Compounder Fund: Portfolio Update (January 2023) - 12 Jan 2023

Jeremy and I intend to share frequent but non-scheduled updates on how Compounder Fund’s portfolio looks like. The last time we shared an update on this was for Compounder Fund’s portfolio as of 20 November 2022.

In it, I mentioned a few things: (a) all 49 holdings that were in the fund’s portfolio; (b) our full sale of Twilio from the fund; and (c) developments with the acquisitions of Activision Blizzard and Pushpay. Since the update, there have been some changes to the portfolio and more changes are – or could be – on the way.

The first change to the portfolio is that we sold all of Compounder Fund’s Pushpay shares in late-December 2022 at an average price of A$1.22 per share. We decided to part ways with Pushpay after we found an attractive redeployment opportunity in Hingham Institution of Savings, a bank that is listed and headquartered in the USA (Compounder Fund’s Hingham shares were bought shortly after Pushpay’s sale). Here’s a brief description of the bank:

- Founded in 1834, the Massachusetts-based Hingham is one of the oldest banks in the USA. It’s also one of the most interesting banks we’ve come across, although it’s not the impressive longevity that caught our eye. Instead, it was Hingham’s remarkable focus. Hingham is led by Robert Gaughen Jr – who has been CEO since 1993 after his father, Robert Gaughen, won a proxy battle in the same year to unseat the bank’s then-leaders after years of mismanagement – and it has an extremely simple business. It does commercial real estate and residential real estate lending, and offers deposit services for businesses and consumers. Even within commercial real estate lending, Hingham focuses on commercially-run properties that are used for residential purposes.

- Under Gaughen Jr’s leadership, Hingham has translated its business-simplicity into excellent long-term results. From 1993 to 2021, Hingham’s book value per share – a key measure of a bank’s intrinsic value – grew in every single year and compounded at 11.8% annually. Over the same period, the bank was also profitable every year and its average return on equity was a respectable 13.9%. Hingham’s profitability in this timeframe is even more noteworthy when considering two things: (1) The bank was – and is – principally engaged with residential-related real estate lending; and (2) the timeframe covers the 2007-09 Great Financial Crisis, a period that saw many American banks suffer financially and US house prices crash. For perspective, while US banks generated returns on equity (ROEs) of 0.7% and -0.7% in 2008 and 2009, Hingham’s ROEs were significantly higher at 11.1% and 12.8%.

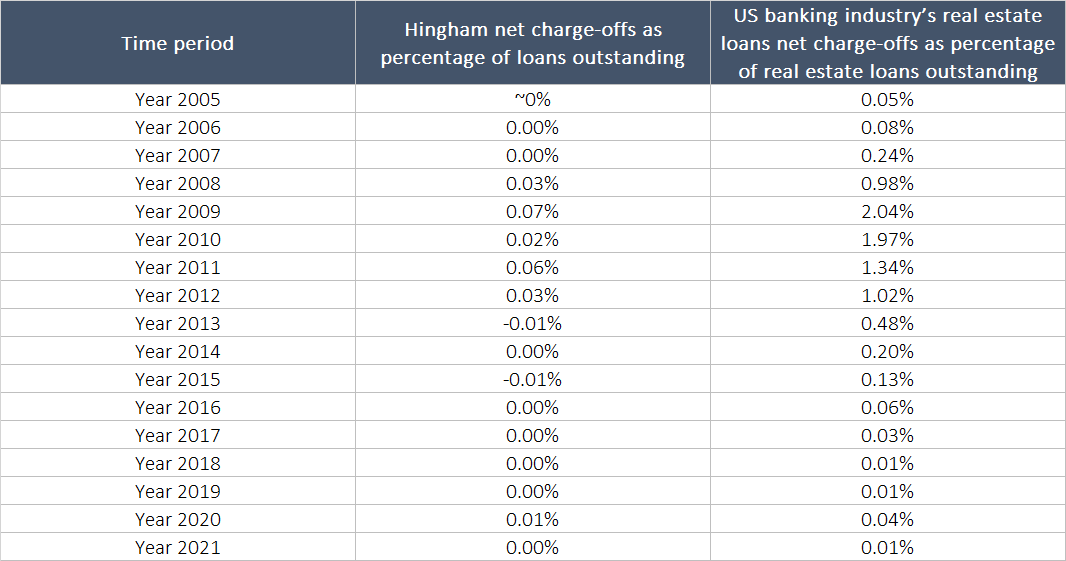

- Hingham’s admirable track record is the result of management’s prudence. For instance, Table 1 demonstrates that Hingham’s net charge-offs (the percentage of outstanding loans that are unlikely to be recovered) have been nearly non-existent since 2005, indicating minimal loan losses for the bank over that time period. Table 1 also shows that Hingham’s net charge-offs are extraordinarily low compared to the net charge-offs for the US banking industry’s real estate loans. In another example, Hingham’s average efficiency ratio from 2016 to 2021 was an impressive 28%, a significantly lower figure compared to the average efficiency ratios over the same timeframe for the US’s five largest banks at the moment: JPMorgan at 58%, Bank of America at 63%, Citigroup at 60%, Wells Fargo at 67%, and US Bancorp at 57%. (The efficiency ratio is a measure of a bank’s profitability and it is calculated by dividing a bank’s operating expenses by its revenue; the lower the ratio, the better.)

- Another aspect of Hingham we’re attracted to is the way it invests in stocks. As of 30 September 2022, Hingham has a portfolio worth US$72.3 million, which is 19% of the bank’s book value. Hingham’s leaders manage the portfolio to “produce superior returns on capital over a longer time horizon,” a trait we have not commonly seen in other banks. What particularly caught our attention was Hingham’s investment process. According to Hingham’s latest annual report, the bank’s leaders focus on businesses “with strong returns on capital, owner-oriented management teams, good reinvestment opportunities or capital discipline, and reasonable valuations.” Management also “views [the holdings] as long-term partnership interests in operating companies.” As far as we can tell, Hingham has not publicly shared details about the composition of its portfolio and its performance. But management’s description of the way they invest still resonates with us because the core of the investment process is about identifying great businesses and patiently holding their shares.

- With total loans of just US$3.56 billion as of 30 September 2022, Hingham has massive room for growth in the USA alone. For context, the US banking industry has total loans of US$12.0 trillion as of 30 September 2022.

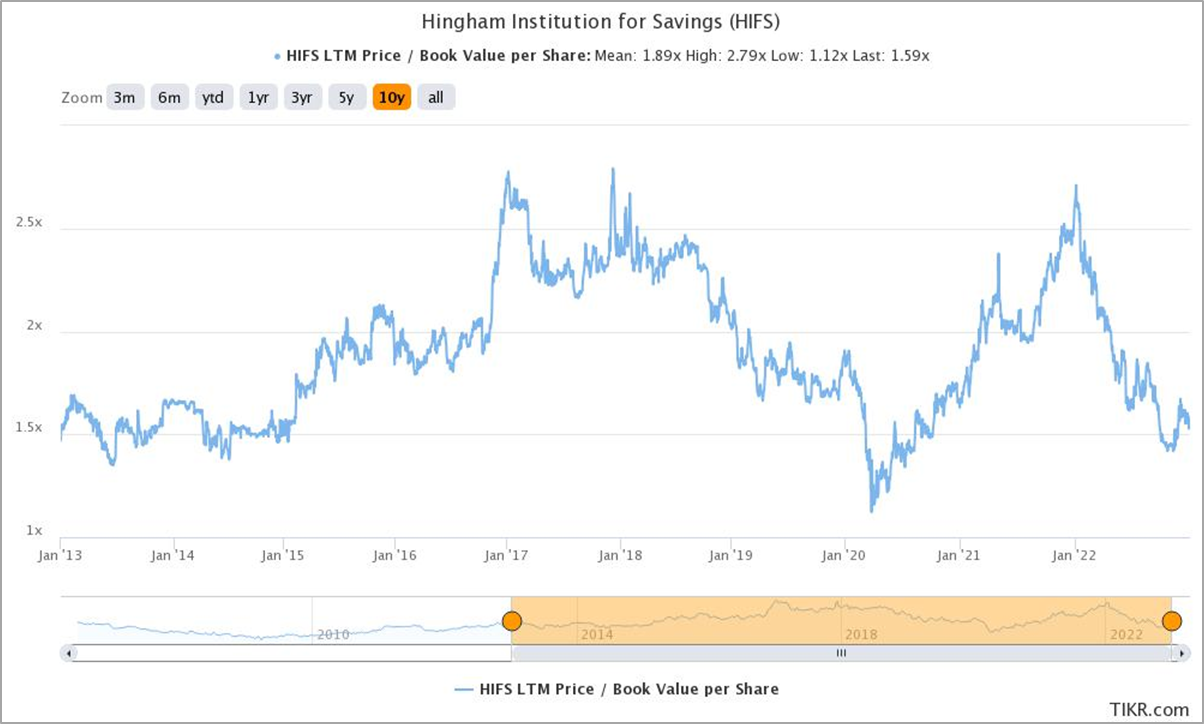

- At our initial purchase price of US$275, Hingham’s shares carried a price-to-book (P/B) ratio of just 1.57. Figure 1 below shows that the P/B ratio of 1.57 is near the low-end of where it has been over the decade ended 2022.

Table 1; Source: Hingham annual reports, and Federal Deposit Insurance Corporation data

Figure 1; Source: Tikr

The second change to Compounder Fund’s portfolio also happened in December 2022 when Haidilao spun off its international operations into a separate entity named Super Hi International, which is listed in Hong Kong (with the ticker symbol “9658”) but headquartered in Singapore. Super Hi’s shares started trading in the Hong Kong stock market on 30 December 2022 and Haidilao shareholders were given one Super Hi share for every 10 Haidilao shares held. Since Compounder Fund owns 43,000 Haidilao shares, the fund received 4,300 Super Hi shares. Jeremy and I have decided for Compounder Fund to hold onto the Super Hi shares because Haidilao’s growth prospects outside of China was also a part of our thesis when we first invested in the company. Here’s a description of Super Hi’s business:

- Haidilao’s international expansion started in 2012 when it opened an outlet in Singapore, its first outside of China. The company steadily grew its international presence over time but accelerated the growth of its international restaurant network only in recent years. For perspective, Super Hi’s restaurant count was 38, 74, and 94, respectively, at the end of 2019, 2020, and 2021. As of 11 December 2022, Super Hi ran 110 restaurants in 11 countries across Asia, North America, Europe, and Oceania (see Table 2 for a precise breakdown). Nearly all of these are Haidilao-branded hotpot restaurants, with just two being other brands. During the first half of 2022, Super Hi earned US$245.8 million in revenue, of which 97.5% came from the company’s restaurants. In the same period, Southeast Asia was the most important geography for Super Hi, accounting for 68.0% of total revenue; North America, East Asia, and Others took up the remaining share at 12.2%, 10.6%, and 9.2%, respectively.

- According to Super Hi’s listing prospectus, Chinese cuisine restaurants can be found in over 130 countries. As of 2021, there were more than 600,000 Chinese cuisine restaurants outside of China, of which 134,000 are hotpot restaurants. These hotpot restaurants’ revenue in 2021 was US$28.9 billion; in 2019, prior to the emergence of COVID-19, the global hotpot restaurant market, excluding China’s, was US$37.3 billion. These numbers dwarf Super Hi’s current restaurant count (110) and revenue (US$423.4 million in the 12 months ended 30 June 2022), and suggest a long growth-runway for the company. Super Hi’s market opportunity looks even better if the entire Chinese cuisine restaurant market, excluding China’s, is considered; in 2021 and 2019, Chinese cuisine restaurants outside of China generated revenue of US$261.1 billion and US$334.3 billion, respectively.

- Zhou Zhaocheng, 49, is Super Hi’s CEO and he first joined Haidilao, as chief strategy officer, in April 2018. We appreciate the fact that Zhou already has a few years of experience as a senior leader of Haidilao. But the command of Super Hi ultimately rests in the hands of Haidilao’s co-founders, the husband and wife team of Zhang Yong and Shu Ping. The couple are majority shareholders of Super Hi and they currently control more than 54% of the company’s shares.

- When Jeremy and I first invested in Haidilao, we were – and still are – attracted to its unique corporate culture. For example, Haidilao’s management team leads the company with kindness in mind; nearly all of the company’s restaurant managers started in non-managerial positions and steadily rose through the ranks; restaurant managers get to share in the profits of the restaurants that they and their first- and second-generation mentees manage; and employees are given service-autonomy within the company’s restaurants to delight customers. Given Super Hi’s current link with Zhang Yong and the fact that it was spun out of Haidilao, we were not surprised to learn that Haidilao’s unique cultural traits are found in Super Hi too.

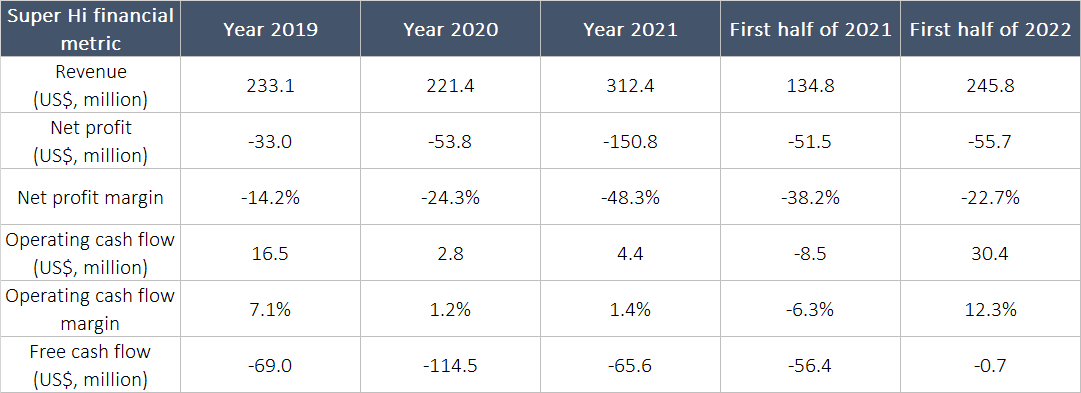

- The earliest financials we have for Super Hi go back to only 2019. In that year, the company experienced a loss because new restaurants accounted for a large portion of its total restaurant count (for perspective, Super Hi expanded into six new countries – Australia, Indonesia, Malaysia, Thailand, the UK, and Vietnam – in 2019). Since then, Super Hi’s business results have been hurt by COVID-19. In 2020 and 2021, all of Super Hi’s restaurants were subjected to some form of COVID-19 restrictions. But in 2022 – especially since June – the situation has improved for Super Hi, as COVID-19 gradually came under control in its geographies. Table 3 below shows Super Hi’s revenue, net profit, operating cash flow, and free cash flow from 2019 to the first half of 2022.

- Super Hi’s recent poor financial results is not entirely COVID-19’s fault – the company also suffered from self-inflicted wounds. But the good thing is management is in the midst of rectifying the problems. In the “Portfolio management thoughts: Haidilao’s Starbucks moment” section of Compounder Fund’s 2021 fourth-quarter letter, I discussed Haidilao’s mistake of expanding its restaurant network too quickly in 2020 and 2021 and the company’s measures – introduced in November 2021 – to improve the operating performance of its business. These measures include slowing down the pace of restaurant openings and changing the way the company’s restaurants are managed, and they delivered positive results for Haidilao in the first half of 2022. Super Hi had implemented similar measures while new ones were also introduced throughout 2022 – collectively, they’ve led to improvements in Super Hi’s operations. As of 11 December 2022, Super Hi only had four restaurants that had yet to achieve initial monthly breakeven, and only three of them had been in operation for more than six months.

Table 2; Source: Super Hi listing prospectus

Table 3; Source: Super Hi listing prospectus

One change to Compounder Fund’s portfolio that would happen in the near future involves Tencent and Meituan. Tencent announced in November 2021 that it will distribute 90.9% of its Meituan stake to its shareholders. Tencent shareholders will receive 1 Meituan share for every 10 Tencent shares that they own in March this year. Compounder Fund owns 5,600 Tencent shares, so it will become a direct owner of an additional 560 Meituan shares soon. Compounder Fund has been a shareholder of Meituan since July 2020 and Jeremy and I intend for Compounder Fund to retain its ownership of the distributed Meituan shares. Tencent’s latest corporate action with Meituan is its second major disposition of shares – following the distribution of JD.com shares in the first quarter of 2022 – from its massive portfolio of investments (worth US$123 billion as of 30 September 2022). In a January 2022 update on the portfolio, I discussed the JD.com distribution and our thoughts on its implications on our Tencent investment:

“We have no insight on the actual motivation of Tencent’s management behind this distribution. From our vantage point, there are three possible reasons for the move: (1) it is driven by the wishes of the Chinese government to reduce Tencent’s sway in China’s technology sector; (2) it is an isolated manoeuvre by Tencent’s management to unlock value from the company’s JD.com shares after first making the investment more than seven years ago in 2014; and (3) it is the start of a coherent strategy by Tencent’s management to unlock the value of the company’s massive portfolio of investments.

Implications that come with the first reason: If true, this would be troubling. Tencent could be forced in the future to offload or spin off its investment portfolio in ways that are harmful for its shareholders – for example, Tencent could be pushed to sell a minority investment when its stock price is temporarily depressed. In the “Investing thoughts: Investing in China” section of Compounder Fund’s 2021 third-quarter letter, I discussed the recent flurry of regulatory changes to China’s business landscape and how Jeremy and I can’t tell what the key intention of the Chinese government is behind these changes (one of the possible intentions I brought up is the Chinese government’s desire to consolidate power). Tencent’s distribution of its JD.com shares could be related to the regulatory changes that were discussed in our 2021 third-quarter letter. We will be watching developments with Tencent’s investment portfolio as it could contain clues on how the Chinese government thinks about the country’s large private-sector companies.

Implications that come with the second reason: If true, then there’s nothing to see here.

Implications that come with the third reason: If true, we see it as a positive development for our Tencent investment. Large conglomerates often carry a “holding discount,” where the sum of the intrinsic values of each of a conglomerate’s various holdings outweighs the conglomerate’s overall market capitalisation. It’s possible that the market is applying a holding discount to Tencent’s investment portfolio. Coherent attempts by Tencent to unlock the value of its portfolio of investments should do no harm to its core businesses’ growth, in our opinion. So it’s a move that would be neutral at-worst or positive at-best. We like these odds.

All told, we can’t tell which possible reason is true. There may even be a combination of any two of the reasons in Tencent’s decision to distribute its JD.com shares. We’re adopting a watch-and-learn stance with Tencent. There’s still much to like about its core businesses (WeChat and digital gaming) and relatively nascent businesses (such as cloud computing), and this is why it still has a place in Compounder Fund’s portfolio.”

With this latest development involving Meituan, we can rule out the second reason from the three mentioned above. It remains to be seen whether the first or third reason is the dominant factor behind Tencent’s distributions of its JD.com and/or Meituan shares. So we’re still in “watch-and-learn” mode with Tencent and its future plans for its investment portfolio.

Finally, a potential change that could happen to Compounder Fund’s portfolio in the near future is Microsoft’s pending acquisition of Activision. There was a material development that happened in early-December: The US FTC (Federal Trade Commission) had challenged the deal. But Activision’s CEO Bobby Kotick published a brief public letter shortly after the FTC’s announcement and reiterated his belief that the acquisition would cross the finish-line:

“I wanted to provide a brief update on our pending merger with Microsoft. This week the U.S. Federal Trade Commission (FTC) announced its decision to challenge the deal. This means they will file a lawsuit to block the merger, and arguments will be heard by a judge. This sounds alarming, so I want to reinforce my confidence that this deal will close. The allegation that this deal is anti-competitive doesn’t align with the facts, and we believe we’ll win this challenge.”

We don’t have any special insights on the FTC’s thought process so we’re watching how the situation unfolds. As first discussed in Compounder Fund’s April 2022 portfolio update, Jeremy and I intend for the fund to hold onto its Activision shares and receive the cash from Microsoft if and once the acquisition is completed (but our intention could change depending on developments at both companies and the stock market in general).

Compounder Fund is able to accept new subscriptions once every quarter with a dealing date that falls on the first business day of each calendar quarter. In the middle of December 2022, Jeremy and I successfully closed Compounder Fund’s ninth subscription window since its initial offering period (which ended on 13 July 2020) and raised a net amount of S$0.03 million. This new capital was deployed quickly in the days after the last subscription window’s dealing date of 2 January 2023 and we added to Compounder Fund’s Adyen position.

In Compounder Fund’s Owner’s Manual, we mentioned that “if Compounder Fund receives new capital from investors, our preference when deploying the capital is to add to our winners and/or invest in new ideas.” We added to Adyen at a stock price of €1,300, which is significantly lower than our initial average purchase price of €1,871 per share. But the company has continued to execute well since our first investment in early-April last year so it has been a winner, according to our definition. In the first half of 2022, Adyen’s net revenue jumped 36.7% year-on-year to €608.5 million and its free cash flow was up 25.4% to €308.9 million. The free cash flow margin, while lower than the 55.4% seen a year ago, remained excellent at 50.8%. Adyen’s lower stock price helped improve its price-to-free cash flow (P/FCF) ratio from 101 at our initial investment to 64 when we added to the position earlier this month.

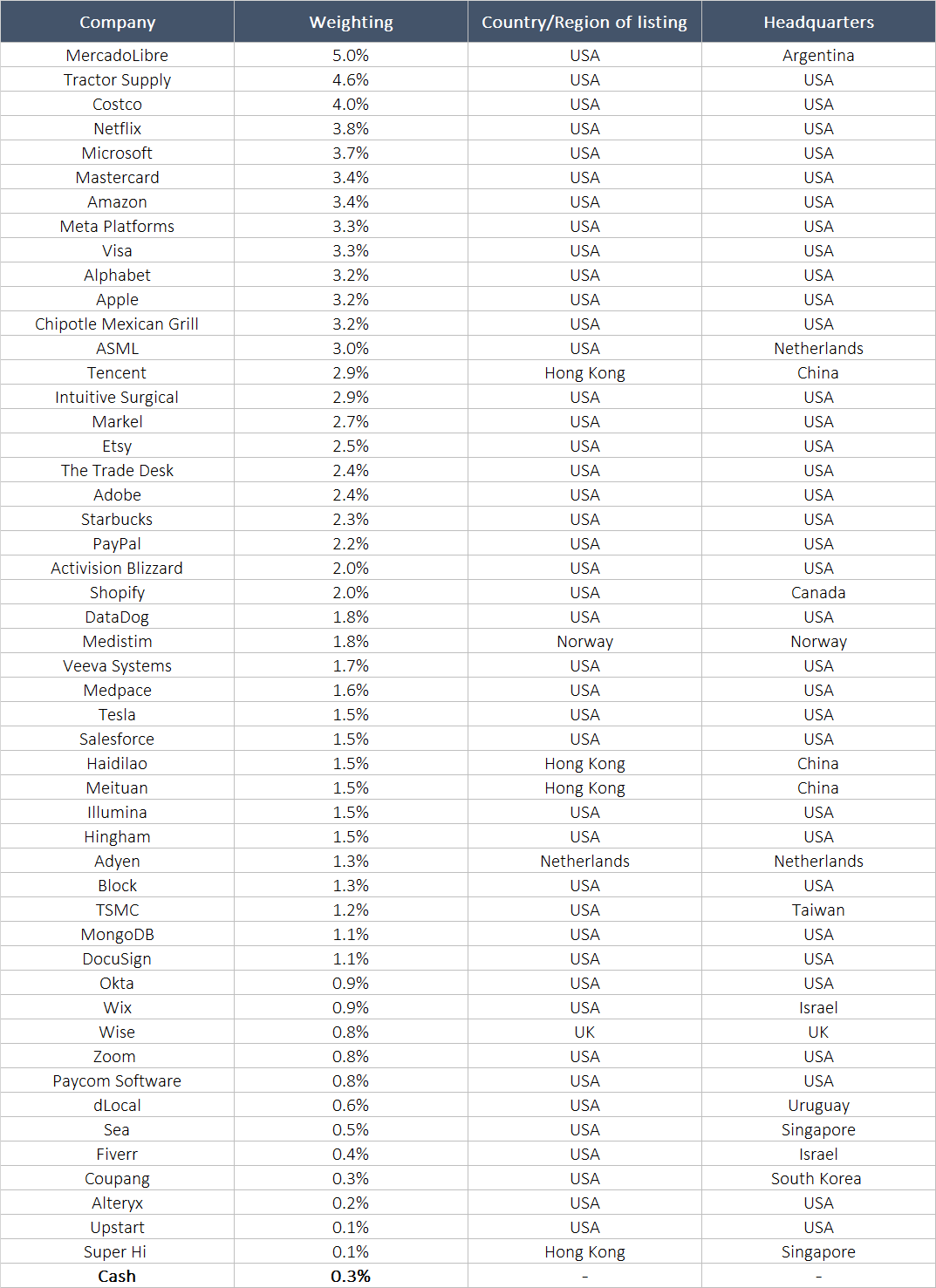

Here’s how Compounder Fund’s portfolio of 50 companies looks like as of 9 January 2023:

We’re sharing all this information with the public and with the fund’s investors for two reasons. First, we believe deeply in investor education and want Compounder Fund’s return and actions to be a source for people to learn about investing. Second, we believe that this transparency will help investors of Compounder Fund develop comfort with our investing process over time, which is great; in turn, this will also free us from the time-consuming activity of dealing with questions on how we invest, and thus give us more to invest better for our investors.

And here’s an important disclaimer: None of the information or analysis presented is intended to form the basis for any offer or recommendation; they are merely our thoughts that we want to share. Holdings are subject to change at any time.