Compounder Fund: PayPal Investment Thesis - 07 Aug 2020

Data as of 1 August 2020

PayPal Holdings (NASDAQ: PYPL) is one of the 40 companies in Compounder Fund’s initial portfolio. This article describes our investment thesis for the company.

Company description

PayPal was first listed in the US stock market in February 2002, but it was acquired by e-commerce site eBay just a few months later. The acquisition made sense for PayPal, as the company could tap on eBay’s larger network of users and gross merchandise volume.

Interestingly, PayPal outgrew eBay over time. Eventually, PayPal was spun off by eBay in mid-2015 through a new IPO. On the day of PayPal’s second listing, its market capitalisation of around US$47 billion was larger than eBay – and has since nearly quintupled.

It’s likely that even for us living in Singapore, we have come across PayPal’s online payment services. But there is more to the company. PayPal’s payments platform includes a number of brands – PayPal, PayPal Credit, Braintree, Venmo, Xoom, and iZettle – that facilitate transactions between merchants and consumers (and also between consumers) across the globe. The platform works across different channels, markets, and networks.

PayPal recently added discount-discovery services for consumers to its portfolio. It announced a US$4 billion acquisition of Honey in November 2019 that closed in January 2020. According to PayPal, Honey “helps consumers find savings as they shop online.” At the time of acquisition, Honey had around 17 million monthly active users, partnered with 30,000 online retailers across various retail categories, and had helped its user base find more than US$1 billion in savings in the last 12 months.

PayPal’s revenue comes primarily from taking a small cut of its platforms’ payment volume. This transaction revenue accounted for 90.6% of PayPayl’s net revenue of US$17.8 billion in 2019. Other business activities including partnerships, subscription fees, gateway fees, service-related fees, and more (collectively known as other value added services) comprise the remaining 9.4% of PayPal’s net revenue.

The US was PayPal’s largest country by revenue in 2019 with a 53.0% share. In a distant second is the UK, with a weight of 10.5%. No other single country made up more than 10% of the company’s net revenue.

Investment thesis

We have laid out our investment framework in Compounder Fund’s website. We will use the framework to describe our investment thesis for PayPal.

1. Revenues that are small in relation to a large and/or growing market, or revenues that are large in a fast-growing market

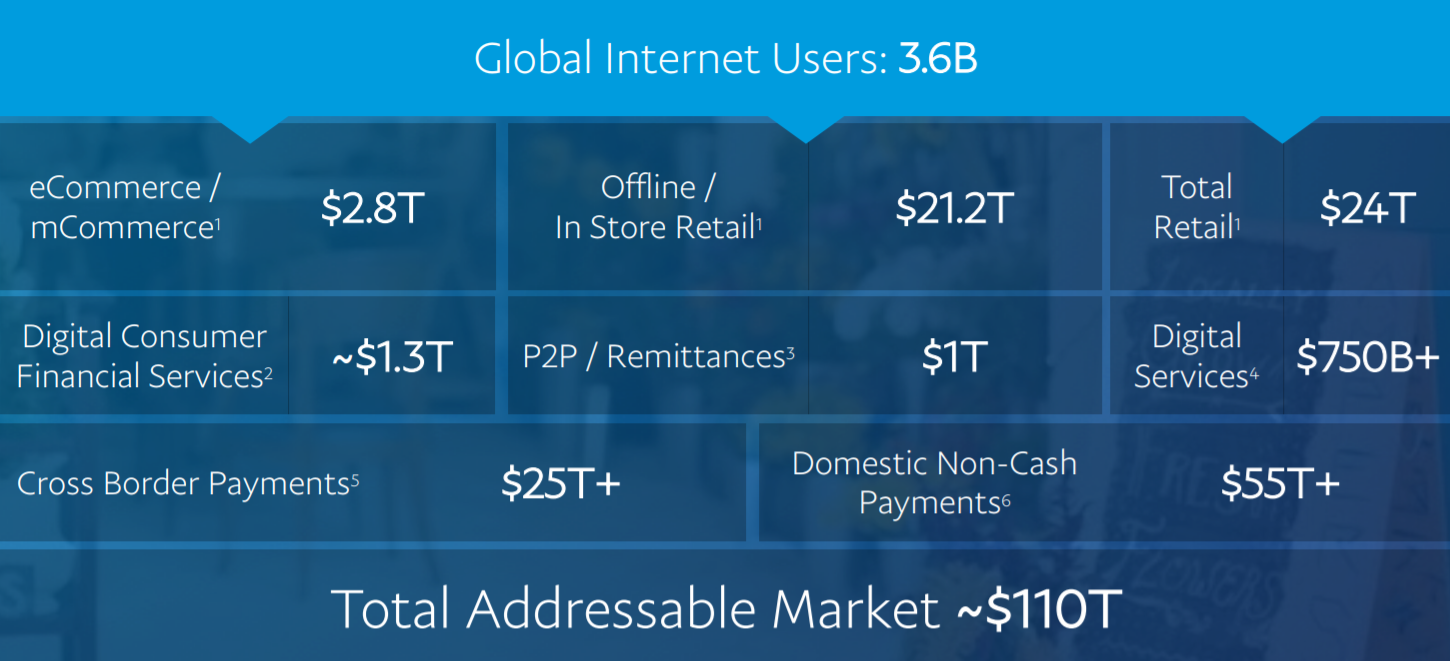

PayPal’s business is in digital and mobile payments. According to a 2018 PayPal investor presentation, this market is worth a staggering US$110 trillion, as shown in the chart below. For context, PayPal raked in just US$17.8 billion in revenue in 2019 based on US$712 billion (or just US$0.712 trillion) in payment volume that flowed through its platform.

Source: PayPal presentation

Around 80% of transactions in the world today are still settled with cash, which means digital and mobile payments still have low penetration. And this spells opportunity for PayPal.

2. A strong balance sheet with minimal or a reasonable amount of debt

PayPal’s balance sheet looks rock-solid at the moment, with US$8.9 billion in debt against US$13.0 billion in cash and short-term investments (consisting of US$6.35 billion in cash and equivalents and US$6.70 billion in short-term investments) as of 30 June 2020. Moreover, PayPal has a storied history of producing strong free cash flow which we’re going to discuss later.

3. A management team with integrity, capability, and an innovative mindset

On integrity

PayPal’s key leader is CEO Dan Schulman, who’s 62 this year. In 2019, 85% to 88% of the compensation for PayPal’s key leaders (including Schulman and a handful of other senior executives) came from the following:

- Stock awards that vest over a three-year period

- Restricted stock awards that depend on the growth in PayPal’s revenue and free cash flow over a three-year period

PayPal’s compensation structure for its key leaders has emphases on free cash flow, and multi-year-vesting for stock awards (which means a dependence on the company’s long-term share price movement). We think this structure is well designed and aligns Compounder Fund’s interests as a shareholder with the company’s leaders.

Moreover, PayPal requires its CEO and other senior executives to hold shares that are worth at least six times and three times their respective base salaries. So there’s skin in the game for PayPal’s leaders. As of 27 March 2020, Schulman himself controlled 596,803 PayPal shares that are collectively worth around US$117 million at the share price of US$196 as of 1 August 2020; other members of the company’s senior management team each controlled around US$6.6 million to US$43.7 million worth of shares.

On capability and innovation

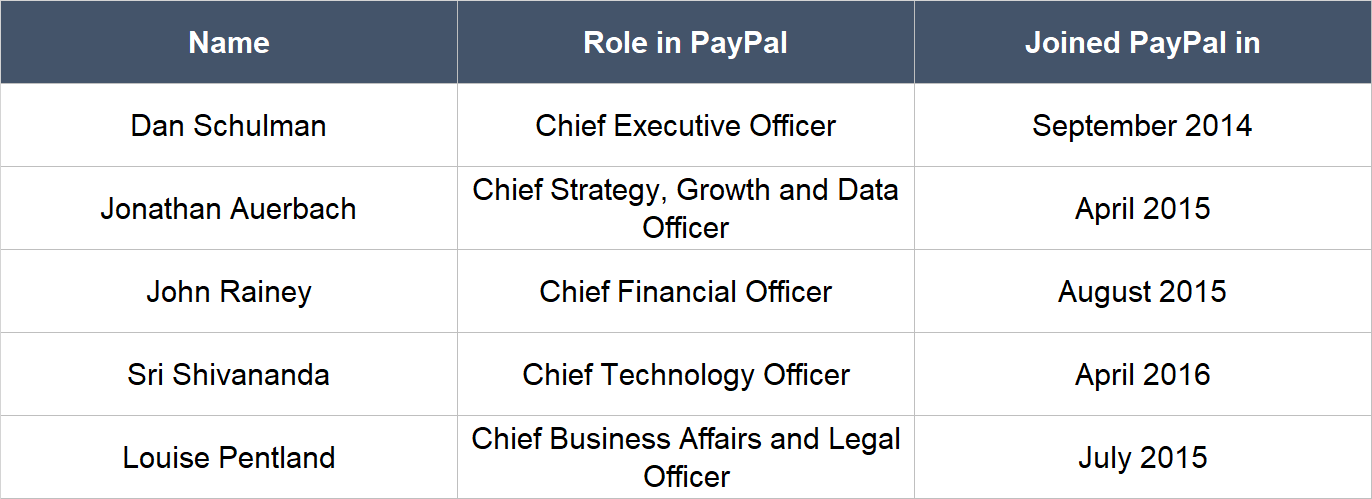

Some members of PayPal’s senior management team have relatively short tenures with the company, as illustrated in the table below. But together, they have accomplished plenty since PayPal’s separation from eBay

Source: PayPal website, and other press releases

First, the company has grown its network of users impressively since the spin-off. The table below shows how PayPal’s transactions, payments volume, and active accounts have changed from 2014 to 2019.

![]()

Source: PayPal IPO document, annual reports, and quarterly filings

Second, PayPal has made a number of impressive acquisitions and business deals in recent years under Schulman. They are:

- The acquisition of digital international money-transfer platform Xoom in November 2015 for US$1.1 billion; Xoom’s money-transfer network covers 160 countries.

- The September 2018 acquisition of iZettle, a provider of solutions to small businesses for the acceptance of card payments and sales management and analytics,for US$2.2 billion). PayPal acquired iZettle to strengthen its payment capabilities in physical stores and provide better payment solutions for omnichannel merchants. We believe that a retailer’s ability to provide a seamless omnichannel shopping experience is crucial in today’s environment. When iZettle was acquired, it operated in 12 countries across Europe and Latin America, and was expected to deliver US$165 million in revenue and process US$6 billion in payments in 2018.

- The aforementioned acquisition of Honey. We will discuss Honey in more detail in “The Risks Involved” section of this article.

- An investment in Latin American e-commerce kingpin MercadoLibre (also one of Compounder Fund’s portfolio holdings) in March 2019, which has now expanded into a collaboration in digital payments in certain countries in Latin America.

- An investment in GoJek in June 2020. GoJek has over 170 million users in Southeast Asia and provides ride-hailing, food delivery, and mobile payment services in the region.

These investments and collaborations help broaden PayPal’s reach and also knowledge about the payments landscape across the world.

Third, PayPal has been striking up strategic partnerships in many areas since becoming an independent company. The slides below from PayPal’s 2018 Investor Day event says it all: PayPal had no strategic partners when it was still under eBay!

Source: PayPal investor presentation

We also appreciate the management team’s willingness to invest in PayPal’s business at this current juncture. Because of the COVID-19 pandemic, there has been a surge in the adoption of digital payments. We think that going on the offensive at this moment is a smart move. Here are some comments from PayPal’s management in the 2020 second-quarter earnings conference call:

“[CEO Dan Schulman]

In the first half of 2020, the penetration of e-commerce as a percentage of retail sales outpaced prior to external forecasts by an astonishing three to five years. In this environment, the demand for our products and services has dramatically increased and unleashed multiple opportunities. We are focused on several key initiatives to fully leverage this unique moment in time. First and foremost is our push to accelerate in-store contactless payments, both consumers and merchants are rapidly moving toward digital payments across their online and offline experiences.

This is an existential issue for merchants who realize that reopening the retail stores depends on touchless forms of payments to keep both their employees, and customers safe, and healthy. There are numerous market research studies highlighting that consumers no longer want to handle cash or other forms of payments that require any physical touch at checkout. We are significantly investing to accelerate our presence in all forms of omnichannel commerce from the point of sale in-store, to buy online and pick up in-store, order ahead, pay at the table, and home delivery.

[CFO John Rainey]

And while we know more today than we did a few months ago about both the virus and the economy there continues to be palpable uncertainty. As we sit here today, the concept of normalcy is being redefined, and at times feels elusive. What we do know is that this is a pivotal moment in PayPal’s history. We believe that we’ve never been in a better position to realize our ambition for greater relevance, ubiquity, and impact as a global payment leader.

We recognize that this is our time to capitalize on our strategic position, and financial capacity to serve our customers better, and to advance our platform. And we’re committed to achieving our full potential.”

4. Revenue streams that are recurring in nature, either through contracts or customer-behaviour

We mentioned earlier that PayPal’s primary revenue source is payments that take place on its platform. And when we discussed PayPal’s management, we also pointed out that the company had processed 12.4 billion transactions in 2019 from 305 million active accounts (of which 281 are consumer accounts and 24 million are merchant accounts).

We think that these high numbers highlight the recurring nature of PayPal’s business. It’s also worth noting that there’s no customer-concentration: No single customer accounted for more than 10% of PayPal’s revenues in 2019, 2018, and 2017.

5. A proven ability to grow

PayPal returned to the stock market only in 2015, so we don’t have a long track record to study. But we’re impressed by what the company has.

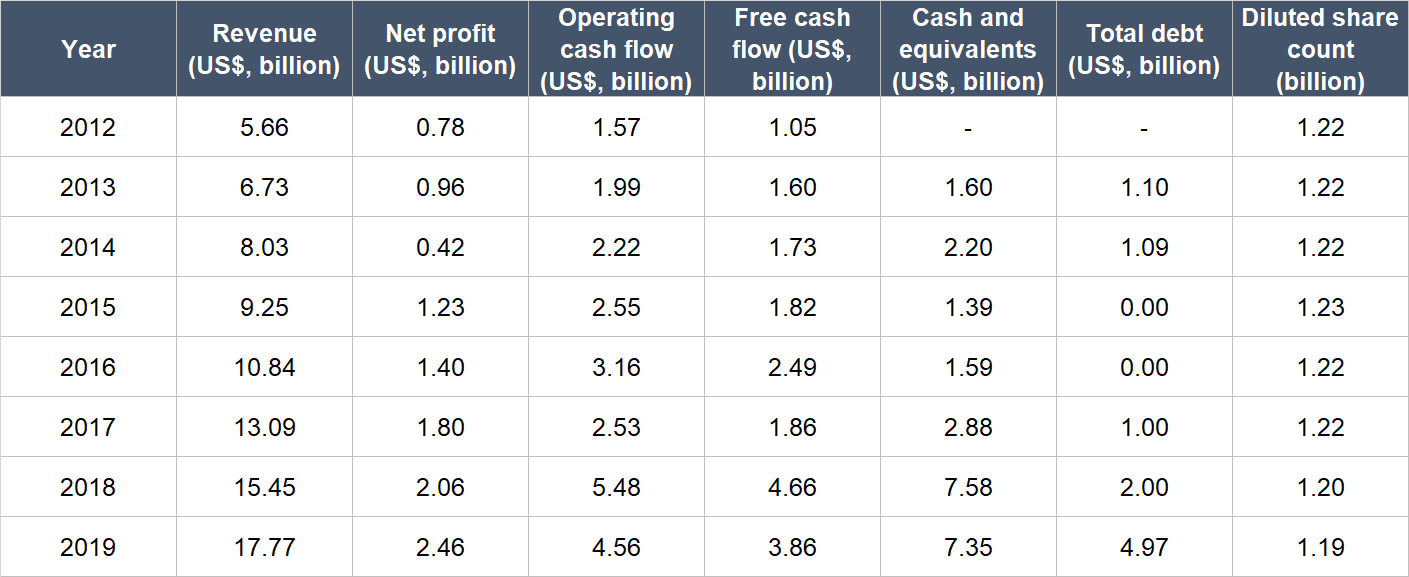

Source: PayPal annual reports

Here are a few key things to note about PayPal’s financials:

- Revenue has increased in each year from 2012 to 2019, and has compounded at a healthy clip of 17.8% per year.

- Net profit was always positive, and has increased by 17.9% annually.

- PayPal has not diluted shareholders too, since its diluted share count has actually fallen from 2015 to 2019.

- Operating cash flow and free cash flow were always positive in each year from 2012 to 2019, and the two important financial metrics have compounded at impressive annual rates of 16.5% and 20.4%, respectively.

- PayPal’s operating cash flow and free cash flow in 2018 had enjoyed a one-time boost from the sale of the company’s US consumer credit receivables portfolio in July that year. But even after making the relevant adjustments, PayPal’s operating cash flow and free cash flow for the year would still be strong at US$4.1 billion and US$3.3 billion, respectively.

- PayPal’s balance sheet was stellar throughout, given the significantly higher cash position compared to debt.

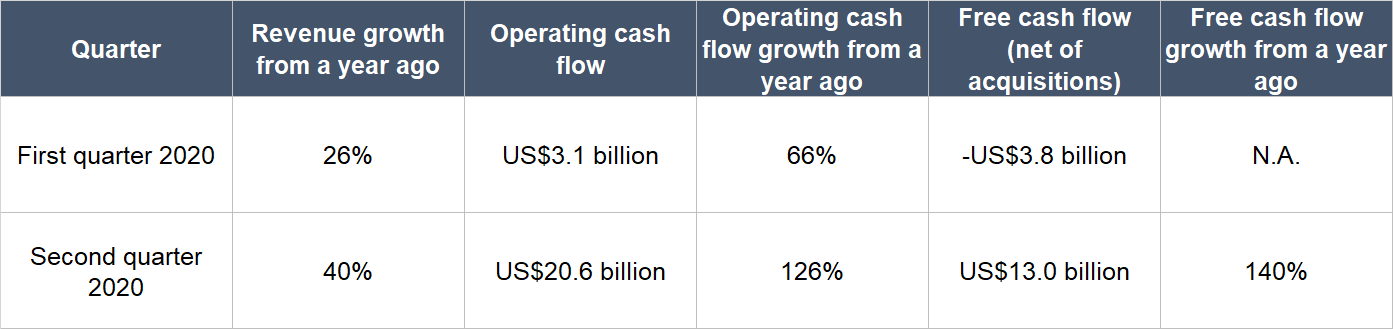

Despite COVID-19 having wrecked the global economy in 2020 thus far, PayPal has managed to produce stellar growth. In the first half of 2020, PayPal’s revenue was up 17.1% to US$9.88 billion, driving an 8.3% jump in net income to US$1.61 billion. Operating cash flow and free cash flow came in at US$3.89 billion and US$3.49 billion, respectively, representing growth of 76.6% and 89.2% from a year ago. The diluted share count also dipped slightly from 1.188 billion to 1.185 billion. For the whole of 2020, PayPal expects revenue growth of 20% and earnings per share growth of 25%.

We see two notable traits in PayPal’s network:

- PayPal has a global reach. It is able to handle transactions in over 200 markets, and allows its customers to receive money in 100 currencies, withdraw funds in 56 currencies, and hold PayPal account balances in 25 currencies.

- We believe PayPal’s business exhibits a classic network effect. Its competitive position strengthens when its network increases in size. When we discussed PayPal’s management earlier, we showed that the volume of payments and number of transactions increased faster than the number of accounts. This means that PayPal’s users are using the platform more over time – to us, this indicates that PayPal’s platform is becoming more valuable to existing users as more users come onboard.

We also want to point out two of PayPal’s payment services providers that we think are crucial for the company’s future growth:

- The first is mobile payments services provider Braintree, which was acquired in 2013 for US$713 million. Braintree provides the technological backbone for the payment tools of many technology companies, including ride-hailing app Uber, cloud storage outfit DropBox, and online accommodations platform AirBnB. Braintree helps PayPal better serve retailers and companies that conduct business primarily through mobile apps.

- The second is digital wallet Venmo (acquired by Braintree in 2012), which allows peer-to-peer transactions. Venmo is highly popular among millennials in the US, and PayPal reported that there were more than 60 million active accounts for the digital wallet in 2020’s second quarter. During the same quarter, Venmo’s total payment volume surged 52% to US$37 billion and was up nearly five times from the volume of US$8 billion seen just three years ago in the second quarter of 2017. PayPal does not regularly disclose Venmo’s revenue numbers, but we’re encouraged to know that (1) the digital wallet’s annual revenue run rate in 2019’s third quarter was nearly US$400 million, double the US$200 million seen in 2018’s fourth quarter, and (2) management said during the 2020 second-quarter earnings conference call that Venmo enjoyed one of its “best quarters ever” during the quarter.

6. A high likelihood of generating a strong and growing stream of free cash flow in the future

PayPal has excelled in producing free cash flow from its business for a long time, and has huge growth opportunities ahead. There’s no reason to believe these will change any time soon.

For perspective, PayPal’s free cash flow margin (free cash flow as a percentage of revenue) had averaged at an impressive 21.6% from 2012 to 2019. In the first half of 2020, PayPal did even better, with a free cash flow margin of 35.3%.

Valuation

We like to keep things simple in the valuation process. In PayPal’s case, we think the price-to-free cash flow (P/FCF) ratio is a suitable gauge for the company’s value. That’s because the payment services outfit has a strong history of producing positive and growing free cash flow.

PayPal carries a trailing P/FCF ratio of around 40 at Compounder Fund’s average purchase price of US$184 per share. This ratio looks a little high relative to history. For perspective, PayPal’s P/FCF ratio was only around 28 in the early days of its 2015 listing.

But we’re happy to pay up, since PayPal excels in all the traits we’re looking out for in Compounders.

The risks involved

There are five key risks we see in PayPal.

First, the payments space is highly competitive. PayPal’s muscling against other global payments giants such as Mastercard and Visa that have larger payment networks (both Mastercard and Visa are also holdings in Compounder Fund’s portfolio). Then there are technology companies with fintech arms that focus on payments, such as China’s Tencent and Alibaba. In November 2019, Bloomberg reported that Tencent and Alibaba plan to open up their payment services (WeChat Pay and Alipay, respectively) to foreigners who visit China. Let’s not forget that there’s blockchain technology (the backbone of cryptocurrencies) jostling for room too. There’s no guarantee that PayPal will continue being victorious. But the payments market is so huge that we think there will be multiple winners – and our bet is that PayPal will be among them.

The second risk we’re watching is regulations. The payments market is heavily regulated. What PayPal can take per payment-transaction could be lowered in the future by regulators for various reasons.

The third risk concerns recessions. A June 2020 report from the World Bank stated:

“The [COVID-19] pandemic is expected to plunge most countries into recession in 2020, with per capita income contracting in the largest fraction of countries globally since 1870. Advanced economies are projected to shrink 7 percent. That weakness will spill over to the outlook for emerging market and developing economies, who are forecast to contract by 2.5 percent as they cope with their own domestic outbreaks of the virus. This would represent the weakest showing by this group of economies in at least sixty years.”

COVID-19 has so far been a net positive for PayPal. But there’s no telling how far the global economy would fall before the world finally controls the virus. If there’s a prolonged contraction in global economic activity, payment flows on PayPal’s platform could be lowered. PayPal’s business was remarkably resilient during the last major global economic downturn in 2008 and 2009. Back then, eBay had no revenue-growth from its main e-commerce platform. But the segment that consisted primarily of PayPal produced strong double-digit revenue growth in both years. We’re encouraged by PayPal’s historical track record, but the company is much larger today, so it may not be able to grow through tough economic conditions that easily.

Source: eBay annual report

The US$4 billion acquisition of Honey represents the fourth risk. We want to be clear: We like the deal and we think it will work out great. Honey’s revenue in 2018 was over US$100 million, with growth of more than 100% – and the company was already profitable. In a recent article, Ben Thompson from Stratechery shared how the acquisition could lead to upside for PayPal’s business:

“The most important effect, according to Schulman, was on PayPal’s relationship with consumers. Now, instead of being a payment option consumers choose once they have already committed to a purchase, PayPal can engage with consumers much higher in the purchase funnel. This might be one step higher, as would be the case with coupon search, but it could also be around discovery and calls-to-action, as might be the case with the app or notifications and price-tracking…

…Honey is also an intriguing way for PayPal to actually make money on Venmo in particular. Honey’s audience skews heavily female and millennial, which means there is a lot of overlap with Venmo, and there is a good chance PayPal can really accelerate Honey’s adoption by placing it within its core apps (which it plans to do within the next 6 to 12 months)…

…If PayPal, via Honey, knows exactly what you are interested in buying, and can make it possible for merchants to offer customized offers based on that knowledge, well, that may be a very effective way to not only capture affiliate revenue but also payment processing revenue as well. Demand generation remains one of the most significant challenges for merchants… And here the fact that PayPal has 24 million merchant partners versus Honey’s 30,000 is a very big deal.”

Moreover, the early signs of the Honey acquisition have been encouraging. For example:

- PayPal’s management commented in the 2020 first-quarter earnings conference call that cross-selling between PayPal and Honey has resulted in customers with “much higher LTV [lifetime value].”

- Honey’s net new active users in the second quarter of 2020 were nearly three times that in the first quarter.

But the deal is still a risk. Honey is PayPal’s largest acquisition ever, and it came with a steep price tag of US$4 billion. Assuming Honey grew its revenue by 100% in 2019, PayPal is effectively paying 20 times revenue for the discount discovery company. We will have to face a situation of PayPal writing down the value of Honey if the integration of the two fails to live up to expectations.

Lastly, we’re mindful of succession risk. PayPal’s CEO, Dan Schulman, is already 62 this year. Fortunately, PayPal’s other key leaders are mostly in their mid-fifties or younger.

Summary and allocation commentary

We think the transition from cash to cashless payments holds immense opportunities for companies. We also think a payment company with a wide network of consumers and merchants (PayPal, for instance) stands a good chance of being one of the eventual winners.

Furthermore, PayPal has a robust balance sheet, a proven ability to generate strong free cash flow, high levels of recurring revenues, and an excellent management team whose interests are aligned with shareholders. PayPal’s P/FCF ratio is on the high end, but we’re happy to pay up for a top-quality business.

Every company has risks, and we’re aware of the important ones with PayPal. They include competition, regulation, recessions, and more.

We initiated a 4.0% position in PayPal with Compounder Fund’s initial capital. To us, PayPal is a company with (1) a huge addressable market, and (2) a high probability of being able to grow at a strong clip for many years in the future. Given this trait, we’re happy to have PayPal be one of the larger positions in Compounder Fund’s portfolio.

And here’s an important disclaimer: None of the information or analysis presented is intended to form the basis for any offer or recommendation; they are merely our thoughts that we want to share.