Compounder Fund: Alteryx Investment Thesis - 13 Dec 2020

Data as of 12 December 2020

Alteryx (NYSE: AYX), which is based and listed in the USA, is one of the 40 companies in Compounder Fund’s initial portfolio. This article describes our investment thesis for the company.

Company description

Alteryx provides a self-service subscription-based software platform that allows organisations to easily scrub and blend data from multiple sources and perform sophisticated analysis to obtain actionable insights.

The company’s platform can interact with nearly all data sources. These include traditional databases offered by the likes of IBM, Oracle, and SAP, as well as newer offerings such as those from MongoDB, Amazon Web Services, Google Analytics, and even social media platforms.

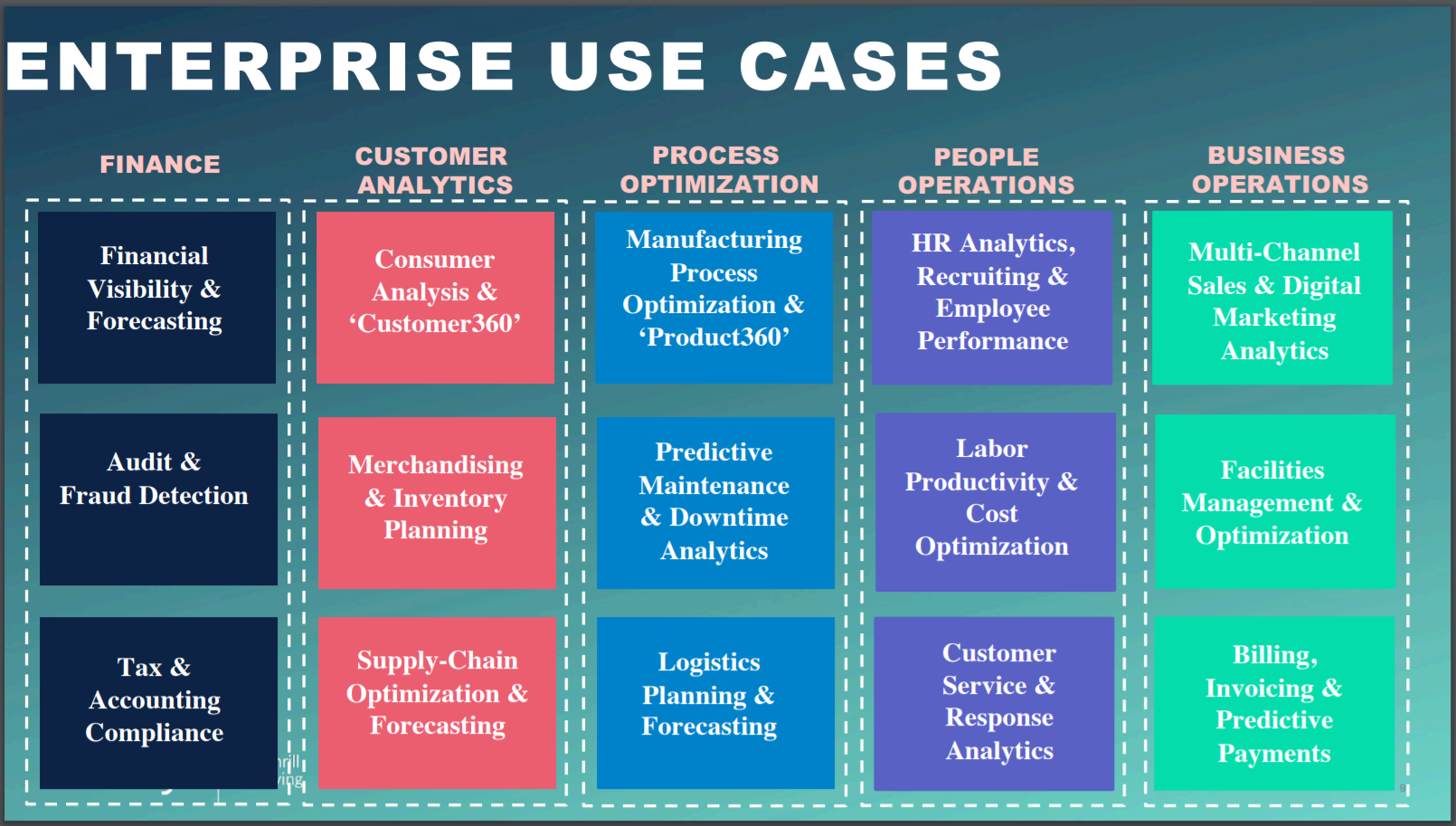

Once data from different sources are fed into Alteryx’s platform, it cleans and blends the data. Users can easily build configurable and sophisticated analytical workflows on the platform through drag-and-drop tools. The workflows can be easily automated and shared within the users’ organisation, and the results can be displayed through Alteryx’s integrations with data-visualisation software from companies such as Tableau Software and Qlik. Here’s a chart showing the various use cases for Alteryx’s data analytics platform:

Source: Alteryx June 2019 investor presentation

Alteryx exited the third quarter of 2020 with nearly 7,000 customers, of all sizes, in more than 90 countries. These customers come from a wide variety of industries and include 38% of the Global 2000 companies. The Global 2000 is compiled by Forbes and it’s a list of the top 2,000 public-listed companies in the world ranked according to a combination of their revenue, profits, assets, and market value. With thousands of customers, it’s no surprise that Alteryx does not have any customer concentration – no single customer accounted for more than 10% of the company’s revenue in the three years through 2019. The graphic below illustrates the diversity of Alteryx’s customer base:

Source: Alteryx 2020 third-quarter earnings presentation

Despite having customers in over 90 countries, Alteryx is currently still a US-centric company. In the first nine months of 2020, 68% of its revenue came from the USA. There is no other country that accounted for more than 10% of Alteryx’s revenue in the same period.

Investment thesis

We have laid out our investment framework in Compounder Fund’s website. We will use the framework to describe our investment thesis for Alteryx.

1. Revenues that are small in relation to a large and/or growing market, or revenues that are large in a fast-growing market

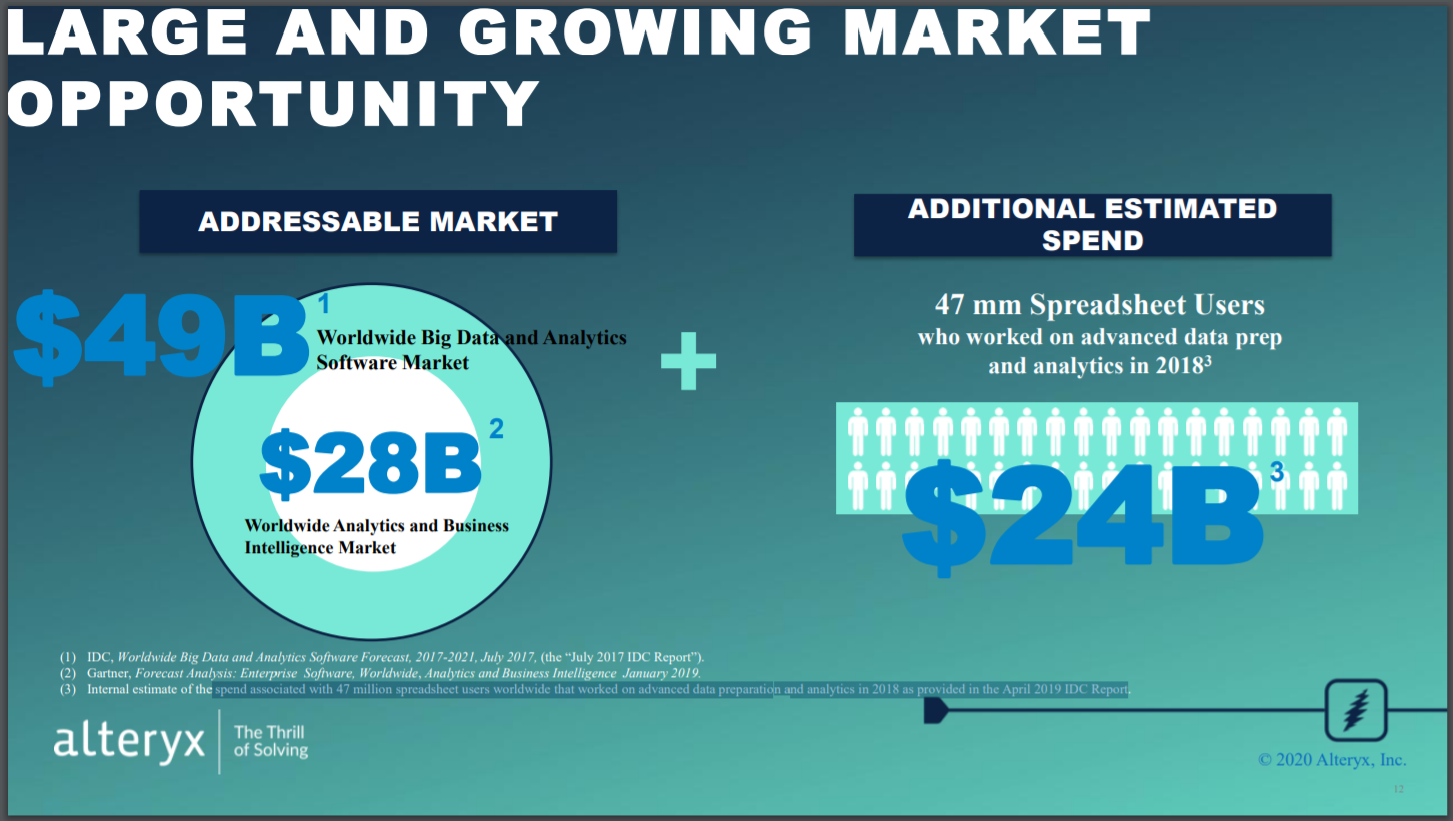

Alteryx earned US$491.2 million in revenue in the 12 months ended 30 September 2020. This is significantly lower than the US$49 billion addressable market that the company is currently seeing. It comprises two parts:

- First, there’s the US$25 billion global analytics and business intelligence software market (according to a January 2020 Gartner report); in the diagram just below, this is shown as the IT category

- Second, there’s a US$24 billion opportunity, based on Alteryx’s estimate of the spending associated with 47 million spreadsheet users worldwide who worked on advanced data preparation and analytics in 2018 (according to an April 2019 report from market research firm IDC)

Source: Alteryx 2020 third-quarter earnings presentation

The company appears to have recently walked back from a previous view that its addressable market is around US$79 billion. The image below comes from Alteryx’s 2019 fourth-quarter earnings presentation and it shows what the company thought its market opportunity was back then. The big missing piece from the current numbers is an additional US$21 billion slice (US$49 billion minus US$28 billion) of the global big data and analytics software market that’s based on estimates found in a July 2017 report from IDC.

Source: Alteryx 2019 fourth-quarter earnings presentation

It’s not a good look for Alteryx to suggest that its market opportunity is now smaller than previously thought. But we’re not too concerned for two reasons. First, the new estimate is still orders of magnitude larger than Alteryx’s current revenue. Second, it’s possible that Alteryx’s market opportunity could end up expanding again in the future.

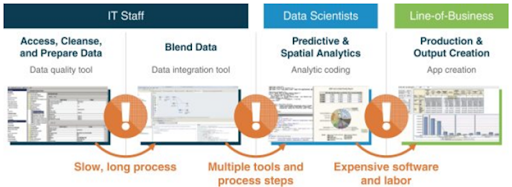

We mentioned earlier that Alteryx’s data analytics platform can interact with nearly all data sources. This interactivity is important. A 2015 Harvard Business Review study sponsored by Alteryx found that 64% of organizations use five or more sources of data for analytics. IDC predicted in late 2018 that the quantity of data in the world (generated, captured, and replicated) would compound at an astounding rate of 61% per year, from 33 zettabytes then to 175 zettabytes in 2025. That’s staggering. 1 zettabyte equals to 1012 gigabytes. A 2013 survey on more than 400 companies by business consultancy group Bain found that only 4% of them had the appropriate human and technological assets to derive meaningful insights from their data. In fact, Alteryx’s primary competitors are manual processes performed on spreadsheets, or custom-built approaches. These traditional methods for data analysis involve multiple steps, require the support of technical teams, and are slow (see chart below). Crucially, Alteryx’s self-service data analytics platform is scalable, efficient, and can be mastered and used by analysts with no coding skill or experience. We think this leads to two good things for Alteryx:

- First, it democratises access to sophisticated data analytics for companies, and hence could open up Alteryx’s market opportunity in the future.

- Second, it places Alteryx’s platform in a sweet spot of riding on a growing trend (the explosion in data generated) as well as addressing a pain-point for many organisations (the lack of resources to analyse data, and the laborious way that data analysis is traditionally done).

(Traditional way to perform data analysis)

Source: Alteryx IPO prospectus

2. A strong balance sheet with minimal or a reasonable amount of debt

As of 30 September 2020, Alteryx held US$982.5 million in cash, short-term investments, and long-term investments. This is comfortably higher than the company’s total debt of US$722.0 million (all of which are convertible notes).

For the sake of conservatism, we also note that Alteryx had US$48.0 million in operating lease liabilities. But the company’s cash, short-term investments, and long-term investments still outweighs the sum of its debt and operating lease liabilities (US$770.0 million).

3. A management team with integrity, capability, and an innovative mindset

There are recent management changes at Alteryx that we want to comment on. Alteryx was founded in 1997. One of its co-founders, Dean Stoecker, 63, recently stepped down as CEO in October 2020 after being in the role since the company’s birth. Stepping into Stoecker’s shoes as CEO is the 58 year-old Mark Anderson. Anderson’s not a stranger to Alteryx because he has been a director of the company since October 2018. Alteryx’s new CEO brings with him around a decade of leadership experience in technology companies. Prior to joining Alteryx as a director, Anderson was President of Palo Alto Networks, a company specialising in cybersecurity.

It’s still too early to tell if Anderson will be a good CEO for Alteryx, so that’s a risk. But he looks like a safe pair of hands for now. In Alteryx’s announcement on the appointment of Andersen as CEO, Stoecker said:

“When I decided to transition from day-to-day operations, it was clear to me that Mark is the ideal candidate to serve as Alteryx’s next CEO given his passion for our company and our newly created Analytic Process Automation category, coupled with his experience in scaling organizations. Since joining our Board two years ago, Mark has proven himself as a trusted advisor providing valuable insights and strategic direction. I am confident that Alteryx will achieve new heights under his leadership.”

It’s also a positive sign for us that Anderson had already been a director of the company for two years before he took on the CEO role. Moreover, Stoecker continues to have a heavy say on Alteryx’s future – he was appointed as executive chairman of the company on the same day he stepped down as CEO. Stoecker has been Alteryx’s chairman since the company’s founding.

The other recent change of the guard involves another of Alteryx’s co-founders, the 57-year-old Olivia Duane Adams. Earlier this month, Adams stepped down from her role of chief customer officer (CCO) to become the company’s chief advocacy officer (CAO) and “focus on strengthening upskilling efforts for customers to enable a culture of analytics, scaling the presence of Alteryx in academia and furthering diversity and inclusion in the technology space.” Alteryx’s new CCO is Matthew Stauble, who has more than 20 years of experience in customer-centric roles. Prior to joining Alteryx, Stabuel was with Pensando Systems, “a developer of new edge services models of enterprise and cloud computing.” Stauble was also once at Palo Alto Networks, helping grow the company’s customer organisation from just 15 people to a huge team of more than 1,200.

On integrity

We can’t tell what Mark Anderson’s compensation as Alteryx’s CEO will look like. But we’re heartened by what we know about the compensation structure for Alteryx’s management team in 2019. Here are the highlights:

- For the year, Dean Stoecker’s total compensation as CEO was US$6.53 million. This is a reasonable sum when compared to the scale of Alteryx’s business.

- 81.7% of Stoecker’s total compensation in 2019 came from restricted stock units (RSUs) and stock options that both vest over three years.

- 71.1% to 98.1% of the total compensation of Alteryx’s other key leaders in 2019 also came from RSUs and stock options that both vest over three years.

- What these numbers mean is that the vast majority of the total compensation of Alteryx’s management team in 2019 depends on multi-year changes in the company’s stock price, which is in turn driven by the company’s business performance. So, the interests of Alteryx’s management team are well-aligned with the company’s other shareholders, in our opinion.

Moreover, Stoecker controlled 8.25 million Alteryx shares as of 1 March 2020. These shares are worth nearly US$974 million at the company’s stock price of US$118 as of 12 December 2020. This is a large stake and it likely further aligns the interests of Stoecker with Alteryx’s other shareholders.

We want to highlight that nearly 98% of Stoecker’s Alteryx shares are of the Class B variety. Alteryx has two share classes: (1) The publicly-traded Class A shares with 1 voting right per share; and (2) the non-traded Class B shares with 10 voting rights each. So, Stoecker controlled nearly 44% of the voting power in the company as of 1 March 2020 despite holding only 12.5% of the total shares. A manager having significant control over the company can potentially be bad for shareholders. This concentration of Alteryx’s voting power in the hands of Stoecker means that we need to be comfortable with his influence over the company. We are.

On capability and innovation

Alteryx’s business has changed dramatically over time since its founding. In its early days, the company was selling software for analysing demographics. Alteryx’s current core data analytics software platform was launched only in 2010, and a subscription model was introduced relatively recently in 2013. We see Alteryx’s long and winding journey to success as a sign of Stoecker and his team’s ability to adapt and innovate.

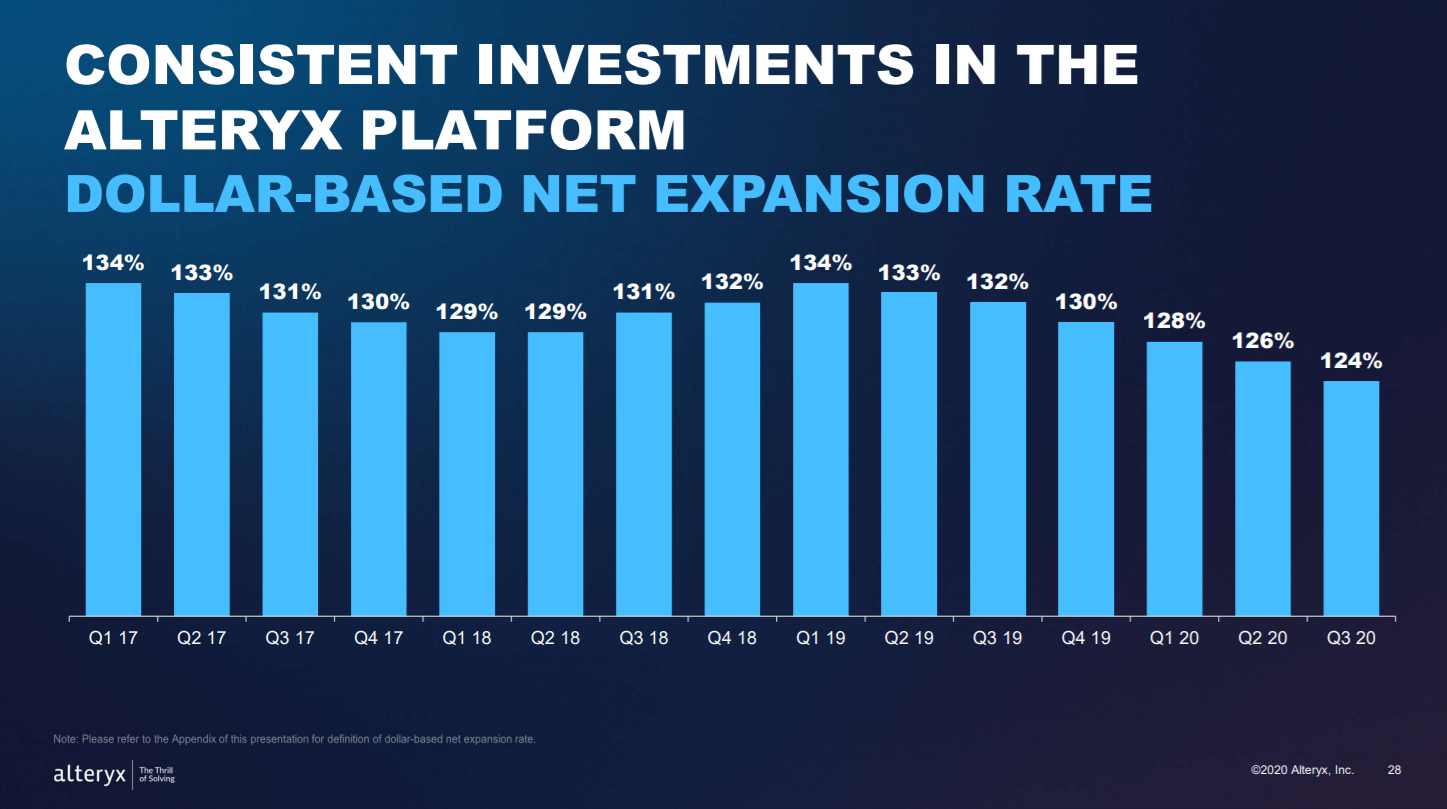

We also credit Alteryx’s management with the success that the company has found in the land-and-expand strategy. The strategy starts with the company landing a customer with an initial use case, and then expanding its relationship with the customer through other use cases. The success can be illustrated through Alteryx’s impressive dollar-based net expansion rates (DBNERs). The metric is a very important gauge for the health of a SaaS (software-as-a-service) company’s business. It measures the change in revenue from all the company’s customers a year ago compared to today; it includes positive effects from upsells as well as negative effects from customers who leave or downgrade. Anything more than 100% indicates that the company’s customers, as a group, are spending more.

Alteryx’s DBNER has been more than 120% in each of the last 23 quarters – that’s nearly six years! The chart below illustrates Alteryx’s DBNER going back to 2017’s first quarter.

Source: Alteryx 2020 third quarter earnings presentation

Alteryx’s management has also led impressive customer-growth at the company. The company’s customer count has nearly quintupled from 1,398 at the end of 2015 to 6,955 in 2020’s third quarter.

But there is a key area where Alteryx’s management has fallen short: The development of the company’s culture. Glassdoor is a platform that allows employees to rate their companies anonymously. Alteryx currently has a 3.7-star rating on Glassdoor (out of 5), and only 70% of reviewers will recommend the company to friends. Mark Anderson has a high CEO-approval rating of 98%, but that has come from only six reviews; moreover, he has not been in the CEO role long enough yet to really warm the seat. Meanwhile, SAP, a competitor of Alteryx, has 4.6 stars on Glassdoor, and recommendation and CEO-approval ratings of 95% and 97%, respectively. Alteryx has managed to post impressive business-results despite its seemingly poorer culture, but we’re keeping an eye on things here.

All of the positive points (and the one negative point) we mentioned above about Alteryx’s management team in the “On capability and innovation” sub-section of this article probably does not have too much to do with the company’s new CEO Mark Anderson. But as we mentioned earlier, Anderson seems like a safe pair of hands to us for now. Moreover, he will still be able to tap on the experience of Stoecker, Olivia Duane Adams, and Alteryx’s third co-founder, Ned Harding. Harding, who’s 52 this year, was a key technology leader in the company and left in July 2018; he remains an advisor to Alteryx’s software engineering teams. And speaking of Alteryx’s leadership in technological roles, the company’s chief technology officer is currently Derek Knudsen, 46. He stepped into the position in August 2018 after Harding’s departure. Knudsen had accumulated over 20 years of experience working with technology in companies in senior leadership positions before joining Alteryx.

4. Revenue streams that are recurring in nature, either through contracts or customer-behaviour

Alteryx’s business is built nearly entirely on subscriptions, which theoretically generate recurring revenue for the company. The company sells access to its data analytics platform through subscriptions, which typically range from one to three years. For the first nine months of 2020 and the whole of 2019, 2018, 2017, and 2016, more than 95% of Alteryx’s revenue in each year came from subscriptions to its platform; the rest of the revenue came from training and consulting services, among others.

But just having a subscription model does not equate to actually having recurring revenues. If your business has a high churn rate (the rate of customers leaving), you’re constantly filling a leaky bucket. That’s not recurring income. In the case of Alteryx, the company has an excellent track record of producing high DBNERs, and this means the company has no problem with retaining customers and getting them to spend more in aggregate over time.

5. A proven ability to grow

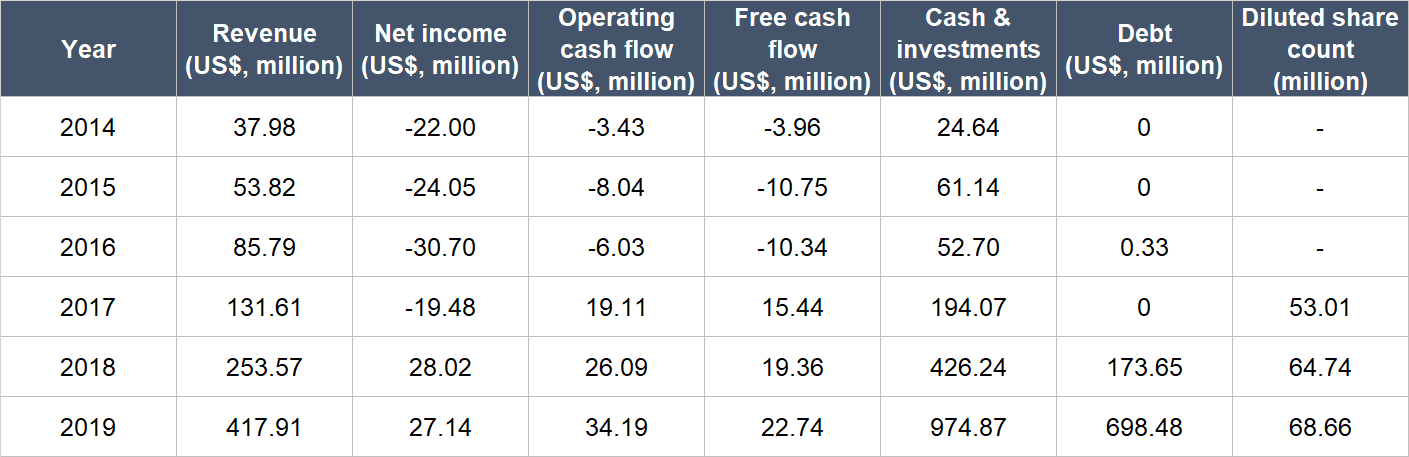

There isn’t much historical financial data to study for Alteryx, since the company was listed only in March 2017. But we do like what we see.

Source: Alteryx IPO prospectus and annual reports

A few key points to note:

- Alteryx has compounded its revenue at an impressive annual rate of 61.6% from 2014 to 2019. The astounding revenue growth of 92.7% in 2018 was partly the result of Alteryx adopting new accounting rules in the year. Alteryx’s revenue for 2018 would have been US$204.3 million after adjusting for the impact of the accounting rule, representing slower-but-still-impressive top-line growth of 55.2% for the year. 2019 saw the company maintain breakneck growth, with its revenue up by 64.8%.

- Alteryx started making a profit in 2018, and also generated positive operating cash flow and free cash flow in 2017, 2018, and 2019.

- Annual growth in operating cash flow and free cash flow from 2017 to 2019 was strong at 33.8% and 21.4%, respectively.

- The company’s balance sheet remained robust throughout the timeframe under study, with significantly more cash and investments than debt.

- At first glance, Alteryx’s diluted share count appeared to increase sharply by 22.1% from 2017 to 2018. But the number we’re using is the weighted average diluted share count. Right after Alteryx got listed in March 2017, it had a share count of around 57 million. This means that the increase in 2018 was milder (in the mid-teens range) though still higher than what we would typically like. The good news is that the diluted share count inched up by only 6% in 2019, which is acceptable, given the company’s rapid growth. We will be keeping an eye on Alteryx’s dilution.

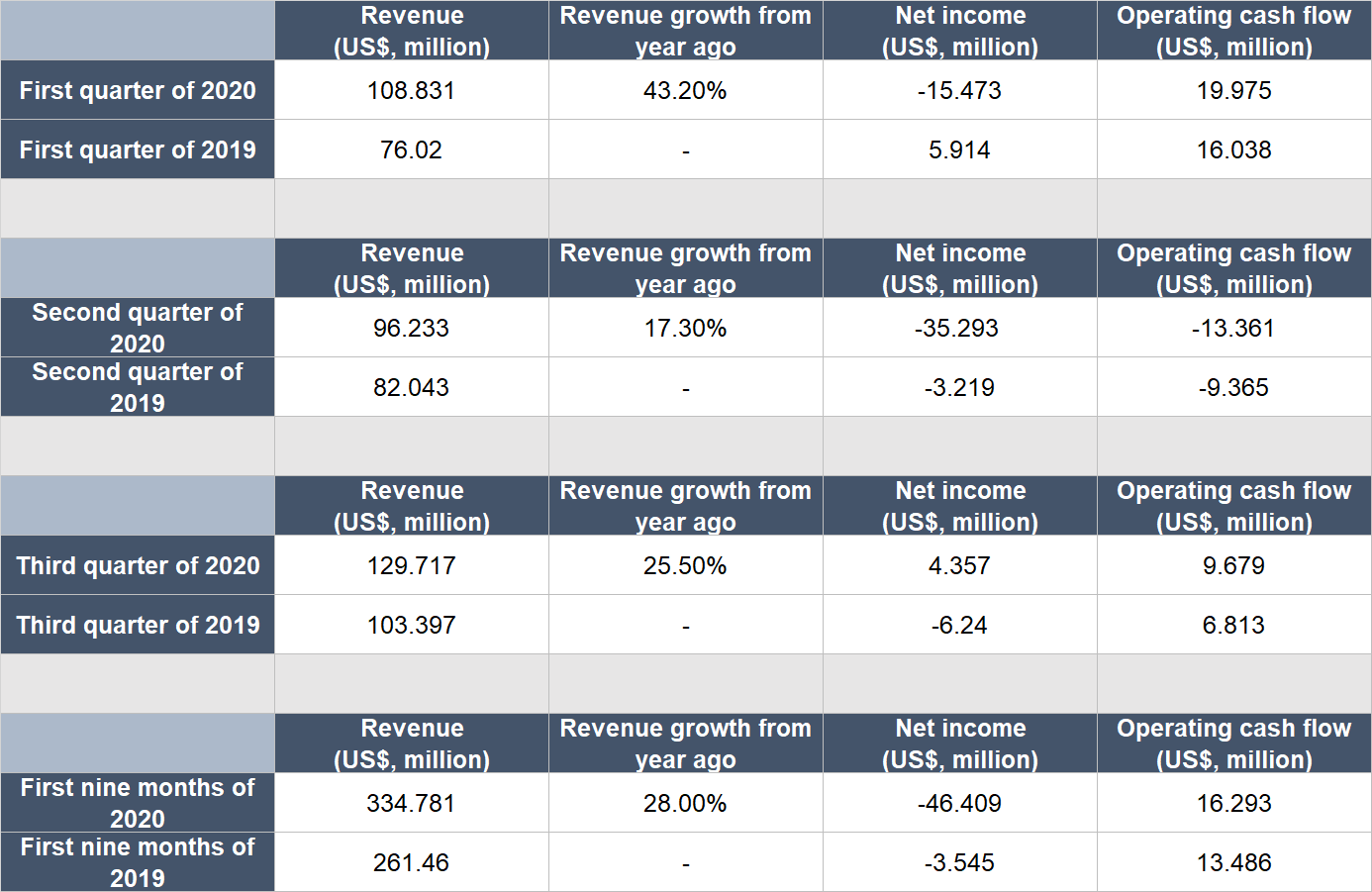

Alteryx has managed to continue growing in 2020, but its growth in this year so far has decelerated significantly because of the current COVID-19 pandemic. The table below illustrates the year-on-year changes in Alteryx’s revenue, net income, and operating cash flow for the first three quarters of this year. Alteryx started to experience negative impacts to its customers’ buying behaviour (such as decreased customer engagement, longer sales cycles, and deterioration in near-term demand) in March of this year because of COVID-19 and these impacts are still being felt. It’s not really a big surprise that COVID-19 has hurt Alteryx’s growth, since the company’s software products are not cheap – they cost upwards of thousands of dollars per user. But we think COVID-19 is only a short-term hiccup for the company. Alteryx’s self-serve data analytics platform helps solve an important pain-point for many organisations and there is a powerful long-term tailwind in the company’s favour (the strong growth in data-creation mentioned earlier).

Source: Alteryx quarterly earnings updates

6. A high likelihood of generating a strong and growing stream of free cash flow in the future

Alteryx has already started to generate free cash flow. Right now, the company has a poor trailing free cash flow margin (free cash flow as a percentage of revenue) of just 3.6%.

But over the long run, Alteryx expects to generate a strong free cash flow margin of 30% to 35%. We think this is a realistic and achievable target. There are other larger subscription-based software companies – such as Adobe and Veeva Systems in Compounder Fund’s portfolio – with a free cash flow margin around that range or higher.

Valuation

We completed our purchases of Alteryx’s shares with Compounder Fund’s initial capital in late July 2020. Our average purchase price was US$170 per Alteryx share. At our average price and on the day we completed our purchases, Alteryx’s shares had a trailing price-to-sales (P/S) ratio of around 25. We like to keep things simple in the valuation process. In Alteryx’s case, we think the P/S ratio is an appropriate metric to gauge the value of the company, since it does not have a long history yet of generating free cash flow.

There’s no need to consult any historical valuation chart to know that the P/S ratio of 25 is high – and that’s a risk. For perspective, if we assume that Alteryx has a 30% free cash flow margin today, then the company would have a price-to-free cash flow ratio of 83 (25 divided by 30%).

But Alteryx also has a few strong positives going for it. The company has: (1) a huge addressable market in relation to its revenue; (2) a large and rapidly expanding customer base; and (3) very sticky customers who have been willing to significantly increase their spending with the company over time. We believe that with these traits, there’s a high chance that Alteryx will continue posting excellent revenue growth – and in turn, excellent free cash flow growth – in the years ahead.

For perspective, Alteryx carried a P/S ratio of around 16 at the 12 December 2020 stock price of US$118.

The risks involved

We see a few key risks in Alteryx, with the high valuation being one. If there are any future slowdowns in Alteryx’s growth – even if they are temporary – there could be a painful fall in the company’s share price. This is a risk we’re comfortable taking on as long-term investors.

Competition is another important risk. We mentioned earlier that Alteryx’s primary competitors are spreadsheets, or custom-built approaches. But the company’s data analytics platform is also competing against services from other technology heavyweights with much stronger financial resources, such as IBM, Microsoft, Oracle, and SAP. Providers of data visualisation software, such as Tableau, could also decide to move upstream and budge into Alteryx’s space. To date, Alteryx has dealt with competition admirably – its quarterly DBNERs and growth in customer numbers are impressive. We’re watching these two metrics to observe how the company is faring against competitors.

Two other key risks deal with hacking and downtime in Alteryx’s services. The company’s platform is important for users, since it is used to crunch data to derive actionable insights; it is also likely that Alteryx’s platform is constantly fed with sensitive information of its users. Should there be a data breach on the platform, and/or if the platform stops working for extended periods of time, Alteryx could lose the confidence of its customers.

Then there’s also succession risk with Alteryx. We had discussed the recent management shuffles at Alteryx earlier. We’re watching how Mark Anderson, Alteryx’s new CEO, performs.

Lastly, the following are all yellow-to-red flags for us regarding Alteryx: (1) The company’s DBNER comes in at less than 100% for an extended period of time; (2) it fails to increase its number of customers; and (3) it’s unable to convert revenue into free cash flow at a healthy clip in the future.

Summary and allocation commentary

Summing up Alteryx, it has:

- A valuable self-service data analytics platform that addresses customers’ pain-points and is superior to legacy methods for data analysis;

- high levels of recurring revenue;

- outstanding revenue growth rates;

- positive profit and free cash flow, with the potential for much higher free cash flow margins in the future;

- a large and mostly untapped addressable market;

- an impressive track record of winning customers and increasing their spending; and

- a capable and sensibly-incentivised CEO in Dean Stoecker who recently transitioned to the executive chairman role

The company does have a premium valuation, so we’re taking on valuation risk. There are also other risks to note, such as tough competition; hacking and downtime; and the recent CEO change.

But after considering Alteryx’s pros and cons, we initiated a 1.0% position – a small-sized allocation – in the company with Compounder Fund’s initial capital. We appreciate all the positives that we see in Alteryx, but our enthusiasm is tempered by the company’s high valuation and slowdown in growth because of COVID-19.

And here’s an important disclaimer: None of the information or analysis presented is intended to form the basis for any offer or recommendation; they are merely our thoughts that we want to share. Of all the companies mentioned in this article, Compounder Fund also currently owns shares in Alphabet, Amazon.com, Microsoft and MongoDB. Holdings are subject to change at any time.