Compounder Fund: Portfolio Update (July 2024) - 09 Jul 2024

Jeremy and I intend to share frequent but non-scheduled updates on how Compounder Fund’s portfolio looks like. The last time we shared an update on this was for Compounder Fund’s portfolio as of 07 April 2024. In it, I shared all 46 holdings that were in the fund’s portfolio at the time. In late June, we made some changes to the portfolio, the most prominent of which were the complete sales of the DocuSign and Etsy stakes, small trims to the Chipotle Mexican Grill and Costco positions, and a new investment in Nu Holdings.

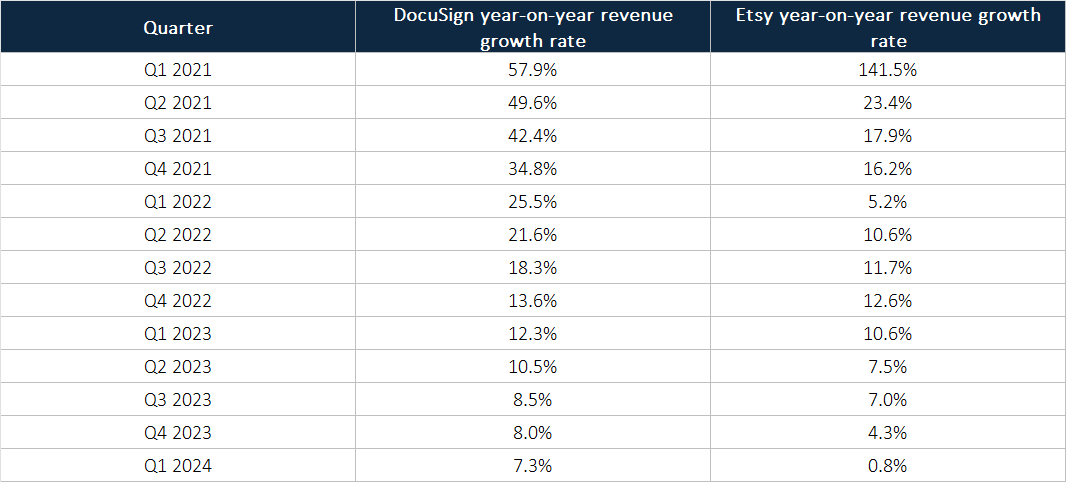

We sold DocuSign and Etsy primarily because their revenue growth rates plummeted in 2023 and in the first quarter of 2024 – see Table 1 below – and we do not have confidence in both of their businesses returning to a high-growth state.

Table 1; Source: DocuSign and Etsy earnings releases

In the case of e-signature specialist DocuSign, Allan Thygessen assumed the chief executive role in October 2022 and spoke of his desire to run a company with double-digit revenue growth rates during his first earnings conference call as CEO. But DocuSign’s revenue growth has declined steadily since, as shown in Table 4. Moreover, guidance for DocuSign’s revenue growth for 2024 was just 6%. Thygessen’s new product strategy for the company, a platform named Intelligent Agreement Management, or IAM, was announced this April. It is a one-stop platform for users to create, manage, and learn from their agreements. But in the first quarter of 2019, DocuSign launched Agreement Cloud, a platform similar to IAM, that was billed as a solution for “how organisations prepare, sign, act on and manage their agreements.” Agreement Cloud appears to have failed to achieve major commercial success and the last earnings conference call in which management voluntarily commented on the platform was for the first quarter of 2022. We’ll be sharing more of our thoughts on DocuSign in a sell-thesis that will be published on Compounder Fund’s website in the coming months.

As for Etsy, we now think we were wrong about the characteristics of its namesake craft items ecommerce marketplace (the italicised “Etsy” would refer to the company’s Etsy marketplace, while the non-italicised “Etsy” would refer to the company). When we first invested, we considered “the Etsy marketplace to be well-differentiated from other ecommerce marketplaces due to its unique products.” But according to an early-June 2024 article from The Information:

“A September 2023 analysis by MoffettNathanson found that nearly 30% of Temu’s top-selling women’s clothing items were also listed for sale on Etsy, and 19 of Temu’s top 25 jewelry items also appeared on Etsy, often listed at much higher prices.”

This is not what a well-differentiated marketplace looks like to us. We were also alarmed by management’s comments in Etsy’s 2024 first-quarter earnings conference call regarding the company’s Chinese competitors (Temu is an online marketplace of Chinese e-commerce company PDD Holdings):

“I think what we’ve been saying all along is that we think that the Chinese competitors are more symptoms than a root cause. I think what we’re observing again and again, both at Etsy and what we read in the commentary from so many others in our space, is that consumers feel really pressured in spite of what we’re seeing about a generally healthy economy. Consumers feel really pressured and so they are seeking value in deep discounts and deep promotions. And so yes, the Chinese competitors are offering that, but Amazon and Walmart are, too.”

The above excerpt suggests that Etsy’s management sees a weak US economy and lower prices from Chinese competitors as the main challenges faced by the company. We think management is not seeing the key issue, which is the lack of differentiation with the Etsy marketplace. Similar to DocuSign, we will let you know once we have published our sell-thesis for Etsy in the coming months.

Regarding the trimming of Chipotle Mexican Grill and Costco, they were done because of valuation reasons and also because we wanted to free up some capital to invest in Nu Holdings. I mentioned in April 2024 update that we’re “still really positive on the future growth potential of Chipotle and Costco’s businesses” but that they “ended March 2024 with high price-to-earnings ratios of 66 and 48, and high price-to-free cash flow ratios of 66 and 53, respectively.” Both conditions still hold true. Chipotle posted 14.1% year-on-year revenue growth in the first quarter of 2024, same-store sales growth of 7.0%, an impressive restaurant level operating margin of 27.5%, and a 23.9% increase in diluted earnings per share. As for Costco, same-store sales growth of 6.6% for the same quarter drove a 9.1% revenue increase, leading to a 29.0% jump in diluted earnings per share (or growth of 10.2%, excluding one-off charges in the year-ago quarter). At the end of June 2024, Chipotle’s price-to-earnings and price-to-free cash flow ratios were 67 and 65, respectively, while Costco’s were 52 and 51. Taking a small number of chips off the table still seems like a sensible move to us.

Coming to the latest addition to Compounder Fund’s portfolio, Nu Holdings, you can expect to see our detailed investment thesis in the weeks ahead. But meanwhile, here are some highlights on the company, which held its initial public offering in December 2021:

- Nu Holdings is the holding company of Nubank, which is today one of the largest digital banks in the world. Nubank is currently active in three Latin American markets – Brazil, Colombia, and Mexico – with Brazil being its most important geography by far.

- Nu Holdings’ first product, the Nu Credit Card, a purple Mastercard-branded credit card, was launched in 2014 in Brazil. In just roughly a decade, the digital bank has grown its total customer base impressively from nothing to more than 100 million as of May 2024; of the 100 million, around 83% are monthly active customers. In the first quarter of 2024, Nu Holdings had 91.8 million customers in Brazil, which was 54% of the country’s adult population. The digital bank is well-loved by its customers, seeing as how it has (1) acquired a “significant part” of its customers since inception through word-of-mouth or direct unpaid referrals from existing customers, and (2) a net promoter score that management believes is much higher than other financial institutions in its geographies.

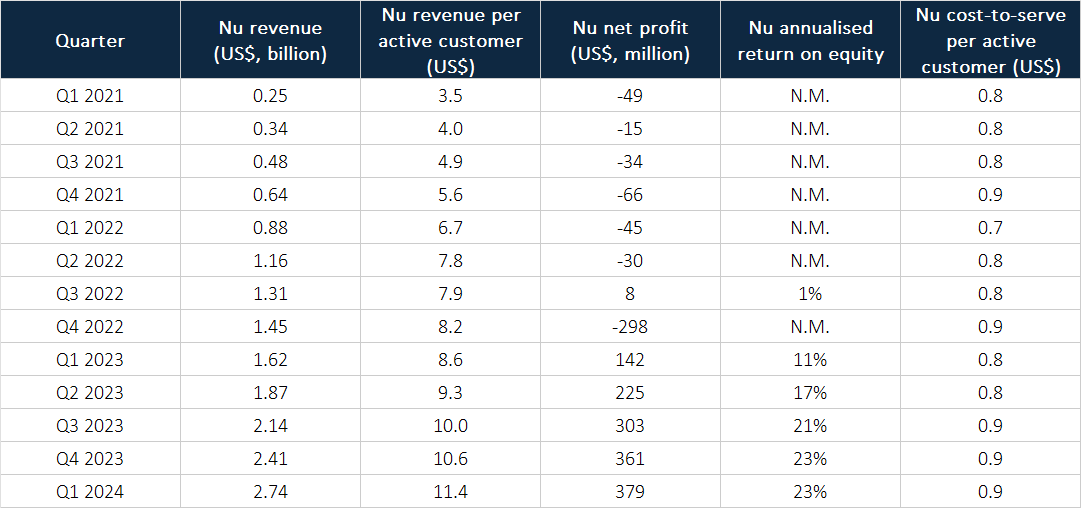

- Nu Holdings has expanded its product-suite significantly over time, and now has solutions to cover what it calls the “Five Financial Seasons” of its customers: Spending, saving, investing, borrowing, and protection (insurance). This has played a role in Nu Holdings’ outstanding annualised growth of 124% in revenue and 48% in average revenue per active customer from the first quarter of 2021 to the first quarter of 2024.

- The digital bank has started to generate positive IFRS (International Financial Reporting Standards) net profit in the past few quarters and produced a strong annualised return on equity of 23% in the first quarter of 2024. But even better economics are likely to be on the way for a few reasons:

- Nu Holdings held excess capital of US$2.4 billion at the holding level in the first quarter of 2024 when its shareholders’ equity was US$6.8 billion.

- The digital bank’s operations in Mexico and Colombia are still loss-making, and the return on equity in the Brazil business alone was more than 40% in the first quarter of 2024.

- In a May 2024 interview with Bloomberg, Nu Holdings’ co-founder and CEO, David Velez, said that around 50% of the company’s employees “today are working on products that are generating zero revenue.” If any of these products succeed in becoming profitable, it will improve Nu Holdings’ overall profitability.

- Nu Holdings has maintained a low cost-to-serve per active customer while growing its revenue per active customer significantly over time.

- Mature customer cohorts have an average revenue per active customer of around US$27 per month, nearly twice that of the company-wide average revenue per active customer of US$11.40 per month.

- Nu Holdings had a low loan-to-deposit ratio of just 40% in the first quarter of 2024. Nu Holdings’ excess deposits are invested in public bonds, which have much lower yields than its credit products. As management puts more of the deposits to work in credit products, the digital bank’s profitability should trend upwards.

- Nu Holdings’ retail financial services revenue opportunity in Brazil, Mexico, and Columbia was US$200 billion in 2023, with Brazil alone accounting for US$146 billion. In comparison, Nu Holdings’ trailing revenue was US$9.2 billion. For another perspective, although Nu Holdings ended the first quarter of 2024 with nearly 100 million customers, it accounted for less than 5% of the Latin American continent’s financial services revenue.

- Table 2 below shows Nu Holdings’ quarterly revenue, revenue per active customer, net profit, annualised return on equity, and cost-to-serve since the first quarter of 2021.

Table 2; Source: Nu Holdings earnings presentations

There’s one other thing we want to share about Nu Holdings in this letter: David Velez strikes us as a leader who believes that proactively delivering as much value as possible to customers, even if doing so would be a short-term negative for Nu Holdings, is the right thing to do for building the company’s long-term value. We agree with his belief. During a recent internal interview, Velez shared the following story (emphases are mine):

“A couple of years ago we had an analyst that came and said, “Hey, we’re suddenly making more money per customer.” Our cohorts were tilting up very fast. And we went in and took a look and see what was happening. And it turns out that there had been a bug in our system and we had stopped sending a reminder email to our customers. Since the beginning – being we care about the values – we remind the consumer almost every day to pay on time. We don’t want them to revolve unnecessarily. So we remind the consumers and only the ones that really need to revolve will end up revolving and pay a late fee. So for us, having that consumer value was very easy to know what to do. Not only we had to go back and put that email immediately, but also go beyond and send an email to all of our customers and apologize for having stopped reminding them to pay on time and reimburse that fee.

Now here some people might ask, “Well, what are you? Are you not for profit? You’re not going to make that much money anymore. How is this consistent with long-term value creation?” And our view is that they’re actually completely consistent, in the long run. In the long run, that customer that has just received an email from Nubank apologizing for having done something that they didn’t need to do and reimbursing that money will say, “Wow, this is a fundamentally different experience.” And we have just earned a customer for the next 50 years. So that trust is extremely valuable and in the long run, sending that reminder email might make us make less money in the short-term but will help us have a customer working with us for a longer run. And that’s how that value and that strategy are completely consistent with each other and with maximizing for shareholder value in the long run.”

This story is something that helps build our confidence that Nu Holdings’ leaders are truly thinking about the long-term when growing the company. The actions of Velez and his team also reminds us of what Jeff Bezos wrote in Amazon’s 2012 shareholders’ letter:

“Proactively delighting customers earns trust, which earns more business from those customers, even in new business arenas. Take a long-term view, and the interests of customers and shareholders align.”

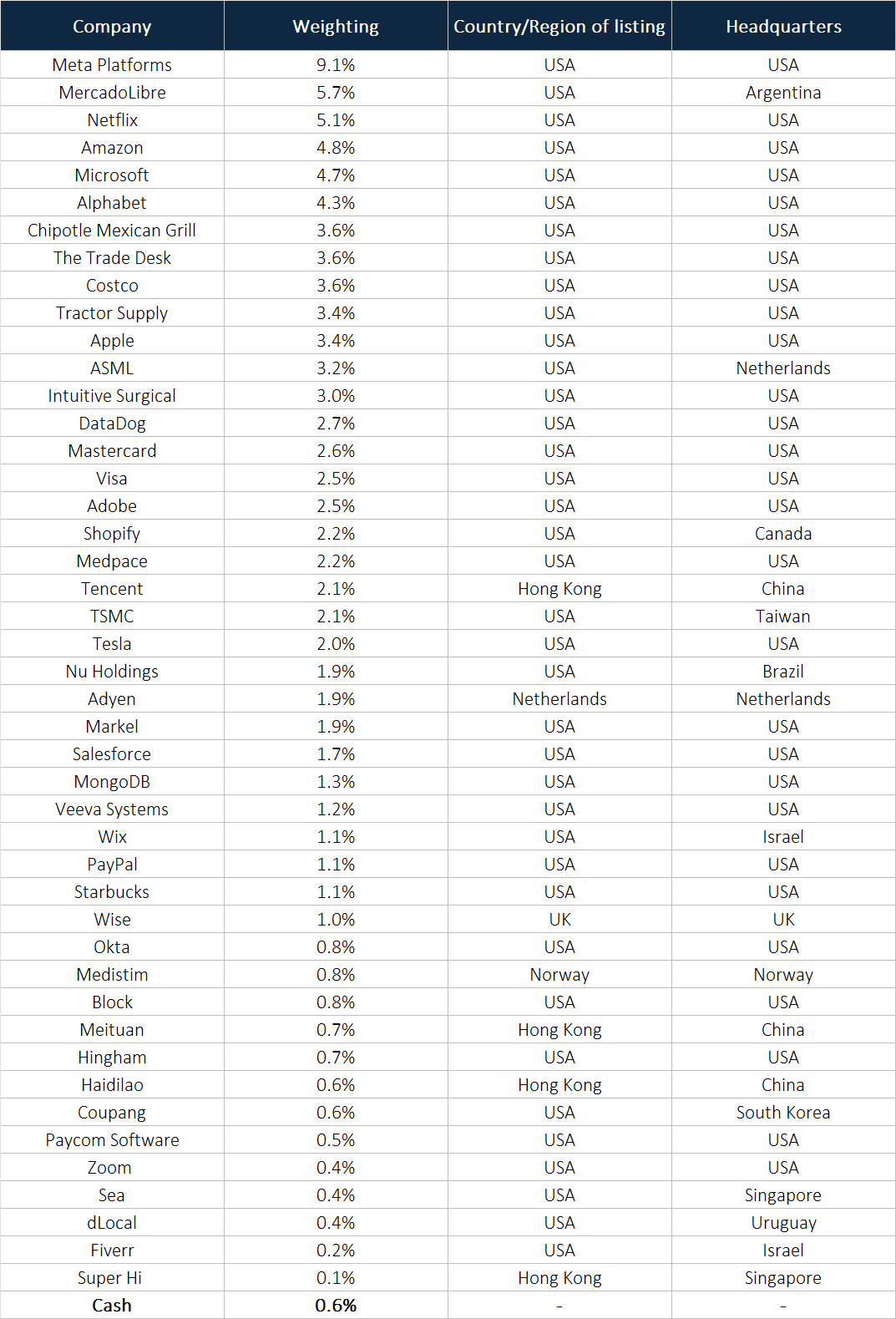

Here’s how Compounder Fund’s portfolio of 45 companies looks like as of 7 July 2024:

Table 3