Compounder Fund: MercadoLibre Investment Thesis - 12 Aug 2020

Data as of 11 August 2020

MercadoLibre (NASDAQ: MELI) is one of the 40 companies in Compounder Fund’s initial portfolio. This article describes our investment thesis for the company.

Company description

MercadoLibre – “free market” in Spanish – was founded in 1999 and has rode the growth of the internet and online retail to become the largest e-commerce company in Latin America today, based on unique visitors and page views. The company is present in 18 countries including Brazil, Argentina, Mexico, and Chile.

There are six integrated e-commerce services that MercadoLibre provides:

- MercadoLibre Marketplace: An online platform that connects buyers and sellers; it earns revenue by taking a small cut of each transaction.

- Mercado Pago: A fintech platform that primarily facilities online payments, and online-to-offline (O2O) payments. It can be used both within and outside MercadoLibre’s marketplaces.

- Mercado Envios: A logistics solution that includes fulfilment and warehousing services.

- MercadoLibre Classifieds: An online classifieds service for motor vehicles, real estate, and services; it also helps direct users to Mercadolibre’s marketplaces.

- MercadoLibre advertising: A service that allows advertisers to display ads on MercadoLibre’s websites.

- Mercado Shops: A solution that helps sellers establish, run, and promote their own online stores.

MercadoLibre has two business segments. The first is Enhanced Marketplace, which consists of MercadoLibre Marketplace and MercadoEnvios. In 2019, Enhanced Marketplace accounted for 52% of the company’s total net revenue of US$2.3 billion. The second segment is Non-Marketplace, which houses the other four of MercadoLibre’s services. It accounted for the remaining 48% of MercadoLibre’s total net revenue in 2019. Most of the net revenue from Non-Marketplace is from MercadoPago – in 2019, more than 86% of Non-Marketplace’s net revenue came from payment fees.

From a geographical perspective, Brazil is MercadoLibre’s most important country. It accounted for 63.6% of the company’s total net revenue in 2019. Argentina and Mexico are in second and third place, respectively, with shares of 19.9% and 12.0%. The remaining 4.5% are from the other Latin American countries that MercadoLibre is active in.

Investment thesis

We have laid out our investment framework in Compounder Fund’s website. We will use the framework to describe our investment thesis for MercadoLibre.

1. Revenues that are small in relation to a large and/or growing market, or revenues that are large in a fast-growing market

According to a June 2020 report from market researcher eMarketer, e-commerce sales in Latin America was US$70.1 billion in 2019, and represented just 4.4% of total retail sales in the region. For perspective, e-commerce was 11.8% of total retail sales in the US in the first quarter of 2020. eMarketer also expects the Latin America e-commerce market to compound at 13.5% annually from 2019 to US$116.2 billion by 2023.

Forrester, another market research firm, produced a report in August 2019 and stated that the e-commerce market in Latin America’s six largest economies – that would be Argentina, Brazil, Chile, Colombia, Mexico, and Peru, which are all countries that MercadoLibre is active in – to grow by more than 22% annually from 2018 to 2023.

The projection of high growth for Latin America’s e-commerce space is reasonable in our eyes for two reasons.

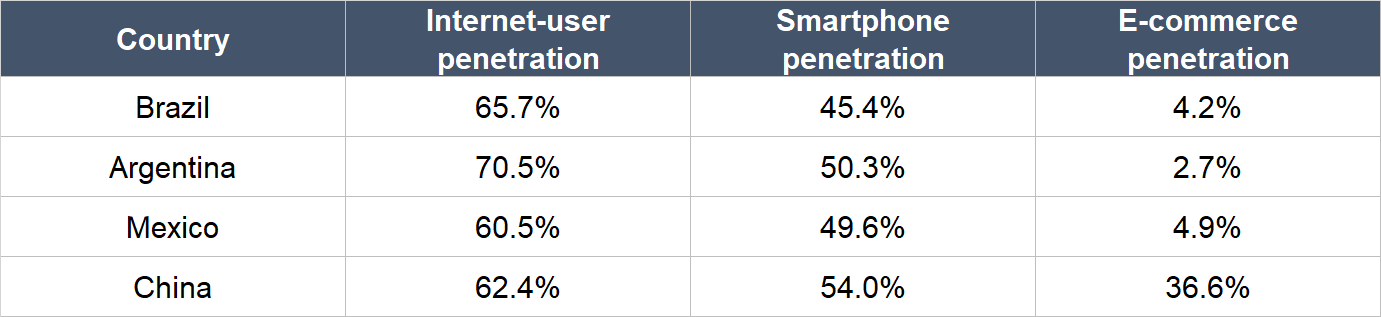

First, there’s the aforementioned low penetration rate of online retail in Latin America’s overall retail scene. It’s worth noting too that despite Brazil, Argentina,and Mexico (MercadoLibre’s three largest markets) having similar internet-user and smartphone penetration rates as China, online retail is a much higher percentage of total retail in the Asian giant; the data you see in the table below came from a MercadoLibre presentation in 2019.

Source: MercadoLibre data

Second, internet penetration rates in Latin America are still relatively low: 86.0% of the US population in 2019 currently has access to the internet, which is much higher than in Brazil, Argentina, and Mexico. For another perspective, Latin America has a population of around 640 million people, but has internet users and online shoppers of merely 362 million and 200 million, respectively.

Given all the numbers described above – and MercadoLibre’s current revenue of US$2.8 billion over the 12 months ended 30 June 2020 – it’s clear to us that the company has barely scratched the surface of the growth potential of Latin America’s e-commerce market. We also want to point out that we see MercadoLibre possessing the potential to expand into new markets over time – we will discuss this in detail later.

2. A strong balance sheet with minimal or a reasonable amount of debt

At the end of 2020’s second quarter, MercadoLibre held just US$1.2 billion in debt against US$2.8 billion in cash, short-term investments, and long-term investments. That’s a strong balance sheet.

3. A management team with integrity, capability, and an innovative mindset

On integrity

MercadoLibre’s co-founder is Marcos Galperin. He’s still young at just 49, but he has been leading the company as CEO, chairman, and president since its founding in 1999. Galperin is not the only young member of MercadoLibre’s senior management team with long tenure. In fact, MercadoLibre’s Chief Financial Officer, Chief Operating Officers, Chief Technology Officer, and head of its financial technology operations are all between 42 and 52 years old, but have each been with the company for more than 10 years. They also joined MercadoLibre in less senior positions. To us, it’s a positive sign on MercadoLibre’s culture to see it promote from within.

Source: MercadoLibre proxy statement

In 2019, Galperin’s total compensation was US$13.6 million, which is a tidy sum. But more than 80% of the compensation of MercadoLibre’s key leaders (Galperin included) for the year depended on the company’s annual business performance (including revenue and profit growth, and the company’s net promoter score, which measures customer satisfaction) and multi-year changes in the company’s stock price. To us, this is a well-designed compensation plan that aligns the interests of Mercadolibre’s leaders with the company’s shareholders. Moreover, MercadoLibre paid its key leaders less in 2018 (Galperin’s compensation of US$11.4 million in 2018 was 6% lower than in 2017) despite growing net revenue by 18%. That’s because MercadoLibre had flopped in terms of its profit-performance. We’ll explain this in greater detail later.

We also like the fact that Galperin controls a significant number of MercadoLibre shares, which increases the likelihood that he will view himself as being on the same boat as the company’s other shareholders. As of 13 April 2020, Galperin controlled 4 million MercadoLibre shares (8.1% of the total number of shares) through a family trust. These shares are worth around US$4.4 billion at the company’s share price of US$1,100 as of 11 August 2020.

On capability and innovation

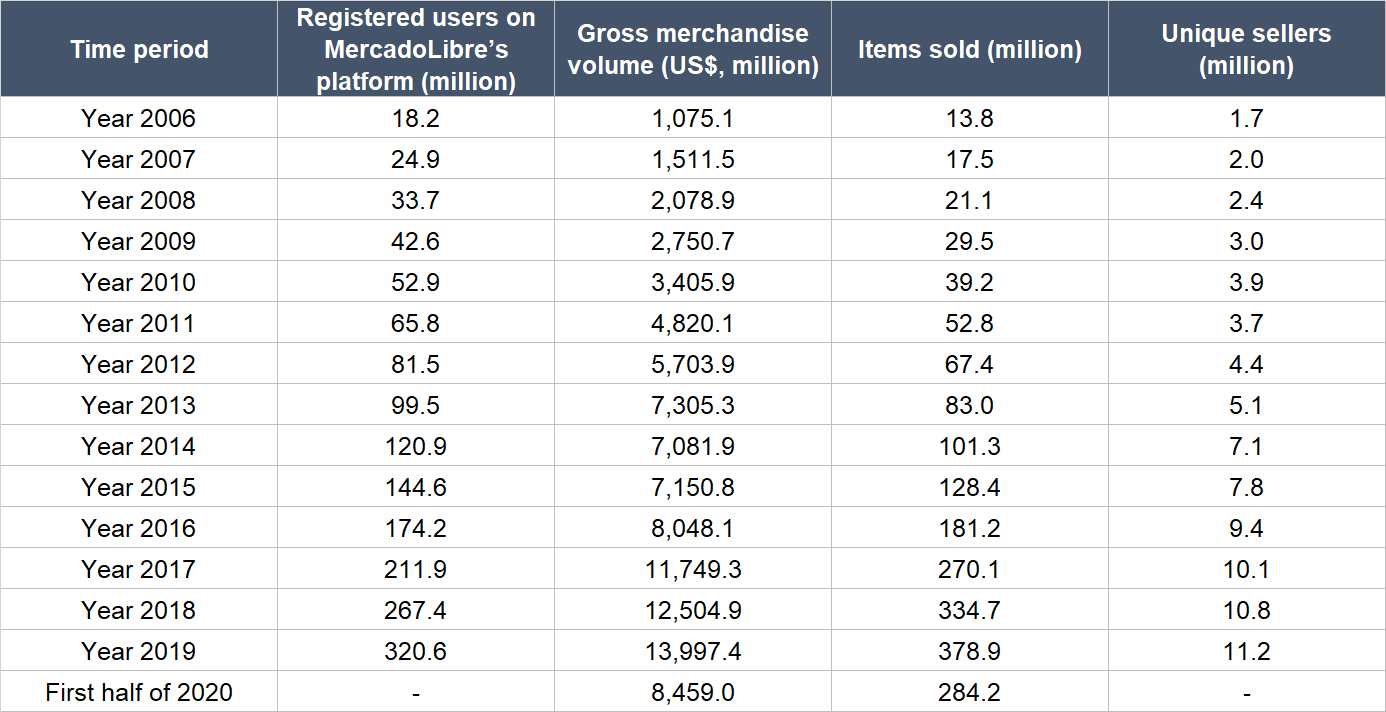

As an e-commerce platform, there are a number of important business metrics for MercadoLibre, such as registered users, gross merchandise volume, items sold, and unique sellers. All four have grown tremendously over the years – even from 2007 to 2009, the period when the world was rocked by the Great Financial Crisis – as the table below illustrates. This is a strong positive sign on management’s capability.

Source: MercadoLibre IPO prospectus, annual reports, and quarterly earnings update

A short walk through MercadoLibre’s history can also reveal the strength of the company’s management team and their innovativeness.

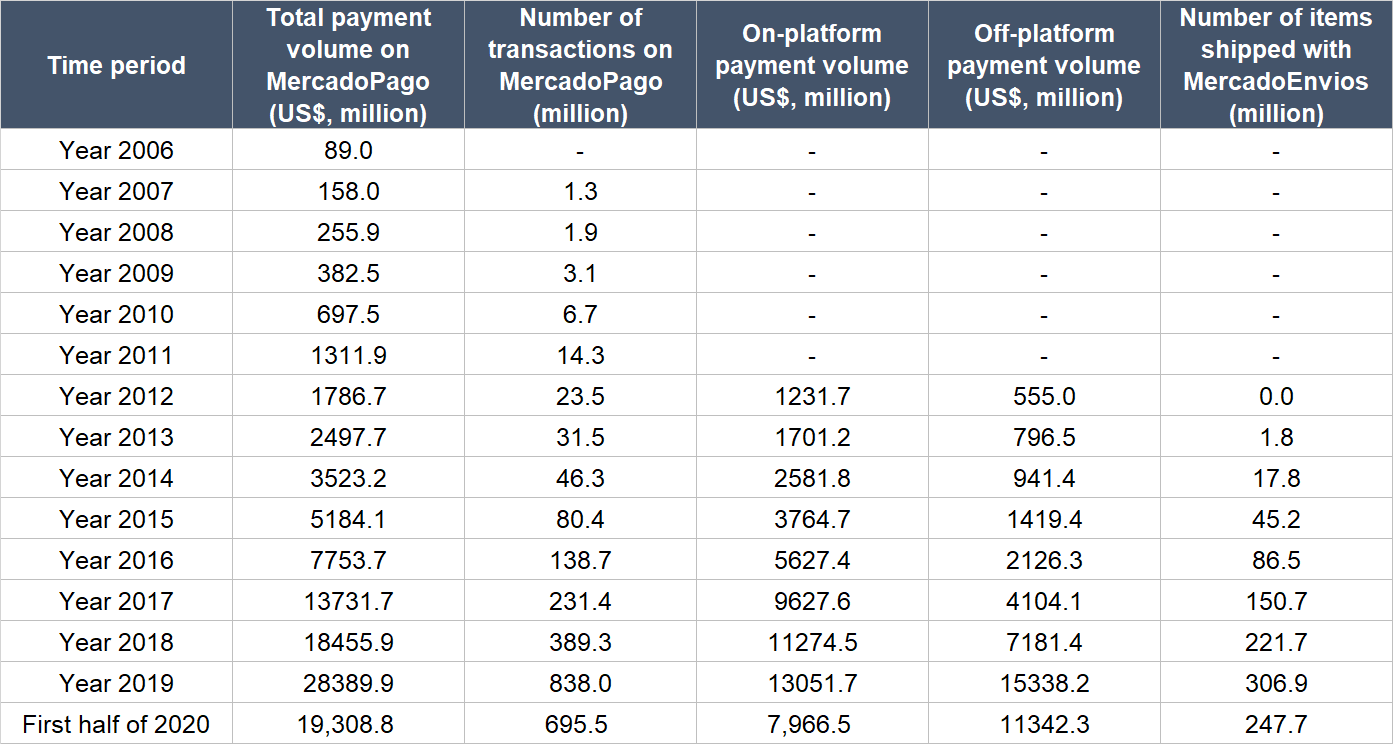

MercadoLibre started life in the late 1990s operating online marketplaces in Latin America. In 2004, the company established MercadoPago to facilitate online payments on its own platform. Over time, MercadoPago has seen explosive growth (in terms of payment volume and number of transactions); opened itself up to be used outside of MercadoLibre’s marketplaces; and added new capabilities that facilitate O2O payments, such as a mobile wallet, and processing payments through QR codes and mobile point of sales solutions. Impressively, during 2019’s third quarter, MercadoPago’s off-platform payment volume exceeded on-platform payment volume in a full quarter in Brazil (MercadoLibre’s largest market), for the first time ever. Then in 2013, MercadoLibre launched MercadoEnvíos, its logistics solution. MercadoEnvios has also produced incredible growth in the number of items it has shipped.

Source: MercadoLibre annual reports and quarterly earnings update

MercadoLibre’s service-innovations are intended to drive growth in the company’s online marketplaces. Right now, there are a number of relatively new but growing services at MercadoLibre:

- MercadoFondo: A mobile wallet service launched in the second half of 2018 that attracts users with an asset-management function.

- MercadoCredito: MercadoCredito, which was introduced in the fourth quarter of 2016, provides loans to merchants. Providing loans can be a risky business, but MercadoLibre is able to lower the risk since it knows its merchants well (they conduct business on the company’s online marketplaces). Furthermore, MercadoLibre can automatically collect capital and interest through MercadoPago, since its merchants’ business flows through the payment-service. Over time, MercadoLibre has steadily expanded MercadoCredito to consumers in addition to merchants that use the company’s mobile point of sales solution.

Amazon.com (another company in Compounder Fund’s portfolio) is North America’s e-commerce kingpin. But it’s so much more than just online retail. Over time, Amazon has successfully branched into completely new areas with aplomb, such as cloud computing and digital advertising. We would not be surprised to see MercadoLibre’s future development follow a similar arc as Amazon’s, in terms of having powerful growth engines outside of the core e-commerce business.

Today, there are new growth areas for MercadoLibre that have already been developed outside – such as in the case of MercadoPago. MercadoLibre has an expansive and noble mission – to democratise commerce and access to money for the people of Latin America. We think MercadoFondo and, in particular, MercadoCredito, have the potential to grow significantly beyond MercadoLibre’s online marketplaces. Access to credit and investment/banking services is low in Latin America for both businesses and individuals (see chart below). It will be up to MercadoLibre to grasp the opportunity with both hands. We are confident the company will do so.

Source: MercadoLibre 2019 investor presentation

4. Revenue streams that are recurring in nature, either through contracts or customer-behaviour

We think it’s highly likely that MercadoLibre enjoys high levels of recurring business because of customer behaviour. Two things to lend weight to our view:

- No single customer accounted for more than 5% of MercadoLibre’s net revenues in the first six months of 2020, and in each of 2019, 2018, and 2017.

- The company’s gross merchandise volume, number of items sold, number of registered users, payment volume, and number of payment transactions range from hundreds of millions to billions.

5. A proven ability to grow

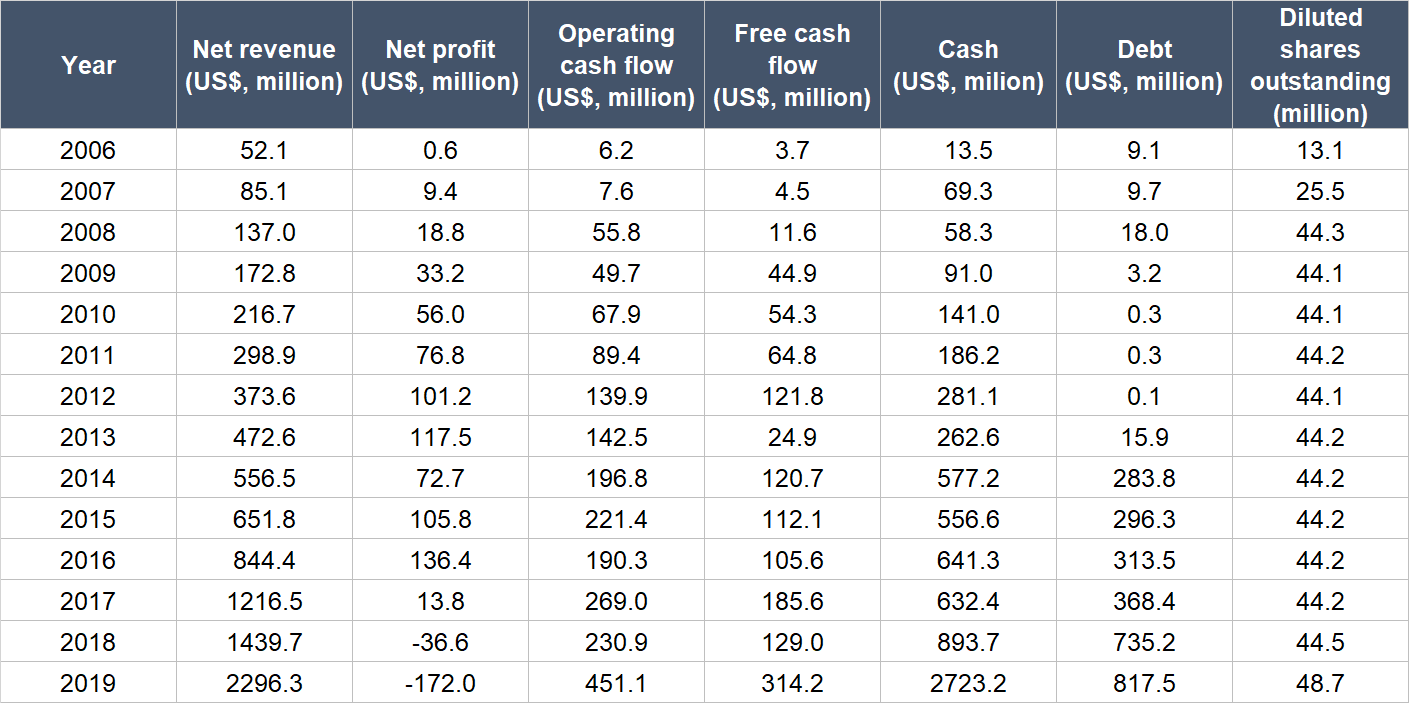

The table below shows MercadoLibre’s important financials from 2006 to 2019:

Source: MercadoLibre annual reports

A few things to note:

- Revenue growth has been excellent at Mercadolibre, with compound annual growth rates of 33.8% from 2006 to 2019, and 32.8% from 2014 to 2019.

- Net profit was growing strongly up to 2016, before the situation appeared to have deteriorated dramatically. Thing is, the company had ramped up investments into its business, such as increasing marketing spend, subsidising shipping services for buyers on its marketplaces, and selling mobile point of sales solutions at low margins to entice off-platform usage of MercadoPago. These actions hurt MercadoLibre’s bottom-line in the short run, but we see them as positive for the long run. They draw in customers to MercadoLibre’s ecosystem, in turn creating a network effect. The more users there are on the online marketplaces, the more sellers there are, which lead to more users – and off the flywheel goes. It’s the same with MercadoPago, especially with off-platform transactions. The more merchants there are that accept MercadoPago, the more users there will be, leading to even higher merchant-acceptance – and off the flywheel goes, again. (Another reason for the drastic decline in profit in 2017 was an US$85.8 million loss related to the deconsolidation of MercadoLibre’s Venezuelan business in December of the year – more on Venezuela later.)

- Operating cash flow and free cash flow have both been consistently positive since 2006, and have also grown significantly. But in more recent years, both were pressured by the aforementioned investments into the business, with a rebound in growth seen in 2019. It’s all the more impressive that MercadoLibre has produced positive operating cash flow and free cash flow while making the investments.

- The balance sheet has been strong throughout, with cash (including short-term investments and long-term investments) consistently been higher than the amount of debt.

- At first glance, MercadoLibre’s diluted share count appeared to increase sharply in 2008 (we started counting only in 2007, since the company was listed in August of the year). But the number we’re using is the weighted average diluted share count. Right after MercadoLibre got listed, it had a share count of around 44 million. This means that the company has actually not been diluting shareholders much at all. MercadoLibre’s diluted share count increased by 9.3% in 2019 because the company had issued 4.1 million new shares of itself during the year to raise US$1.9 billion. But we’re not worried. The capital raised was for good reasons: It is earmarked for investments to drive growth in the company’s payment initiatives, logistics capacity, and adoption of these services; meanwhile, US$750 million of the capital raised came from digital payments powerhouse PayPal (which is also in Compounder Fund’s portfolio), and the investment has now led to PayPal’s services being integrated into MercadoLibre’s payments network in Brazil and Mexico. Furthermore, the increase in MercadoLibre’s share count is much lower than the revenue growth of 59.5% seen during the year.

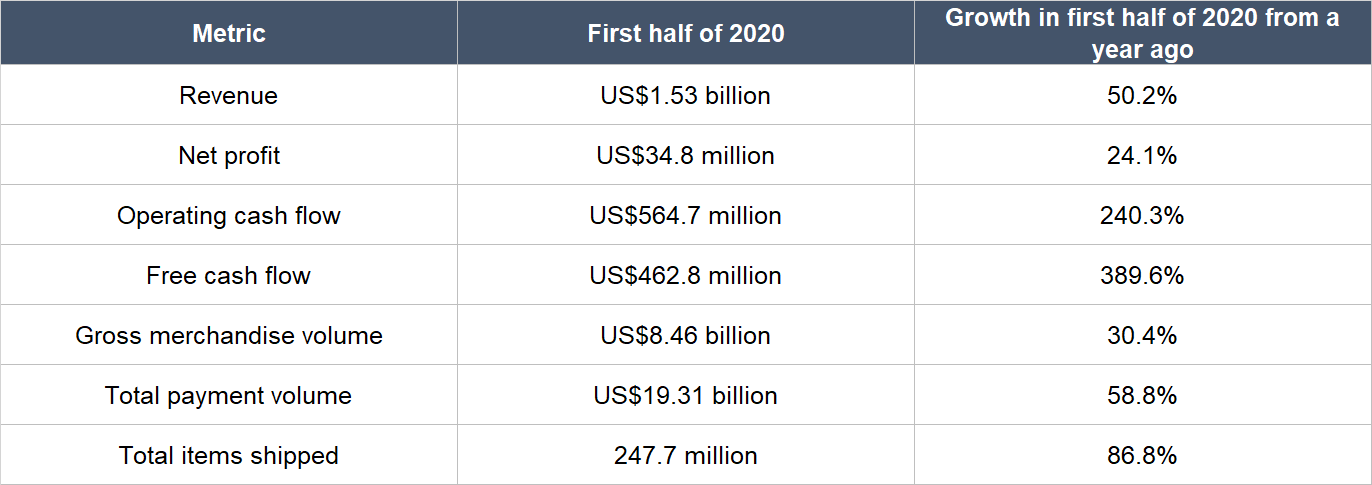

COVID-19 has hit Latin America hard. In late June 2020, the International Monetary Fund said that Latin America and the Caribbean are expected to see a 9.3% contraction in their economies this year. But MercadoLibre has continued to put up stunning growth numbers so far in 2020 (see table below) with the COVID-19 pandemic driving the adoption of e-commerce and digital payments.

Source: MercadoLibre quarterly earnings update

It’s worth noting too that MercadoLibre’s revenue growth in the second quarter of 2020 (up 61% from a year ago) actually accelerated from the first quarter of 2020 (up 38% from a year ago).

6. A high likelihood of generating a strong and growing stream of free cash flow in the future

MercadoLibre has tremendous room to expand its business in the future while also displaying a strong history of growth and innovation. These traits suggest that MercadoLibre could grow its business significantly in the years ahead.

Meanwhile, the Latin America e-commerce giant has a good track record over the past few years in generating free cash flow despite heavy reinvestments into its business. In the first half of 2020, MercadoLibre’s free cash flow margin (free cash flow as a percentage of revenue) was an impressive 30.2%. The strong possibility of a much larger revenue stream in the future, as well as the good track record in generating free cash flow, means that MercadoLibre ticks the box in this criterion.

Valuation

At Compounder Fund’s average purchase price of US$1,027, MercadoLibre has a negative price-to-earnings (P/E) ratio since the company is sitting on a loss of US$3.50 per share over the 12 months ended 30 June 2020. Meanwhile, the trailing price-to-free cash flow (P/FCF) ratio is 75.

We think that MercadoLibre’s valuation numbers look so bad and high right now because (1) it is reinvesting heavily into its business to grab the massive opportunity that it sees in Latin America’s e-commerce and digital payment markets, and (2) the market expects great things from the company because it still has tremendous runway for growth. Management is willing to endure ugly short-term results for a good shot at producing excellent long-term business performance – we appreciate management’s focus on the long run.

The current sky-high P/FCF ratio and negative P/E ratio do mean that MercadoLibre’s share price is likely going to be volatile. But that’s something we’re very comfortable with.

The risks involved

For us, we see the instability in the political and economic landscape of the Latin America region as a huge risk for MercadoLibre.

If you look at the table on the company’s historical financials that we shared earlier, you’ll see this big drop in profit in 2014. The reason was because of impairments MercadoLibre made to its Venezuela business during the year. As recently as 2017, Venezuela was still the fourth-largest market for MercadoLibre. In fact, Venezuela accounted for 10.4% of the company’s revenue in 2014. But the country’s contribution to MercadoLibre’s business has since evaporated after the company deconsolidated its Venezuelan operations in late 2017, as mentioned earlier. Venezuela has been plagued by hyperinflation as well as political and social unrest in the past few years, making it exceedingly difficult for MercadoLibre to conduct business there.

On 12 August 2019, MercadoLibre’s share price fell by 10%. We seldom think it makes sense to attach reasons to a company’s short-term share price movement. But in this particular case, we think there’s a clear culprit: Argentina’s then-president, Mauricio Marci, who was deemed as pro-business, lost in the country’s primary election to Alberto Fernandez, a supporter of the Peronist movement; Fernandez ended up winning the actual presidential election a few months later. Meanwhile, Brazil’s president, Jair Bolsonaro, and his family are currently embroiled in serious corruption scandals. It’s worth mentioning too that COVID-19 is currently a big crisis in Brazil – the country has more than 3.1 million COVID-19 cases and a death toll of around 100,000 (the world’s second highest).

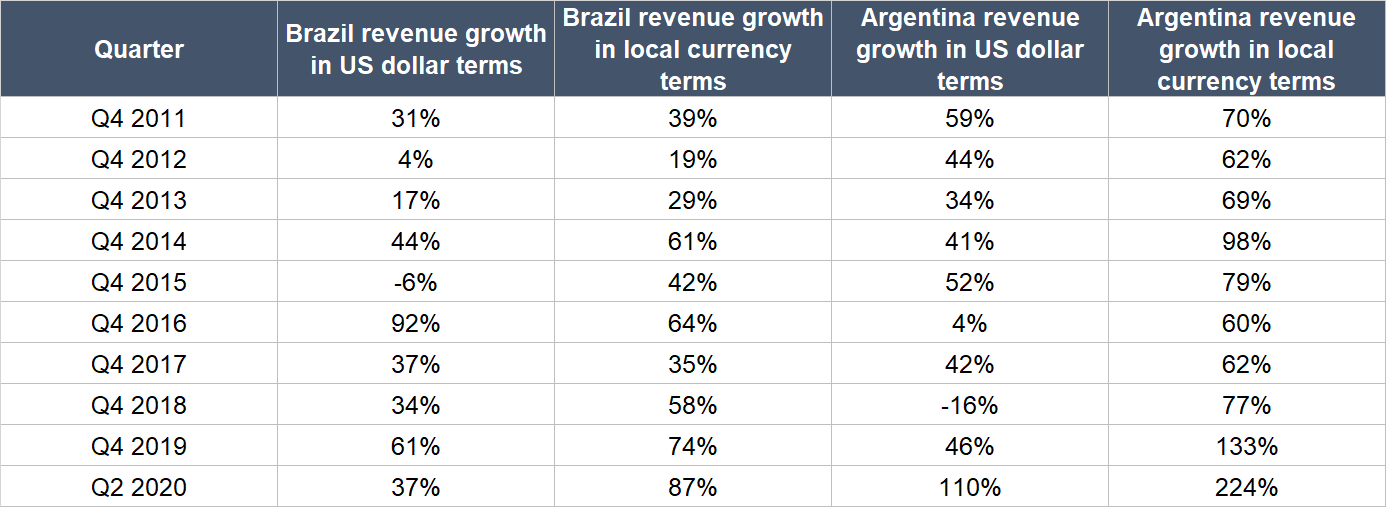

MercadoLibre reports its financials in the US dollar, but it conducts business mostly in the prevailing currencies of the countries it’s in. This means the company is exposed to adverse currency movements and inflation in these countries. Unfortunately, both are rampant in Latin America (relatively speaking, compared to quaint Singapore). The table below shows the growth of MercadoLibre’s revenues in Brazil and Argentina in both US-dollar terms and local-currency terms going back to 2011’s fourth quarter. Notice the local-currency growth rates frequently coming in much higher than the US-dollar growth rates.

Source: MercadoLibre earnings updates

The silver lining here is that MercadoLibre has still produced excellent revenue growth in US dollars since 2006, despite the difficulties associated with operating in Latin America. In fact, we think that MercadoLibre is a great example of how a company can still thrive even in adverse macroeconomic conditions if it is in the right business (one powered by powerful secular growth trends) and has excellent management.

Another big risk we’re keeping an eye on is related to competition. Other e-commerce giants in other parts of the world could want a piece of MercadoLibre’s turf. For instance, in December 2019, Amazon (another holding in Compounder Fund’s portfolio) announced the launch of its second distribution centre in Brazil. We’re confident that MercadoLibre has already established a strong competitive position for itself, but we’ll still be watching for the moves of its competitors.

The last risk we’re concerned with is key-man risk. Marcos Galperin has led the company since its founding, and has done a fabulous job. The good news here is that Galperin is still young. But should he depart from the CEO role for whatever reason, we will be watching the leadership transition.

Summary and allocation commentary

Latin America may scare many investors away because of the frequent unrest happening in the region. But MercadoLibre has grown its business exceptionally well for more than a decade despite the troubles there. The company also aces the other criteria in Compounder Fund’s investment framework:

- Latin America still appears to be in the early days of e-commerce adoption, so the region’s e-commerce market is poised for rapid growth in the years ahead.

- MercadoLibre’s balance sheet is robust with billions in cash and investments, and much lower debt.

- Through a study of the compensation structure of MercadoLibre and the history of how its business has evolved, it’s clear to us that the management team of the company possesses integrity, capability, and the ability to innovate.

- There are high levels of recurring revenue streams in MercadoLibre’s business because of customer behaviour

- MercadoLibre has been adept at generating free cash flow even when it is reinvesting heavily into its business.

There are of course risks to note. Besides the inherent political and economic instability in Latin America, we see two other key risks for MercadoLibre: Competition, and key-man risk. The company’s valuation is also really high at the moment because of heavy reinvestments back into the business, and the market’s expectation for high growth. But the high valuation is something we’re comfortable with.

In all, we initiated a 4.0% position in MercadoLibre with Compounder Fund’s initial portfolio. We’re happy to have MercadoLibre be one of Compounder Fund’s larger holdings because we think the company possesses a top-quality business with huge addressable markets and a high probability of being able to grow at a rapid clip for many years in the future.

And here’s an important disclaimer: None of the information or analysis presented is intended to form the basis for any offer or recommendation; they are merely our thoughts that we want to share.