Compounder Fund: Shopify Investment Thesis - 17 Oct 2020

Data as of 15 October 2020

Shopify (NYSE: SHOP) is one of the 40 companies in Compounder Fund’s initial portfolio. This article describes our investment thesis for the company.

Company description

Shopify is an ecommerce enabler that is headquartered in Canada and listed in both Canada and the USA (Compounder Fund owns the US-listed shares). The company provides software and other services for entrepreneurs to start and manage their own retail businesses online. From the design of a website and securing financing, to payment-processing and the fulfilment of deliveries, Shopify does it all for the merchant. Merchants can use Shopify’s software to manage their businesses across all sales channels, including web and mobile storefronts, social media, online marketplaces, and even physical retail locations. Importantly, Shopify’s solutions can serve merchants of all sizes.

We want to clarify that Shopify is very different from another Compounder Fund holding, Amazon.com. Unlike Amazon.com, which offers an online marketplace as well as its own inventory as an online retailer, Shopify is not a marketplace for merchants to list their products or services nor does it retail products. Instead, Shopify provides the tools and solutions for merchants to build their own retail businesses online – merchants get to fully control their own brand and following.

Shopify’s business can be split into Subscription Solutions and Merchant Solutions. In 2019, these two segments accounted for 40.7% and 59.3%, respectively, of Shopify’s total revenue of US$1.58 billion in the year. Here’s what the two segments are about:

1. Subscription Solutions. Shopify earns revenue here primarily from merchants paying for subscriptions to use the company’s platform.

There are a few tiers to Shopify’s subscription service. At the low end are the Shopify Lite, Basic Shopify, Shopify, and Advanced Shopify tiers which have monthly fees of US$9, US$29, US$79, and US$299, respectively. There are differences between these four tiers in terms of their features and functionality (such as the number of staff accounts allowed and the level of access to advanced analytics and reports).

At the high end is Shopify Plus, which costs at least US$2,000 per month. Shopify Plus caters to established merchants that require more advanced features. An example of Shopify Plus’s advanced features include Shopify Flow, which can help merchants automate tasks such as tracking and rewarding top customers; inventory management; onboarding B2B wholesale customers, and more.

Shopify’s platform had more than one million merchants from over 175 countries at the end of 2019, but just 7,100 were subscribers to Shopify Plus. A large majority of the company’s subscribers are also on plans that cost less than US$50 per month. Nonetheless, most of the GMV (gross merchandise volume) facilitated by Shopify’s platform come from larger merchants who subscribe to the Advanced Shopify and Shopify Plus plans. Some of the merchants on Shopify Plus include Nestle and Heinz.

2. Merchant Solutions. This is where Shopify provides additional solutions that create value for merchants by saving them time and money. Below is a list of merchant solutions that Shopify provides:

-

- Shopify Payments is a fully integrated payment processing service for merchants to accept and process payment cards online and offline. Shopify charges payment processing fees for Shopify Payments and these fees account for most of the revenue from the Merchant Solutions segment. Merchants that are on Shopify’s platform but that have not signed up for Shopify Payments pay transaction fees that are based on a percentage of their GMV facilitated by Shopify.

- Shopify Shopping allows merchants that do their own fulfilment and shipping to work with a variety of shipping partners and track orders within the Shopify Platform.

- Shopify Fulfillment Network provides an outsourced fulfillment service for merchants. Shopify works with a partner network of fulfillment centres to ensure that merchants’ orders are delivered to buyers quickly and at low cost.

- Shopify Capital provides working capital to merchants that are on Shopify’s platform. Through Shopify Capital, Shopify either makes loans to merchants, or purchases receivables from merchants at a discount. To mitigate risk, Shopify has insured against merchant defaults for some of Shopify Capital’s portfolio.

- Shopify earns referral fees when it directs business to partners.

- Shopify POS is a mobile app for merchants to sell their products physically. Shopify also sells its self-designed POS (point of sales) hardware that is compatible with the Shopify POS app.

The one million-plus merchants on Shopify’s platform at the end of 2019 came from these geographies: USA (52%); UK (7%); Canada (6%); Australia (6%); and the rest of the world (29%). From a revenue perspective, Shopify’s geographical diversification is similar to where its merchants are located. In 2019, Shopify’s revenue came from the following countries/regions: USA (68.4%); UK (6.6%); Canada (6.1%); Australia (4.3%); and the rest of the world (14.6%).

Investment thesis

We have laid out our investment framework in Compounder Fund’s website. We will use the framework to describe our investment thesis for Shopify.

1. Revenues that are small in relation to a large and/or growing market, or revenues that are large in a fast-growing market

Using its own average revenue per user (ARPU) of US$1,653 in 2019, and a count of 47 million retail businesses globally based on 2017 data from AMI Partners, Shopify estimates that its total addressable market for small and medium businesses is US$78 billion. Shopify’s revenue in the 12 months ended 30 June 2020 was just US$2.08 billion, and as already mentioned, the company had over one million merchants on its platform at the end of 2019. So it’s clear to us that Shopify has barely scratched the surface of its market opportunity.

For another perspective, Shopify’s platform facilitated GMV (gross merchandise volume) of US$30.1 billion in the second quarter of 2020, up 119% from a year ago. This GMV translates to an annual run rate of US$120.4 billion, which seems huge. But it is still just a tiny fraction of the entire global ecommerce market, which is expected to be around US$3.914 trillion (or US$3,914 billion) this year, according to research outfit eMarketer. Statista reported that global ecommerce activity represented just 14.1% of total retail sales in the world in 2019. The current COVID-19 pandemic has impacted the way people in many countries live and shop. Ecommerce has recently benefited with governments around the world encouraging shelter-in-place measures. But even so, there’s still plenty of room for ecommerce to grow. For perspective, data from the Federal Reserve Bank of St Louis shows that the percentage of total retail sales in the USA that comes from ecommerce had increased from 11.3% in the fourth quarter of 2019 to 16.1% in the second quarter of 2020. As ecommerce blooms, Shopify, as an ecommerce enabler, is in a great spot to capitalise on the opportunities.

We also think it’s highly likely that Shopify will expand its addressable market over time. The company is very innovative and has a long history of coming up with new products and services regularly (more on this later); Shopify’s future ARPU could thus be significantly higher than what it is today.

2. A strong balance sheet with minimal or a reasonable amount of debt

Shopify has a rock solid balance sheet. The company exited the second quarter of 2020 with no debt and US$4.0 billion in cash and marketable securities.

For the sake of conservatism, we also note that Shopify had lease liabilities of US$153.1 million as of 30 June 2020. But this is only a tiny fraction of the cash and marketable securities that Shopify holds.

3. A management team with integrity, capability, and an innovative mindset

On integrity

Shopify is led by CEO Tobi Lütke, who co-founded the company in 2004. Lütke is only 39 this year, but he has been CEO of Shopify since 2008. We appreciate the fact that Lütke has more than a decade of leadership experience at the company despite his young age. The table below shows some of the other important leaders at Shopify. We like the fact that they are also relatively young and have each been at the company for a number of years.

Source: Shopify regulatory filing and website; Market Screener; Forbes

The compensation structure for Shopify’s leadership team demonstrates integrity, in our view. Here are a few points we want to highlight:

- In 2019, the base salaries for Lütke, Shapero, Finkelstein, and Forsyth were unchanged from 2018, even though Shopify’s revenue surged by 47% during the year.

- Shopify does not provide any form of short-term incentives to its key leaders.

- In 2019, Lütke, Shapero, Finkelstein, and Forsyth’s total compensation ranged from US$2.81 million to US$10.62 million each. These look like reasonable sums to us given the scale of Shopify’s business.

- The total compensation for each of the quartet in 2019 can be split into two components, namely, the base salary and equity awards. For Lütke, Shapero, Finkelstein, and Forsyth, the equity awards made up 88% to 94% of each of their total compensation in 2019. The equity awards consist of restricted stock units and stock options that vest over three years. This means that the lion’s share of the compensation for each Shopify key leader is tied to multi-year changes in the company’s stock price, which in turn, depends on the company’s business performance. The interests of Shopify’s management team and its shareholders are thus well aligned, in our view.

And speaking of alignment of interest, Lütke controlled 8.31 million Shopify shares as of 9 April 2020. Based on Shopify’s share price of US$1,082 on 15 October 2020, Lütke’s stake is worth a staggering US$9.0 billion. So there’s significant skin in the game for Shopify’s CEO and co-founder.

We want to highlight that 97% of Lütke’s Shopify shares are of the Class B variety. Shopify has two share classes: (1) Class B, which are not traded and hold 10 voting rights per share; and (2) Class A, which are publicly traded and hold just 1 vote per share. As a result, Lütke controlled 34.95% of Shopify’s voting power (as of 9 April 2020) despite holding only 7.0% of Shopify’s total shares. A manager having significant control over the company can potentially be bad for shareholders. This concentration of Shopify’s voting power in the hands of Lütke means that we need to be comfortable with him at the company’s helm. We are.

On capability and ability to innovate

The bottom line here is that we think Tobi Lütke is an exceptional entrepreneur and businessman, and we’re glad to have Compounder Fund ‘partner’ alongside him in Shopify. There are a few things we want to discuss.

The first concerns Shopify’s founding story. Here’s an account from Lütke that he shared in the masterclass of an investors’ letter he wrote for Shopify’s IPO prospectus (Shopify listed in Canada and the US in May 2015):

“The first Shopify store was our own. In 2004, we took something we loved, snowboarding, and built a business around it. The idea was to set up an online store and create a snowboarding empire. But there was a problem: the software landscape we encountered seemed to work against our ambitions at every step. Back then, online store software was built for existing big businesses that were transitioning online. It was incredibly expensive, unnecessarily complex, and infuriatingly inflexible.

Existing software was not designed with the new entrepreneur in mind, so we rejected the existing models and created our own. Our custom software met our needs so well that we decided to take everything we learned and shift our business away from snowboards and towards fixing the glaring hole in the ecommerce market. We knew that many future businesses would be created online first, and software needed to support the first steps of entrepreneurship, not just the established big guys. We set out to create the software that we wished would have existed, and we launched it in 2006 under the name Shopify.”

We are attracted to companies that are created because their founders saw a big problem that needed fixing – to us, it’s a sign of the entrepreneurial drive and innovative mindset of the companies’ leaders. Lütke saw a huge problem that needed to be solved, and boy has he succeeded, as you’ll see later!

The second involves the incredible long-term vision and mindset that Lütke has. In fact, he’s more than willing to sacrifice short-term gains if it means that Shopify would benefit over the long run. This mindset is not easy to find among business people, based on our experience. In the aforementioned letter in Shopify’s IPO prospectus, Lütke wrote the following passages on this topic (emphases are ours):

“Over [US]$8 billion of GMV [gross merchandise volume] has already been transacted through our platform, with the most recent quarter coming in at over [US]$1 billion. We’ve proven that there’s incredible potential in early-stage entrepreneurs when they are empowered with great technology. Focusing on inspiring entrepreneurship and helping people iterate their ideas, launch new stores and scale their businesses creates a sense of solidarity: we did it together. We believe that by giving merchants an affordable, easy to use solution that helps them sell and run their business, Shopify will share in their success as they grow. We’ve shown that it was possible to build a single platform that works from the very beginning—an entrepreneur with an idea—to a business with millions of orders. And while many of our larger merchants switched to Shopify based on the quality of our platform, a large number of our merchants are “homegrown” and started their businesses with us. I’m incredibly proud of this.

Over the years we’ve also helped foster a large ecosystem that has grown up around Shopify. App developers, design agencies, and theme designers have built businesses of their own by creating value for merchants on the Shopify platform. Instead of stifling this enthusiastic pool of talent and carving out the profits for ourselves, we’ve made a point of supporting our partners and aligning their interests with our own. In order to build long-term value, we decided to forgo short-term revenue opportunities and nurture the people who were putting their trust in Shopify. As a result, today there are thousands of partners that have built businesses around Shopify by creating custom apps, custom themes, or any number of other services for Shopify merchants.

This is a prime example of how we approach value and something that potential investors must understand: we do not chase revenue as the primary driver of our business. Shopify has been about empowering merchants since it was founded, and we have always prioritized long-term value over short-term revenue opportunities. We don’t see this changing…

… I want Shopify to be a company that sees the next century. To get us there we not only have to correctly predict future commerce trends and technology, but be the ones that push the entire industry forward. Shopify was initially built in a world where merchants were simply looking for a homepage for their business. By accurately predicting how the commerce world would be changing, and building what our merchants would need next, we taught them to expect so much more from their software.”

We believe Lütke really means what he said in the passages just above. This is because the GMV that Shopify has facilitated has increased tremendously over the years – and this is the third thing about Lütke that we want to discuss. The table below shows the growth in Shopify’s GMV, number of merchants, and revenue since 2012. Shopify’s merchant count grew admirably from 2012 to 2019, but the company’s GMV and revenue both increased at even faster rates. To us, these are clear signs of Shopify’s excellent ability to facilitate ecommerce activity for its merchants and generate higher revenue per user over time. It is also strong proof that Lütke is walking the talk when it comes to his desire to empower merchants.

Source: Shopify IPO prospectus, annual reports, and earnings update

Fourth, Shopify has a strong history of innovation to help merchants sell better. Here’s a sample timeline starting with 2014:

- February 2014 – Shopify introduces Shopify Plus

- March 2015 – Shopify releases features that makes it easier for merchants to manage and sell their products across all sales channels

- September 2015 – Shopify enables merchants to sell products on Facebook and Twitter; Shopify launches Shopify Shipping; Shopify provides integration with Amazon.com offerings (Login and Pay with Amazon, Fulfillment by Amazon, and Selling on Amazon) after being named as the preferred migration provider upon the closure of Amazon.com’s Amazon Webstore service.

- 2016 – Shopify launches Shopify Capital; Shopify’s merchants become one of the first to be able to accept Apple Pay and Google Pay for web orders on mobile; Shopify becomes the first ecommerce platform to integrate with Facebook’s Messenger service; Shopify enables merchants to manage their product catalogs for Amazon.com and other sales channels in one place.

- First quarter of 2017 – Shopify introduces wholesale features for Shopify Plus to enable its users to efficiently manage B2B wholesale activities.

- Second quarter of 2017 – Shopify improves Shopify Payments by introducing Shopify Pay, a feature to streamline the mobile checkout process

- Third quarter of 2017 – Shopify makes selling on Instagram available on a limited basis

- First quarter of 2018 – Shopify provides wider availability for selling on Instagram

- Third quarter of 2018 – Shopify introduces the Locations feature that enables merchants to manage inventory across multiple locations; Shopify releases its new App Store that makes it easier and faster for merchants to find the right apps to grow their businesses; Shopify launches Shopify AR to allow small businesses to use augmented reality technology to sell products.

- Fourth quarter of 2018 – Shopify launches a fraud protection feature (Fraud Protect) on Shopify Payments

- First quarter of 2019 – Shopify introduces a feature within Shopify Plus to allow merchants to sell in multiple currencies and get paid in their local currency; Shopify launches Shopify Studios, a full-service TV and film content production house that will create inspiring and educational video content on entrepreneurship

- Second quarter of 2019 – Shopify introduces a language-translation feature for merchants to reach international shoppers; Shopify launches Shopify Fulfillment Network, which provides “merchants with a network of distributed fulfillment centers that utilizes machine learning to ensure timely deliveries and lower shipping costs” (Shopify acquired warehouse automation and fulfillment technologies provider 6 River Systems for US$394 million in the fourth quarter of 2019 to accelerate the growth of Shopify Fulfillment Network)

- Third quarter of 2019 – Shopify launches a native chat function to allow merchants to have real-time conversations with customers

- First quarter of 2020 – Shopify opens a R&D centre in Canada to trial new fulfillment and robotics technologies

- Second quarter of 2020 – Shopify partners with fintech company Affirm to launch a “buy now, pay later” product called Shop Pay Installments that could boost merchant sales through larger cart-sizes and higher customer-conversion; Shopify announces Shopify Balance to improve the cash flow of merchants by giving merchants money management tools and faster access to their cash.

Fifth, Shopify’s actions in the midst of the COVID-19 pandemic in 2020 are both admirable and a sign of a company that’s able to execute really well. We’ll let you read straight from Shopify’s earnings update for the second quarter of 2020:

“In light of the ongoing COVID-19 pandemic, we have continued to focus on the health and well-being of our employees, partners, service providers, and communities. We have also accelerated products that we believe will best serve our merchants as they deal with the challenges of COVID-19.

In the first quarter [of 2020], we launched several initiatives to support our merchants in this difficult time, including offering an extended 90-day free trial for all new standard plan sign-ups from March 21, 2020 through May 31, 2020, availability of gift card capabilities to merchants on all plans, local in-store or curbside pick up and delivery for POS [point-of-sale] merchants, and an increased funding commitment of [US]$200 million above the March 31, 2020 level for the remainder of 2020 to increase funding for Shopify Capital in the United States and expand Shopify Capital to the United Kingdom and Canada, where we are working with partners who share in the revenue and risk.

In the second quarter, we continued to focus on supporting merchants with additional products and features, including enhanced curbside pickup and local delivery capabilities, and the Express theme, as well as tipping capabilities, aimed at helping local restaurants and coffee shops and other merchants looking to connect with customers online…

… Demand for Shopify Capital was strong in Q2, with merchants receiving [US]$153 million in funding across the U.S., the U.K. and Canada. This represents a 65% increase in funding over the second quarter of 2019. Access to capital is even tougher as a result of COVID-19, which makes it even more important to continue lowering this barrier by making it quick and easy to access capital, so merchants can focus on growing their business.”

Sixth, we think Lütke has built a great culture at Shopify. Glassdoor is a platform that allows employees to rate their companies anonymously. Currently, 76% of Shopify-raters on Glassdoor will recommend the company to a friend. Meanwhile, Lütke has a 90% approval rating as CEO, far higher than the average Glassdoor CEO rating of 69%. An interesting aspect of Shopify’s culture that we’re watching is Lütke’s recent decision to make remote-work permanent at Shopify. Here’s Lütke sharing his thought process on Twitter (emphases are ours):

“As of today [21 May 2020], Shopify is a digital by default company. We will keep our offices closed until 2021 so that we can rework them for this new reality. And after that, most will permanently work remotely. Office centricity is over.

Until recently, work happened in the office. We’ve always had some people remote, but they used the internet as a bridge to the office. This will reverse now. The future of the office is to act as an on-ramp to the same digital workplace that you can access from your #WFH setup.

This means that the work experience should be the same for everyone who works together at Shopify no matter where they are working from. Everyone will be in their own tile during meetings and we will use the best digital communications tools to work together.

This is actually true for our merchants in many cases as well. Many DTC [direct-to-consumer] companies are digital by default. It will be good for us to have more empathy in building Shopify in this way and preparing it for the new requirements.

Shopify has had many big transitions. The first was when Snowdevil became Shopify. Becoming a venture-backed company in 2010 was another. In 2015, on this very day, we went public. In 2017, we reorganized the entire company into multiple product lines. And here we go again.

A common misconception about company culture is that if you have a good one, you have to hold on to it. I believe this to be wrong. If you want to have a great culture, the trick is to evolve it forward with your environment. Take the best things with you from version to version.”

After understanding Lütke’s thinking behind Shopify’s stance on remote-working, we think he has made a good decision to have Shopify employees work-from-home permanently. We also want to say that we really like Lütke’s view that a company’s culture is one of constant change for the better. We believe that the culture Lütke has helped shape at Shopify is one of the company’s key strengths.

4. Revenue streams that are recurring in nature, either through contracts or customer-behaviour

We think Shopify excels in this criteria. As mentioned earlier, Shopify has two business segments, namely, Subscription Solutions and Merchant Solutions. We believe both are highly recurring in nature. The Subscription Solutions segment has a business model based on automatic subscription renewals unless a merchant cancels. Meanwhile, the Merchant Solutions segment earns revenue based on the level of commerce-activity of Shopify’s merchants (measured by the GMV facilitated by Shopify’s platform), and these commerce activities happen on a regular basis.

We believe that ecommerce will continue to grow and merchants can derive a lot of value from using Shopify’s platform. Shopify helps merchants host websites and provides back-end commerce support, payment and fulfillment solutions, and more. This makes Shopify a sticky platform for successful merchants (leading to sticky Subscription Solutions revenue) and it also means that Shopify is likely to enjoy higher GMV over time (leading to recurring Merchant Solutions revenue).

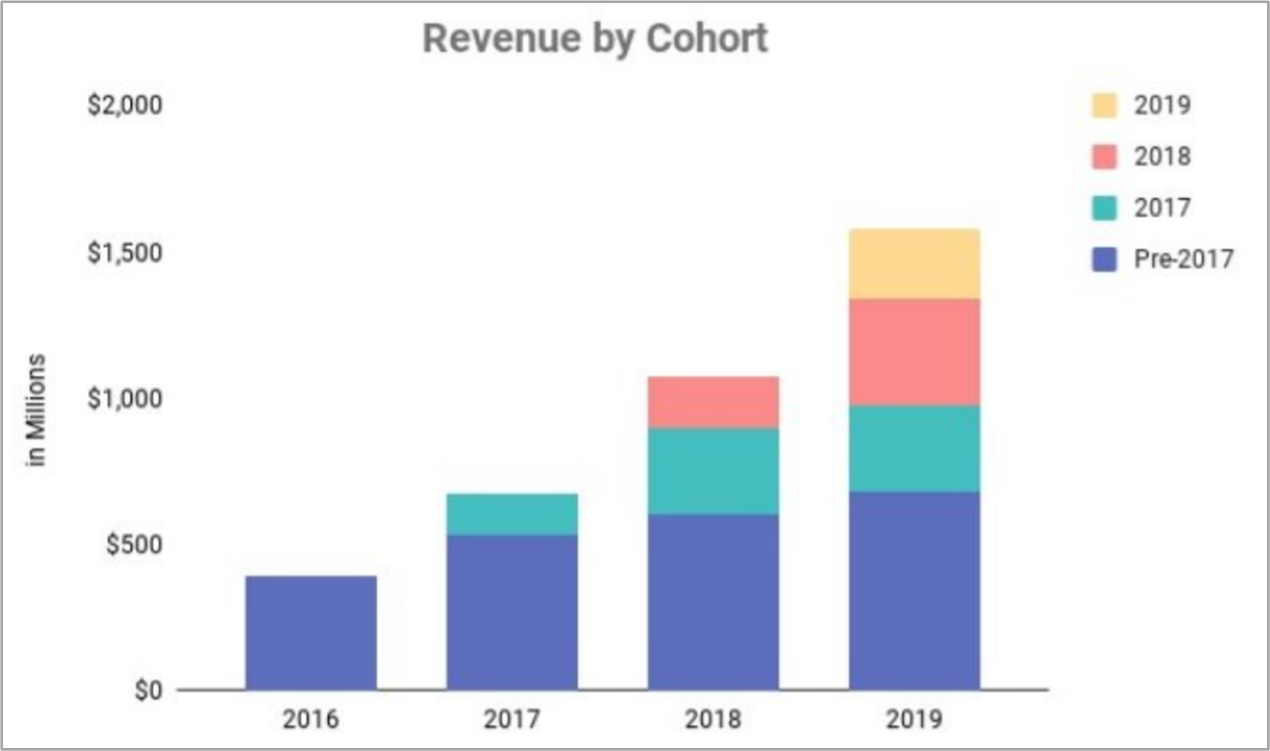

Lending weight to our view on the recurring nature of Shopify’s revenue streams is the fact that Shopify’s customers tend to generate more revenue for Shopify over time. The chart below shows Shopify’s annual revenue by merchant-cohort over the past few years. Each coloured bar represents a cohort of merchants who started using Shopify’s platform at different years. The height of each coloured-bar lengthens over time, illustrating that Shopify earns higher revenues from each merchant-cohort as the years progress. Importantly, the revenue numbers shown in the chart take into account merchant-churn. For example, revenue from the pre-2017 cohort (the blue bars) grew in 2018 over 2017, as lost revenue from merchants who left Shopify were more than offset by higher revenue from existing merchants as they increased their GMV and adopted additional Shopify solutions.

Source: Shopify annual report

Speaking of churn, we want to highlight that we’re not worried about possible high merchant-churn at Shopify. In fact, higher merchant-churn could be a good thing for the company. Why? Ben Thompson explained in a July 2019 article for his excellent business-strategy newsletter, Stratechery (emphasis is ours):

“At first glance, Shopify isn’t an Amazon competitor at all: after all, there is nothing to buy on Shopify.com. And yet, there were 218 million people that bought products from Shopify without even knowing the company existed.

The difference is that Shopify is a platform: instead of interfacing with customers directly, 820,000 3rd-party merchants sit on top of Shopify and are responsible for acquiring all of those customers on their own.

This means they have to stand out not in a search result on Amazon.com, or simply offer the lowest price, but rather earn customers’ attention through differentiated product, social media advertising, etc. Many, to be sure, will fail at this: Shopify does not break out merchant churn specifically, but it is almost certainly extremely high.

That, though, is the point.

Unlike Walmart, currently weighing whether to spend additional billions after the billions it has already spent trying to attack Amazon head-on, with a binary outcome of success or failure, Shopify is massively diversified. That is the beauty of being a platform: you succeed (or fail) in the aggregate.

To that end, I would argue that for Shopify a high churn rate is just as much a positive signal as it is a negative one: the easier it is to start an e-commerce business on the platform, the more failures there will be. And, at the same time, the greater likelihood there will be of capturing and supporting successes. [Shopify can serve the smallest to the largest of merchants, so it is able to grow alongside its successful merchants as they scale.]”

5. A proven ability to grow

The table below shows Shopify’s key financials since 2012 (they are the earliest data we can find, since the company listed only in May 2015).

Source: Shopify annual reports

A few important things to note about Shopify’s historical financials:

- Shopify’s revenue has compounded impressively at 82.2% from 2012 to 2019. Growth has slowed in recent years (it was 59.4% and 47.0% in 2018 and 2019, respectively), but is still really strong.

- Shopify is still loss-making, but it has been consistently generating positive operating cash flow since 2015. In 2019, Shopify’s free cash flow turned positive for the first time. The free cash flow margin is extremely thin at just 0.5%, but we believe the margin will improve over time as Shopify scales its business.

- Shopify’s balance sheet has been rock-solid for the entire time frame we’re looking at with debt being zero in each year. The company’s cash also increased significantly. But we want to point out that Shopify’s cash has grown over time because the company has been issuing new shares regularly in secondary offerings to raise capital. For instance, Shopify raised US$647 million in February 2018 at US$137 per share, US$395 million in December 2018 at US$154 per share, and US$688 million in September 2019 at US$317.50 per share. More recently, Shopify raised US$1.46 billion in May this year at US$700 per share and then nearly US$1.14 billion in September at US$900 per share.

- At first glance, Shopify’s diluted share count appeared to increase significantly by 36% from 2015 to 2016 (we only started counting from 2015 since Shopify was listed in the month of May during the year). But the number we’re using is the weighted average diluted share count. Right after Shopify got listed, it had a share count of around 76 million. From 2016 to 2019, Shopify’s diluted share count increased by 10.4% per year. It’s not a surprise to learn that Shopify has exhibited shareholder-dilution given the aforementioned secondary offerings (stock-based compensation also played a role in the dilution). The share count growth of 10.4% annually from 2016 to 2019 is much lower than the company’s revenue growth rate so that’s good. But it is still somewhat higher than what we typically like to see and we’ll be keeping an eye on future changes in Shopify’s diluted share count. Nonetheless, we think it’s still sensible for Shopify to take advantage of its rising share price to issue new shares and raise capital to shore up its balance sheet and to provide dry powder for growth investments.

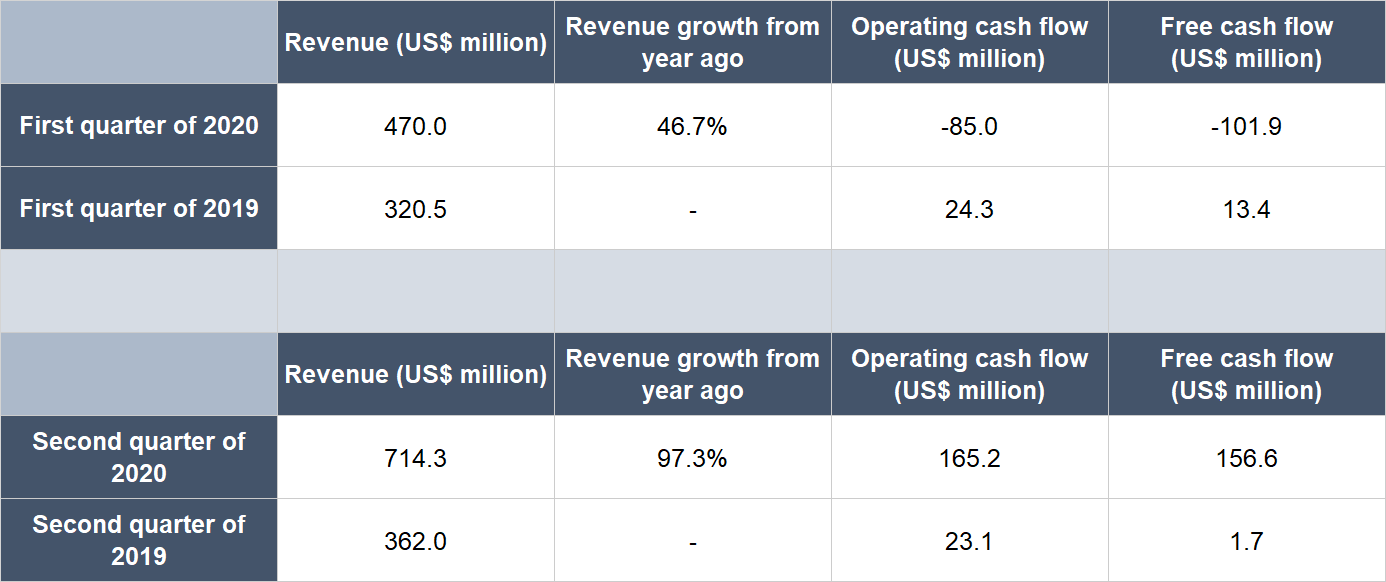

Shelter-in-place measures that governments around the world have enacted to fight COVID-19 have accelerated the adoption of ecommerce. This has helped Shopify to experience strong growth in the first half of 2020 as the table below shows (note the significant acceleration in revenue growth from the first quarter to the second quarter). In its outlook statement given in the earnings update for 2020’s second quarter, Shopify said: “The COVID-19 pandemic has accelerated the growth of ecommerce, shifting a larger share of retail spending to online commerce, a trend we believe will persist.” We agree. (In the first half of 2020, Shopify’s diluted share count increased by 9.4% from a year ago; this looks good, since it is much lower than the company’s revenue growth of 73.5%.)

Source: Shopify earnings updates

6. A high likelihood of generating a strong and growing stream of free cash flow in the future

Shopify’s growth is something we admire. But the real question is whether the company can consistently generate positive free cash flow in the future. The company has begun to generate free cash flow – it did so in 2019 and in the first half of 2020. Shopify’s free cash flow margin (free cash flow as a percentage of revenue) is still razor-thin, but it improved from 0.5% in 2019 to 4.6% in the first half of 2020.

We think Shopify has plenty of room to grow its free cash flow margin in the future. In the first half of 2020, Shopify’s gross margin for its Subscription Solutions and Merchant Solutions segments were both high at 78.6% and 41.2%, respectively. At the same time, Shopify is still spending a tonne of cash on sales & marketing and R&D. For perspective, Shopify’s sales & marketing expense was 25.3% of total revenue in the same period while R&D expense was 20.8%. As Shopify is still in a high-growth phase, we believe this spending is justified. But as the company grows, we believe that these expenses will start to decline as a percentage of revenue, leading to higher free cash flow margins.

Valuation

We completed our purchases of Shopify shares with Compounder Fund’s initial capital in late July 2020. Our average purchase price was US$1,025 per Shopify share. At our average price and on the day we completed our purchases, Shopify shares had a trailing price-to-sales (P/S) ratio of 60. We like to keep things simple in the valuation process. In Shopify’s case, we think the P/S ratio is an appropriate metric to value the company, since the company does not have a long history yet of generating free cash flow.

There’s no need to consult any historical valuation chart to know that the P/S ratio of 60 is really high – and that’s a risk. For perspective, if we assume that Shopify has a 20% free cash flow margin today, then the company would have a price-to-free cash flow ratio of 300 (60 divided by 20%). But we think Shopify is an exceptional company that has years of rapid growth ahead of it. This makes us comfortable with paying up for Shopify’s shares.

For perspective, Shopify carried a P/S ratio of 63 at the 15 October 2020 share price of US$1,082.

The risks involved

We’ve identified a few important risks with Shopify.

1. The first to look out for is COVID-19. Shopify’s business has so far performed admirably in the face of the pandemic. But the company also warned in its earnings update for the second quarter of 2020 that “going forward, we may experience a decrease in GMV as a result of lower consumer spending, but also expect that any decrease would be at least partially offset by more traditional retail businesses expanding or migrating their operations online with our platform and services.” The good thing for now is that entrepreneurship is on the rise, in the USA at least. Yahoo! Finance reported in late-September 2020 that new business applications with a high chance of surviving “reached their highest quarterly level on record for the third quarter, after seeing virus-related declines in March and April.” The chart below, from the same Yahoo! Finance reporting, illustrates the massive surge in business creation in the USA seen in 2020 compared to the past. As an ecommerce enabler, Shopify is well positioned to benefit.

2. We are also mindful of the risk from competition. Shopify competes with other ecommerce enablers that provide similar services, such as Adobe’s Magento, Wix.com, and BigCommerce. Then there are also the ecommerce players themselves, such as the juggernaut that is Amazon. Shopify has been facing intense competition for a long time, but that has not stopped the company from growing. We also believe that Shopify has the most complete solution for merchants who want their own online storefront and an end-to-end service from building the site to last-mile delivery. Nonetheless, we are keeping an eye on Shopify’s competitive landscape.

3. We think Tobi Lütke’s leadership has been a critical reason behind Shopify’s success over the years, so there’s key-man risk. If Lütke steps down from his leadership role at Shopify for whatever reason, we will be watching the transition closely. The good thing is that Lütke is only 39 this year, as already mentioned, so he likely still has plenty of gas left in the tank.

4. Dilution is another risk we’re watching. We discussed Shopify’s history of shareholder dilution – a result of stock-based compensation and secondary offerings – earlier in this article. We think Shopify has so far been opportunistic in the way it has issued new shares to raise capital, and the company’s business growth has significantly outpaced the increase in its share count. But we’re still mindful of dilution and we will be keeping a close eye on Shopify’s future capital-raising activities and capital allocation decisions.

5. Lastly, there’s valuation risk. We think Shopify’s business is likely to grow at a rapid clip for many years and so it deserves its premium valuation. But if there are any hiccups in Shopify’s business – even if they are temporary – there could be a painful fall in the share price. This is a risk we’re comfortable taking as long-term investors.

Summary and allocation commentary

In our view, Tobi Lütke is an incredible and innovative business leader. Shopify has Lütke as CEO, and that in itself is an incredible competitive advantage for the company – no one else has Tobi Lütke. Besides excelling in the management-criteria within Compounder Fund’s investment framework, Shopify also shines in all the other areas:

- The company is operating in the large and growing market of ecommerce and could potentially expand its market opportunity in the future because of its keen ability to innovate

- Shopify’s balance sheet is pristine, with zero debt.

- The nature of Shopify’s business (with subscription as well as transaction-based models) means there are high levels of recurring revenues.

- The company has an impressive long-term track record of growth.

- Shopify has so far only been generating meagre cash flow, but we have strong reason to believe its free cash flow margins could expand significantly in the future.

The company’s valuation – based on the P/S ratio – is high, and that’s a risk. Other important risks we’re watching with Shopify include a slowdown in consumer spending because of COVID-19; intense competition; key-man risk; and the risk of shareholder dilution. But Shopify is a very high quality business, in our view, which means the high valuation currently could be short-term expensive but long-term cheap. Moreover, we see Shopify as a company with (1) a huge addressable market and (2) a high probability of being able to grow at a rapid clip for many years in the future. As a result, we’re happy to have Shopify be one of the holdings in Compounder Fund’s portfolio.

The question is how big should Shopify be in Compounder Fund’s portfolio? After weighing the pros and cons (especially the risks related to Shopify’s high valuation), we decided to initiate a 2.5% position in Shopify – a medium-sized allocation – with Compounder Fund’s initial capital.

And here’s an important disclaimer: None of the information or analysis presented is intended to form the basis for any offer or recommendation; they are merely our thoughts that we want to share. Of all the companies mentioned in this article, Compounder Fund also currently owns shares in Amazon.com, Facebook, Alphabet (the parent of Google), Adobe, and Wix.com. Holdings are subject to change at any time.