Compounder Fund: DocuSign Investment Thesis - 14 Sep 2020

Data as of 11 September 2020

DocuSign (NASDAQ: DOCU) is one of the 40 companies in Compounder Fund’s initial portfolio. This article describes our investment thesis for DocuSign.

Company description

DocuSign provides DocuSign eSignature, currently the world’s leading cloud-based e-signature solution. This software service enables users to sign a document securely using almost any device from virtually anywhere in the world. It is the core part of the broader DocuSign Agreement Cloud, which is a suite of software services – again all delivered over the cloud – that automates and connects the entire agreement process. Among other features, DocuSign Agreement Cloud includes:

- Automatic generation of an agreement from data in other systems;

- Support of negotiation-workflow;

- Collection of payment after signatures;

- Use of artificial intelligence (AI) to analyse agreement-documents for risks and opportunities; and

- Hundreds of integrations with other systems, so that the agreement process can be seamlessly combined with other business processes and data

At the end of its fiscal year ended 31 January 2020 (FY2020), DocuSign had over 585,000 paying customers and hundreds of millions of users. From its founding in 2003 through to FY2019, the company had processed over 1 billion successful transactions (around 300 million in FY2019 alone). DocuSign defines a successful transaction as the completion of all required actions (such as signing or approving documents) by all relevant parties in an Envelope; an Envelope is, in turn, a digital container used to send one or more documents for signature or approval to the relevant recipients.

DocuSign serves customers of all sizes, from sole proprietorships to the companies that are among the top 2,000 publicly-traded enterprises. The company’s customers also come from many different industries, as the chart below illustrates.

Source: DocuSign investor presentation

For a geographical perspective of DocuSign’s business, its users are in over 180 countries. But in FY2020, 82% of the company’s revenue came from the US.

Investment thesis

We have laid out our investment framework in Compounder Fund’s website. We will use the framework to describe our investment thesis for DocuSign.

1. Revenues that are small in relation to a large and/or growing market, or revenues that are large in a fast-growing market

Has it ever occured to you that the innocuous act of signing documents with pen-and-paper can actually be a significantly wasteful activity for companies? Think about it. Signing a paper document requires you to fax, scan, email, snail-mail, courier, and file. DocuSign’s solution can save us both time and money.

There are many use-cases for DocuSign’s software services, ranging from sales contracts to employment contracts, non-disclosure agreements, and more. In fact, DocuSign has a customer that has implemented over 300 use-cases. DocuSign documents are legally accepted and protected with cryptographic technology from tampering. The documents also have a full audit trail, including party names, email addresses, public IP addresses, and a time-stamped record of each individual’s interaction with a document.

DocuSign estimated that it had a total addressable market of US$25 billion in 2017, using (1) the number of companies in its core markets, and (2) its internal estimate of an annual contract value based on each respective company’s size, industry, and location. This estimate remains unchanged (it was mentioned in the company’s FY2020 annual report), though recent business moves may have significantly expanded its addressable market. More on this later. At just US$1.16 billion, DocuSign’s revenue in the 12 months ended 31 July 2020 is merely a fraction of its estimated market opportunity.

We believe that DocuSign’s addressable market will likely grow over time. There are clear benefits to e-signatures. A 2015 third-party study by Intellicap (commissioned by DocuSign) found that the company’s enterprise customers derived an average incremental value of US$36 per transaction (with a range of US$5 to US$100) when using the company’s software as compared to traditional paper-processes. In FY2020, 82% of all the successful transactions that flowed through DocuSign’s platform were completed in less than 24 hours, while 50% were completed within just 15 minutes. DocuSign’s services help companies save money and time. The current COVID-19 pandemic has also accelerated the adoption of DocuSign’s services and crucially, we think this boost will persist even when the pandemic ends. During DocuSign’s earnings conference calls for the first and second quarters of FY2021, CEO Daniel Springer said:

“[First quarter of FY2021]

While no one is 100% sure what the world will look like, it’s clear that the ways of doing business are changing. Remote work is here to stay. Core business processes will only become more digital and agreements will need to be completed from anywhere, at any time on almost any device. As a result, for organizations that hadn’t already embraced DocuSign for eSignature, that were only using us for a few select use cases, the pandemic has been a catalyst for the greater digital transformation of their end-to-end agreement processes. We always believed this transformation will happen and that a unifying platform for agreements will be needed. COVID-19 is just happening faster.That said, even when the COVID-19 situation is behind us, we don’t anticipate customers returning to paper or manual-based processes. Once they take their first digital transformation steps with us and they realize the time, cost and customer experience benefits, they rarely go back. So, in short, we expect the adoption of our core eSignature offering by new customers and the expansion of use cases by existing ones to continue. This also acts as the on-ramp for the adoption of other Agreement Cloud products, sometimes at the same time, sometimes as follow ons.”

“[Second quarter of FY2021]

I spoke last quarter about how so many of them faced a sudden need to transition to remote work when the pandemic first hit. Today, that need has evolved from initial crisis response to business necessity. And because agreements are central to doing business, the need to agree electronically and remotely has never been stronger. This is causing greater adoption of our offerings, something we believe will persist beyond the crisis. Because in our experience, it’s very rare to see anyone go back to paper once they’ve gone digital…… One of our largest retail customers runs a network of healthcare clinics within its source. When COVID-19 hit, the company accelerated plans to provide telehealth services using DocuSign eSignature to handle consent and other paperwork remotely. This is a great example of COVID-accelerated demand that we see as durable. Now telehealth will remain after COVID-19, but the paperless processes that came with it will likely end up getting implemented for in-person clinic visits too because the electronic way is more efficient and a better experience than paper and clipboards.”

2. A strong balance sheet with minimal or a reasonable amount of debt

As of 31 July 2020, DocuSign held US$740.3 million in cash, short-term investments, and long-term investments. This is significantly higher than the company’s total debt of US$479.1 million (all of which are convertible notes). For the sake of conservatism, we also note that DocuSign had US$208.3 million in operating lease liabilities. But the company’s cash, short-term investments and long-term investments still outweighs the sum of the company’s debt and operating lease liabilities (US$687.4 million).

3. A management team with integrity, capability, and an innovative mindset

On integrity

Leading DocuSign as CEO is Daniel Springer, 56, who joined the company in January 2017. Some of the other key leaders in DocuSign, who are all young from a business perspective, are shown below:

- Scott Olrich, Chief Operating Officer, 48

- Cynthia Gaylor, Chief Financial Officer, 47

- Loren Alhadeff, Chief Revenue Officer, 41

- Kirsten Wolberg, Chief Technology and Operations Officer, 52

- Trâm Phi, General Counsel, 49

- Michael Sheridan, President International, 55

- Kamal Hathi, Chief Technology Officer

Most of the management team members mentioned above have relatively short tenure with DocuSign, but have collectively clocked decades in senior leadership roles in other technology companies.

Source: DocuSign proxy statement

We think DocuSign has a well-designed compensation structure. In FY2020, Daniel Springer received total compensation of US$8.73 million, 92% of which came from stock-based awards in the form of restricted stock units (RSUs) and performance-based stock units (PSUs). The RSUs vest over four years, while the PSUs depend on DocuSign’s relative share price performance compared to the NASDAQ index over a three-year period. We typically frown upon compensation plans that are linked to a company’s short-term stock price movements. In DocuSign’s case, the compensation for Springer is tied to multi-year changes in its stock price, which in turn is driven by the company’s business performance. So we think this aligns the interests of Springer and the company’s shareholders, which includes Compounder Fund. It’s worth noting too that DocuSign’s other key leaders saw the lion’s share (at least 84%) of each of their total compensation come from PSUs and/or RSUs with the same terms as Springer’s.

Notably, Springer also directly owned 1.43 million shares of DocuSign as of 31 March 2020 (with an additional 1.66 million options and 142,198 RSUs that were both exercisable within 60 days of 31 March 2020). The 1.43 million shares are worth nearly US$284 million at DocuSign’s 11 September 2020 share price of US$198.

On capability

From FY2013 to the second quarter of FY2021, DocuSign has seen its number of customers increase nearly 14-fold (42% per year) from 54,000 to 750,000. So the first thing we note is that DocuSign’s management has a terrific track record of growing its customer count.

Source: DocuSign investor presentation, annual report, and quarterly earnings update

To win customers, DocuSign’s software service offers over 300 pre-built integrations with widely used business applications from other tech giants such as salesforce.com, Oracle, SAP, Google, and more (Compounder Fund also owns shares in salesforce.com and the parent company of Google, Alphabet). These third-party applications are mostly in the areas of CRM (customer relationship management), ERP (enterprise resource planning), and HCM (human capital management). DocuSign also has APIs (application programming interfaces) that allow its software to be easily integrated with its customers’ own apps.

We also credit DocuSign’s management with the success that the company has found with its land-and-expand strategy. The strategy starts with the company landing a customer with an initial use case, and then expanding its relationship with the customer through other use cases. The success can be illustrated through DocuSign’s strong dollar-based net retention rates (DBNRRs). The metric is a very important gauge for the health of a SaaS (software-as-a-service) company’s business. It measures the change in revenue from all of DocuSign’s customers a year ago compared to today; it includes positive effects from upsells as well as negative effects from customers who leave or downgrade. Anything more than 100% indicates that the company’s customers, as a group, are spending more. DocuSign’s DBNRRs have been in a healthy low-teens to mid-teens range in the past few years, but the metric has surged to 120% (a record-high for DocuSign) in the second quarter of FY2021.

Source: DocuSign IPO prospectus and earnings call transcripts

We think DocuSign’s excellent execution in the face of the current COVID-19 pandemic is also worth highlighting, especially when considering that the company’s employees (around 5,000 people) are nearly all working remotely. A few examples:

- In the first quarter of FY2021, DocuSign’s eSignature solution helped the US government’s Department of Labor distribute over US$500 million in benefits to more than 500,000 residents in less than a week. DocuSign also helped a large US financial institution process more than 500,000 loan applications for loans, 75% of which were signed in less than 24 hours.

- DocuSign accelerated its hiring efforts in the first quarter of FY2021 to “address current demand and prepare for future growth.” In fact, DocuSign has hired 1,000 people since the COVID-19 pandemic erupted; this is a significant addition of headcount given that the company currently has around 5,000 employees.

- Despite seeing spikes in usage during the first quarter of FY2021, DocuSign was never near any capacity-constraint limits.

- In the first half of FY2021, DocuSign acquired more new customers (around 88,000 new customers were added) than it did for the entire FY2020.

We also want to highlight the high likelihood that Springer has created a fabulous culture at DocuSign. According to Glassdoor, a platform that allows employees to rate their companies anonymously, 92% of raters will recommend DocuSign to a friend. Meanwhile, Springer has a 98% approval rating, far higher than average Glassdoor CEO rating of 69%.

On innovation

We think DocuSign’s management scores well on the innovation front too. The company has been busy with using blockchain technology and AI to improve its services.

Blockchain technology is the backbone of cryptocurrencies and DocuSign has been experimenting with blockchain-based smart contracts since 2015. In June 2018, DocuSign joined the Enterprise Ethereum Alliance and showed how a DocuSign agreement can be automatically written onto the Ethereum blockchain. Here’s an example of a smart contract described by DocuSign:

“A smart contract turns a contract into something like a computer program. The Internet-connected program monitors data and triggers actions relevant to the contract’s terms. For example, a crop-insurance smart contract might use a trusted Internet feed of weather data. If the temperature goes above 85 degrees Fahrenheit in April, the smart contract will automatically trigger a crop-insurance payout, again via the Internet. This total automation eliminates ambiguity and promises large savings in time and effort for all parties involved.”

It’s early days for DocuSign’s use of blockchain, but we’re watching its moves here. DocuSign’s management acknowledges that many of the company’s customers don’t yet see the value of blockchain technology in the agreement process. But the company still believes in blockchain’s potential.

DocuSign has been working with AI since at least 2017 when it acquired machine-learning firm Appuri during the year. In February 2020, DocuSign inked an agreement to acquire Seal Software and the deal was completed in May with an outlay of around US$185 million. Seal Software was founded in 2010 and uses AI to analyse contracts. For example, Seal Software can search for legal concepts (and not just keywords) in large collections of documents, and automatically extract and compare critical clauses and terms. Prior to the acquisition, DocuSign was already tacking Seal Software’s services onto DocuSign Agreement Cloud. The combination of Seal Software and DocuSign’s technologies have helped a “large international information-services company” reduce legal-review time by 75%. Ultimately, DocuSign thinks that Seal Software will be able to strengthen DocuSign Agreement Cloud’s AI foundation.

Speaking of DocuSign Agreement Cloud, it was released in March 2019. As mentioned earlier, it includes multiple software services. DocuSign sees DocuSign Agreement Cloud as a new category of cloud software that connects existing cloud services in the realms of marketing, sales, human resources, enterprise resource planning, and more, into agreement processes. We see two huge positives that come with the introduction of multi-product sales. Firstly, it will likely lead to each DocuSign customer using more of the company’s products. This means that DocuSign could be plugged into an increasing number of its customers’ business processes, resulting in stickier customers. Secondly, DocuSign thinks that covering a wider scope of the entire agreement process could roughly double its market opportunity from the current size of US$25 billion to around US$50 billion.

As an example of recent product innovation, DocuSign acquired LiveOak Technology in July 2020 for US$48 million to accelerate the launch of DocuSign Notary, a new product for remote online notarization, where signers and the notary public are in different places. Although DocuSign Notary is not expected to significantly increase DocuSign’s market opportunity, we still think it’s a smart move to make. Online notarisation is likely to be a strong complement to DocuSign’s existing solutions. LiveOak Technology’s platform “includes several technologies specific to remote agreements, such as video conferencing, video identity verification, collaborative form-filling, an integration with DocuSign eSignature, and a detailed audit trail.” DocuSign Notary is slated for a beta launch in November this year.

4. Revenue streams that are recurring in nature, either through contracts or customer-behaviour

DocuSign’s business is built nearly entirely on subscriptions, which generate recurring revenue for the company. Customers of DocuSign gain access to the company’s software platform through a subscription, which typically ranges from one to three years. In FY2020, FY2019, and FY2018, more than 93% of DocuSign’s revenue in each fiscal year came from subscriptions to its cloud-based software platform; the rest of the revenue came from services such as helping the company’s customers deploy its software efficiently.

There are two other data points that give us confidence in the recurrent-nature of DocuSign’s revenue. First, almost two-thirds of the transactions that flow through DocuSign’s platform are from organisations that have integrated DocuSign’s products into their own systems, and not just simply using the company’s software to create a document to be e-signed. Second, there is no customer-concentration with DocuSign, since there was no customer that accounted for more than 10% of the company’s revenue in FY2020.

5. A proven ability to grow

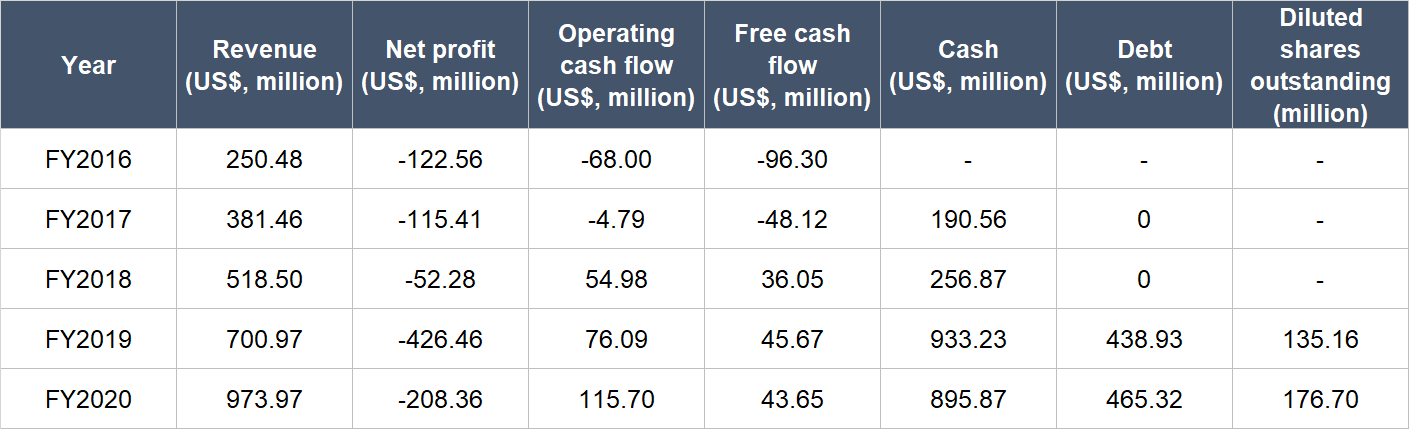

There isn’t much historical financial data to study for DocuSign, since the company was only listed in April 2018. But we do like what we see:

Source: DocuSign annual reports and IPO prospectus

A few notable points from DocuSign’s financials:

- DocuSign has compounded its revenue at an impressive annual rate of 40.4% from FY2016 to FY2020. The rate of growth has not slowed much, coming in at a still-impressive 38.9% in FY2020.

- DocuSign is still making losses, but the good thing is that it started to generate positive operating cash flow and free cash flow in FY2018.

- Annual growth in operating cash flow from FY2018 to FY2020 was strong, at 45.1%. Free cash flow has increased at a much slower pace, but the company is investing for growth.

- The company’s balance sheet remained robust throughout the timeframe under study, with significantly more cash and investments than debt.

- At first glance, DocuSign’s diluted share count appeared to increase sharply by 30.7% from FY2019 to FY2020. (We only started counting from FY2019 since DocuSign was listed in April 2018, which is in the first quarter of FY2019.) But the number we’re using is the weighted average diluted share count. Right after DocuSign got listed, it had a share count of around 152 million. Moreover, DocuSign’s weighted average diluted share count showed acceptable year-on-year growth rates (acceptable in the context of the company’s rapid revenue growth) in the first, second, and third quarters of FY2020.

Source: DocuSign quarterly earnings updates

At a time when the US economy is suffering because of COVID-19 (US GDP fell by 9.1% year-on-year in the second quarter of 2020), DocuSign has managed to continue posting strong revenue growth in the first half of FY2021. In fact, DocuSign’s revenue growth accelerated in the second quarter of FY2021 compared to the first quarter. The company is also starting to really grow its cash-flow-muscle. These are all shown in the table below.

Source: DocuSign earnings updates

6. A high likelihood of generating a strong and growing stream of free cash flow in the future

DocuSign has already started to generate positive operating cash flow and free cash flow. We think it’s likely that DocuSign’s free cash flow will increase at a rapid clip in the future for two reasons.

First, it looks likely to us that DocuSign will be producing impressive top-line growth in the years ahead. As we discussed earlier, COVID-19 has not dented DocuSign’s growth and has in fact been a positive catalyst for its business. But even when the pandemic blows over, we think DocuSign is set to capitalise on strong secular tailwinds with the growing adoption of eSignatures and digital solutions for managing business agreements because they save users time and money.

Second, we think DocuSign can enjoy a higher free cash flow margin in the future as its business scales. Right now, DocuSign has a poor trailing free cash flow margin (free cash flow as a percentage of revenue) of just 11.5%. But we think there’s plenty of room for improvement given the typically asset-light nature of a software business. And for perspective, Veeva Systems, a SaaS company serving the life sciences industry and another of Compounder Fund’s holdings in the initial portfolio, has an average free cash flow margin of 29% in its last five completed fiscal years.

Valuation

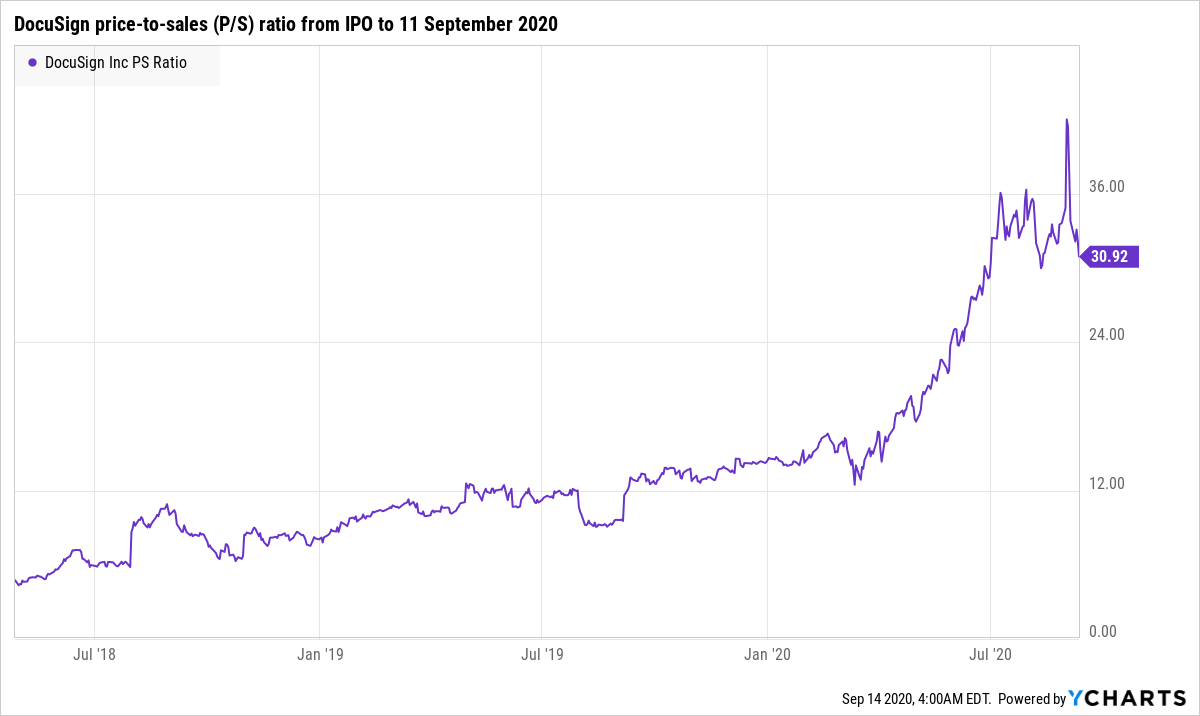

We completed our purchases of DocuSign shares with Compounder Fund’s initial capital in late July 2020. Our average purchase price was US$199 per DocuSign share. At our average price and on the day we completed our purchases, DocuSign shares had a trailing price-to-sales (P/S) ratio of around 34. We like to keep things simple in the valuation process. In DocuSign’s case, we think the P/S ratio is an appropriate metric to value the company, since the company has yet to produce much free cash flow.

The P/S ratio of 34 is pretty darn high and that’s a risk. For perspective, if we assume that DocuSign has a 25% free cash flow margin today, then the company would have a price-to-free cash flow ratio of 136 (34 divided by 25%). Moreover, the P/S ratio of 34 is high when compared to history. The chart below shows DocuSign’s P/S ratio from its listing to 11 September 2020:

But DocuSign also has a few strong positives going for it. The company has: (1) revenue that is low compared to a fast-growing addressable market; (2) a business that solves important pain points for customers; (3) a large and rapidly expanding customer base; and (4) sticky customers who have been willing to significantly increase their spending with the company over time. We believe that with these traits, there’s a high chance that DocuSign will continue posting excellent revenue growth – and in turn, excellent free cash flow growth – in the years ahead.

The risks involved

There are four key risks we’re watching with DocuSign.

The first is DocuSign’s short history in the stock market, given that its IPO was just two years ago in April 2018. But we are willing to back DocuSign because we think its business holds promise for fast-growth for a long period of time (the company’s eSignature and Agreement Cloud services are very important for the digital transformation that so many companies are currently undergoing).

Competition is another risk we’re keeping an eye on. Adobe, another holding in Compounder Fund’s initial portfolio, is a much larger SaaS company with trailing revenue of over US$12 billion. Through its Adobe Sign product, Adobe is the primary competitor of DocuSign. So far, DocuSign has defended its turf admirably. This is shown in DocuSign’s strong revenue and customer growth rates, and its long history of achieving a DBNRR in the low to mid-teens range. But Adobe’s much stronger financial might compared to DocuSign means competition is a risk.

Another important risk for DocuSign – the third risk – relates to data breaches and downtime in the company’s services. DocuSign handles sensitive information about its customers due to the nature of its business. If there are any serious data breaches in DocuSign’s software services, the company could lose the confidence of customers and the public, leading to growth difficulties. The signing of documents may be highly time-sensitive events. So if there is any significant downtime in DocuSign’s services, it could also lead to an erosion of trust among existing as well as prospective customers. So far, DocuSign has done a great job by providing 99.99% availability in FY2020.

DocuSign’s high valuation is the fourth risk. The high valuation adds pressure on the company to continue executing well; any missteps could result in a painful fall in its stock price. This is a risk we’re comfortable taking.

Ultimately, we will consider parting ways with DocuSign if we see any or all of the following signs from the company: (1) The DBNRR comes in at less than 100% for an extended period of time; (2) it fails to increase its number of customers; and (3) it’s unable to convert revenue into free cash flow at a healthy clip in the future.

Summary and allocation commentary

Summing up DocuSign, it has:

- Valuable cloud-based software services in the agreements space that solves customers’ pain-points;

- high levels of recurring revenue;

- outstanding revenue growth rates;

- positive operating cash flow and free cash flow, with the potential for much higher free cash flow margins in the future;

- a large, growing, and mostly untapped addressable market;

- an impressive track record of winning customers and increasing their spending; and

- capable leaders who are in the same boat as the company’s other shareholders

The company does have a premium valuation, so we’re taking on valuation risk. There are also other risks to note, such as DocuSign’s short listing history; the presence of competitors with significantly stronger financial might; and the potential for a severe loss of customer-confidence in the event that DocuSign’s services are hacked and/or are down for an extended period of time.

After weighing the pros and cons, we initiated a 2.5% position – a medium-sized allocation – in DocuSign with Compounder Fund’s initial portfolio. We think DocuSign scores well in terms of having a sizeable market opportunity and a high probability of being able to grow into its market. But our enthusiasm for the company is also tempered by its high valuation.

And here’s an important disclaimer: None of the information or analysis presented is intended to form the basis for any offer or recommendation; they are merely our thoughts that we want to share.