Compounder Fund: Upstart Sell Thesis - 06 Dec 2023

Data as of 04 December 2023

We first invested in Upstart (NASDAQ: UPST) for Compounder Fund’s portfolio in August 2021. Our investment thesis for the company can be found here. In mid-November this year, we completely exited Upstart. This article describes our Sell thesis for the company.

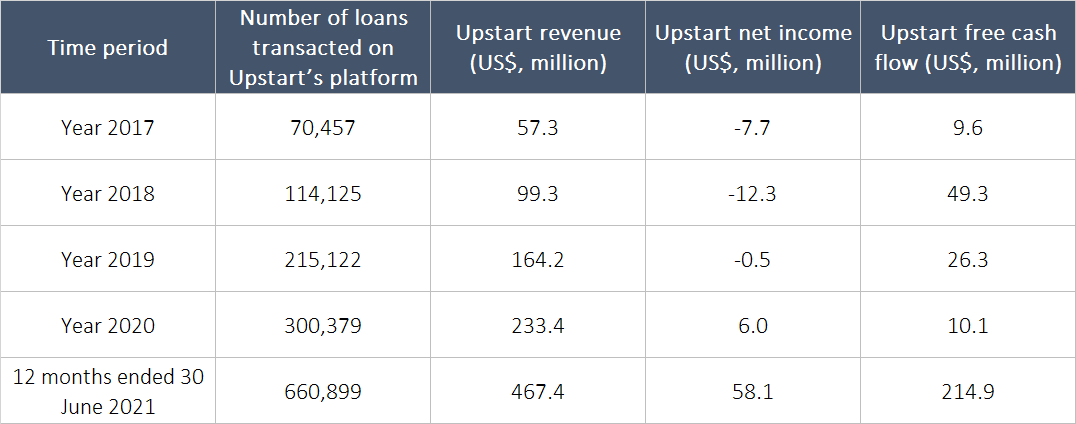

When we first invested in Upstart, it offered a cloud-based lending software platform – powered by AI (artificial intelligence) – to banks. Upstart’s platform was able to better assess credit risk compared to banks’ traditional credit models. As a result, the number of loans that flowed through Upstart’s platform increased by more than 800% from 2017 to the 12 months ended 30 June 2021 as shown in Table 1 below. The table also illustrates the significant improvement in Upstart’s revenue, net income, and free cash flow over the same time period.

Table 1; Source: Upstart regulatory filings

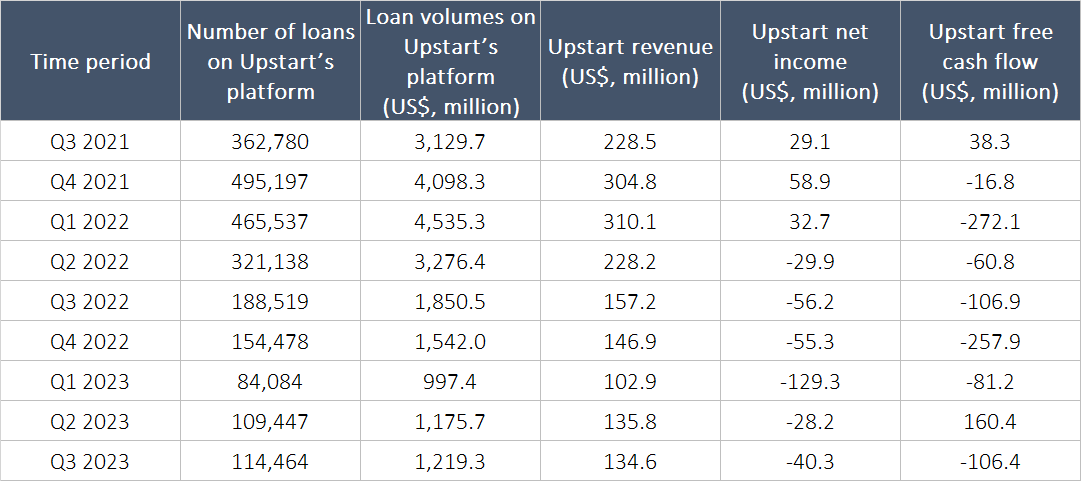

But Upstart’s rapid ascent was followed by a swift deterioration in its business. Table 2 below details Upstart’s loans, revenue, net income, and free cash flow for each quarter from the third quarter of 2021 to the third quarter of 2023. Notice the year-on-year deterioration for these metrics.

Table 2; Source: Upstart regulatory filings

The Federal Reserve, the USA’s central bank, raised interest rates at an unprecedented pace in 2022 and continued hiking throughout most of 2023 before pausing in September. The sharp rise in interest rates created three important problems for Upstart:

- First, institutional investors lost appetite for Upstart-powered loans

- Second, Upstart’s AI credit models were caught off-guard and under-estimated credit risks for Upstart-powered loans that were originated between the second quarter of 2021 and the third quarter of 2022

- Third, the loans offered through Upstart’s platform came with high interest rates and this put off potential borrowers

The end result? The drastic fall in the number of Upstart-powered loans and the company’s financial performance that is found in Table 2. We now think that the quality of Upstart’s AI credit models and management team are much poorer compared to our original view.

The issue with Upstart’s AI credit models can be explained by the aforementioned poor estimation of credit risks by the models. The concern with Upstart’s management team involves the institutional investors that the company works with. In our thesis for Upstart, we wrote that an “Upstart-powered loan can either be retained by the bank partner that originated the loan or be purchased by Upstart, which then (1) immediately resells the loan to institutional investors, (2) holds the loan for a period of time before selling it to institutional investors, or (3) retains it.” These institutional investors, for the most part, do not have long-term agreements with Upstart. In other words, the capital was not sticky: They could disappear at short notice and this happened in earnest starting in the second quarter of 2022, with the first signs of trouble appearing in the first quarter. We now think it’s a strategic mistake that Upstart’s management team did not ink any long-term funding commitments with institutional investors earlier, even though the company had already been working with such investors since 2015 – management said that they only started pursuing such commitments in the company’s 2022 second-quarter earnings call that was held in August 2022. We also think it’s an error on our part that we did not realise Upstart’s management team had made a strategic mistake when we initially invested in the company.

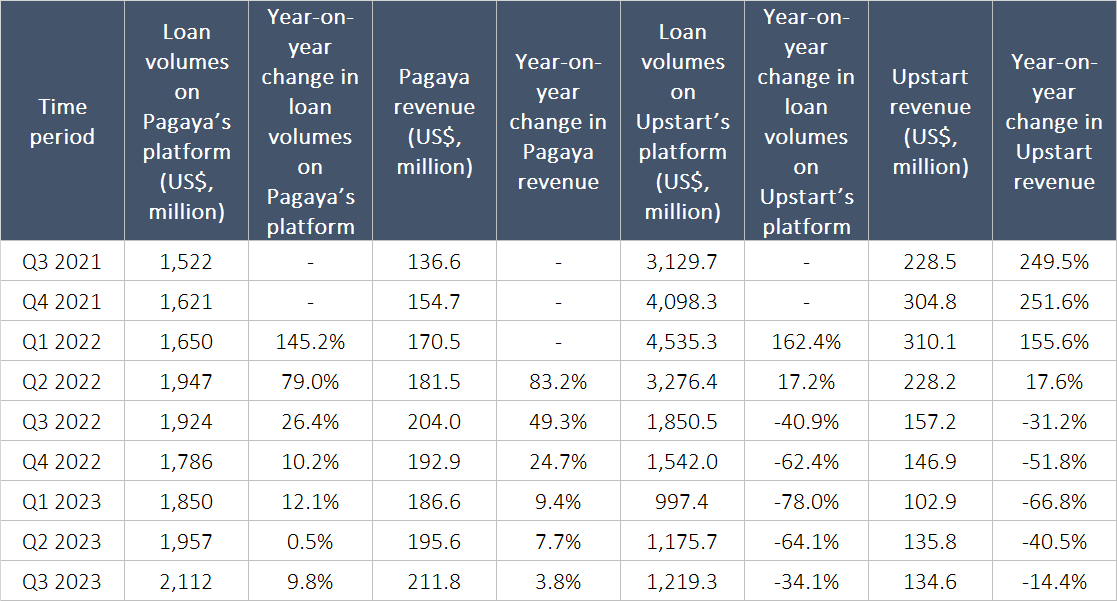

Pagaya Technologies (NASDAQ: PGY) is a company listed in the USA but headquartered in Israel. Similar to Upstart, Pagaya also provides lending software to financial institutions that uses AI to improve the institutions’ credit decisioning. But Pagaya raises pools of capital from institutional investors first – in what the company calls Financing Vehicles – before the company’s AI-powered platform is used to help originate loans. In this way, Pagaya ensures that there’s a ready pool of capital to fund growth in loans through its platform. Pagaya and Upstart’s business growth from the third quarter of 2021 to the third quarter of 2023 has been as different as night and day, as shown in Table 3.

Table 3; Source: Pagaya and Upstart regulatory filings

The impressive rise in Pagaya’s loan-volume at a time when Upstart struggled also raised further questions in our minds on the quality of the latter’s management team and AI credit models. Ever since Upstart’s management shared in the 2022 second-quarter earnings call that they are pursuing long-term funding commitments, Upstart has failed to make significant progress, apart from an announcement in the 2023 first-quarter earnings call (held in May) that more than US$2 billion in committed funding had been secured for the next 12 months.

Given all the above, we no longer have confidence that Upstart would be the high-growth and high-margin company we thought it was when we invested initially. When Upstart’s management team first said in August 2022 that they were going to pursue long-term funding commitments, we decided to give the company time. But our patience with management was eventually worn thin as we noticed that Pagaya continued to grow its loan volume while Upstart concurrently failed to sign up more partners and saw its loan volume carry on plummeting. Upstart’s stock price reflected the difficulties in its business, falling from US$195 at our initial investment (our weighted average purchase price was US$219, as we had added to Upstart on a few occasions after the initial investment) to our average sale price of US$26 when we exited last month. The big decline in Upstart’s stock price might lead someone reading this to ask: “Couldn’t you have sold Upstart earlier?” It’s a valid question. Our response will be something we shared in Compounder Fund’s Owner’s Manual:

“And on the topic of selling stocks, we will typically sell a stock in Compounder Fund’s portfolio if we find that the investment thesis is completely broken, or we have made a big mistake in our analysis. But we will be very slow to sell. The slowness is by design – it strengthens our discipline in holding onto the winners in Compounder Fund. Holding onto the winners will be a very important contributor to Compounder Fund’s long run performance.”

With our analysis of Upstart being wrong, we eventually decided to sell – after holding on for some time – and redeploy the capital in other companies that we think have brighter growth prospects and thus, return potential (in this case, the companies are Paycom Software and The Trade Desk).

And here’s an important disclaimer: None of the information or analysis presented is intended to form the basis for any offer or recommendation; they are merely our thoughts that we want to share. Compounder Fund owns shares in Paycom Software and The Trade Desk. Holdings are subject to change at any time