Compounder Fund: Portfolio Update (December 2023) - 06 Dec 2023

Jeremy and I intend to share frequent but non-scheduled updates on how Compounder Fund’s portfolio looks like. The last time we shared an update on this was for Compounder Fund’s portfolio as of 08 October 2023.

In it, I shared all 49 holdings in the fund’s portfolio. As of 06 December 2023, Illumina and Upstart are no longer in the portfolio after we completely exited both companies in mid-November 2023. Our sell-thesis for them can be found here (Illumina) and here (Upstart). We used the cash that Compounder Fund received from the full sale of the two companies to add to the fund’s existing positions in Paycom Software and The Trade Desk.

Both Paycom and Trade Desk saw their stock prices fall hard after the release of their respective results for the third quarter of 2023; on the day after their results were released, Paycom’s stock price sank by 38% while Trade Desk’s stock price slid by 17%. We thought that the declines gave us opportunities to add to the fund’s positions in them at attractive valuations.

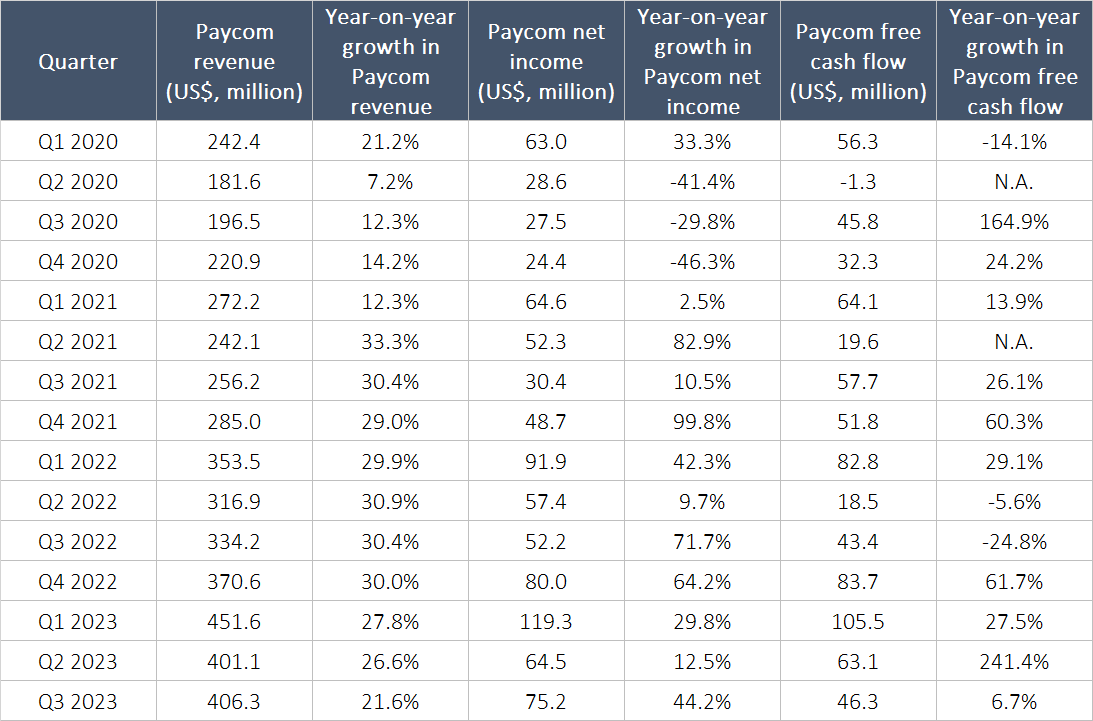

Let’s discuss Paycom first. Table 1 below shows Paycom’s quarterly revenue, net income, and free cash flow going back to the first quarter of 2020 (this was the most recent results we had for the company when we first invested in it in July 2020; see our original thesis here). There’s a clear trend of all three financial numbers growing over time. Even in the third quarter of 2023 – the results that preceded the aforementioned decline in Paycom’s stock price – the human capital management software provider experienced strong double-digit growth in both revenue and net income.

Table 1; Source: Paycom quarterly earnings updates

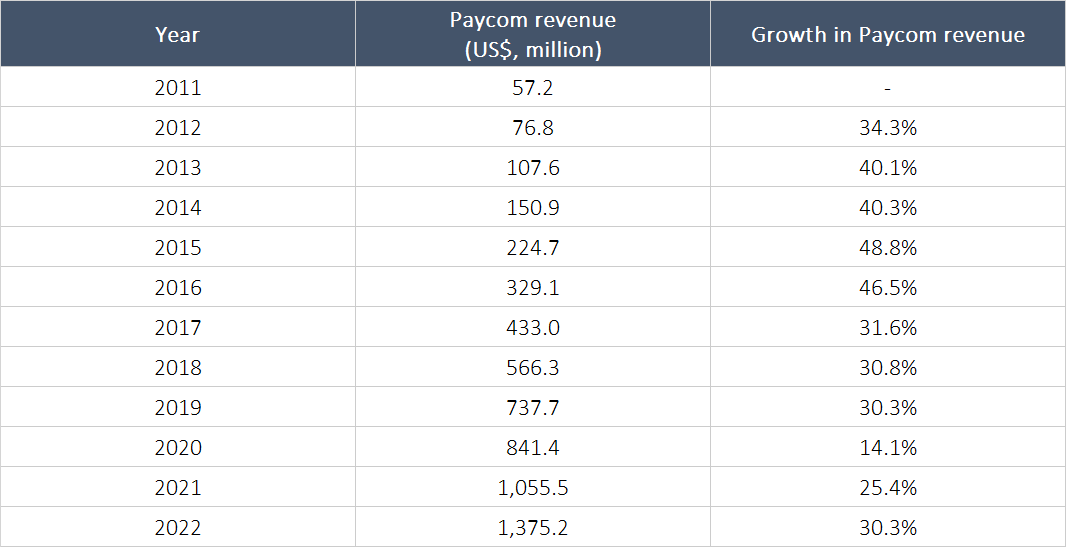

Jeremy and I are often wary of identifying drivers for short-term stock price movements because we think that these movements can happen for no rhyme or reason. Moreover, if we’re constantly coming up with reasons for short-term stock price movements and they happen to be wrong, our investment decision-making ends up being negatively impacted. But for Paycom, we think there are three clear agitants for the post-earnings decline in its stock price. First, the company’s revenue for the quarter was below its guidance range (management expected revenue of US$410 million to US$412 million for the quarter). Second, management lowered the company’s revenue guidance for 2023 from growth of 25% to growth of 22%. Third, management expects Paycom’s top-line to increase by between 10% to 12% in 2024, which is a far cry from what Paycom has achieved in the past, as shown in Table 2.

Table 2; Source: Paycom quarterly earnings updates

But we believe there is a healthy underlying reason behind the three factors, namely, BETI (Better Employee Transaction Interface), Paycom’s self-service payroll technology for employees to perform their own payroll, which was launched in July 2021. This piece of software has caught on fast with Paycom’s clients; by the third quarter of 2023, two thirds of the company’s client base were BETI users. The fast adoption is not surprising, given that BETI users are deriving a high return on investment: A recent study commissioned by Paycom and conducted by Forrester Consulting found that BETI users saw a 90% reduction in labour for payroll processing and their HR and accounting teams saved over 2,600 hours annually. But Paycom’s management was a little surprised by just how effective BETI is for users. Here’s what management said during Paycom’s 2023 third-quarter earnings call (emphasis is mine):

“We are continuing to help clients navigate to the new way of doing things. And as a result, nearly 2/3 of our clients have made the shift to BETI. For most employees, the value of the perfect payroll is oftentimes immeasurable. If their check is perfect, they don’t need to borrow money from a friend or family member to get through the weekend or make a bill payment. How do you measure the value of that?

We’re getting better and better at helping employers measure the full value available to them when payrolls are perfect. A portion of that value is easy to calculate because it’s the value they receive by the elimination of after-the-fact payroll errors that require correction payroll runs, manual checks, voided checks, direct deposit reversals, additional wires, tax adjustments, W2Cs, et cetera, et cetera. Perfect payrolls eliminate these common after-the-fact payroll corrections that would otherwise be billable. So the more employees do their own payroll, the greater the savings delivered to the client from Paycom future billings, which results in lower related revenue recognized by Paycom…

…Revenue of $406.3 million was up approximately 22% compared to the prior year period. That came in below our guidance range as a result of lower-than-expected service revenues and unscheduled payroll runs. As Chad mentioned, BETI adoption and usage creates tremendous value to clients as they experience perfect payrolls and eliminate errors, corrections and unscheduled payrolls, which would otherwise be billable items.”

So what happened to Paycom in the third quarter of 2023 was that the company’s clients had seen significant reductions in payroll-related errors because of their usage of BETI. These error-reductions in turn resulted in lower revenue for Paycom because there were less mistakes for the company to correct for clients. Despite BETI’s short-term hit to Paycom’s revenue, management is pressing ahead to promote adoption of the self-service payroll software among new as well as existing clients (BETI is provided for all new clients). This drove Paycom’s management to lower the company’s revenue guidance for the fourth quarter of 2023 and to expect relatively anaemic revenue growth for 2024. But why is management willing to swallow this bitter pill? Paycom’s CEO and founder, Chad Richison, explained during the 2023 third-quarter earnings conference call (emphases are mine):

“The only person that wins in the old model is the payroll company. I mean we’ve been charging people to fix mistakes for 80 years, our industry, mistakes that we’ve allowed them to make. And so yes, we could look at — well, if we eliminate all these mistakes, we’re not going to have as many direct deposit reversals and tax changes and W2Cs and new payroll runs. I mean we get it, and we’ve been mitigating it with business sales along the way. But now our CRR [customer relations representative] group, as I said on the last call, we’re dedicated to helping clients achieve value. That’s where we’re at today and the decisions we’re making today will drive long-term share or long-term value for our shareholders, me being one of them, and so the decisions we’re making today will allow us to get to the next step. But we’re not abandoning and/or changing our strategy in regards to BETI. If anything, I would say we’re leaning in more.”

Paycom’s management believes that proactively delivering as much value as possible to clients, even if doing so would be a short-term negative for Paycom, is the right thing to do for building the company’s long-term value. We agree. The actions of Paycom’s management today reminds us of what Jeff Bezos wrote in Amazon’s 2012 shareholders’ letter:

“Proactively delighting customers earns trust, which earns more business from those customers, even in new business arenas. Take a long-term view, and the interests of customers and shareholders align.”

What Paycom’s management is doing with BETI, in our view, is to align the interests of the company’s customers and shareholders over the long run.

Earlier in this update, I mentioned that the post-earnings decline in Paycom’s stock price gave us an attractive valuation. At the time of our addition, Paycom’s P/E (price to earnings) and P/FCF (price to free cash flow) ratios were 31 and 35, respectively, noticeably lower than when we first invested (88 and 141) and the most recent time we added to Paycom (59 and 73, in early-July 2023).

Let’s now move to Trade Desk, which provides a self-service programmatic advertising platform (see our thesis on the company for more). Again, Jeremy and I tend to avoid coming up with reasons for the short-term movement of stock prices. But in the case of Trade Desk, we think we have identified what spooked the market, leading to the company’s 17% post-earnings decline in its stock price: Management’s guidance for revenue growth of at least 18% for 2023’s fourth quarter, which was meaningfully lower than analysts’ estimates for 24% growth.

We were happy to add to Compounder Fund’s Trade Desk position despite the lower-than-expected revenue growth-guidance for two reasons. First, 18% revenue growth is hardly a tragedy. Second, management shared the following during Trade Desk’s 2023 third-quarter earnings conference call (emphasis is mine):

“We represent the vast majority of the Ad Age top 200 advertisers, the largest advertisers in the world. Starting in the second week of October we have seen some transitory cautiousness across some of those advertisers. These include, for example, industries that have been impacted by recent strikes, such as the U.S. Auto industry. Through the first week of November, we have seen spend stabilize and we are optimistic for the remainder of the year and for 2024.”

In other words, Trade Desk’s business was affected by short-term issues in the early parts of the fourth quarter of 2023 that have since been resolved, and management remains optimistic about the company’s future growth. We share the same enthusiasm.

Trade Desk’s UID2 (Unified ID 2.0), an open-source identity framework, is now adopted by nearly all major streaming companies in the USA. UID2 helps advertisers target audiences with greater precision and provides better measurement of the results from advertising campaigns. Adopting UID2 brings substantial tangible benefits for the digital advertising ecosystem. Here are some examples that management shared during Trade Desk’s 2023 third-quarter earnings conference call:

- A leading streaming platform recently implemented UID2 and saw its average daily revenue from Trade Desk increase by 150%.

- Luxury Escapes, a high-end travel agency, used UID2 to hone in on potential new customers who are similar to its most loyal customers. UID2 helped Luxury Escapes achieve a conversion rate for its advertising campaigns in the US that was more than 400% higher than with cookies. Moreover, the travel agency’s return on asset was 900% higher and its cost per acquisition was 83% lower.

In July 2023, linear TV (the traditional way of viewing TV through broadcast and cable) dropped below 50% of US TV viewership for the first time, down from 51% in June. Streaming, meanwhile, accounted for 39% of viewership in July, up from 38% the previous month. The growth in streaming viewership is a tailwind for Trade Desk. Video ads, which includes CTV (CTV, or connected TV, refers to streaming), was Trade Desk’s largest business segment in the third quarter of 2023, accounting for a mid-40s percentage share of revenue, and continues to grow in importance for the company. More importantly, despite linear TV’s decline, and the fact that streaming’s viewership is inching closer to that of linear TV, the amount of advertising dollars spent on linear TV still dwarfs that of streaming. According to eMarketer, ad spending on linear TV and CTV are expected to be US$61 billion and US$25 billion, respectively, this year. We think the disparity between the time-spent and ad-spending on linear TV compared to streaming is unsustainable. As streaming continues its likely path of ascension, we expect it to pull away an increasing amount of advertising dollars from linear TV. Trade Desk’s UID2 and other technologies are potential catalysts in the transition, as they provide a better advertising experience for both viewers and advertisers.

Elsewhere, Trade Desk is also using AI to improve its advertising platform in four areas that are crucial to the platform’s success – bidding, pricing, value, and ad-relevance – and already has private betas for these categories. Jeff Green, Trade Desk’s co-founder and CEO, shared in the 2023 third-quarter earnings conference call that the impact of Trade Desk’s AI-related investments this year will start showing up in 2024. We look forward to observing the AI-driven improvements to Trade Desk’s business.

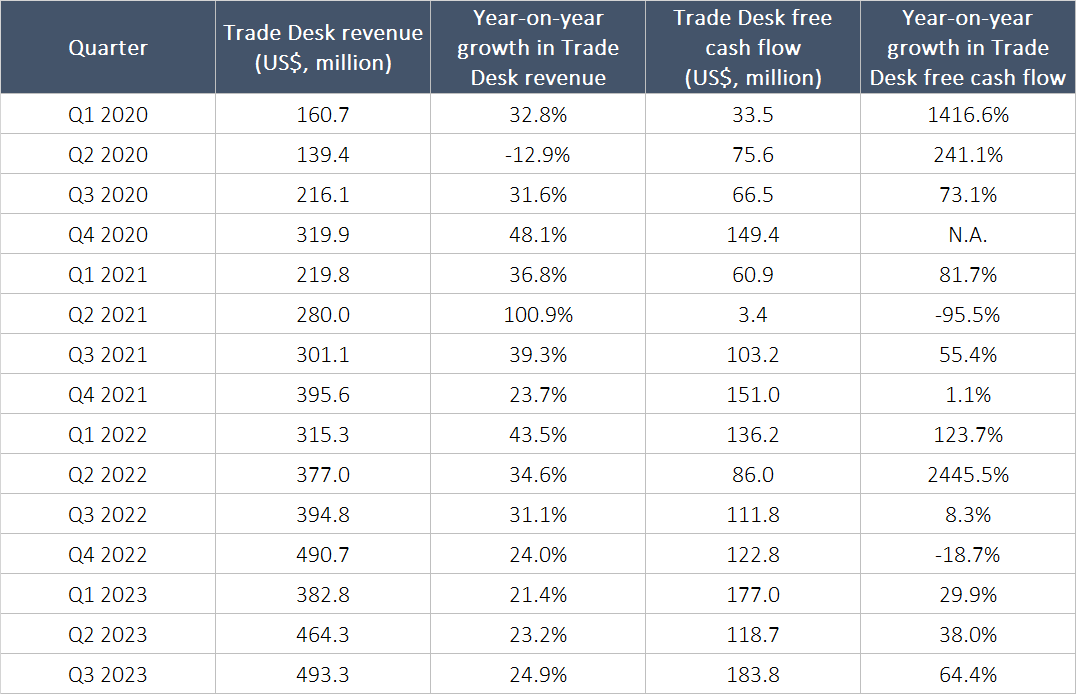

Adding to our confidence in Trade Desk is the company’s consistently strong revenue growth and ability to generate largely positive and growing free cash flow going back to the first quarter of 2020 (the most recent data we had when we first invested in the company in July 2020):

Table 3; Source: Trade Desk quarterly earnings update

And lastly, as cherry on the cake, Trade Desk’s P/S (price to sales) and P/FCF ratios fell to 18 and 56, respectively, when we added to Compounder Fund’s position in the company. These look like attractive valuations to us, and are significantly lower than the P/S and P/FCF ratios seen when we first invested (30 and 415) and during our most recent addition in late-November 2021 (45 and 159).

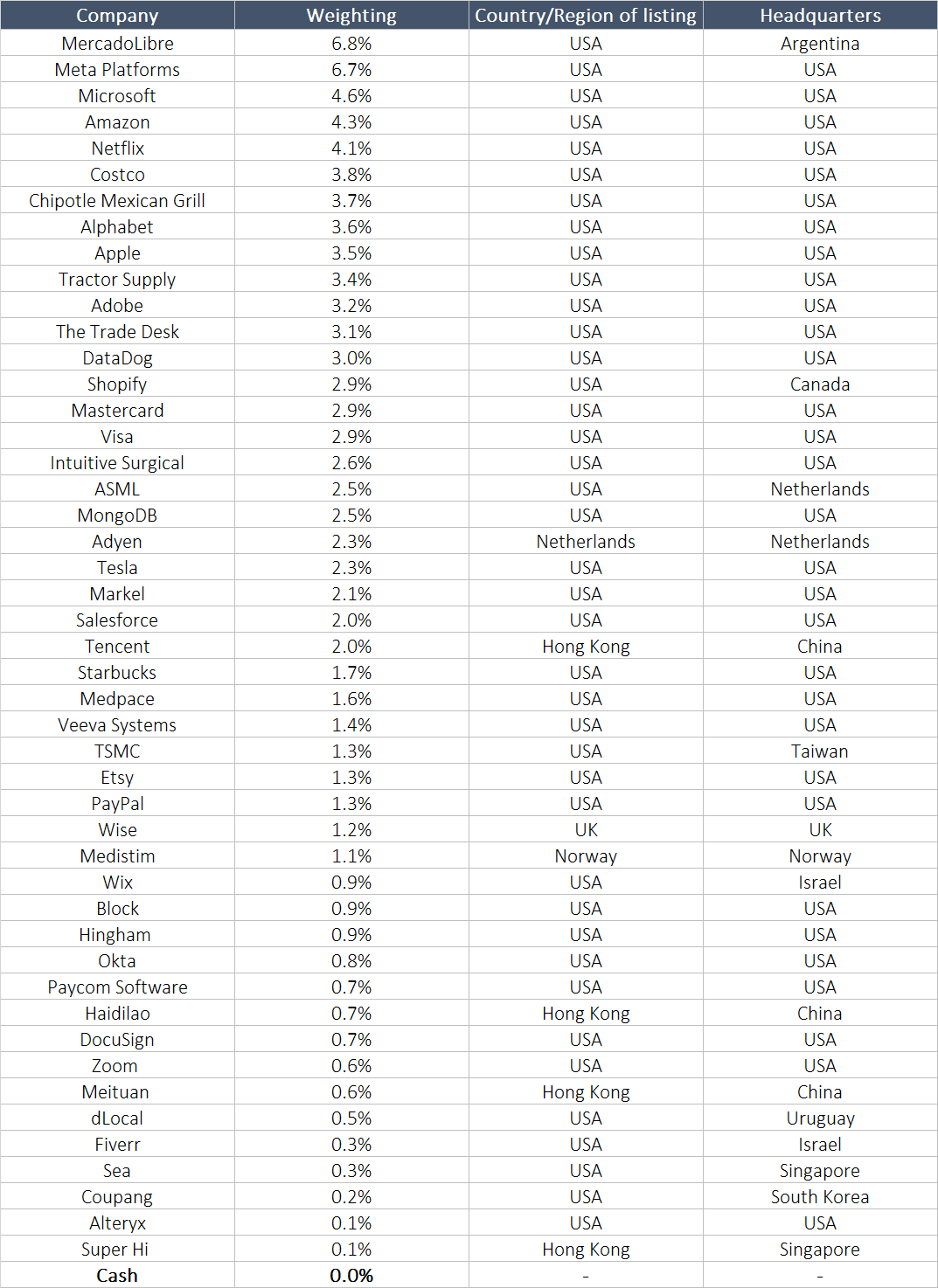

Here’s how Compounder Fund’s portfolio of 47 companies looks like as of 04 December 2023:

We’re sharing all this information with the public and with the fund’s investors for two reasons. First, we believe deeply in investor education and want Compounder Fund’s return and actions to be a source for people to learn about investing. Second, we believe that this transparency will help investors of Compounder Fund develop comfort with our investing process over time, which is great; in turn, this will also free us from the time-consuming activity of dealing with questions on how we invest, and thus give us more to invest better for our investors.

And here’s an important disclaimer: None of the information or analysis presented is intended to form the basis for any offer or recommendation; they are merely our thoughts that we want to share. Holdings are subject to change at any time.