Compounder Fund: Etsy Investment Thesis - 29 Apr 2021

Data as of 28 April 2021

Etsy (NASDAQ: ETSY), which is based and listed in the USA, is one of the four companies in Compounder Fund’s portfolio that we invested in for the first time in April 2021. This article describes our investment thesis for the company.

Company description

Etsy owns and operates two ecommerce marketplaces that connect buyers and sellers. The first is the company’s eponymous marketplace – Etsy – which focuses on being a destination for unique and creative products.

(From here on, the italicised “Etsy” would refer to the company’s Etsy marketplace, while the non-italicised “Etsy” would refer to the company.)

If you visit the Etsy marketplace, which can be accessed via desktop and mobile (through both a mobile website and mobile app), you will find that the listed products are typically hand-crafted, custom-designed, vintage, or one-of-a-kind products that cannot be found elsewhere. We consider the Etsy marketplace to be well-differentiated from other ecommerce marketplaces due to its unique products. The sellers on Etsy are typically creative artisans and entrepreneurs and they range from hobbyists to professional merchants. Etsy’s 2021 seller survey found that 45% of Etsy sellers sell through only one channel; the other 55% are multi-channel sellers but on average, Etsy is their primary source of sales. A 2020 survey also found that 88% of Etsy buyers agreed that Etsy has items that can’t be found anywhere else.

The Etsy marketplace currently features around 85 million item listings across multiple retail categories (more than 50) and ended 2020 with 4.1 million active sellers (an active seller is defined as a seller who has sold an item in the last 12 months).

There were 81 million active buyers on the Etsy marketplace (defined as a buyer who has bought an item in the last 12 months) in 2020. As described by the company, buyers on the Etsy marketplace “value self-expression, unique items, and buying directly from creative artisans and entrepreneurs.” The marketplace allows buyers to connect directly with sellers to ask questions about the products and make customisation requests. We think that the ability for buyers and sellers to have meaningful interactions is another point of differentiation for the Etsy marketplace.

In 2020, the Etsy marketplace facilitated around US$9.4 billion in gross merchandise sales (GMS). Excluding masks, GMS on the Etsy marketplace came in at US$8.7 billion; 2020, being the year of the COVID-19 pandemic, saw the Etsy marketplace facilitate an unusually high number of mask sales (US$743 million worth, or 8% of the marketplace’s total GMS) compared to previous years. The chart below shows the top six retail categories for the Etsy marketplace in 2020 and their respective GMS (masks, which belong to the Beauty & Personal Care category, are excluded). These six categories accounted for around 80% of the Etsy marketplace’s total GMS in 2020.

Source: Etsy March 2021 investor presentation

Etsy’s second marketplace is named Reverb and it was acquired by Etsy in 2019. Reverb, which is also available via a website and mobile app, is an ecommerce marketplace that is dedicated to buyers and sellers of new, used, and vintage musical instruments. In 2020, the Reverb marketplace had 0.9 million active buyers and 0.3 million active sellers. It also ended the year with 1.8 million listings – a wider variety of inventory than any single retailer can achieve – that include unique used and vintage gear; instruments played on tour and on popular albums by well-known musicians; and exclusive, boutique, and handmade items that can only be found on Reverb.

Collectively, the Etsy and Reverb marketplaces ended 2020 with 4.4 million active sellers, 81.9 million active buyers, nearly 87 million item listings, and US$10.3 billion in GMS. The two marketplaces helped Etsy to earn total revenue of US$1.73 billion in 2020. This revenue can be split into marketplace revenue (US$1.30 billion, or 75.5% of total revenue) and services revenue (US$422 million, or 24.5%).

Etsy earns marketplace revenue by charging fees for (1) listing an item for sale, (2) completing transactions between a buyer and a seller, and (3) processing payments with its payment platform, Etsy Payments. Typically, Etsy charges the following for the Etsy and Reverb marketplaces:

- US$0.20 to list an item on the Etsy marketplace (for up to four months).

- A 5% transaction fee for each completed transaction on the Etsy marketplace.

- Additional transaction fees of 12% or 15% if a seller uses Etsy’s offsite advertising service; offsite advertising fees kick in when Etsy places an advertisement on a third-party internet platform that leads to a sale for a seller.

- Payment-processing fees of between 3.0% and 4.5%, plus a flat fee; there are additional fees for transactions that involve currency conversions. In 2020, 92% of total GMS from the Etsy marketplace was processed through Etsy Payments.

- A 5.0% seller transaction fee and payment processing fees for each completed transaction on Reverb.

Meanwhile, Etsy’s services revenue consists of fees sellers pay Etsy for optional services that are designed to help sellers grow their businesses. There are two main optional services for the Etsy marketplace currently. The first is on-site advertising, which allows Etsy sellers to pay for prominent placements in search results. The second is Etsy Shipping Labels, which allows Etsy sellers to purchase discounted shipping labels, print shipping labels at home (thereby saving sellers time and money), and reduce the administrative burden for sellers (such as by automatically populating shipping addresses and providing buyers with tracking and shipping notifications). Optional services for the Reverb platform include an on-site advertising service called Bump (where sellers can determine their own ad rates) and Reverb Shipping Labels (where sellers can access discounted shipping).

There are a few different ways to understand the geographic-split of Etsy’s business. The company has seven core markets, namely, the USA, the UK, Germany, Canada, Australia, France, and India. The first way to look at the geographic contour of Etsy’s business is the location of its sellers. The USA is the most important country for Etsy from this perspective, with 67% of Etsy’s total revenue of US$1.73 billion in 2020 coming from sellers that are based in the country; the remaining 33% came from UK-based sellers (11%) and sellers from other countries (no other country’s sellers accounted for 10% or more of the company’s revenue during the year). Looking at where Etsy’s sellers and buyers are located gives another geographic perspective on Etsy’s business. In 2020, 36% of Etsy’s total GMS of US$10.3 billion was generated when a seller or buyer, or both, were located outside the USA.

Investment thesis

We have laid out our investment framework in Compounder Fund’s website. We will use the framework to describe our investment thesis for Etsy.

1. Revenues that are small in relation to a large and/or growing market, or revenues that are large in a fast-growing market.

In 2019, Etsy conducted a market opportunity analysis. The company estimated that its aforementioned seven core geographical markets, excluding India, had a total commerce opportunity – involving the retail categories that are relevant to the Etsy marketplace – of US$1.7 trillion in 2018. Of the US$1.7 trillion, US$249 billion was in online commerce and roughly US$100 billion of the US$249 billion was for “special” niche products (see chart below). But that’s not all. Etsy believes that the total commerce opportunity should expand from US$1.7 trillion in 2018 to US$2 trillion in 2023, with the online commerce portion increasing to US$437 billion. Extrapolating the same “special”-niche-products-to-online-commerce-opportunity ratio in 2018 (US$100 billion divided by US$249 billion) to the 2023 projections will result in a dollar amount of around US$175 billion.

Source: Etsy March 2021 investor presentation

With Etsy’s total GMS of ‘just’ US$10.3 billion in 2020, the company still has plenty of space to run. But even more importantly, we think Etsy is well-placed to capture the GMS growth opportunity it has for three reasons.

The first reason is that Etsy appears to have built a strong brand for itself. The company believes that “many new buyers and sellers” discover the company’s marketplaces through word of mouth. Meanwhile, the Etsy marketplace has a net promoter score (NPS) of 59 among Etsy buyers based on a January 2021 survey. The NPS ranges from -100 to +100 and it measures the willingness of customers to recommend a company’s product or service to others and can be a gauge of customer loyalty and satisfaction. An important way that we think Etsy has made the Etsy marketplace popular with users – both buyers and sellers – is by improving their experiences with it through the use of technology such as artificial intelligence and machine learning.

For example, Etsy has been improving the search experience for buyers, such as by (1) introducing a new feature in 2020 that prioritises the most helpful reviews for buyers to make more informed decisions, and (2) introducing personalised search in the third quarter of the year, where different buyers will get different results for the same search if they have exhibited different behaviour on the Etsy marketplace. As Etsy collects more data on buyers’ behaviour over time, the personalised search feature should improve, making the user-experience for buyers even better. Tangible results can already be seen – the percentage of total Etsy marketplace purchases that come from products appearing on the first page of search results have increased from 77% at the start of 2018 to 86% at the end of 2020. In another example, this time for sellers, Etsy is able to translate listings within the Etsy marketplace to increase the selection variety for non-English speaking buyers and thus give sellers access to a truly global audience.

The second reason, which is related to the first, is that Etsy already has a strong network of buyers and sellers. As already mentioned, the company’s core Etsy marketplace ended 2020 with 81 million active buyers and 4.1 million active sellers. Together with the Reverb marketplace, Etsy can boast of 81.9 million active buyers and 4.4 million active sellers. We think that a marketplace type of business that Etsy operates exhibits network effects, where more buyers leads to more sellers, which leads to even more buyers, and so on. It will become increasingly difficult over time for new entrants to compete with Etsy, especially if Etsy continues to improve the user experience for its marketplaces. Earlier, we shared examples of how Etsy has made its marketplaces better for users through technology. Later, we’ll discuss the company’s culture, which is what we think makes Etsy’s marketplaces special for users.

The third reason is that, according to Etsy, “the COVID-19 pandemic [in 2020] significantly shifted global consumer shopping behavior towards online purchases of many retail categories.” And now, there’s an opportunity for Etsy to deepen engagement with buyers by inspiring them to make purchases for different occasions throughout the year, as shown in the graphic below.

Source: Etsy 2020 annual report

We also want to highlight that Etsy’s growth opportunities go beyond the GMS that it could potentially capture. There’s also the angle of its take rate – the total amount of revenue earned by Etsy per dollar of GMS it facilitates – to consider. By introducing more optional services for sellers, and by getting more sellers to adopt current optional services, Etsy would be able to increase its take rate in the future. The company has already been doing so successfully. In 2014, services revenue was 17.6% of Etsy’s total revenue and it helped Etsy to achieve a take rate of 10.1%; in 2020, services revenue grew to 24.5% of Etsy’s total revenue and the take rate was 16.8%. There may be more to come. As mentioned previously, there are two main optional services for the Etsy marketplace currently: On-site advertising, and Etsy Shipping Labels. In 2020, just 22% of active sellers on the Etsy marketplace used on-site advertising while only 22% of active Etsy sellers in regions where Etsy Shipping Labels was offered used the service.

2. A strong balance sheet with minimal or a reasonable amount of debt

Etsy has what we would consider a strong balance sheet. The company exited 2020 with US$1.67 billion in cash and short-term investments, and US$1.06 billion in total debt, giving rise to a net-cash position of US$607 million. For the sake of conservatism, we note that Etsy has finance leases of US$53.5 million at the end of 2020. But this is dwarfed by the company’s aforementioned net-cash position.

It helps too that Etsy has been generating strong free cash flow for a few years. There will be more on this later.

3. A management team with integrity, capability, and an innovative mindset

On integrity

Etsy is currently led by the 52 year-old Josh Silverman, who assumed the role in May 2017 after joining the company’s Board in November 2016. Before Etsy, Silverman already had years of experience in senior leadership roles in the digital payments giant American Express, as well as in other technology companies. Etsy’s other key leaders are shown in the table below. Like Silverman, they (1) are young in a business sense, (2) each have at least a few years under their belt in senior leadership roles at Etsy, and (3) also have had management experience at other technology firms, with Patel Goyal being the exception – but in her case, she was already in senior roles in Etsy prior to being Etsy’s product head. These are all traits that we appreciate.

Source: Etsy 2020 proxy statement

We think that the compensation structure of Etsy’s aforementioned key leaders demonstrates integrity. In May 2017 Silverman was given a front-loaded equity grant in conjunction with his appointment as CEO. The equity grant was designed to provide him with a meaningful equity stake in Etsy and also barred him from receiving any additional equity grants until 2021. Early this year, Etsy implemented a new compensation plan for Silverman. Under the new plan, Silverman will earn between 0 and 229,672 shares of Etsy as PSUs (performance share units), with the number of PSUs to be determined by Etsy’s (1) GMS, (2) revenue, (3) adjusted-EBITDA margin, and (4) total stockholder return relative to the constituents of the Nasdaq index. All four metrics are equally weighted and will be measured over the three year period from 2021 to 2023. The new plan will also see Silverman be granted Etsy shares with a grant-date value of US$9 million, of which 60% will be in RSUs (restricted share units) and 40% in stock options. The RSUs and stock options vest over a four-year period, beginning on 1 October 2021.

So, all of Silverman’s equity-related compensation for 2021 will ultimately be determined by the multi-year performance of Etsy’s business (technically, the RSUs and stock options depend on multi-year changes in Etsy’s stock price, but a company’s long-term stock price movement is largely governed by its underlying business performance). Meanwhile, the equity-related compensation for Etsy’s other key leaders in 2021 would have a mix of 25% in PSUs, 50% in RSUs, and 25% in stock options that all have the same terms as Silverman’s.

It’s also worth pointing out that the monetary-value of Silverman’s equity-related compensation for 2021 will likely dwarf his base salary and non-equity-related compensation for the year. For perspective, the total value of Silverman’s base salary and non-equity-related compensation in 2020 and 2019 were US$1.93 million and US$1.08 million, respectively. As already mentioned, the RSUs and stock options that would be granted to Silverman would have a grant-date value of US$9 million, while the PSUs would have an upper-limit of US$47.7 million at Etsy’s 28 April 2021 share price of US$207.

Another thing worth highlighting is that Silverman has massive skin in the game. As of 13 April 2021, Silverman controlled (a) 64,097 Etsy shares, and (b) 3 million Etsy shares in the form of stock options that were already exercisable or exercisable within 60 days as of that date. Collectively, Silverman’s Etsy shares have a value of around US$636 million at the aforementioned share price of US$207 as of 28 April 2021.

On capability and ability to innovate

We rate Silverman and his team highly here, and there are a few things we want to discuss.

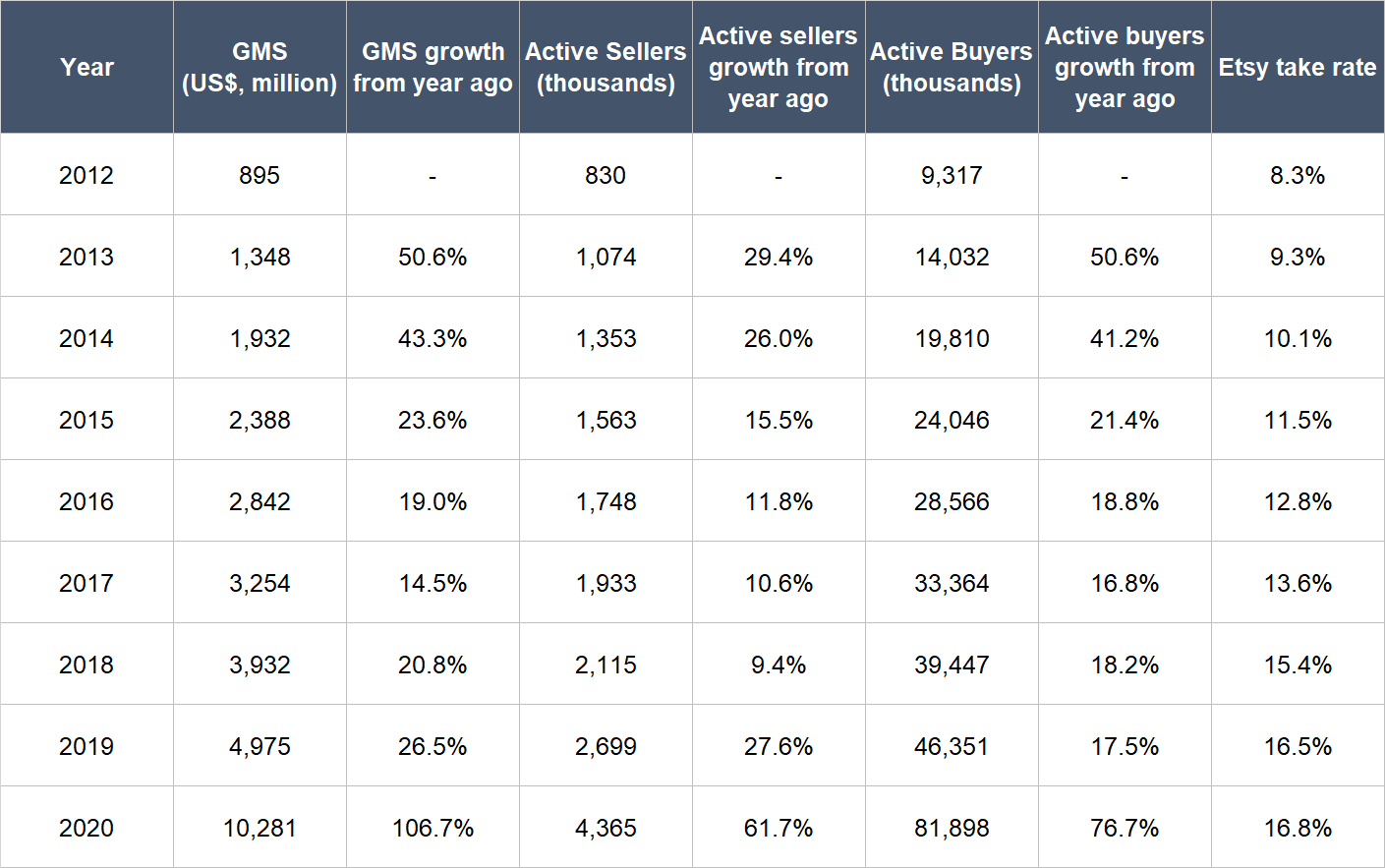

The first thing is the historical growth in Etsy’s GMS, number of active buyers and sellers, and its take rate. These are all metrics that can let us know the health of Etsy’s marketplaces. The table below shows Etsy’s track record in this matter from 2012 to 2020. Growth was strong throughout the timeframe we’re looking at for the four merics. But we want to highlight that (1) Etsy’s GMS growth accelerated from 2017 – the year Silverman became CEO – to 2019 and the growth rate skyrocketed in 2020, (2) a similar growth-dynamic to Etsy’s GMS was present as well for Etsy’s number of active sellers, and (3) Silverman and his team had managed to continue growing Etsy’s take rate from 2017 to 2020.

Source: Etsy annual reports

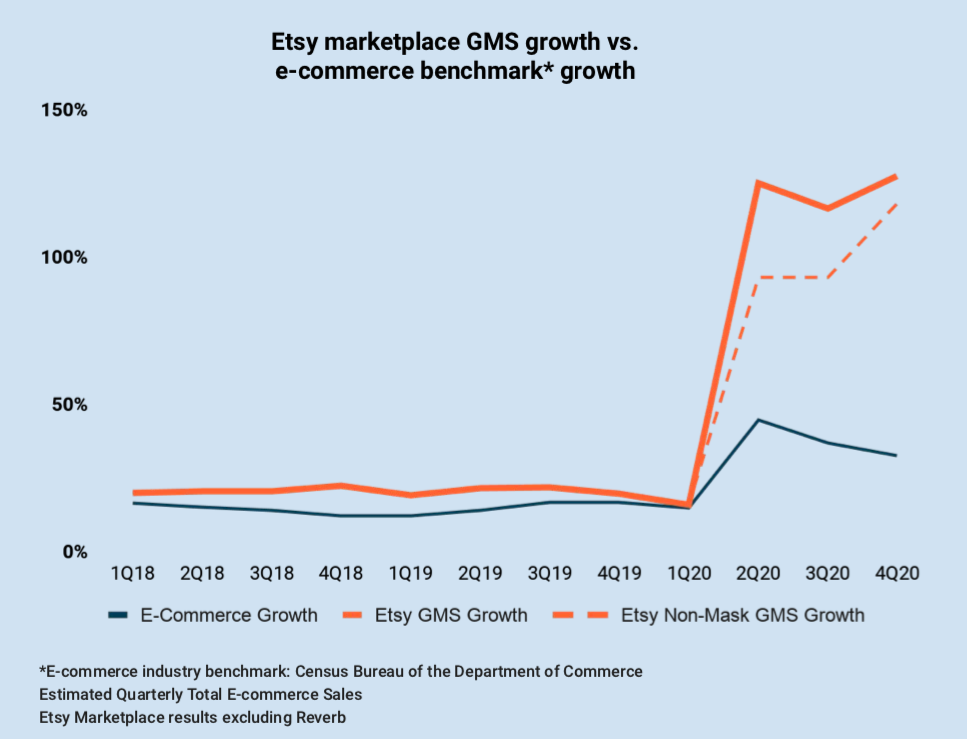

Speaking of Etsy’s performance in 2020, this is the second thing we want to discuss. During the year, COVID-19 caused a surge in ecommerce activity, which benefited Etsy. But as the chart below shows, the GMS growth for the Etsy marketplace (see the solid orange line) was much faster compared to the overall ecommerce space (dark blue line) and we think Silverman and his team deserves credit for this. Part of Etsy’s growth in 2020 can be traced to a massive spike in demand for masks – as we shared earlier, masks accounted for 8% of the Etsy marketplace’s total GMS in 2020 when it was only a small retail category for the marketplace previously. But even after excluding masks (see the dotted orange line), the increase in GMS for the Etsy marketplace in the second, third, and fourth quarters of 2020 still came in at around or above 100% and far outpaced the ecommerce market.

Source: Etsy March 2021 investor presentation

Sticking with COVID-19, we’re impressed with the actions that Silverman and his team took during the pandemic to support employees and sellers and this is the third thing we want to discuss. Some examples of what Etsy did in 2020:

- Etsy shifted to a fully remote work environment in March of the year. The switch caused stress to many employees and to cope with that, management initiated company-wide “rest and recharge” days as well as expanded paid family leave.

- Etsy published its “Ultimate Guide to Running Your Shop During COVID-19” to help its sellers navigate the challenges brought about by the pandemic.

- The company provided over US$13 million in one-time investments and donations to support sellers and the community, and launched the “Stand with Small” advertising campaign to remind consumers that buying from the Etsy marketplace helps support independent sellers.

- Etsy communicated with US lawmakers to ensure that the self-employed were included in major COVID-19 relief bills and legislation.

- The company expanded 24/7 live chat and phone support for both buyers and sellers.

- When it was clear that masks would be in high demand, Etsy called for its sellers to produce masks while supporting the sellers by providing educational resources on best practices and permissible mask products.

The fourth thing we want to discuss is the technological progress that Etsy has made under Silverman and his team. Earlier, we shared Etsy’s recent use of artificial intelligence and machine learning to improve the search experience for buyers. There’s more. Etsy completed the migration of its data center and ecommerce marketplace to Google Cloud in February 2020. For a company the size of Etsy, moving so much data from its private on-premise systems to a public cloud obviously took a sizable effort from the team; all told, Etsy migrated 5.5 petabytes of data to the cloud. According to Google Cloud, Etsy ended up with more than 50% savings in compute energy. The migration also helped Etsy process twice as much data per search query in 2020 compared to 2019. In other examples:

- Etsy launched listing videos in 2020 and it helps Etsy sellers to showcase their products in ways they previously could not with just photos; around 3.2 million seller videos were uploaded as of end-2020.

- Etsy implemented free shipping in the Etsy marketplace in 2019 by providing sellers with tools and support to help them to offer free shipping to US buyers for orders above a certain value. At the end of 2020, 66% of items on the Etsy marketplace had free shipping for US buyers, 73% of US listing views were eligible for free shipping, and 46% of global orders were delivered with free shipping.

- In 2020, Etsy continued to improve shipping transparency for buyers and around 34% of US listing views, as of 31 December 2020, had an expected delivery date.

- The company continued to expand support channels for buyers and sellers in 2020. In the fourth quarter of the year, 73% of buyer contacts happened through phone and chat with the balance happening through email; the selfsame percentages in the fourth quarters of 2019 and 2018 were 64% and 26%, respectively.

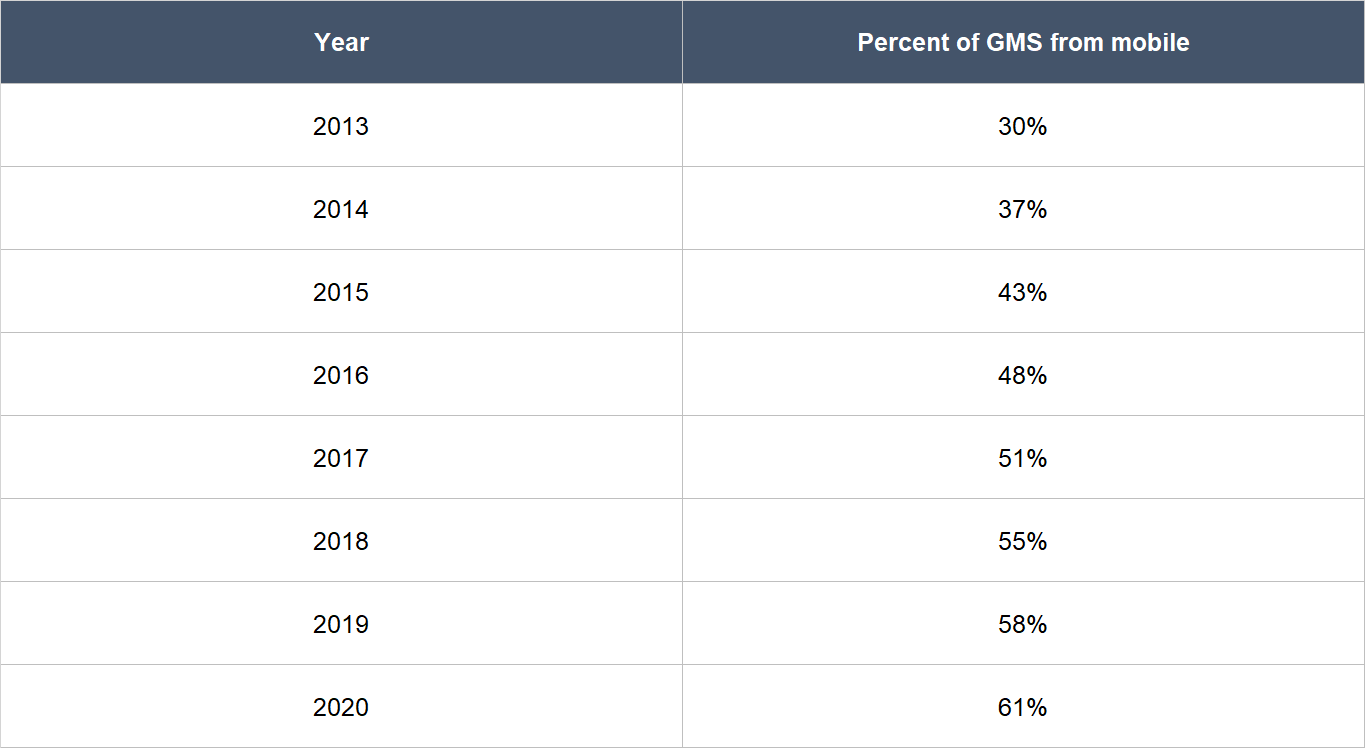

Etsy’s progress in mobile is the fifth thing we want to discuss. In a mobile dominated world (when it comes to the internet, users in the USA spent nearly double the time on mobile than on desktops in 2018, according to data from Mary Meeker’s Internet Trends 2019 report), getting the right mobile strategy can be important for ecommerce companies. The mobile website and app for Etsy buyers include search and discovery, curation, personalisation, augmented reality, and social shopping features; Etsy also offers a connected experience through each channel (desktop, mobile web, and mobile app). We think that these traits are likely to make the Etsy mobile experience great for buyers and the numbers lend strength to this view. The table below shows the percentage of Etsy’s total GMS coming from transactions that are made on mobile devices in each year from 2013 to 2020. The percentage was already rising prior to Silverman’s appointment as CEO, but he and his team have continued to grow it and today, mobile is the dominant channel for Etsy’s GMS.

Source: Etsy annual reports

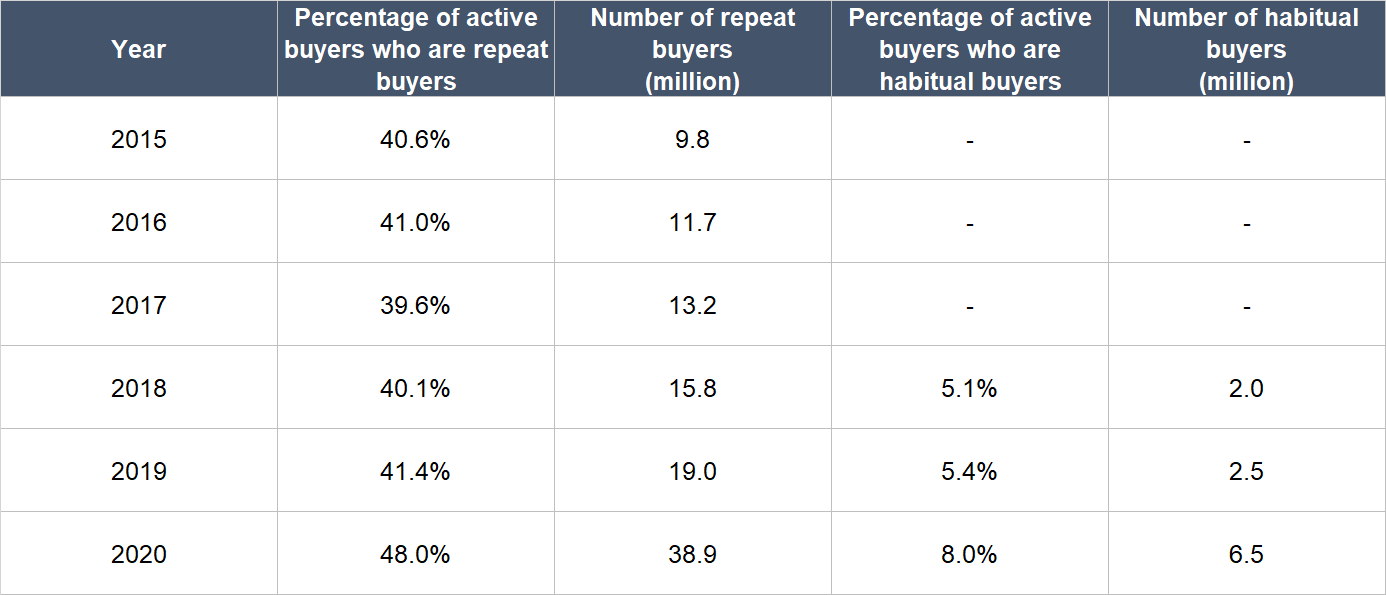

The sixth thing we want to discuss is the strong growth in Etsy’s repeat and habitual buyers. Repeat buyers are consumers on the Etsy marketplace who have made purchases on two or more days in the last 12 months. Meanwhile, habitual buyers are consumers on the marketplace who have spent US$200 or more and made purchases on at least six days in the last 12 months. Growth in repeat and habitual buyers is a sign of increasing customer-loyalty for the Etsy marketplace. The table below illustrates two things that have happened under Silverman’s watch: (a) The number of repeat and habitual buyers have increased; and (b) the percentage of active Etsy buyers who are repeat and habitual buyers have also risen.

Source: Etsy annual reports

The seventh and last thing we want to talk about is Etsy’s culture, which is what we think makes the company’s marketplaces special for both buyers and sellers. It is thus also related to most of everything else we’ve been discussing in the “On capability and ability to innovate” sub-section of this article. Here’s what Etsy mentioned about its mission in its latest annual report for 2020:

“Our mission to “Keep Commerce Human” is rooted in our belief that, although automation and commoditization are parts of modern life, human creativity cannot be automated and human connection cannot be commoditized. We believe that consumers are demanding more of the businesses they support and that companies that build win-win solutions that are good for people, the planet, and profit will be best positioned to succeed. We are committed to growing sustainably by aligning our mission, guiding principles, and business strategy. This is what makes us distinct from mass retailers. Our mission guides our daily decisions, sets the path for our long-term success, and reinforces our commitment to make a positive social, economic, and ecological impact.”

It’s clear to us that Etsy walks its talk. Proof of this can be seen in a few things we discussed earlier: (1) Etsy’s actions during the COVID-19 pandemic; (2) the massive growth over the years in Etsy’s active buyers and active sellers; (3) the high NPS that Etsy buyers give to the marketplace; and (4) the increase in buyer-engagement over time under Silverman’s tenure as CEO. Here are other examples:

- Etsy’s 2020 Pay Equity analysis found no unexplained pay gaps adverse to women employees, employees from other marginalised genders, or non-white employees.

- Etsy sourced 100% of its electricity in 2020 from renewable energy sources and also achieved zero waste operations during the year (its third year in a row of doing so).

- According to Glassdoor, a website that allows a company’s employees to rate it anonymously: Etsy currently has a 4.2-star rating out of 5; 82% of Etsy-raters would recommend a friend to work at the company; and Silverman has a 95% approval rating as CEO, far higher than the average Glassdoor CEO rating of 69% in 2019.

Etsy was co-founded in 2005 by the talented wood-worker, Rob Kalin, and his two friends, Haim Schoppik and Chris Maguire (all three are no longer with the company). They wanted to create a marketplace for crafters and artisans that had a strong human touch, to the point where it was nearly anti-capitalistic. To us, the company was always tethered to the idea of having that strong human touch in its commercial activities from the time of Etsy’s founding to when Silverman took over as CEO. Before Silverman’s appointment, Etsy’s mission was “to reimagine commerce in ways that build a more fulfilling and lasting world” – the company’s current mission to “Keep Commerce Human” was created under Silverman’s watch. In our eyes, Silverman has managed to keep what’s special about Etsy intact, while continuing to improve its business.

What makes Silverman’s achievements with Etsy even more impressive is that Etsy’s employees were initially skeptical of his appointment. According to a New York Times profile of Silverman’s early days at Etsy, when he gave an introductory speech to employees after the company had announced his appointment as CEO, he was met with a hostile reception. Undeterred, Silverman wasted no time in making sweeping changes to speed up the pace of sales growth at the company. In short order, he had pushed for initiatives such as more transparent pricing, sales promotions during the holidays, and giving buyers more assurances when they made purchases on Etsy. Silverman also had to undertake a few rounds of lay-offs to sharpen the workforce. Not everything Silverman tried in his early days at Etsy worked. But over the longer run, we think that Etsy’s achievements from 2017 to 2020 – the growth in its business and community, and the excellent Glassdoor ratings seen currently – speak for themselves.

We want to be clear that we think the biggest factor that can affect Etsy’s future growth is its degree of adherence to its mission of keeping commerce human. We have confidence that Silverman will be able to keep the company trucking along this North Star.

4. Revenue streams that are recurring in nature, either through contracts or customer-behaviour

We think that Etsy enjoys a high level of recurring revenue from customer behaviour. There are a number of things we looked at that gave us the thought.

First, the active buyers and active sellers on Etsy’s marketplaces have increased significantly over time, as shown earlier, and are now at an impressive 81.9 million and 4.4 million, respectively. Moreover, the proportion of buyers on Etsy’s marketplaces who are repeat buyers and habitual buyers have also increased over time.

Second, Etsy has respectable user retention numbers. The left chart immediately below shows the retention rates for different cohorts of sellers on the Etsy marketplace. Many Etsy sellers sell products for one year and then do not come back. For example, if we look at the black bar (which is the 2013 seller cohort, meaning active sellers as of 31 December 2013), only slightly more than 50% continued to be active sellers in the second year. But those who remained active sellers mostly continued to do so as around 30% or so of the 2013 cohort continued to be active sellers in the fourth year. The right chart immediately below shows the retention rates for different cohorts of buyers on the Etsy marketplace and it paints the same dynamic as the seller cohorts. Many Etsy buyers (more than 50% for the 2013 to 2017 cohorts) make a purchase in their first year on the marketplace and then do not return. But those who do make an additional purchase in the following year keep doing so in the years ahead, as shown in the relatively low churn after the second year.

Source: Etsy 2020 annual report

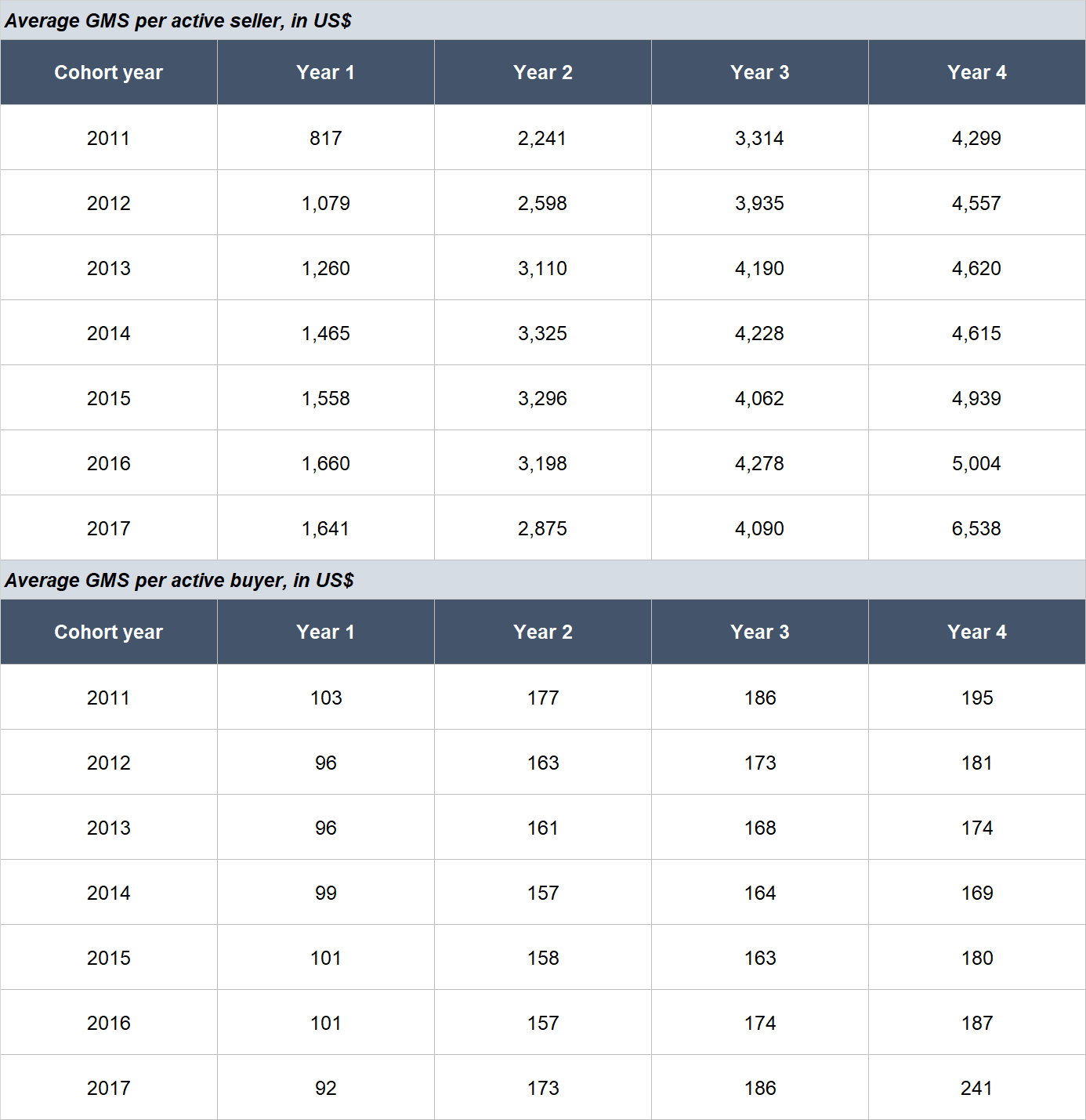

Third, Etsy has very strong dollar retention numbers (as opposed to the user retention numbers above). The table below shows that the average annual GMS per active seller for each seller cohort from 2011 to 2017 had increased significantly over time. It also shows a similar but less pronounced dynamic for the average annual GMS per active buyer for each buyer cohort over the same period.

Source: Etsy annual reports

5. A proven ability to grow

The table below shows Etsy’s key financials from 2012 (the earliest date we could find) to 2020.

Source: Etsy IPO prospectus and annual reports

A few key things to highlight from Etsy’s historical financials:

- Revenue growth from 2012 to 2019 was already outstanding at 40.1% annualised, with 2019’s growth rate coming in at 35.6%. We already mentioned that 2020 was a banner year for Etsy, as COVID-19 drove a shift in consumer behaviour from offline to online shopping and also increased demand for masks significantly. As a result, Etsy’s revenue growth was an astounding 110.9% in 2020.

- 2017 was the first year when Etsy produced positive net income. Since then, Etsy has been consistently profitable, and its net income margin also widened from 18.5% in 2017 to 20.2% in 2020.

- Etsy’s growth in operating cash flow has been outstanding. From 2012 to 2019, operating cash flow was consistently positive and had compounded at 54.9% per year. 2020’s growth was even better at 228.1%.

- Etsy has been generating positive free cash flow since 2014. Moreover, the free cash flow margin (free cash flow as a percentage of revenue) for both 2018 and 2019 were impressive at 23.7% and 23.2%, respectively. The massive jump in operating cash flow in 2020 led to a 253.7% surge in free cash flow during the year, with the free cash flow margin expanding to an excellent 38.9%.

- Etsy has been operating with a conservative balance sheet for the time period we’re looking at (2013 to 2020 – we couldn’t find publicly available balance sheet data for 2012) as the amount of cash and investments outweighed debt in each year.

- There’s no dilution problem at Etsy. We only started looking at the company’s share count in 2015 as it was listed in April of the year. At first glance, Etsy’s share count appears to have increased significantly from 2015 to 2016 (a 24.6% jump). But the number we’re using is the weighted average diluted share count. Right after Etsy got listed in April 2015, it had a share count of around 111 million. This means that the increase in 2016 was much milder at just around 2%. Moreover, from 2016 to 2020, Etsy’s weighted average diluted share count grew by just 4.7% per year, which is much slower than the annual growth in revenue of 47.5%.

6. A high likelihood of generating a strong and growing stream of free cash flow in the future

There are two reasons why we think Etsy excels in this criterion. First, there’s still significant room to grow for the company as we had already discussed. Etsy’s core Etsy marketplace has a strong network of buyers and sellers and we think its network effect – of more buyers leading to more sellers, which leads to more buyers, and so on – is likely to grow stronger and become increasingly difficult to break over time.

Second, Etsy stands out from many other relatively young and fast-growing technology companies in that it already has a great track record in recent years at generating free cash flow. We shared earlier that the company’s free cash flow margins were 23.7%, 23.2%, and 38.9%, in 2018, 2019, and 2020, respectively. We think Etsy can continue to post robust free cash flow margins in the future, since the company’s business is about operating asset-light ecommerce marketplaces.

Valuation

We completed our initial purchases of Etsy shares in early April 2021. Our average purchase price was US$197 per share. At our average price and on the day we completed our purchases, Etsy’s shares had a trailing price-to-free cash flow (P/FCF) ratio of around 40. We like to keep things simple in the valuation process. In Etsy’s case, we think the P/FCF ratio is currently an appropriate metric to gauge the value of the company, since it has already been generating substantial free cash flow for a number of years.

The P/FCF ratio of 40 looks very reasonable to us, since Etsy has both a huge market opportunity and – in our view – a high probability of being able to grow at a rapid clip in the years ahead.

For perspective, Etsy carried a P/FCF ratio of around 42 at its 28 April 2021 share price of US$207.

The risks involved

There are two key risks that we see with our investment in Etsy.

The first is the risk of management losing their way. Etsy has built a solid reputation for itself as the go-to place for (a) artisanal entrepreneurs to showcase their creativity and monetise their passions, and (b) consumers who are seeking thoughtful, creative, and niche products. But Etsy is competing for the attention of sellers with other online marketplaces, commerce channels on social networks, and also service providers that enable small businesses to effectively sell online. Meanwhile, consumers also have an effectively unlimited variety of online shopping venues to choose from. We believe that Etsy needs to remain true to its mission to “Keep Commerce Human” in order to continue to win mindshare among artisanal entrepreneurs and buyers who are looking for unique products from these artisans. If Josh Silverman and his team ever lose sight of Etsy’s mission, then the whole edifice could crumble.

Based on the latest data, Etsy has earmarked its market opportunity for niche and special products to be US$100 billion in 2018. But there’s no guarantee that the actual market opportunity for such products is that big – it could be significantly smaller, and this is the second key risk we see with Etsy. We’ll be watching for tell-tale signs of Etsy approaching saturation in its market. These signs include slow growth in GMS or in the number of buyers and sellers.

Summary and allocation commentary

To sum up, Etsy has all the makings of a long-term compounder. It has:

- A huge and growing market opportunity in the form of commerce activity for special products, and an online marketplace – with an already strong and still-growing network effect – that focuses on such products

- A robust balance sheet that has significantly more cash and investments than debt

- A management team with well-aligned incentives, and a great track record of execution and innovation

- A high level of recurring revenue from customer behaviour

- A strong history of growth in revenue, profit, and free cash flow without any significant dilution to shareholders

- A high chance of producing a growing stream of free cash flow in the future

The company also has a valuation that we find to be very reasonable. But as it is with every company, there are also risks to note, such as the risk of management losing sight of what makes Etsy special, and the possibility of the company’s actual market opportunity being smaller than expected.

After weighing the pros and cons, we decided to initiate a position of around 2.5% in Etsy in April 2021. We appreciate all the strengths we see in Etsy’s business, but our enthusiasm is tempered slightly by the tiny question-mark we have over the company’s runway for growth.

And here’s an important disclaimer: None of the information or analysis presented is intended to form the basis for any offer or recommendation; they are merely our thoughts that we want to share. Of all other companies mentioned in this article, Compounder Fund only owns shares in Etsy. Holdings are subject to change at any time.