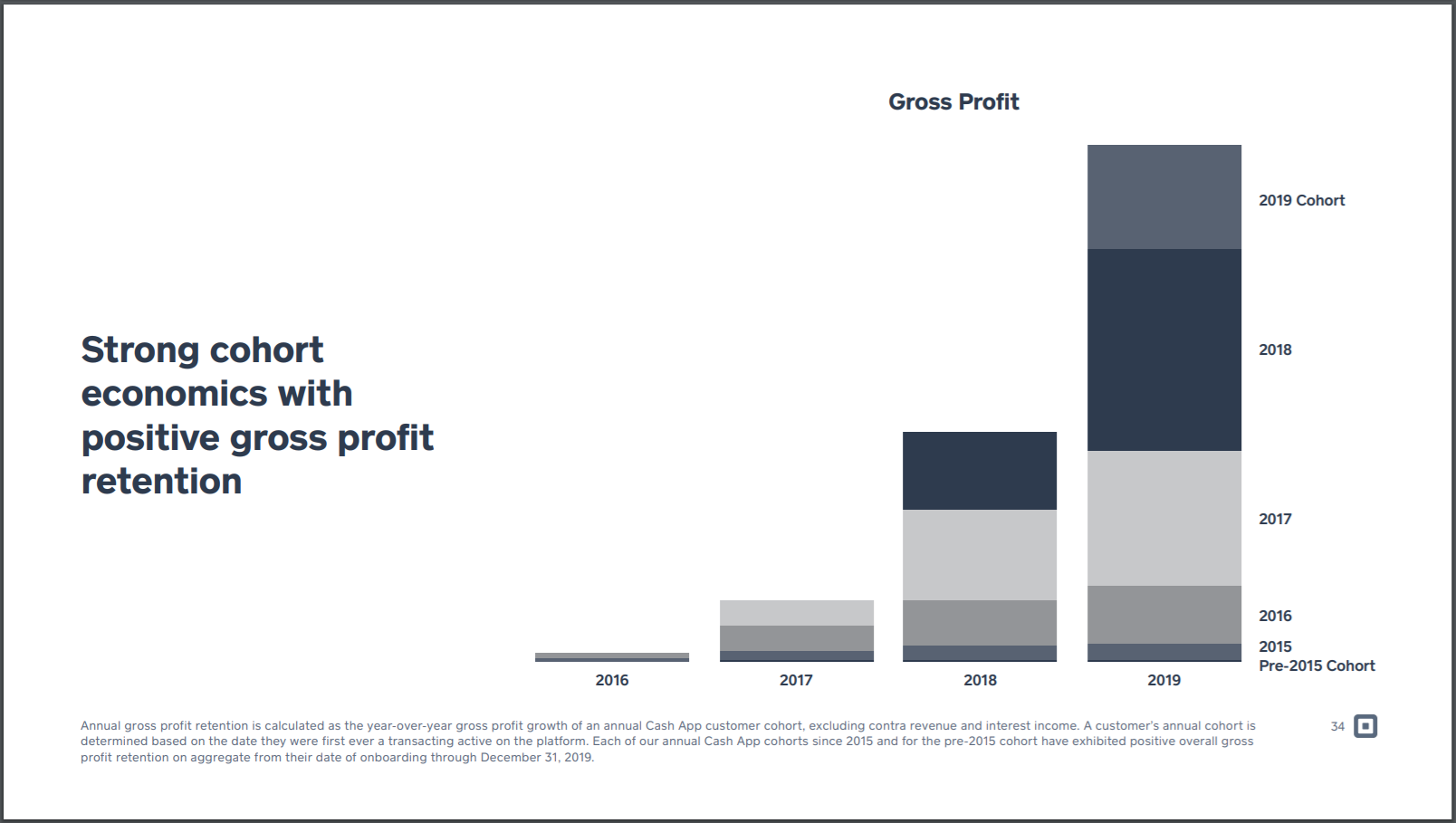

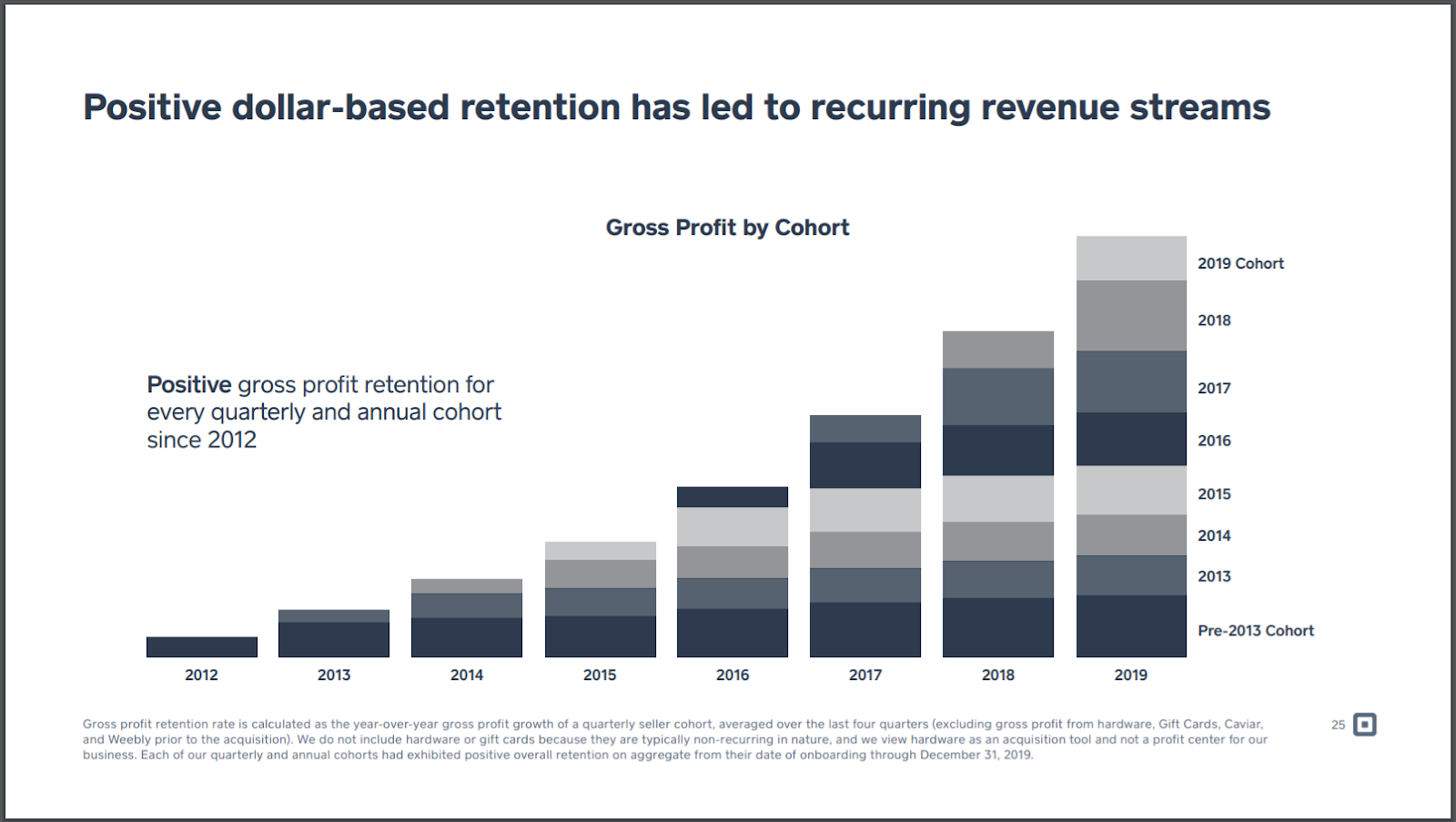

Lending further weight to our view that Square’s revenue streams are recurring in nature is the fact that the gross profit produced by each user-cohort of the company has grown over time. This is shown in the two charts below and here’s what’s happening in the charts:

- First chart: We showed it earlier when we were discussing Square’s management team. It shows the growth of the total gross profit Square earned from each year’s Cash App user-cohort from 2016 to 2019. The bar for each user-cohort fattens each year, showing that each annual cohort is collectively generating more business for Cash App in each year after they are acquired.

- Second chart: It shows the same dynamic as in the first chart, but it’s for Square’s Seller Ecosystem user-cohorts from 2012 to 2019.

Source: Square investor presentation

5. A proven ability to grow

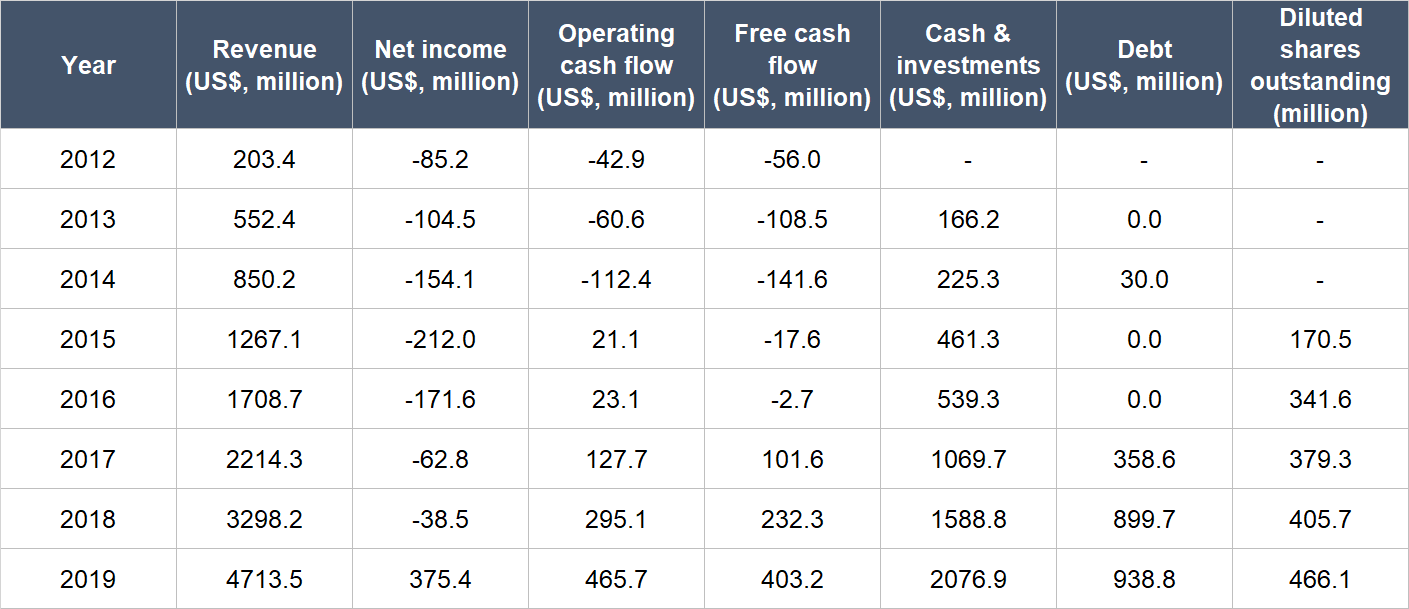

The table below shows Square’s key financials since 2012 (they are the earliest data we can find, since the company listed only in November 2015).

Source: Square annual reports and IPO prospectus

There are a few things we want to highlight about Square’s historical financials:

- Revenue has compounded at an impressive annual rate of 56.7% from 2012 to 2019. Growth was still strong in 2019 at 42.9%. Bitcoin trading was introduced by Square in the fourth quarter of 2017. If Bitcoin revenue was removed in 2018 and 2019 (US$166.5 million and US$516.5 million, respectively), Square’s revenue growth in 2019 would be 34.0%. This is lower than the reported revenue growth but it is still strong.

- Square’s net income turned positive in 2019 for the first time. But the profit was mostly driven by the sale of Square’s food delivery business, Caviar, to DoorDash in October 2019. The good thing is that Square’s losses have narrowed over time.

- The company started producing positive operating cash flow in 2015 and also turned free cash flow positive in 2017. In the past three years (2017 to 2019), Square’s operating cash flow and free cash flow have both increased substantially. In 2019, the company’s free cash flow margin was 8.6%.

- Square’s balance sheet was strong throughout the timeframe we’re looking at, with its cash & investments outweighing debt by a wide margin.

- At first glance, Square’s diluted share count appeared to double from 2015 to 2016 (we only started counting from 2015 since Square was listed in November of the year). But the number we’re using is the weighted average diluted share count. Right after Square got listed, it had a share count of around 323 million. From 2016 to 2019, Square’s diluted share count increased by 10.9% per year. This is much lower than the company’s revenue growth rate and the apparent doubling in share count that happened from 2015 to 2016. But it is still typically higher than what we like to see. We’ll be keeping an eye on future changes in Square’s diluted share count. The good thing is that Square’s diluted share count in the first half of 2020 was up by just 3.9% from the first half of 2019.

Square continued growing strongly in the first two months of 2020, with a 29% year on year increase in GPV. But then the COVID-19 pandemic arrived, which caused a sharp decline in Seller GPV in March. In the second quarter of 2020, Square’s GPV fell by 15% from a year ago. The declines in GPV affected Square’s Seller business segment. But growth in the Cash App segment helped pick up some of the slack. The table below shows the dynamics in revenue changes in Square’s Cash App and Seller business segments in the first half of 2020 compared to a year ago. You can see that even without Bitcoin revenue, the Cash App segment had experienced rapid revenue growth in the first half of 2020 (up 121%). In March, Cash App added its largest number of net-new transacting active users and during the second quarter of 2020, Cash App users transacted 15 times per month on average, up by nearly 50% from a year ago.

Source: Square earnings update; numbers for 2019 exclude contributions from Caviar

It’s not all doom and gloom for Square’s Seller business segment too. In the second quarter of 2020, Seller GPV from online channels jumped by more than 50% year on year, and accounted for over 25% of total Seller GPV (up from just 14% a year ago).

Square’s net income and free cash flow for the first half of 2020 were both negative and had worsened from the first half of 2019. But we’re not concerned, as we think the longer term outlook for Square is bright.

6. A high likelihood of generating a strong and growing stream of free cash flow in the future

We think Square excels in this criterion for two reasons.

First, there’s Square’s excellent unit economics. Earlier, we showed the chart just below and we said this: “The green bars show the cumulative gross profit at each point in time that is generated by the cohort of users that first joined Cash App in June 2017. You can see that from June 2017 to February 2020, the June 2017 user-cohort had generated cumulative gross profit of US$7.7 million. Crucially, the June 2017 Cash App user-cohort had cost Square only US$1.4 million to acquire (the grey bar).”

Source: Square investor presentation

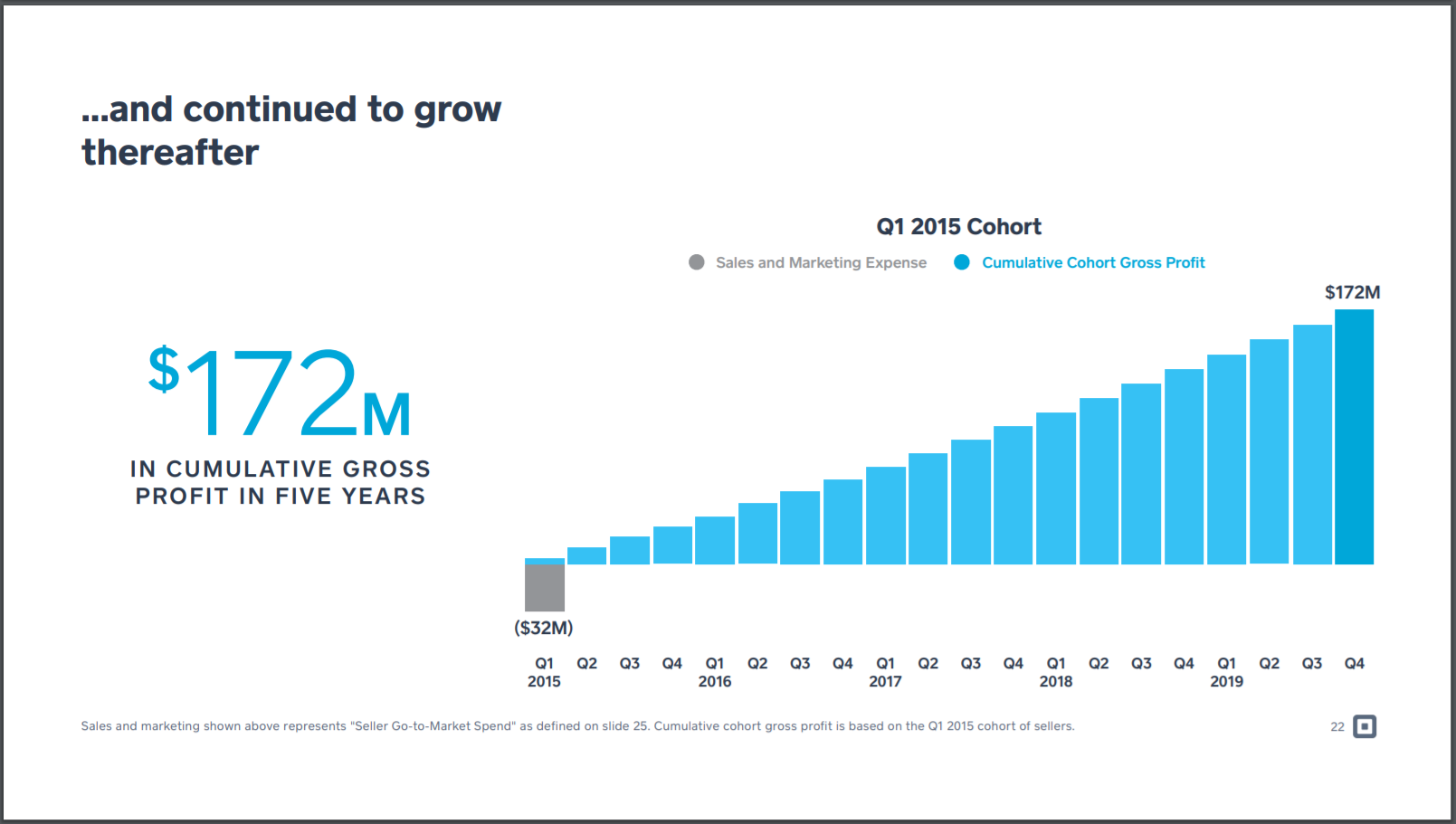

A similar dynamic exists for customers of Square’s Seller segment. The chart below shows the cumulative gross profit, as of 2019’s fourth quarter, for the Seller cohort that onboarded in the first quarter of 2015, compared with the marketing spend to acquire the cohort. Square spent US$32 million in sales and marketing to acquire the 2015 first-quarter cohort, and the cumulative gross profit in five years was US$172 million. The payback period (time taken to earn a gross profit that exceeds the marketing spend) was less than four quarters.

Source: Square investor presentation

Source: Square investor presentation

Second, the Cash App segment is growing rapidly. In the first half of 2020, Cash App’s total revenue was US$1.73 billion, up 295% from a year ago; excluding Bitcoin revenue, Cash App’s revenue would be US$546.4 million, up 121% from a year ago. The Cash App business has a higher margin profile than the Seller segment, so as Cash App’s weight in Square grows, the company’s overall free cash flow margin will likely expand too.

Valuation

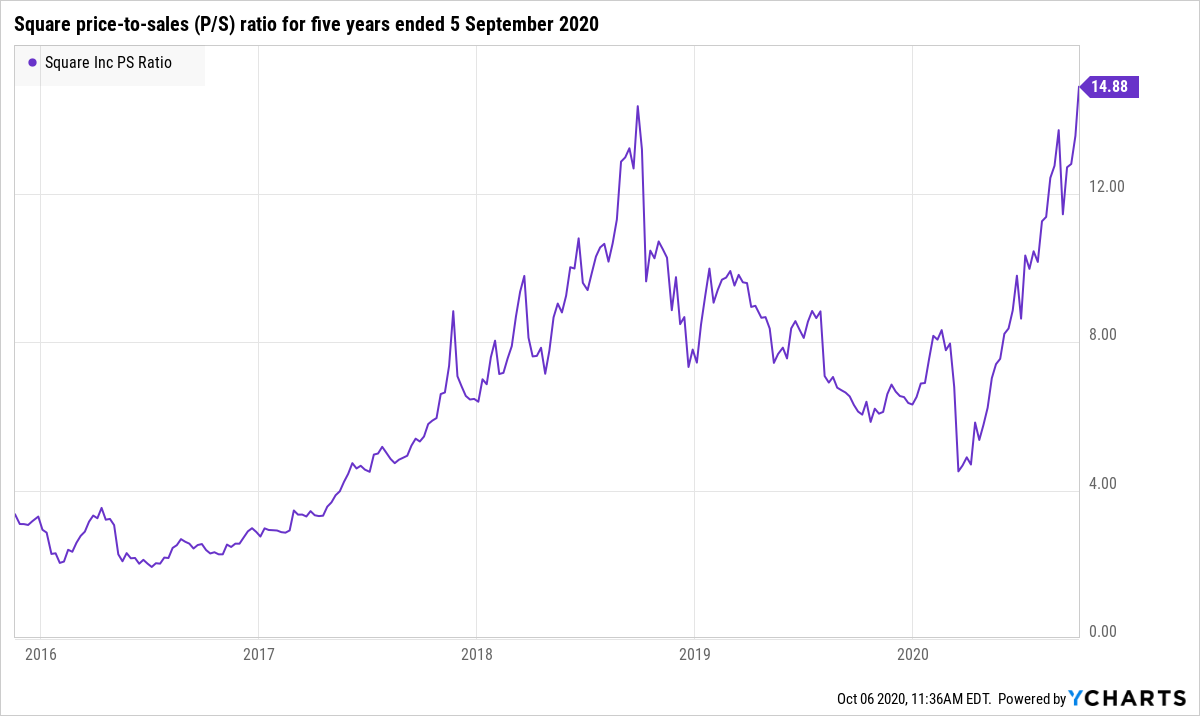

We completed our purchases of Square shares with Compounder Fund’s initial capital in late July 2020. Our average purchase price was US$127 per Square share. At our average price and on the day we completed our purchases, Square shares had a trailing price-to-sales (P/S) ratio of around 10.8. Excluding Bitcoin revenue, Square’s adjusted P/S ratio rises to 12.6. We like to keep things simple in the valuation process. In Square’s case, we think the P/S ratio is an appropriate metric to value the company. Even though Square generated positive free cash flow in each of 2017, 2018, and 2019, the first half of 2020 saw the company’s free cash flow fall into the red. The chart below shows Square’s P/S ratio over the past five years.

It’s clear that the P/S ratio of 10.8 at our point of investment is high relative to history. We think that Square can achieve a free cash flow margin of at least the high-teens range when it’s more mature. Applying an 18% free cash flow margin to the P/S ratio of 10.8 gives us a price-to-free cash flow (P/FCF) ratio of 60. This is not a low valuation. But we think it’s still reasonable. Square has barely scratched the surface of its huge market opportunity and the company has proven to be highly innovative – this means Square is likely going to be able to grow its revenue at a strong clip in the years ahead.

For perspective, Square carried a P/S ratio of 12.7 at the 5 October 2020 share price of US$170; the adjusted P/S ratio, excluding Bitcoin revenue, is 17.1.

The risks involved

There are six main risks we see for Square:

- Key-man risk: We think Jack Dorsey has been a key reason for Square’s success. Briand Grassadonia, who has served as Square’s Cash App lead since January 2013, should also be credited for the company’s results so far. If any of these two men leave the company, we think Square will have a big hole to fill (Dorsey to a much greater extent than Grassadonia). It’s also worth noting that it’s not easy to be CEO of two huge companies, as Dorsey is currently. So far, Square has executed brilliantly, but there’s a chance in the future that Dorsey’s attention could be divided too thinly between Twitter and Square.

- Competition risk: Square faces intense competition in both its Seller and Cash App segments. For example, Cash App competes with other mobile wallets and fintech solutions. Mobile wallet competitors include Venmo, which is owned by digital payments juggernaut Paypal. Square’s ability to build great products that are easy to use will play a big part in how the company can grow Cash App. But we think that there can be multiple winners in this space, and Cash App is likely to be one of them in our opinion.

- Recession risk: In the first half of 2020, transaction-based revenue from Square’s Seller segment accounted for 64% of the company’s total ex-Bitcoin revenue. This means a significant chunk of Square’s revenue currently depends on retail transactions. COVID-19 has resulted in significantly lower GPV in physical stores, which has hurt Square’s transaction-based Seller revenue. Even though online GPV has seen growth, it’s not enough to offset the negative impacts to physical GPV. An extended recession could lower consumer confidence and hurt Square’s online GPV growth too. An extended recession could also lead to higher default rates for Square Capital. The good things are: (1) Square has a robust balance sheet; (2) Cash App is doing well; and (3) Square’s online GPV is currently growing well.

- Regulatory risk: The payments space is rife with regulatory risks, and this is something we’ll have to watch for Square. It’s just the nature of the beast.

- Dilution risk: As already mentioned, Square’s share count has increased relatively quickly in the past. This is something we’re keeping an eye on.

- Valuation risk: Lastly, we invested in Square at a high valuation. The company reported negative free cash flow and losses in the first half of FY2020. We think the current valuation is justified by the company’s potential for growth, especially in Cash App. But if there are any hiccups in Square’s business – even if they are temporary – there could be a painful fall in the share price. This is a risk we’re comfortable taking as long-term investors.

Summary and allocation commentary

To summarise Square:

- Its revenue is tiny compared to its current total addressable market, which will likely expand in the future.

- It has a strong balance sheet that helps it to navigate the current COVID-19 crisis.

- It has an incredible tech-entrepreneur CEO in Jack Dorsey and a compensation structure that aligns the interests of its key leaders and shareholders.

- It has a high level of recurring revenue from subscriptions as well as repeat customer-use.

- It has an impressive track record of growing its business and had generated positive and growing free cash flow in recent years.

- It has excellent unit economics for both its Seller and Cash App business segments, and we believe this will provide the foundation for Square to achieve strong and growing free cash flow in the future.

There are a few important risks we’re watching with Square, including key-man risk; intense competition; recession risk because of COVID-19; potential regulatory issues; dilution risk; and lastly, valuation risk. But after weighing the pros and cons, we decided to initiate a 2.0% position – a medium-sized allocation – in Square with Compounder Fund’s initial capital. We’re excited about Square’s growth prospects and the chance to ‘partner’ with Jack Dorsey, but we think a medium allocation is more suitable at this time given the risk-profile of the company.

And here’s an important disclaimer: None of the information or analysis presented is intended to form the basis for any offer or recommendation; they are merely our thoughts that we want to share. Of all the companies mentioned in this article, Compounder Fund also currently owns shares in Apple, Facebook, and PayPal.