Compounder Fund: Sea Limited Investment Thesis - 22 May 2021

Data as of 20 May 2021

Sea Limited (NYSE: SE), which is headquartered in Singapore but listed in the USA, is one of the four companies in Compounder Fund’s portfolio that we invested in for the first time in April 2021. This article describes our investment thesis for the company.

Company description

Sea is a crown jewel of Singapore’s technology scene. Founded in 2009 as Garena Interactive Holding Limited, Sea has grown to become the largest company by market capitalisation among Singapore-headquartered companies (there was a name change that happened in April 2017). The Sea of today has three key businesses: Garena, Shopee, and SeaMoney.

Garena is Sea’s oldest business – started since the company’s inception – and it curates games from third-party developers, licenses these games for distribution to gamers across the world (mostly in Southeast Asia, other parts of Asia, and Latin America), and also localises the licensed games to suit gamers from different countries. Under its licensing contracts, Garena typically retains between 65% and 80% of gross billings (gross billings are the value of all virtual items sold by Garena’s games). Besides distributing games, Garena also develops its own games. Garena launched its first self-developed game, Free Fire (a mobile game of the battle royale genre), in December 2017. Free Fire has become a worldwide phenomenon – it was the most downloaded mobile game globally in 2020 (as well as in 2019), and was also the highest-grossing mobile game in India, Latin America, and Southeast Asia for the year.

Garena focuses on both mobile and PC online games and its games – both self-developed and licensed – span a wide variety of genres, including battle royale, multiplayer online battle arena, action role-playing games, massively multiplayer online role-playing games, and more. The Garena platform also has social features embedded within – such as user chats and online forums – and allows live streaming of online gameplay.

A key third-party game developer that Garena works with is the Chinese technology juggernaut, Tencent, which is also a major shareholder of Sea (Tencent controlled 22.9% of Sea’s outstanding shares as of 5 March 2021). Some of Garena’s most popular games, such as League of Legends, Arena of Valour, and Call of Duty: Mobile, are owned or developed by Tencent. In November 2018, Sea obtained a five-year right of first refusal from Tencent to distribute Tencent’s mobile and PC games in Taiwan and several South East Asian countries.

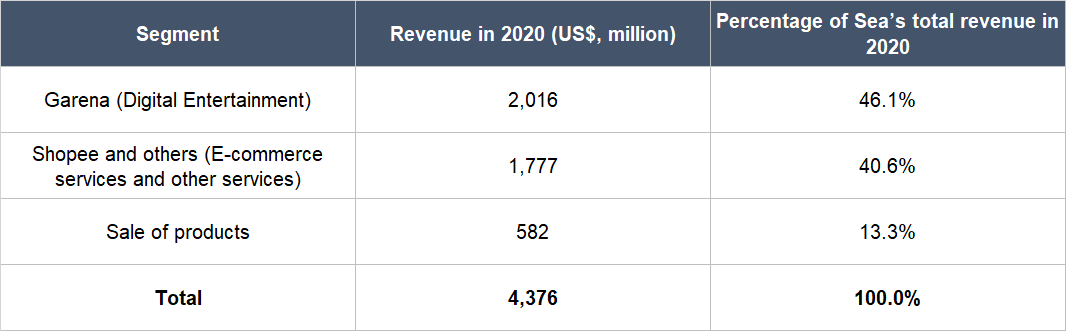

Garena’s user base has seen tremendous growth over the years and this is something we will discuss later. In 2020, Garena accounted for 46.1% of Sea’s total revenue of US$4.38 billion, or US$2.02 billion. Garena monetises its games with a freemium model – gamers can play its fully-functional games for free, but can also purchase virtual in-game items and season passes.

Shopee is Sea’s mobile-first e-commerce marketplace that connects buyers and sellers of products. It was first launched in June and July of 2015, in Taiwan and a number of Southeast Asian countries that includes Indonesia, Vietnam, Thailand, the Philippines, Malaysia, and Singapore. In 2019, Shopee entered Brazil, followed by Mexico in the first quarter of 2021. From as early as the first half of 2017, Shopee had become Southeast Asia’s largest e-commerce player in terms of gross merchandise volume (GMV) and total number of orders – this is a lead Shopee has held onto since. We will discuss Shopee’s rapid GMV and order growth over the past few years later.

Sea earns revenue from Shopee mainly by charging transaction fees and providing advertising and other value-added services. In 2020, these revenue sources from Shopee – together with relatively small revenues from SeaMoney and other services – collectively came up to US$1.78 billion and made up 40.6% of Sea’s total revenue for the year. Although Shopee is predominantly an e-commerce marketplace, Sea also purchases products directly from merchants and manufacturers and then sells them to consumers through Shopee. This revenue was US$582.4 million in 2020 and was 13.3% of Sea’s total revenue for the year.

The earliest incarnation of SeaMoney, which is Sea’s digital financial services arm, started operations in 2014. SeaMoney offers mobile wallet services, payment processing services, credit-related digital financial offerings, and other financial products. These services and products are offered by Sea under different brands (such as AirPay, ShopeePay, SPayLater, and more) in its different markets. In 2020, SeaMoney pulled in US$60.8 million in revenue. SeaMoney generates revenue from merchant commissions when its mobile wallet is used, and from the interest it earns from consumers from its credit products.

Source: Sea 2020 annual report

Sea counts Southeast Asia as its most important geography currently, with the region making up 63.8% of its total revenue in 2020. Latin America comes next at 18.1%, followed by the rest of Asia at 15.0%. Other parts of the world make up the remaining 3.1%. Latin America has become an increasingly important geographical market for Sea, with its contribution to Sea’s total revenue having increased from just 1.8% in 2018.

Investment thesis

We have laid out our investment framework in Compounder Fund’s website. We will use the framework to describe our investment thesis for Sea.

1. Revenues that are small in relation to a large and/or growing market, or revenues that are large in a fast-growing market.

We believe that Sea has tremendous growth opportunities ahead. If we look at Garena, Sea’s 2017 IPO prospectus (the company was listed in October 2017) mentioned that the online games market of Southeast Asia (including Taiwan) was expected to grow by nearly 20% per year from US$3.5 billion in 2016 to US$8.6 billion in 2021, according to Newzoo and Niko Partners. This is already huge compared to the size of Garena today – in the 12 months ended 31 March 2021, Garena pulled in revenue of US$2.43 billion. But Garena is not just in Southeast Asia. Its self-developed mobile game, Free Fire, is available in 130 markets globally and the game accounts for a “significant portion” of Garena’s overall revenue. According to Statista, the global mobile games market is expected to reach US$110 billion this year and rise by 10% annually to hit US$161 billion in 2025.

Garena also regularly organises esports events (in the hundreds, per year) and operates the largest mobile-game professional league in Southeast Asia, Taiwan, and Brazil. We think this makes Garena one of the key players in driving the growth of the nascent global esports market. Esports could be huge in the future – as an early sign of its progress, esports will be an official medal event for the first time ever at the Hangzhou 2022 Asian Games. Grandview Research estimates that the global esports market was US$1.1 billion in 2019 and could compound at an impressive annual rate of 24.4% from 2020 to 2027.

Garena has done a phenomenal job at growing its base of quarterly active users (QAU) and quarterly paying users (QPU). The two metrics have increased at annual rates of 80.2% and 85.8%, respectively, from the first quarter of 2015 to the first quarter of 2021. These are shown in the table below.

Source: Sea annual reports and earnings updates

We think it’s likely that Garena will continue to grow into the online/mobile games market in Southeast Asia and other parts of the world for two key reasons. First, as mentioned earlier, Sea currently has the right of first refusal to distribute Tencent’s games in Southeast Asia. The partnership allows Sea, as a distributor, to directly tap on Tencent’s own incredible track record of growing its online games business. But there’s more – the partnership could also be very useful for Sea in learning how to create hit games. For its part, Sea is continuing to expand its own game development capabilities. It acquired Canada-based Phoenix Labs, a developer of AAA games, in January 2020 for over US$150 million. Sea also had more than 750 game developers under its payroll at the end of 2020.

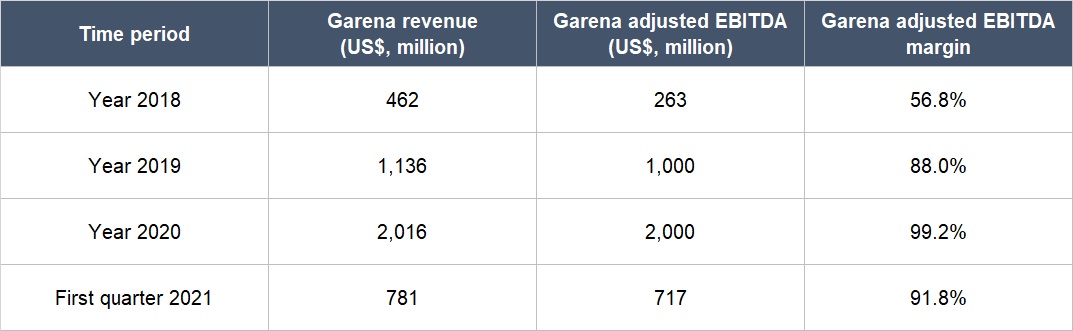

Second, Garena generates a tonne of cash. The table below shows a few things about Garena: Its rapid revenue growth over the past few years; its even more impressive growth in adjusted EBITDA (earnings before interest, taxes, depreciation, and amortisation); and its really high adjusted EBITDA margins (adjusted EBITDA as a percentage of revenue). The adjusted EBITDA can be taken to be a rough proxy for the cash flow produced by Garena. The cash flow can be invested for Garena’s own growth or for the growth of Sea’s other businesses. This brings us to Shopee, in which Sea has been funnelling Garena’s cash.

Source: Sea earnings updates

The e-commerce opportunities for Shopee in Southeast Asia and Latin America are huge. Let’s talk about Latin America first. In our August 2020 investment thesis for Latin American e-commerce powerhouse MercadoLibre, we discussed the potential growth of the region’s e-commerce market. It’s worth noting that our discussion mostly used numbers before the emergence of COVID-19. The pandemic has had a positive impact on the adoption of e-commerce in Latin America, so the growth opportunities today are even brighter than when we first published our thesis. We wrote:

“According to a June 2020 report from market researcher eMarketer, e-commerce sales in Latin America was US$70.1 billion in 2019, and represented just 4.4% of total retail sales in the region. For perspective, e-commerce was 11.8% of total retail sales in the US in the first quarter of 2020. eMarketer also expects the Latin America e-commerce market to compound at 13.5% annually from 2019 to US$116.2 billion by 2023.

Forrester, another market research firm, produced a report in August 2019 and stated that the e-commerce market in Latin America’s six largest economies – that would be Argentina, Brazil, Chile, Colombia, Mexico, and Peru, which are all countries that MercadoLibre is active in – to grow by more than 22% annually from 2018 to 2023.

The projection of high growth for Latin America’s e-commerce space is reasonable in our eyes for two reasons.

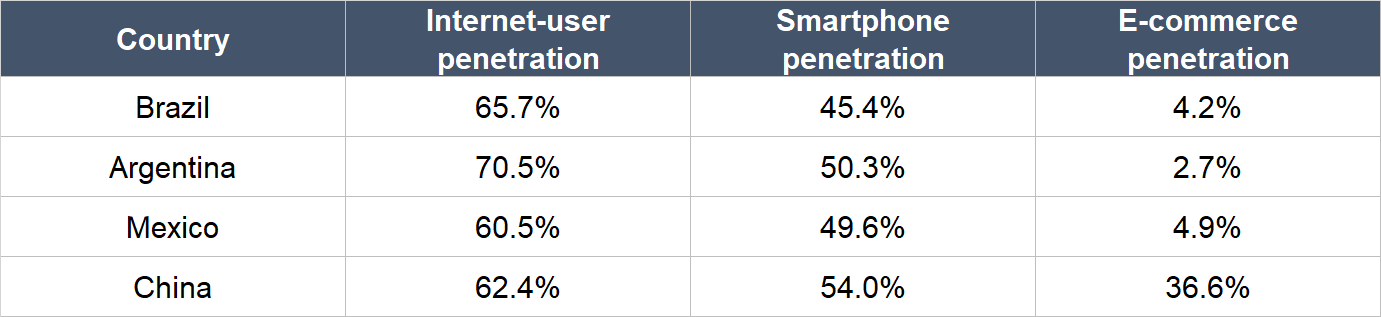

First, there’s the aforementioned low penetration rate of online retail in Latin America’s overall retail scene. It’s worth noting too that despite Brazil, Argentina,and Mexico (MercadoLibre’s three largest markets) having similar internet-user and smartphone penetration rates as China, online retail is a much higher percentage of total retail in the Asian giant; the data you see in the table below came from a MercadoLibre presentation in 2019.

Source: MercadoLibre dataSecond, internet penetration rates in Latin America are still relatively low: 86.0% of the US population in 2019 currently has access to the internet, which is much higher than in Brazil, Argentina, and Mexico. For another perspective, Latin America has a population of around 640 million people, but has internet users and online shoppers of merely 362 million and 200 million, respectively.”

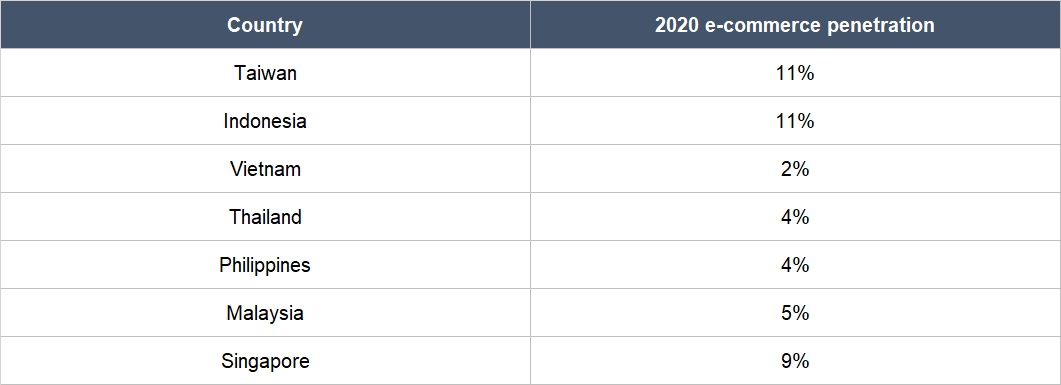

Coming to Southeast Asia, the region’s e-commerce penetration rates are also very low, just like they are in Latin America. Using data and estimates from Euromonitor, Morgan Stanley Research, and the e-Conomy SEA 2020 Report prepared by Bain, Google, and Temasek, here are the recent e-commerce penetration rates for Shopee’s key Southeast Asian markets (including Taiwan):

Shopee has done an admirable job over the past few years in (1) growing its GMV and orders handled, and (2) improving its take rate, which is the revenue it earns as a percentage of the GMV it facilitates. These are shown in the table below.

Source: Sea annual reports and earnings updates

We believe that Shopee can continue to take advantage of the growth opportunities in the e-commerce markets of Southeast Asia and Latin America. There have been a number of interesting things Shopee has done to fuel its past growth and we think these are strong positive signs on the innovative thinking and execution chops that Sea’s management possesses. They are:

- Shopee has had a mobile-first approach since its inception. This is important because it’s more common for Asians to access the internet through mobile. According to Statcounter GlobalStats, 65% and 64% of internet usage in Asia in December 2016 and March 2021, respectively, was through mobile – globally, the selfsame percentages are 50% and 54%.

- Shopee employs gamification elements in its user experience, which Sea believes helps in increasing Shopee’s organic user acquisition and user retention. The following are some of Shopee’s gamification features: (a) Shopee Coins can be used to offset the price of purchases and users can earn coins by making purchases, playing mini-games, participating in campaign activities, and/or inviting friends to participate in Shopee; (b) Shopee Live allows buyers to watch sellers livestream themselves to promote products or interact with buyers; (c) Shopee Games are mini-games that promote in-app interactions between Shopee users; (d) Shopee Feed is a continuous-scroll of multimedia listings of products that allow buyers to “follow” their favourite sellers and to “like” or “comment” on product listings.

- Shopee introduced the Shopee Guarantee feature, where it holds a buyer’s payment in escrow until products are received, to reduce e-commerce friction in Southeast Asia between buyers and sellers.

- Shopee has also advertised aggressively and intelligently, such as by using local celebrities as spokespeople. We think such moves appeal to the consumers in the markets that Shopee is targeting and helps Shopee to win mindshare and generate virality.

- Speaking of using local celebrities, Shopee has also been taking a hyper-local approach. Sea’s management team does not view Southeast Asia as one homogenous market. Instead, they recognise – correctly – that the e-commerce market of each country in the region has its unique characteristics and they run Shopee with this recognition in mind. Two examples: (a) Shopee offers seven different versions of its app and has different payment options for different countries; (b) Shopee launched Shopee Barokah in Indonesia to provide Shariah-compliant products and services to meet the needs of Muslim users in the country.

- Shopee has spared no expense in subsidising promotions and shipping fees, even to the extent where the e-commerce business had negative gross margins for a number of years. This is where Garena’s cash flow comes into play, as it provides the fuel for Sea to invest into Shopee. Although heavy subsidies are not sustainable over the long-term, it has enabled Shopee to win market share.

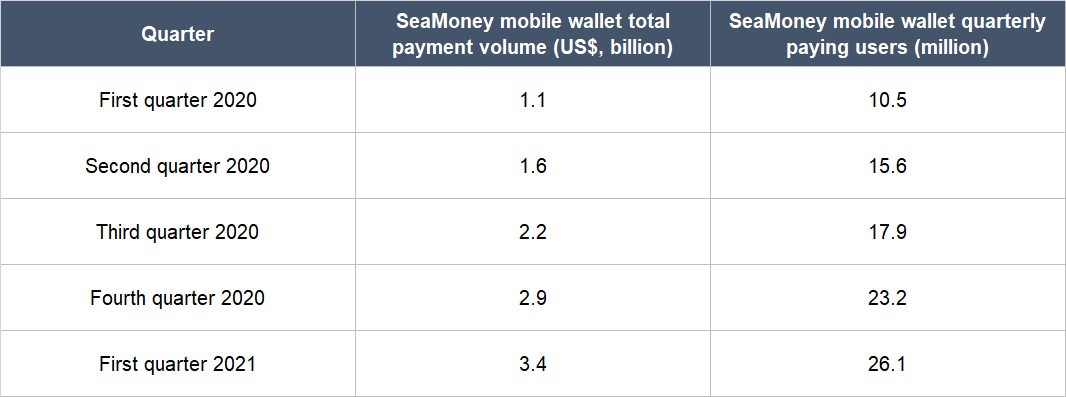

Meanwhile, the market opportunity for SeaMoney, while hard to pin down precisely, is also likely to be immense. This is because Southeast Asians lack access to traditional financial services, which provides a massive opening for providers of digital financial services to win users. According to an October 2019 report by Bain, Google, and Temasek, more than 70% of Southeast Asia’s adult population is unbanked or underbanked. For its part, SeaMoney has done a tremendous job in growing its payment volume and mobile wallet users in recent quarters. This is illustrated in the table below.

Source: Sea annual reports and quarterly earnings update

We want to highlight two other positive things about SeaMoney. First, in December 2020, Sea was selected by the Monetary Authority of Singapore for the award of a digital full bank license. If Sea does end up with the license, SeaMoney could offer even more financial services to users. Second, SeaMoney has an advantage over other digital financial services providers: Sea can easily expose SeaMoney to users of Garena and Shopee.

An important point we want to make about Sea’s growth opportunities is that we think the company exhibits optionality in spades. We first heard of the term “optionality” from The Motley Fool’s co-founder, David Gardner. It’s a term he coined to describe the trait a company has of being able to evolve and find entirely new ways to grow. Sea’s history of building SeaMoney in 2014 and Shopee in 2015 is a testament to the company’s optionality. Sea started with Garena, an online/mobile gaming business, while SeaMoney and Shopee are in digital financial services and e-commerce, respectively – these have no strong connections to online/mobile gaming.

But more importantly, now that huge swathes of Southeast Asia’s population are using Shopee (inferred from Shopee’s high order-volumes), the e-commerce app could be the springboard for Sea to build a super-app that offers a wide variety of digital services to users in the region. In this area, Sea has an excellent mentor to learn from – its major shareholder, Tencent. The Chinese technology juggernaut has excelled with developing its own super-app, WeChat, in China.

Sticking with Sea’s optionality, Free Fire could also expose the company to the potential of the Metaverse. In our recent investment thesis for Tencent, we explained what the Metaverse is and the economic opportunities it could potentially unlock, so we are not repeating the discussion here. But in short, the Metaverse is something like a pervasive virtual world that is interlinked with the real world. During Sea’s recent 2021 first quarter earnings conference call, management said that the company is “developing [Free Fire] to a social platform where people not only come to play the core gameplay but also enjoy other modes, hang out, listen to music, socialize.” This sounds like Free Fire could, in the future, be a game that intermingles the physical and virtual lives of its users.

2. A strong balance sheet with minimal or a reasonable amount of debt

We think Sea has a robust balance sheet. The company exited the first quarter of 2021 with US$5.75 billion in cash and equivalents, and just US$1.76 billion in total debt (in the form of convertible notes). This gives rise to a net-cash position of US$4.0 billion.

For the sake of conservatism, we note that Sea has total operating lease liabilities of US$256.4 million. But this is still dwarfed by the company’s net-cash position.

3. A management team with integrity, capability, and an innovative mindset

On integrity

Sea’s chairman and CEO is the 43-year old Forrest Li Xiaodong. He is Sea’s founder and has been in his current roles since the company’s inception. We appreciate the fact that Li has more than a decade of leadership experience at the company despite his young age. The other important leaders of Sea are Ye Gang, who’s the chief operating officer, and Chris Feng Zhiming, who’s the keyman leading the charge at Shopee and SeaMoney. Both men are young like Li (Ye is 40 and Feng is 38), and each have multi-year tenure at Sea (Ye joined in March 2010 while Feng joined in March 2014) – these are traits we like.

There is very little detail we can find on Sea’s compensation structure for its top leaders. But we’re comfortable with what we know. The following table shows the total compensation received by Sea’s executive officers and directors in each year for 2018 to 2020 (there’s no longer record to look at, since Sea was listed only in October 2017). The cash awards have not grown much, despite Sea’s business having grown by leaps and bounds. For perspective, Sea’s revenue quintupled from US$827.0 million in 2018 to US$4.38 billion in 2020 and its free cash flow margin (free cash flow as a percentage of revenue) improved markedly from -81.5% to 4.5% over the same period. Meanwhile, the number of stock options and restricted stock units that were granted are not egregious when compared to the number of the company’s shares that exist at the end of each year.

Source: Sea annual reports

We also want to highlight positively that Li has significant skin in the game. As of 5 March 2021, Li owns 59.596 million Sea shares (including options that could be exercised within 30 to 60 days of the date). At Sea’s 20 May 2021 share price of US$246, Li’s stake is worth more than US$14 billion.

It’s worth noting that Sea has two share classes: (1) Class B, which are not traded and hold three voting rights per share; and (2) Class A, which are publicly traded and hold just one vote per share. Li’s 59.596 million Sea shares are split into 14.068 million Class A shares and 45.528 million Class B shares. Li controls 37.7% of Sea’s overall voting power as of 5 March 2021, even though he owns ‘only’ 11.5% of the company’s shares. The difference can be explained by two things. First, there’s the difference in voting power between Sea’s two share classes. Second, Li controls the voting rights for some Sea shares that he does not own; for example, Tencent had pledged its voting rights to Li for 46.574 million Sea Class B shares. A manager having significant control over the company can potentially be bad for shareholders. This concentration of Sea’s voting power in the hands of Li means that we need to be comfortable with him at the company’s helm. We are.

We’ve seen an article published a few years ago, which has since been taken down, about the way Li had apparently usurped control of an earlier incarnation of Sea and of the title of “Founder”. We’re unable to determine the veracity of this version of Sea’s founding story. But what we do know is that since Sea’s IPO, we’ve not seen any action by the company that would cause us to question management’s integrity.

On capability and ability to innovate

We rate Forrest Li and his team very highly on this front. The following are examples we shared earlier in this article on the excellent innovation and execution that Sea’s management team has displayed (further commentary from us that we’re mentioning for the first time in this article are given in square brackets):

- Garena’s robust user growth in the past few years.

- The launch of Garena’s self-developed game, Free Fire, in December 2017. [Free Fire had, and continues to have, a significant positive impact on Garena’s growth. For perspective, Garena’s revenue growth rate increased from 11.3% in 2017 to 26.6% in 2018, then to 145.6% in 2019, and 77.5% in 2020.]

- Shopee’s rapid ascension to become the top e-commerce marketplace in Southeast Asia by GMV, and its incredible growth in GMV and order-count from 2016 to the first quarter of 2021. [Revenue from Sea’s e-commerce and other services (this includes Shopee’s marketplace activities and other services such as SeaMoney) grew from just 5.1% of Sea’s overall revenue in 2016 to 40.6% in 2020. This signifies the incredible execution by Chris Feng, who has effectively been the CEO of Shopee since its launch. Before joining Sea in March 2014, Feng was part of the Southeast Asia founding team at Rocket Internet, an European company known for developing successful internet businesses. Feng helped Rocket Internet build companies such as online retailer Zalora and the Southeast Asian-focused e-commerce marketplace, Lazada, which was acquired by Alibaba in 2016. Feng has been instrumental in Shopee’s growth thus far. For instance, he pushed Shopee to play offense in 2018 after he sensed that Lazada was in disarray because of internal conflicts. Equally important to Shopee’s growth was Li’s decision to hire Feng and provide support for Feng’s efforts.]

- Shopee’s mobile-first and hyper-local approach, and introduction of gamification features.

- Latin America’s increasing contribution to Sea’s overall revenue, from a 1.8% share in 2018 to an 18.1% share in 2020. [The sharp rise in Sea’s revenue from Latin America in that period – a surge from US$14.7 million to US$790.3 million – coincided with the launch of Shopee in Brazil in the fourth quarter of 2019. This is once again a testament to Feng’s incredible ability to execute.]

- Garena’s willingness to also adopt a hyper-local approach. [We believe that this has been a key driver of Garena’s growth, as the gaming platform is able to adapt games to suit local preferences, hence opening up new user bases for many games.]

- The willingness to invest Garena’s cash into Shopee and tolerate the cash-burn there. [We don’t think it’s easy for any company to use the cash from a cash-generative business to invest in another one that will be incinerating cash in the shorter-term. Such a move takes patience and a long-term vision and impressively, it is something Sea’s management has excelled in.]

- Striking up a partnership with Tencent.

One area where Sea’s management team does not appear to have done too well is building a good corporate culture. Glassdoor is a platform that allows employees to rate their companies anonymously. Currently, only 64% of Sea raters on Glassdoor would recommend a friend to work at the company. We have also heard anecdotes about Sea’s culture of having long work hours and frequent overtime. The good thing is that Li has an 88% approval rating as CEO, which is higher than the average Glassdoor CEO rating of 69% in 2019.

4. Revenue streams that are recurring in nature, either through contracts or customer-behaviour

We believe that Sea’s three key businesses each enjoy recurring revenue from customer behaviour:

- Garena has an already-huge and still rapidly growing base of users who buy season passes and virtual in-game items – these are purchases that are likely to be repeated over time.

- Shopee facilitated 2.7 billion transactions in 2020 and the products that are bought mostly belong to the categories of fashion, health and beauty, home and living, and baby products – these are products that consumers tend to purchase repeatedly.

- For SeaMoney, digital financial services, such as mobile wallets, are likely to be used frequently. Earlier, we also shared data showing that SeaMoney has a healthy level of usage – it handled US$10.1 billion in payment volume in the 12 months ended 31 March 2021 and had 26.1 million paying users in the first quarter of this year.

5. A proven ability to grow

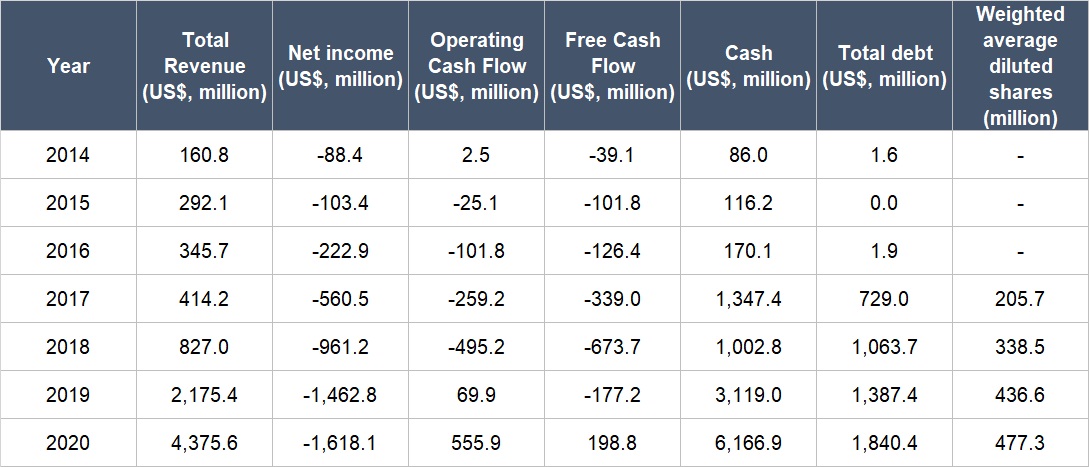

The table below shows Sea’s key financial figures from 2014 (the earliest we could find, since the company’s IPO was in October 2017) to 2020.

Source: Sea annual reports

A few key things to highlight from Sea’s historical financials:

- Revenue has compounded at an astounding annual rate of 73.4% from 2014 to 2020. Growth rates in more recent years have been even faster: 119.4% per year for 2017-2020, and 101.1% in 2020.

- Net income was negative all the way, and had deepened significantly from -US$88.4 million in 2014 to -US$1.62 billion in 2020. But the net income margin (net income as a percentage of revenue) had improved from -55.0% to -37.0% over the same period. The improvement from 2017 to 2020 is even more pronounced, as the net income margin stepped up from -135.3% to -37.0%.

- Sea’s operating cash flow was mostly negative, but 2019 marked a turning point for the company as it started producing positive operating cash flow again. The metric saw a significant surge in 2020 too. Sea’s operating cash flow margin (operating cash flow as a percentage of revenue) also improved markedly from 2017 to 2020, rising from -62.6% to 12.7%.

- Sea’s free cash flow was mostly negative as well – it only turned positive in 2020. In a similar manner to the operating cash flow margin, Sea’s free cash flow margin (free cash flow as a percentage of revenue) also increased significantly from -81.8% in 2017 to 4.5% in 2020.

- Sea has kept its balance sheet strong for the timeframe we’re studying, as cash on hand was substantially higher than total debt for all years except 2018 – and even then, the amount of cash and investments was nearly equal to the amount of debt.

- We only started looking at Sea’s share count since 2017 because it was listed in October of the year. At first glance, Sea’s number of shares appeared to increase significantly by 64.5% from 2017 to 2018. But the number we’re using is the weighted average diluted share count. Right after Sea got listed, it had a share count of around 327 million. This means that the increase in 2018 was much milder at around 4%. From 2018 to 2020, Sea’s weighted average diluted shares increased by 18.7% per year. This was partly because Sea issued 69 million shares in 2019 and 15.18 million shares in 2020 to raise US$1.5 billion and US$3.0 billion, respectively. This rate of dilution is much higher than what we typically like to see. But at the same time, as long as Sea’s business grows at a much faster pace than its diluted share count, there will be a positive impact on shareholder value. For perspective, Sea’s revenue grew by 130.1% per year from 2018 to 2020. Nonetheless, we will be watching Sea’s dilution in the future.

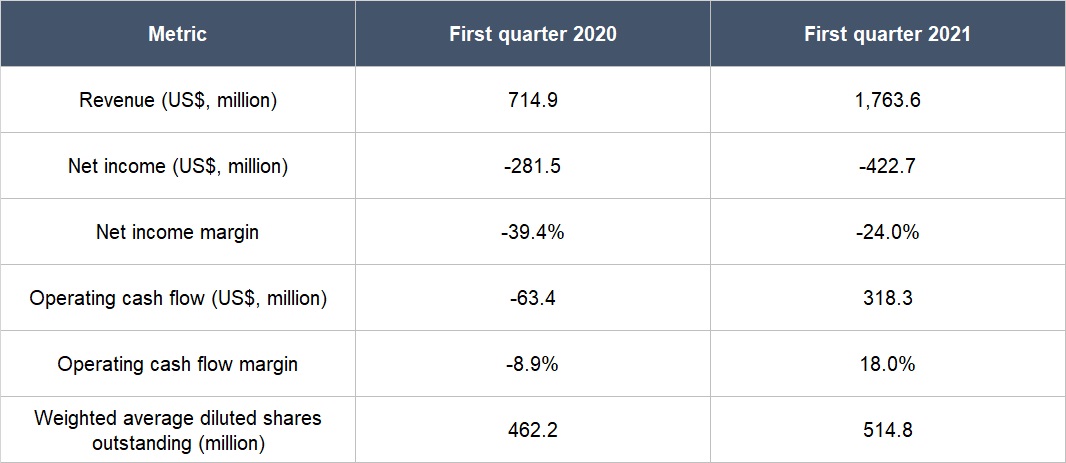

Sea posted impressive year-on-year revenue growth of 146.7% for the first quarter of 2021, as illustrated in the table below. At first glance, Sea’s net income looks bad as it went deeper into the red. But the net income margin actually improved from -39.4% a year ago to -24.0%. Meanwhile, Sea’s cash flow picture looks much better, as operating cash flow climbed from -US$63.4 million a year ago to US$318.3 million, with the operating cash flow margin rising from -8.9% to 18.0%. The company’s weighted average diluted share count again increased at a high rate of 11.4%. But the good thing is that this is dwarfed by Sea’s revenue growth.

Source: Sea 2021 first quarter earnings update

6. A high likelihood of generating a strong and growing stream of free cash flow in the future

This is perhaps the biggest question mark around Sea. Garena is raking in cash and likely has a high free cash flow margin (we mentioned earlier that Garena has produced very high adjusted EBITDA margins in the past few years). But Shopee is burning cash. In 2020, Sea’s e-commerce and other services segment (this includes Shopee’s marketplace and other services such as SeaMoney) had a gross margin of just 1.9%, despite having substantial revenue of US$1.78 billion.

But a key reason why Shopee is burning cash at the moment is that it’s spending heavily on promotions and subsidies to win market share. We believe that these initiatives can be scaled back in the future, as Shopee wins customer loyalty and stronger mindshare. Moreover, Shopee can also increase its overall take-rate in the future by (1) introducing more useful digital services for sellers and buyers, and/or (2) charge higher commissions but still make its marketplace attractive for sellers by attracting more buyers. Earlier, we shared that Shopee’s take rate has been increasing over the past few years. A higher take-rate for Shopee will result in more revenue per order, which could result in operating leverage. We’re already seeing signs of this happening. The table below shows the operating loss that Sea incurs per e-commerce order that it fulfills, and it’s clear that the operating loss per order has been improving over time.

Source: Sea annual reports and quarterly earnings update

(The operating loss per order is calculated by taking the operating loss of both Shopee’s marketplace activities and Sea’s first-party e-commerce sales and dividing it by the number of orders handled by the Shopee marketplace.)

There’s also at least one precedent of an e-commerce marketplace generating high free cash flow margins at maturity. eBay, which was founded in 1995 and runs an e-commerce marketplace in the USA and other parts of the world – had an average free cash flow margin of 24% from 2016 to 2020, the years after it separated from PayPal.

Valuation

We completed our initial purchases of Sea shares in early April 2021. Our average purchase price was US$235 per share. At our average price and on the day we completed our purchases, Sea’s shares had a trailing price-to-sales (P/S) ratio of around 26. We like to keep things simple in the valuation process. In Sea’s case, we think the P/S ratio is currently an appropriate metric to gauge the value of the company, since it has yet to generate much free cash flow for a sustained period of time.

The P/S ratio of 26 is high and that’s a risk. For context, if we assume Sea has a 20% free cash flow margin today, the P/S ratio translates to a price-to-free cash flow (P/FCF) ratio of 130 (26 divided by 20%). But we think the company has years of rapid growth ahead of it. Sea is currently participating – and excelling – in the high-growth markets of online/mobile gaming, e-commerce, and digital payments in Southeast Asia and Latin America. Importantly, we also think that Sea has very strong optionality because its services command huge user bases (which greases the wheel for Sea to introduce new digital services in the future), and its management team has proven to be excellent at innovation.

For perspective, Sea carried a P/S ratio of around 23 at its 20 May 2021 share price of US$246.

The risks involved

There are a few risks that we think could capsize our investment in Sea:

- Key-man risk: We rate Forrest Li, Ye Gang, and Chris Feng highly. They are the architects behind Sea’s success thus far. Should either or all of them leave, we will be watching the leadership transition. The good thing is that the trio are still young (Li is 43, Ye is 40, and Feng is 38), so they should still have plenty of gas left in the tank to continue leading Sea in the years ahead.

- Product-concentration risk: As mentioned earlier, Garena’s self-developed game, Free Fire, has been a breakout hit and now accounts for a “significant” portion of Garena’s revenue. In fact, Garena’s top five games (where Free Fire is likely the top game) accounted for 95.6% of its revenue in 2020. Although we think Free Fire still has plenty of room to grow – especially with management’s intent to introduce heavy social interactivity elements into the game – Garena will need to launch new games in the future eventually. The good thing, as we already discussed, is that Garena is building its game development capabilities. During Sea’s 2020 fourth-quarter earnings call, Li said that Phoenix Labs, the AAA gaming studio Sea acquired in January 2020, will be expanding. Phoenix Labs announced new offices in Montreal and Los Angeles alongside its existing bases in Vancouver and Seattle.

- Partnership risk: Of Garena’s top five games in 2020, if we exclude Free Fire, all or most of them are likely to be games that belong to Tencent, such as League of Legends, Arena of Valor, and Call of Duty: Mobile. Earlier, we brought up that Sea has a five-year right of first refusal with Tencent to distribute Tencent’s games in the Southeast Asia region. There’s no guarantee that Sea will be granted an extension when the contract expires in 2023. But Tencent owns a 22.9% stake in Sea (as of 5 March 2021), so the former has a powerful economic interest to continue supporting the latter. At Sea’s 20 May 2021 share price of US$246, Tencent’s stake is worth US$29 billion.

- Voting power risk: But Tencent’s large interest in Sea comes with a drawback – the Chinese technology company has a heavy influence on Sea’s decision-making. As of 5 March 2021, even after ceding some voting power to Li, Tencent still controls 23.3% of Sea’s votes. The relationship between Tencent and Sea has so far been positive. But if the two companies fall out in the future, Tencent’s voting power in Sea could become a stumbling block to Sea’s growth.

- Intense competition: Shopee has no shortage of competition. For example, it competes with Lazada and Tokopedia in Southeast Asia, momo.com in Taiwan, and MercadoLibre in Latin America, among others. South Korea’s largest e-commerce company, Coupang, also recently set its sights on Singapore and possibly the rest of Southeast Asia. Although Shopee has been growing rapidly, any increase in the intensity of competition could drive down margins and prolong its cash burn. We will be watching how the e-commerce wars unfold.

- Cash-burn risk: Sea currently has a robust balance sheet and is starting to generate positive operating cash flow and free cash flow. But the company had been burning cash in the past. If Sea does so again in the future, it will need to raise capital. Sea’s shareholders could face significant dilution if the company needs to raise money at a time when conditions in the capital markets are poor. We believe that Sea will eventually be able to generate substantial free cash flow, but only time will tell. Moreover, Sea’s need for serious cash may come before its cash flow muscles shape up.

- Currency risk: Sea reports its financials in the US dollar, but it conducts business mostly in the prevailing currencies of the countries it’s in. This means the company is exposed to adverse currency movements in these countries. Unfortunately, the currencies of the countries that Sea is in have historically been weak. For example, we can look at the top three countries by population in Southeast Asia: Indonesia, the Philippines, and Vietnam. Over the 10 years ended April 2021, the Indonesian rupiah, the Filipino peso, and the Vietnamnese dong had declined by around 40%, 10%, and 10%, respectively, against the US dollar. In Latin America, a key market for Sea is Brazil. The Brazilian real fell by over 70% against the US dollar over the same period.

- Valuation risk: We think Sea’s business is likely to grow at a rapid clip for many years and so it deserves its premium valuation. But if there are any hiccups in Sea’s business – even if they are temporary – there could be a painful fall in the share price. This is a risk we’re comfortable taking as long-term investors.

Summary and allocation commentary

To summarise Sea, it has:

- Huge and growing market opportunities in the online/mobile gaming, e-commerce, and digital payments space in Southeast Asia and Latin America; moreover we think the company has a high chance of finding completely new ways to grow in the future.

- A robust balance sheet with significantly more cash than debt.

- A management team that has had reasonable compensation over the past few years (thus demonstrating their integrity) and an excellent track record with execution and innovation.

- High levels of recurring revenues from customer behaviour.

- A history of impressive revenue growth; the company also recently started generating positive operating cash flow and free cash flow.

- A good chance of being able to produce strong free cash flow in the future.

As it is with every company, there are risks to note for Sea. The main ones we’re watching include key-man risk; Sea’s reliance on Free Fire; the company’s relationship with Tencent; competitive pressure; the chance of shareholders facing significant dilution; the possibility that Sea may never be able to produce strong free cash flow; the risk of adverse currency movements in the countries that Sea is operating in; and the company’s high valuation.

After weighing the pros and cons, we decided to initiate a position of around 1.5% in Sea in April 2021, which can be considered to be a medium-sized allocation. We appreciate all the strengths we see in Sea’s business, but our enthusiasm is tempered by the company’s high valuation and the cash-burn at Shopee.

And here’s an important disclaimer: None of the information or analysis presented is intended to form the basis for any offer or recommendation; they are merely our thoughts that we want to share. Of all the other companies mentioned in this article, Compounder Fund also owns shares in Alphabet (parent of Google), Coupang, MercadoLibre, Paypal, and Tencent. Holdings are subject to change at any time.