Compounder Fund: Visa Investment Thesis - 20 Dec 2020

Data as of 18 December 2020

Visa Inc (NYSE: V) is one of the 40 companies in Compounder Fund’s initial portfolio. This article describes our investment thesis for the company.

Company description

Many of you who are reading this are likely to be familiar with Visa. Chances are, you have a Visa credit card in your wallet.

The company’s roots can be traced back to 1958 when Bank of America launched its BankAmericard credit card pilot. Today, Visa a leading global digital payments processor. You can think of Visa as the middleman in a four-party model, where the parties are: The card-issuing financial institution (in Singapore’s context, banks such as DBS, OCBC, and UOB will be the card-issuers); the merchant; the acquirer (the merchant’s bank); and the account holder (the individual who owns the credit card).

![]()

Source: Visa website

It is important to distinguish Visa from financial institutions. Visa does not extend credit to users during transactions, so it does not incur any credit risk that is related to customer defaults; the credit card issuer – the financial institution – ultimately bears the default risk. Visa also does not earn from the interest that credit card users are charged for their credit card debt. What Visa does in a typical transaction is to provide transaction processing services (such as authorisation, clearing, and settlement) to financial institutions and merchants. Visa ensures that the money is safely transferred from the cardholder’s account with the card issuer to the merchant’s account with the acquirer.

Visa’s net revenue for its fiscal year ended 30 September 2020 (FY2020) was US$21.85 billion and this came from five main sources:

- Service revenues (US$9.80 billion) consist of revenues earned by Visa for services provided to customers that use the company’s payment network and they depend primarily on payment volume.

- Data processing revenues (US$10.98 billion) depend mostly on the number of transactions and they are the small fees that Visa charges for authorisation, clearing, settlement, value-added services, network access, and other maintenance and support services that facilitate each transaction happening on Visa’s payment networks.

- International transaction revenues (US$6.30 billion) are earned when Visa processes cross-border transactions and helps with currency conversion activities.

- Other revenues (US$1.43 billion) consist of value-added services, license fees for use of the Visa brand and technology, fees for product enhancements (such as extended account holder protection and concierge services) and more.

- Client incentives (-US$6.66 billion) are payments that Visa pays to its customers to help grow its payment volume. The sum of service revenues, data processing revenues, international transaction revenues, and other revenues make up Visa’s revenue. We arrive at Visa’s net revenue when we subtract client incentives from revenue.

With the ability to facilitate digital payments in more than 200 countries and territories, it should not surprise you to find that Visa has a strong international presence. In FY2020, the USA accounted for 46.3% of the company’s net revenue of US$21.85 billion while international markets collectively accounted for the rest. No other country except for the USA made up more than 10% of Visa’s net revenue during the year.

Investment thesis

We have laid out our investment framework in Compounder Fund’s website. We will use the framework to describe our investment thesis for Visa.

1. Revenues that are small in relation to a large and/or growing market, or revenues that are large in a fast-growing market

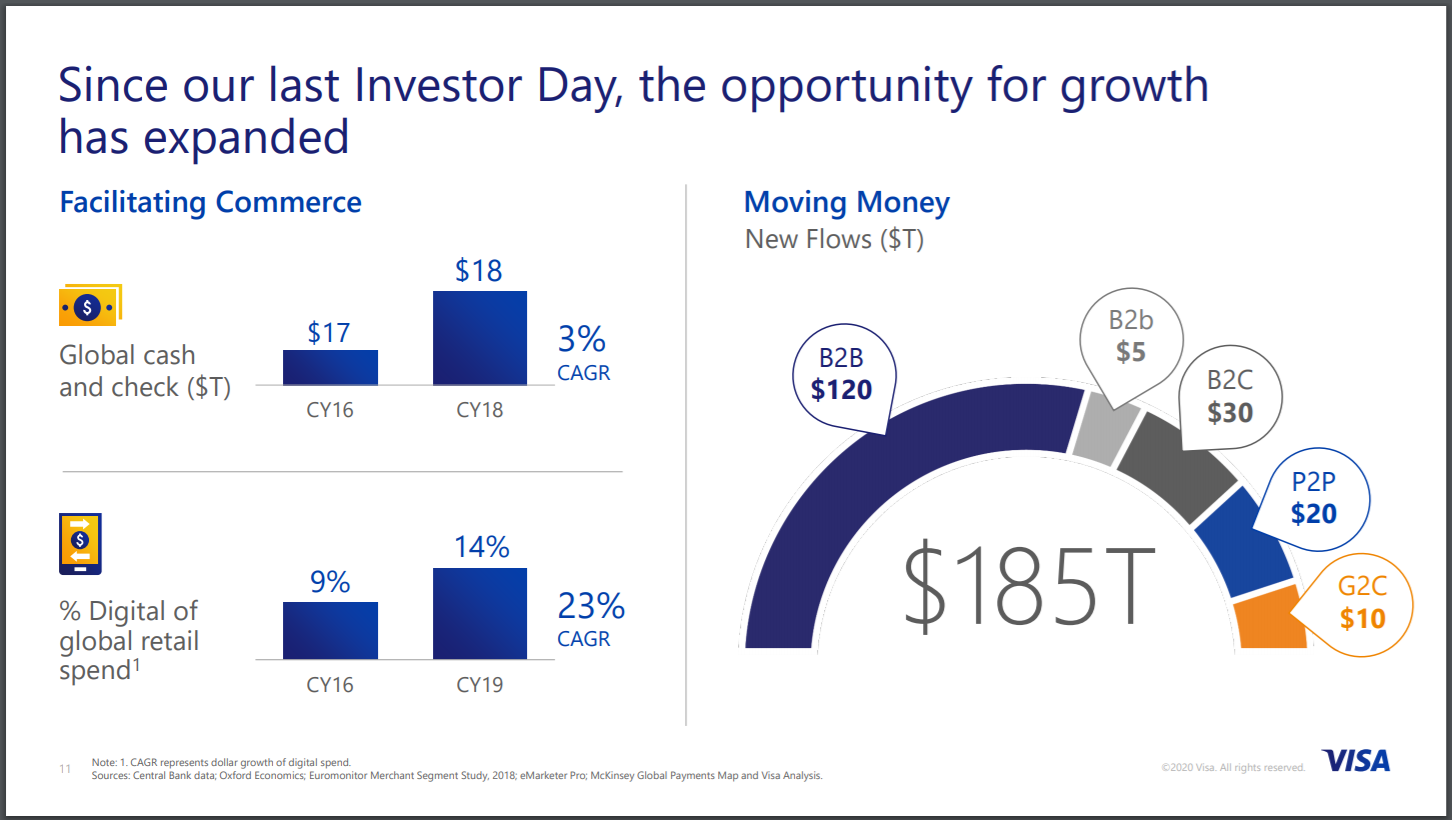

On the surface, Visa’s business already looks huge. As of 30 September 2020, Visa had 3.5 billion cards in issue. The company processed 140.8 billion transactions in FY2020 and handled total volume of US$11.3 trillion during the year (of which US$8.8 trillion was in payments volume and the rest in cash volume). These activities helped Visa to bring in its aforementioned net revenue of US$21.85 billion for the same period. But the reality is that Visa is barely scratching the surface of its global opportunity. Alfred Kelly, Visa’s CEO and chairman, said the following during the company’s 2020 Investor Day event held on 11 February this year:

“Despite the incredible growth in digital payments, the amount of cash and check usage has increased since 2016 [to reach US$18 trillion in 2018]. Retail digital spending has grown a compounded 23% in the last three years. Yet, it is only 14% of global retail spending and we estimate that there’s a US$185 trillion of money movement flows to be captured that are still utilizing checks, wires and ACH (automated clearing house). So, we clearly see a new growth inflexion point, and there’s opportunity to move money via our network of networks. New flows, new players, new partnerships and connected devices will open tremendous opportunities for us in the next 5 to 10 years. And our goal is to take advantage of this inflexion point to continue to drive our key business indicators and financial results as we have over the last number of years.”

So, Visa is seeing total payment flows of US$203 trillion (US$18 trillion in cash and check usage in commerce activity, plus US$185 trillion in money-movement flows) that it could potentially divert to its network. This is shown in the chart below:

Source: Visa 2020 Investor Day presentation

Visa’s core business currently is to facilitate personal consumption expenditure. But as mentioned earlier, the company has recently started focusing on capturing new flows that amount to US$185 trillion. The new flows include money-flow in various areas such as B2B (business to business), B2b (business to small business), B2C (business to consumer), P2P (peer to peer) and G2C (government to consumer); these are shown in the chart below. The new flows represent a large opportunity that Visa has barely tapped. At the time of Visa’s 2020 Investor Day event, the company had only captured less than 1% of the market.

Source: Visa 2020 Investor Day presentation

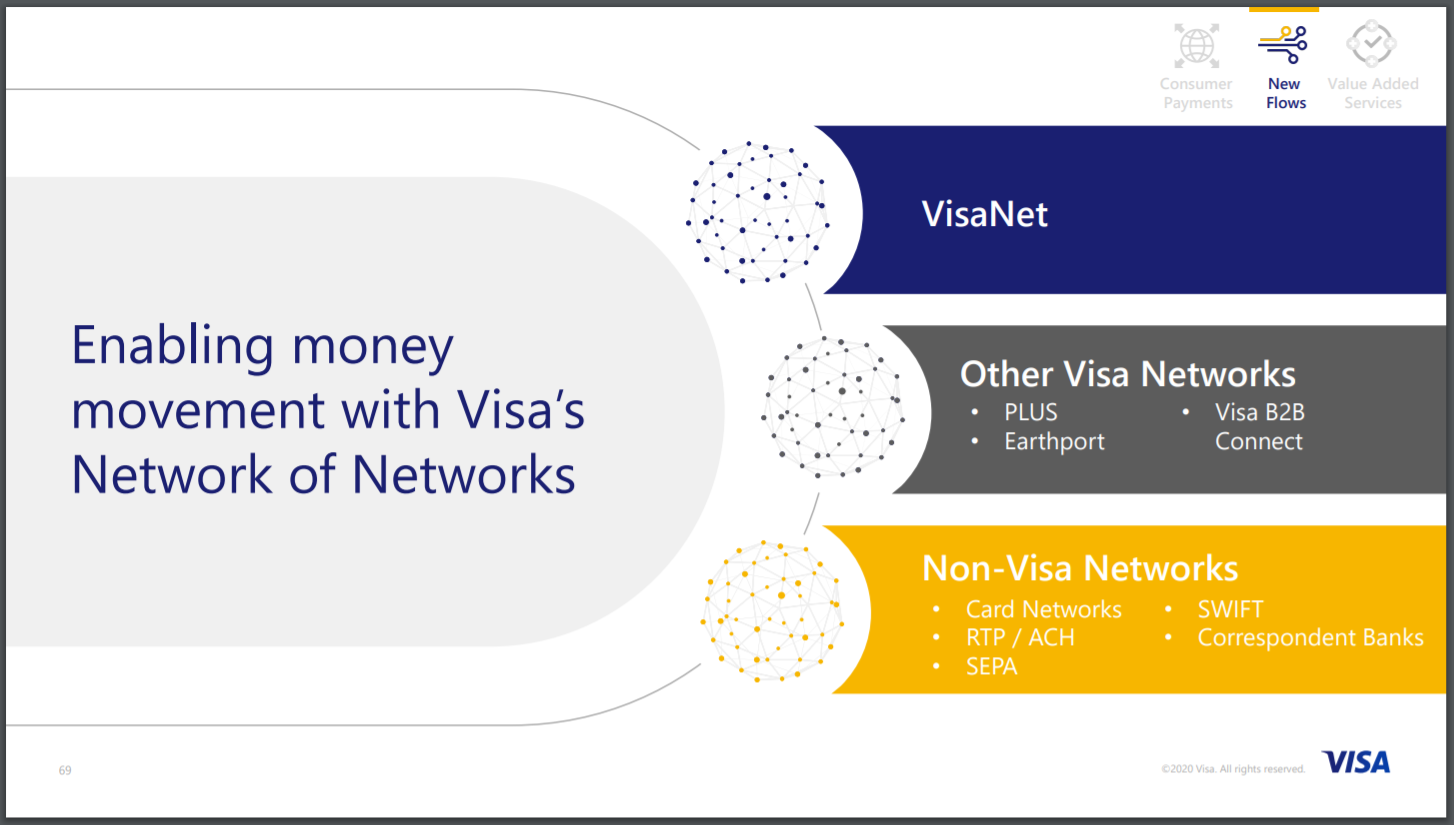

In the chart just above and in the quote from Kelly that we shared earlier, there was the term “network of networks.” This refers to Visa’s strategy of moving money faster and better for its customers through using its own payment networks in conjunction with other networks. The two charts below illustrate how this works:

Source: Visa 2020 Investor Day presentation

2. A strong balance sheet with minimal or a reasonable amount of debt

As of 30 September 2020, Visa has US$20.72 billion in cash and short-term investments, against total debt of US$24.07 billion. This puts Visa in a net debt position of US$3.35 billion.

We generally prefer a balance sheet that has more cash than debt. But we still think that Visa’s balance sheet is healthy. This is because Visa has an excellent track record in generating free cash flow, which we will discuss later. Moreover, Visa’s net debt position looks very manageable when compared to the company’s average free cash flow of US$11.32 billion for FY2018, FY2019, and FY2020.

3. A management team with integrity, capability, and an innovative mindset

On integrity

As we mentioned earlier, Visa is led by Alfred Kelly, 62, who holds the role of CEO and chairman. He has been a director of Visa since 2014 and became Visa’s CEO four years ago in December 2016. We appreciate his multi-year tenure with Visa as well as the experience that he brings to the table. He was with one of Visa’s main competitors, American Express, for 23 years from 1987 to 2010 and served in various senior leadership roles, including as president from July 2007 to April 2010. Just prior to joining Visa, Kelly was president and CEO at Intersection, a technology and digital media company backed by Alphabet, the parent of the internet search engine Google.

For FY2020, Kelly’s total compensation was a princely sum of US$25.15 million. But it’s a rounding error when compared to Visa’s profit and free cash flow of US$10.87 billion and US$9.70 billion, respectively, in the same year. More importantly, we think that his compensation structure strongly aligns his interests with those of Visa’s shareholders. Here are the important points:

- For FY2020, 81.5% of Kelly’s total compensation was from stock options, restricted stock units (RSUs), and performance shares.

- The stock options and RSUs collectively account for half of the total value of Kelly’s stock-based compensation and they both vest over three years.

- The performance shares, which make up the other half of the total value of Kelly’s stock-based compensation, are based on (1) Visa’s earnings per share growth over a three-year period, and (2) changes in Visa’s share price, after adjusting for dividends, over the same timeframe. Kelly may ultimately earn even zero performance shares if the growth of Visa’s earnings per share and dividend-adjusted stock price is not up to mark. We emphasised the term “per share” because Visa shareholders can only benefit from the company’s growth if there is per-share growth.

- The lion’s share of Kelly’s total compensation for FY2020 thus came from components that effectively depend on multi-year changes in both Visa’s share price and business performance.

The majority of the total compensation of Visa’s other key leaders for FY2020 also came from stock options, RSUs, and performance shares that have the same characteristics as Kelly’s (see table below). And just like Kelly, the other important managers in Visa have also mostly been with the company for a number of years and we appreciate their multi-year tenures:

Source: Visa FY2020 proxy statement

And speaking of alignment of interests, there’s something else we want to highlight: Visa has stock ownership guidelines for its key leaders. Kelly is required to own Visa shares that are worth at least six times his base salary (US$1.55 million for FY2020) while Visa’s other key leaders are required to own shares that are between three and four times their base salaries. As of 27 November 2020, Kelly controlled 665,760 Visa shares which have a sizable value of more than US$140 million at the company’s 18 December 2020 share price of US$211.

On capability and ability to innovate

We rate Kelly and his team pretty highly on this front and there are a few things we want to discuss.

First is Visa’s stellar recent track record of growth for its key business metrics. Visa is a digital payment services provider. The important business metrics that showcase the health of its network are: (1) The total volume that flows through the network; (2) the payments volume that its network handles; (3) the number of transactions the network processes; (4) the number of the company’s cards that are in circulation; and (5) the number of merchant locations that accept Visa cards. The table below shows how the five metrics have grown in each year since 2007 (note the large scale of these metrics too). We picked 2007 as the start so that we can understand how Visa’s business fared during the 2008-09 Great Financial Crisis. (As far as we can tell, Visa only started reporting the number of merchant locations in FY2018, so that year is the starting point for the metric.)

![]()

Source: Visa annual reports

Second, we think Visa’s management has been entering into smart partnerships to keep the company relevant for the future. Two examples: (1) fintech company Square’s Cash Card is a Visa debit card that users can use for payments directly from their Cash App balance; (2) Visa has partnered with Phone maker Apple to offer Visa cards on Apple Pay. Here are some choice comments on Visa’s future-proofing partnerships that management shared during the company’s February 2020 Investor Day event:

“Growing our acceptance footprint has been a key focus for Visa in China. And we’ve invested heavily in this and continue to work with our long-term partners to drive acceptance. All that hard work resulted in 18 times increase in pass acceptance in the past three years to over 6 million merchants, diversifying largely from the travel and lodging segment into a wide range of segments, and penetrating further into smaller cities. But this 18 times growth is still not good enough. We’ve still got lots more to do, and that’s why we’re partnering with leading wallet platforms like WeChat pay, Alipay and UnionPay to enable more than 50 million QR merchant locations to accept inbound Visa credentials…

…Person-to-person payments is a huge market for Visa Direct, this is a springboard use case for consumers creating the first exposure to what is possible with real-time payment experiences. Visa partners with all top-seven global P2P brands such as PayPal, Venmo, Square Cash, Google and Apple, and in total, powers over 100 P2P programs globally driving 100-plus year-on-year growth in this segment. P2P partnerships take a number of different forms. For mobile and messenger platforms like Apple and Facebook, we have embedded Visa Direct payment APIs within their customer directories, enabling the billions of consumers they serve to send real-time payments seamlessly within their ecosystem.”

Third, we think Visa has demonstrated a strong ability to innovate. This is related to the second point above because the aforementioned partnerships with fintech leaders around the world itself requires innovative thinking and solutions on the part of Visa. An example of Visa’s innovation is the company’s successful launch of payment tokenisation in recent years.

Tokenisation is the process of replacing the traditional payment card account number with a unique digital token in online and mobile transactions. The whole tokenisation process happens in the background in a way that is invisible to the customer, improving security without hampering the ease of use. Tokens eliminate the need for users to keep entering and reentering their account number when shopping online and can prevent fraud. During Visa’s aforementioned Investor Day event earlier this year, management said that the company has been making tremendous progress with tokenisation and already has more than 750 million tokens that support 6 billion transactions annually.

Fourth, Visa’s recent acquisitions look shrewd to us. In the second half of 2019, Visa purchased Earthport, a provider of cross-border payment services to banks and other money-transfer service providers. The acquisition expanded Visa’s reach to 99% of bank accounts in 88 countries and added 1.5 billion incremental bank accounts that were previously not within Visa’s network; prior to Earthport, Visa could ‘only’ reach about half of the world’s bank accounts.

In January this year, Visa announced that it had agreed to acquire Plaid for US$5.3 billion. Plaid is a financial data network that makes it easy for people to securely connect their financial accounts to the apps they use to manage their financial lives. At the time the acquisition was announced, one in four people with a US bank account were using Plaid to connect to more than 2,600 fintech developers across more than 11,000 financial institutions. Visa’s management believes that Plaid will help to expand Visa’s addressable market by providing high-value connectivity services to fast-growing fintech companies. We agree. But the acquisition has yet to close and is currently put on hold due to an antitrust lawsuit filed by the US government in November 2020. We’re keeping an eye on developments here.

Fifth, we think Kelly and his team have so far been excellent at allocating capital in terms of engaging in share buybacks. From FY2016 to FY2020, Visa’s diluted share count has declined by a total of 2.0% per year (there will be more on Visa’s diluted share count later). From 1 October 2016 to 18 December 2020, Visa’s share price has increased by an impressive 164% after adjusting for dividends. This means that Visa has managed to repurchase its shares at relatively low prices and thus, the buybacks have been great uses of capital.

Sixth, Kelly appears to have built an excellent corporate culture at Visa and we’ve been impressed by the actions of Visa’s leadership during the current COVID-19 pandemic. On the corporate culture front, Visa has strong ratings on Glassdoor, a platform that allows a company’s employees to rate it anonymously. Currently, 77% of Visa-raters on Glassdoor will recommend the company to a friend. Meanwhile, Kelly has a 94% approval rating, far higher than the average Glassdoor CEO rating of 69% in 2019. Regarding the actions of Visa’s leadership during the pandemic, Kelly said the following in an August 2020 interview with Business Roundtable, an “association of CEOs of leading U.S. companies working to promote sound public policy and a thriving U.S. economy”:

“When Covid-19 struck, my immediate priority was the health and well-being of our employees and their families. First, in March, I pledged to our 20,000 employees there would be no Covid-19 related layoffs in the calendar year 2020. This gave employees peace of mind so they could focus on their work and their families.

Second, we made the decision to give employees the option to work from home through the 2020 calendar year. Today, the vast majority of Visa’s employees are working from home, and while things are clearly different, the people of Visa have adjusted and we are operating quite efficiently and effectively. While we will look at bringing employees back into our offices on a site-by-site basis in stages, the flexibility to remain working remotely is the right thing to do at this time for our communities, our employees and their families. It simply seems wrong for Visa employees to be crowding transit systems and roads when we have the flexibility to continue full business continuity while working from home.

Third, given that creating community for employees is more important than ever in a virtual environment, I record weekly videos for our employees globally, providing updates on our business operations. I also have been dropping into virtual happy hours and team meetings. In some ways, I am more connected with employees than ever.

Fourth, in recognition of the challenges working from home and balancing personal and professional responsibilities brings, we have re-invested in employees’ mental health by creating a mental health and wellbeing digital and peer community. To date, we have hosted over 10 mental health and wellbeing events.”

4. Revenue streams that are recurring in nature, either through contracts or customer-behaviour

We believe that Visa has recurring revenue simply due to repeat customer behaviour. Each time someone makes a purchase and pays with a Visa credit card, or a transaction is made on Visa’s network, the company earns a small fee.

We showed earlier that the company handled trillions in dollars worth of payments in FY2020 and processed billions of transactions – both numbers have also grown impressively over time. Visa’s payments volume and number of transactions, together with the fact that no individual customer accounted for more than 12% of Visa’s net revenues in FY2018, FY2019, and FY2020, lend further weight to our view that the company’s revenue streams are largely recurring in nature.

Yes, COVID-19 has hurt Visa’s business by reducing spending opportunities, especially those related to travel. But we think that this is just a temporary deviation from typical human behaviour. When COVID-19 stops being a serious global health threat, spending activity should recover, providing the fuel for Visa’s growth.

5. A proven ability to grow

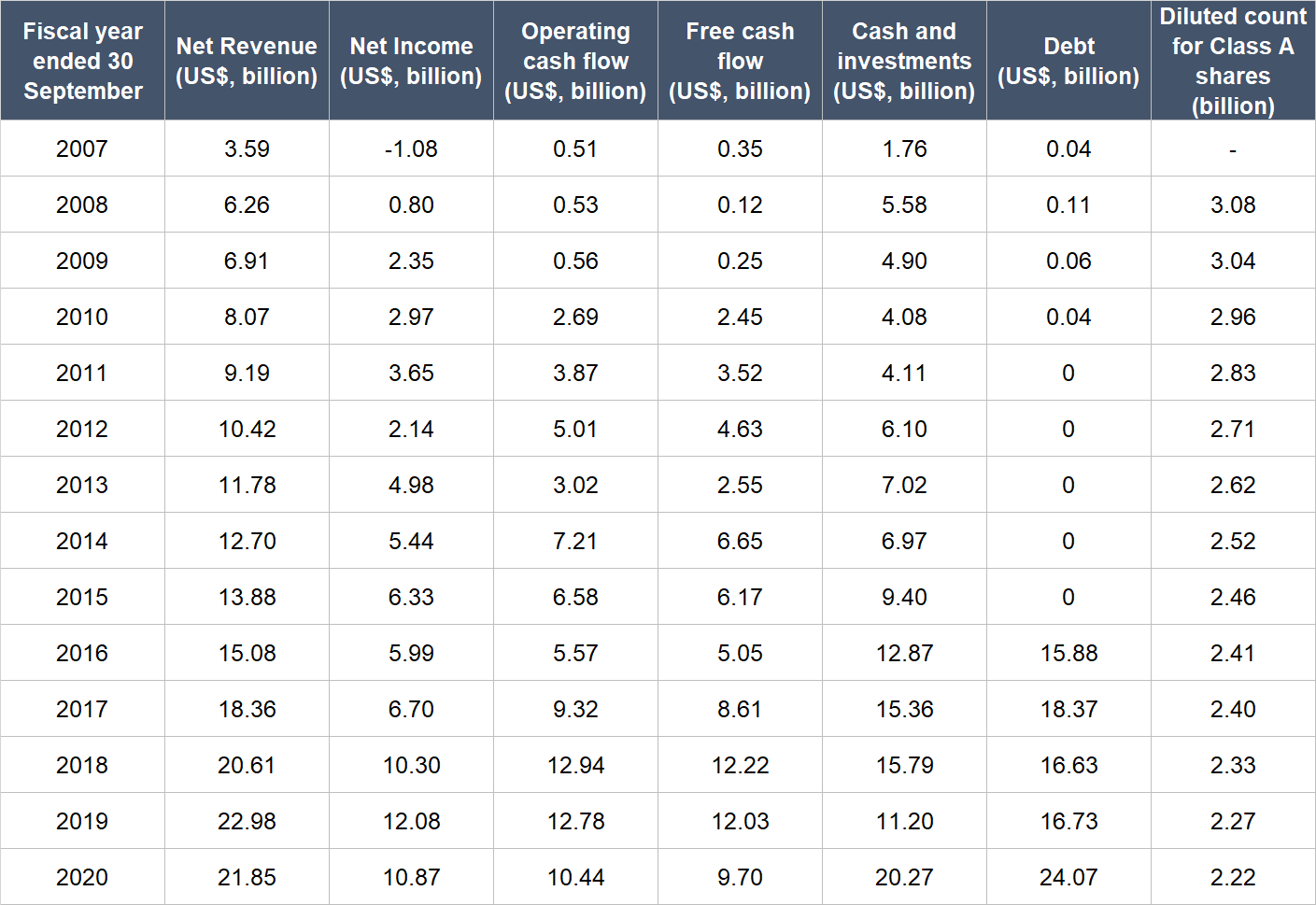

The table below shows Visa’s important financials from FY2007 to FY2020:

Source: Visa annual reports

A few key points about Visa’s financial track record:

- Net revenue compounded decently at 14.9% per year from FY2007 to FY2020; over the last four years from FY2016 to FY2020 (this essentially covers the entire time frame that Kelly has been CEO of Visa), the company’s annual topline growth was slower but still respectable at 9.7%.

- The company also managed to produce net revenue growth in FY2008 (74.5%) and FY2009 (10.4%); those were the years when the global economy was rocked by the Great Financial Crisis.

- Net profit surged by 24.2% per year from FY2008 to FY2020 (we started counting from FY2008 since Visa reported a loss in FY2007). Visa’s annual net profit growth from FY2016 to FY2020 was similarly healthy at 16.1%. Net profit was negative in FY2007 because of a large litigation provision of US$2.65 billion incurred during the year, but it is not a cause for any concern to us.

- Operating cash flow was consistently positive and grew in most years for the entire time frame we studied. It also increased markedly with growth of 26.4% per year. The growth rate from FY2016 to FY2020 was still impressive at 17.0% annually.

- Free cash flow was consistently positive too and had stepped up from FY2007 to FY2020 at a rapid clip of 29.3% per year. The annual growth in free cash flow from FY2016 to FY2020 was 17.7% – not too shabby.

- Visa’s balance sheet carried more cash and investments than debt from FY2007 to FY2015. In June 2016, Visa acquired Visa Europe for a total sum of more than €18.5 billion and Visa had to take up loans to fulfill the deal. Although the purchase of Visa Europe resulted in Visa weakening its balance sheet, we think the deal makes strategic sense as it expanded Visa’s geographical reach and prominence. And as we mentioned earlier, we’re not troubled by Visa currently having more debt than cash and investments, since the company has been adept at producing free cash flow and the amount of net-debt is manageable.

- Visa’s diluted share count declined by 27.8% in total from FY2008 to FY2020 (we only started counting from FY2008 since Visa was listed on 19 March 2008) because of share buybacks. The share count also fell in nearly every year over the same period. From FY2016 to FY2020, Visa’s share count declined by a total of 7.9%. The decline in Visa’s diluted share count is positive for the company’s shareholders, since it boosts the company’s per-share earnings and free cash flow. For perspective, Visa’s free cash flow per share compounded at 20.2% per year from FY2016 to FY2020, which is higher than the annual growth rate of 17.7% over the same period for just free cash flow. We also mentioned earlier why we thought Visa’s share buybacks were smart moves by management.

Visa has been contending with COVID-19 for the second half of FY2020. The pandemic, as discussed earlier, has hurt the company’s business. This can be seen clearly in the table below, which shows the year-on-year changes in Visa’s revenue, net income, operating cash flow and free cash flow in each quarter of FY2020. But we’re looking at the long run here with Visa and we think COVID-19 is merely a short-term hiccup for the company.

Source: Visa quarterly earnings updates

6. A high likelihood of generating a strong and growing stream of free cash flow in the future

There are two reasons why we think Visa excels in this criterion.

First, the company has a long track record of producing strong free cash flow from its business. Moreover, its average free cash flow margin (free cash flow as a percentage of revenue) in the past five years from FY2014 to FY2019 was excellent at 48.1%. Even with COVID-19 hurting Visa’s business in the second half of FY2020, Visa’s free cash flow margin for the period was still at 48.0%.

Two, there’s still tremendous room to grow for Visa in the entire payments space. The company has a strong network (the number of countries it operates in; the sheer payment and transaction volumes it is processing; the billions in its credit cards that are circulating) as well as a capable and innovative management team that has integrity. These traits should lead to higher revenue for Visa over time. If the free cash flow margin stays fat – and we don’t see any reason why it shouldn’t – that will mean even more free cash flow for Visa in the future.

Valuation

We like to keep things simple in the valuation process. In Visa’s case, we think the price-to-earnings (P/E) ratio and price-to-free cash flow (P/FCF) ratio are suitable gauges for the company’s value. This is because the company has been adept at producing positive and growing profit as well as free cash flow for a long period of time.

We completed our purchases of Visa shares with Compounder Fund’s initial capital in late July 2020. Our average purchase price was US$198 per Visa share. At our average price and on the day we completed our purchases, the company’s shares had trailing P/E and P/FCF ratios of around 38 for both. These ratios are high relative to their histories. Here’s a chart showing Visa’s P/E and P/FCF ratios over the five years ended 18 December 2020:

But we’re happy to pay up, since Visa excels under our investment framework for Compounder Fund. We also want to point out two things. First, Visa’s current earnings and free cash flow per share numbers are somewhat depressed because of COVID-19. Second, Visa does not just have a large market opportunity – the chance that it can win in its market is also very high, in our view. Put another way, Visa scores well in both the magnitude of growth and the probability of growth. For companies like this, we’re more than willing to accept a premium valuation. But the current high P/E and P/FCF ratios mean that an investment in Visa carries valuation risk. This is something we are comfortable with.

For perspective, Visa carried P/E and P/FCF ratios of around 43 and 48, respectively, at the 18 December 2020 share price of US$211.

The risks involved

There are a few key risks that we see in Visa.

First is succession risk. Visa’s CEO Alfred Kelly is 62 this year, so he may not have too much gas left in the tank to continue serving as CEO. We think he has done a good job in leading Visa, so when he does step down in the future, we will be keeping an eye on the leadership transition.

Competition is the second risk we’re watching with Visa. We mentioned in our investment thesis for PayPal (a digital payments services provider) that the payments space is highly competitive. We also said:

“Then there are technology companies with fintech arms that focus on payments, such as China’s Tencent and Alibaba. In November 2019, Bloomberg reported that Tencent and Alibaba plan to open up their payment services (WeChat Pay and Alipay, respectively) to foreigners who visit China. Let’s not forget that there’s blockchain technology (the backbone of cryptocurrencies) jostling for room too. There’s no guarantee that PayPal will continue being victorious. But the payments market is so huge that we think there will be multiple winners – and our bet is that PayPal will be among them.”

Just like PayPal, there are no guarantees that Visa will continue winning. But we do think the odds are firmly in Visa’s favour. Visa’s technology platform and the services it provides to support digital transactions are still very relevant in our world today. The company has also taken the initiative to build strong relationships with fintech companies and other technology firms.

The third risk we have our eyes on is regulations. Payments is a highly regulated market, and Visa could fall prey to heavy-handed regulation. Lawmakers could impose hefty fines or tough limits on Visa’s business activities. In general, we expect Visa to be able to manage any new legal/regulatory cases if and when they come. But we’re paying attention to any changes in the regulatory landscape that could impair the health of Visa’s business permanently or for a prolonged period of time.

Fourth is the company’s high valuation. We’re comfortable paying up for Visa, but if there are any hiccups in the company’s growth – even if they are temporary in nature – there could be painful falls in the share price. This is a risk we’re comfortable taking as long-term investors.

Lastly, there is the risk of recessions. Visa did grow its net revenue during the Great Financial Crisis. But the current COVID-19 pandemic, and the ensuing global economic contraction has hurt the company’s business. We don’t know when a future global recession will happen again. But when it does, payment activity on Visa’s network could be lowered.

Summary and allocation commentary

To summarise, Visa ticks all our boxes:

- It has a large and growing addressable market (the US$203 trillion payments opportunity) that it has barely scratched.

- The company currently has more debt than investments, but the net-debt level is manageable and the company has a long history of producing strong free cash flow.

- Visa has leaders with a good track record of innovating, allocating capital intelligently, and executing, but that’s not all – the company’s leaders also have sensible compensation structures that align their interests with shareholders.

- Visa revenue streams are highly likely to be recurring in nature (each time we make a payment with a Visa service or product, the company earns a small fee).

- The company has a long history of producing solid growth in revenue, net income, and free cash flow.

- Visa has a high likelihood of continuing to be a machine at generating free cash flow in the future

The company does have a high valuation – both in absolute terms and in relation to history. But we have no qualms with accepting a premium valuation for a high-quality business. The other risks to our Visa investment includes succession risk; a tough competitive landscape; the potential for regulatory changes to harm the company’s business; and recessions.

After weighing the pros and cons, we initiated a 2.5% position – a medium-sized allocation – in Visa with Compounder Fund’s initial capital. We appreciate all the positives that we see in Visa. But our enthusiasm is slightly tempered by the fact that Visa’s revenue increased at only a mid-teens annual rate for the past 10-plus years, and so the company is unlikely to exhibit hypergrowth in the future. We prefer to have faster-growing companies to be larger positions in the portfolio.

And here’s an important disclaimer: None of the information or analysis presented is intended to form the basis for any offer or recommendation; they are merely our thoughts that we want to share. Of all the companies mentioned in this article, Compounder Fund also currently owns shares in Alphabet, Apple, Facebook, PayPal, Square, and Tencent. Holdings are subject to change at any time.