Compounder Fund: Portfolio Update (August 2024) - 20 Aug 2024

Jeremy and I intend to share frequent but non-scheduled updates on how Compounder Fund’s portfolio looks like. The last time we shared an update on this was in our 2024 second-quarter letter and it was for Compounder Fund’s portfolio as of 07 July 2024. In it, I shared all 45 holdings in the fund’s portfolio.

Since then, we have trimmed the fund’s holdings in Costco, Intuitive Surgical, and Starbucks to add to Amazon and Meta Platforms. Some of the cash from the trimming was also used to invest in a new company for Compounder Fund, namely, Cassava Sciences. These actions were all made in early-August 2024. Our full-thesis for Cassava Sciences can be found here, but the following are a few quick words on the company:

- We invested in Cassava Sciences because we believe it’s currently undergoing a special situation that provides a highly asymmetric risk/reward profile. The clinical-stage biotechnology company has no revenue at the moment and its main therapeutic drug candidate, simufilam, is currently undergoing US FDA (Food & Drug Administration) Phase III clinical trials for the treatment of Alzheimer’s disease.

- The development process of simufilam has been – and still is – mired in controversy, but data from the drug’s Phase II trials are very promising in our view. Moreover, the FDA has allowed simufilam’s trials to carry on, despite the surrounding controversy.

- If simufilam successfully clears its ongoing Phase III trials, we believe Cassava Sciences has the potential to generate a multi-fold return on our investment in a relatively short span of time. If simufilam fails the trials, the company will effectively have zero value. We like the odds of simufilam clearing its Phase III trials and being approved by the FDA for commercialisation but there’s no guarantee. We have thus sized the position in Cassava Sciences accordingly.

The trimmings of Costco and Intuitive Surgical were done for valuation reasons. In our 2024 first-quarter and second-quarter letters, I wrote the following on Costco:

“[2024 first-quarter letter] Costco, the membership-based warehouse retail giant, has been consistently growing its membership count and putting up high membership renewal rates of at least 90%, in addition to posting positive revenue growth and same-store sales growth, over the same period…

…As for Costco, management gave a good description of the company’s long runway for growth in its 2023 fourth-quarter earnings conference call (emphases are mine):

“But what’s interesting is we have a lot more runway than we ever thought possible. If you had asked us 5 years ago, by now, how many would we be putting in this year in the U.S., we would not have said 20-plus. It’s got to slow down at some point. But the volumes that we’re now doing in these locations, we’ve got to bleed some of that off. And so that’s one good point. And then we still got plenty of going on overseas. And you’ll see that continue to ramp up as well…

… If you announced this 10 years ago, will you ever have 150 of your 600 U.S. locations doing over [US]$300 million and 40 of them doing over [US]$400 million? The answer would be no, no way, even with inflation. The fact is we’re doing a lot more volume than we’ve ever thought we would do. And so the biggest answer of not only making it a little more efficient but driving more sales is cannibalizing. We find existing members that sometimes will say, “I don’t want to go there. It’s too busy today.” And by opening up that third or fourth unit in that city, we’re seeing not an increase by 1/3 or 1/4 of the membership base but a significant increase in sales.”

[2024 second-quarter letter] I mentioned in our 2024 first-quarter letter that we’re “still really positive on the future growth potential of Chipotle and Costco’s businesses” but that they “ended March 2024 with high price-to-earnings ratios of 66 and 48, and high price-to-free cash flow ratios of 66 and 53, respectively.” Both conditions still hold true.. As for Costco, same-store sales growth of 6.6% for the same quarter drove a 9.1% revenue increase, leading to a 29.0% jump in diluted earnings per share (or growth of 10.2%, excluding one-off charges in the year-ago quarter). At the end of June 2024, Chipotle’s price-to-earnings and price-to-free cash flow ratios were 67 and 65, respectively, while Costco’s were 52 and 51.”

Our thinking on retail giant Costco’s positive growth prospects has not changed while its valuation remains elevated. When we trimmed Costco, its price-to-earnings (P/E) ratio was 50 while its price-to-free cash flow (P/FCF) ratio was 48.

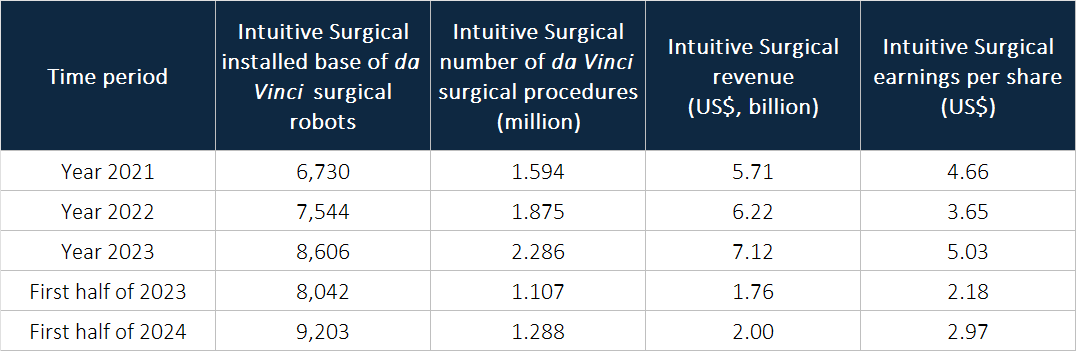

As for Intuitive Surgical, the trailblazer in surgical robots, its customers are at the cusp of starting a major upgrade cycle. wThe company’s fifth-generation of its flagship da Vinci surgical robot system was cleared by the FDA in March 2024. Early customer-feedback on the da Vinci 5 points to “improvements in precision, imaging, ergonomics and integration,” and these have “led to overall efficiency improvements.” The new Force Feedback feature in the da Vinci 5 also shortens the learning curve for surgeons and could potentially help improve patient outcomes by allowing surgeons to apply less force on tissue during surgeries. The company has also consistently grown the installed base of its systems, the number of surgical procedures performed with its systems, its revenue, and its earnings per share in the past few years, as shown in Table 1 below.

Table 1; Source: Intuitive Surgical regulatory filings

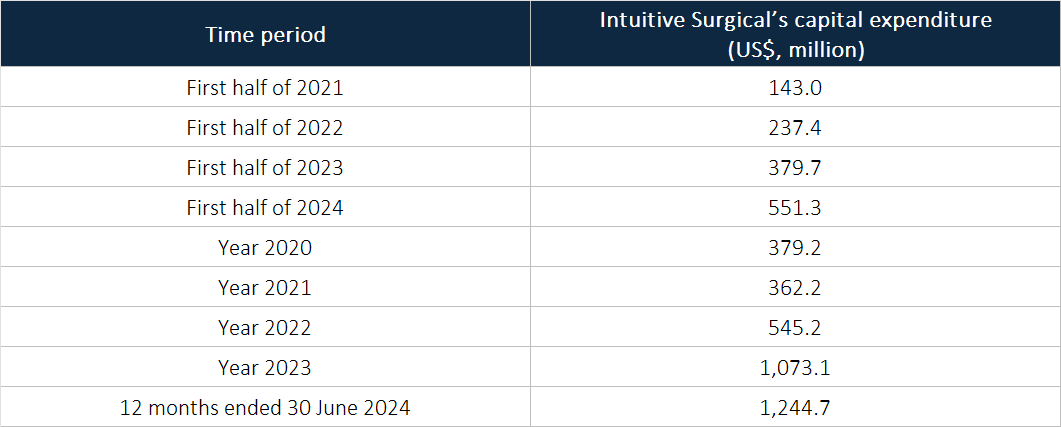

We have confidence in Intuitive Surgical’s ability to grow its business at a healthy rate in the coming years, but its P/E ratio is also really high – it was at 75 when we trimmed the position. Intuitive Surgical’s P/FCF ratio was also really high at the same point in time (377), but it was not a meaningful valuation measure. This is because the company’s free cash flow is currently depressed as a result of materially higher capital expenditures, on a temporary basis, in preparation for the future ramp up of the da Vinci 5. Table 2 below shows Intuitive Surgical’s capital expenditures in the recent past for context.

Table 2; Source: Intuitive Surgical regulatory filings

The high valuations of Costco and Intuitive Surgical made us think they were good candidates to trim when we needed capital for additions to Compounder Fund’s existing positions in Amazon and Meta Platforms, and the new investment in Cassava Sciences.

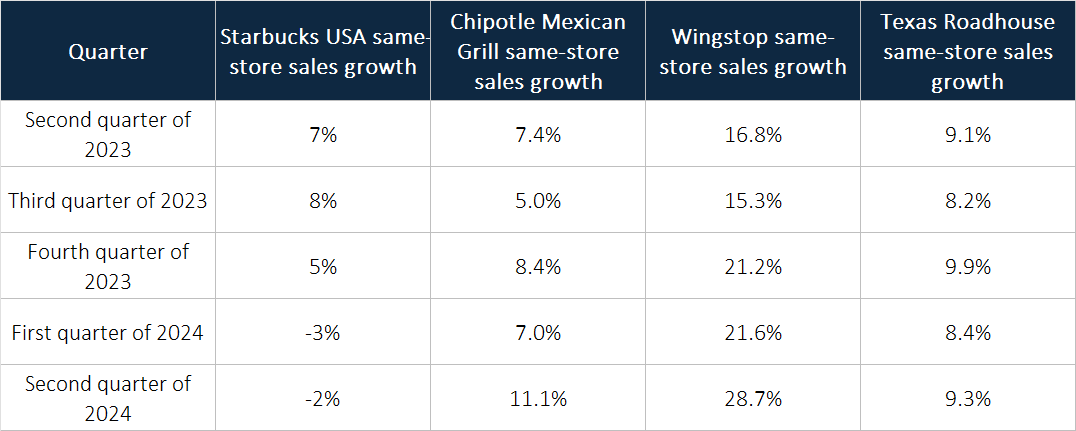

Coming to the coffee-chain giant Starbucks, we thought Laxman Narasimhan’s tenure as CEO has been lacklustre. He joined the company in October 2022 as its would-be CEO and officially assumed the role in April 2023. Starbucks’ same-store sales growth, an important measure of how fast the company’s existing stores are growing, has been trending downwards and has in fact been negative in the past two quarters, as Table 3 illustrates. Meanwhile, Table 3 also shows that there are US-focused food & beverage retail companies – including another Compounder Fund holding, Chipotle Mexican Grill – with healthy same-store sales growth in the same periods when Starbucks’ was declining and negative. This suggests that operational issues at Starbucks are playing a much bigger role in the company’s weak same-store sales growth when compared to macroeconomic issues. But during Starbucks’ 2024 second-quarter earnings conference call, when an analyst asked about the 6% year-on-year decline in traffic in its US stores (the 6% traffic decline was partially offset by a 4% increase in the average order size during the quarter to produce the -2% US same-store sales growth), Narasimhan suggested that challenges consumers were facing was at fault:

“[Question] I think you guys mentioned that traffic was down 6% in the U.S., and the majority of that was due to the non-Rewards customers, which makes up, call it, 40% of your business. That’s a pretty substantial decline in that customer base, by a double-digit decline in that customer base. So can you just talk a little bit about where you think these customers are going?

[Answer] So first of all, I think we are operating in a challenging consumer environment. You see the impact of that in away-from-home consumption. If you look at our business at home, the grocery stores with our brands, you’re seeing volume increase. You’re seeing share increase in a category that’s in decline, but we see volume increase at home. In our ready-to-drink business, we’re seeing clearly that they had some challenges. But with the work that our joint venture team is doing, we’re seeing progress there. But away-from-home consumption, you see the impact of the challenging consumer environment.”

Table 3; Source: Companies’ quarterly earnings updates

Starbucks made a surprise announcement on 13 August 2024 (around a week after we trimmed the position) that Narasimhan would be stepping down from his role on the same day and that Chipotle’s CEO, Brian Niccol, would be joining the company on 9 September 2024 to assume the vacant chief executive role. In our Chipotle thesis, we mentioned that “in all, we give Niccol an A-plus for his time at Chipotle so far” and our opinion on his work with the company has not changed. He has executed brilliantly at Chipotle and we look forward to observing the changes he’ll be implementing at Starbucks. We’re not thrilled that Chipotle has lost Niccol’s leadership, but we’re optimistic that the company will still be in good hands. Even as Chipotle searches for a new permanent CEO, Scott Boatwright, the company’s Chief Operating Officer, has been named as interim CEO. Boatwright, 51, joined the company in 2017, a year before Niccol came onboard as CEO, and has been responsible for implementing Chipotle’s strategic initiatives. Boatwright will be assisted by Chipotle’s long-time CFO, Jack Hartung, whose initial plans to retire from the company in 2025 have been shelved indefinitely.

As for the additions to Amazon and Meta Platforms, they were done primarily because the two companies have excelled with their recent business results and their valuations look attractive to us.

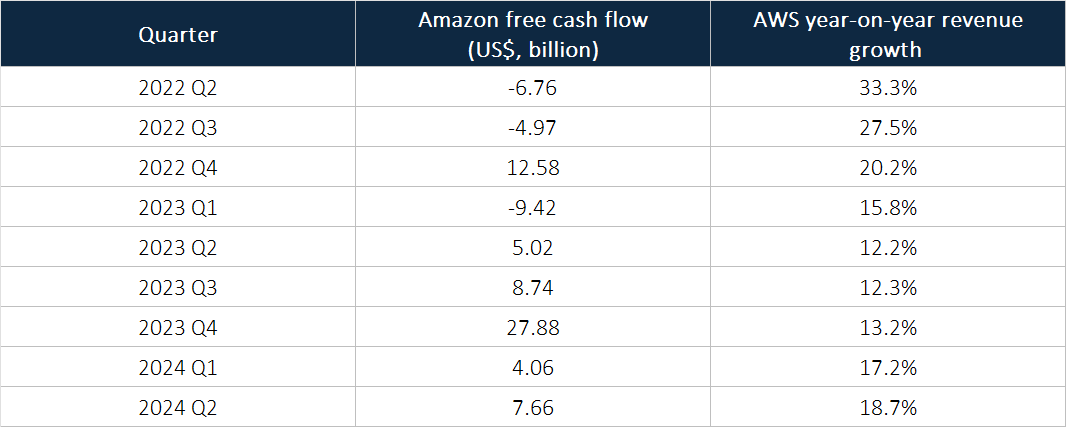

In the case of Amazon, the e-commerce and cloud computing juggernaut, its free cash flow has surged in recent quarters while the year-on-year revenue growth rates at AWS, its cloud-computing arm, has accelerated, as shown in Table 4.

Table 4; Source: Amazon quarterly earnings updates

At the time of our addition, Amazon was trading at a P/FCF ratio of 36. We see continued healthy revenue growth at the company in the coming years, driven by the massive tailwinds present in the e-commerce and cloud computing markets, and a clear path toward higher FCF margins. On margins, management has commented in the past few earnings conference calls that there’s room to continue growing Amazon’s operating margins in the e-commerce business, which would flow through to its overall free cash flow margin. On the tailwinds, e-commerce was still just 15.9% of total retail sales in the USA in the first quarter of 2024 while around 90% of global IT (information technology) spending today is still for on-premise technologies. The latter suggests significant room for further migration of IT spending towards the cloud. Moreover, if and when AI applications become ubiquitous, Amazon’s CEO Andy Jassy thinks that these applications will be built on the cloud from the start. AWS is likely to be a major beneficiary of these trends in our view. In the first quarter of 2024, AWS saw more absolute-dollar sequential growth in revenue than any other cloud provider and during the second-quarter earnings conference call, Jassy revealed that AWS is innovating in AI at a rapid pace:

“During the past 18 months, AWS has launched more than twice as many machine learning and generative AI features into general availability than all the other major cloud providers combined.”

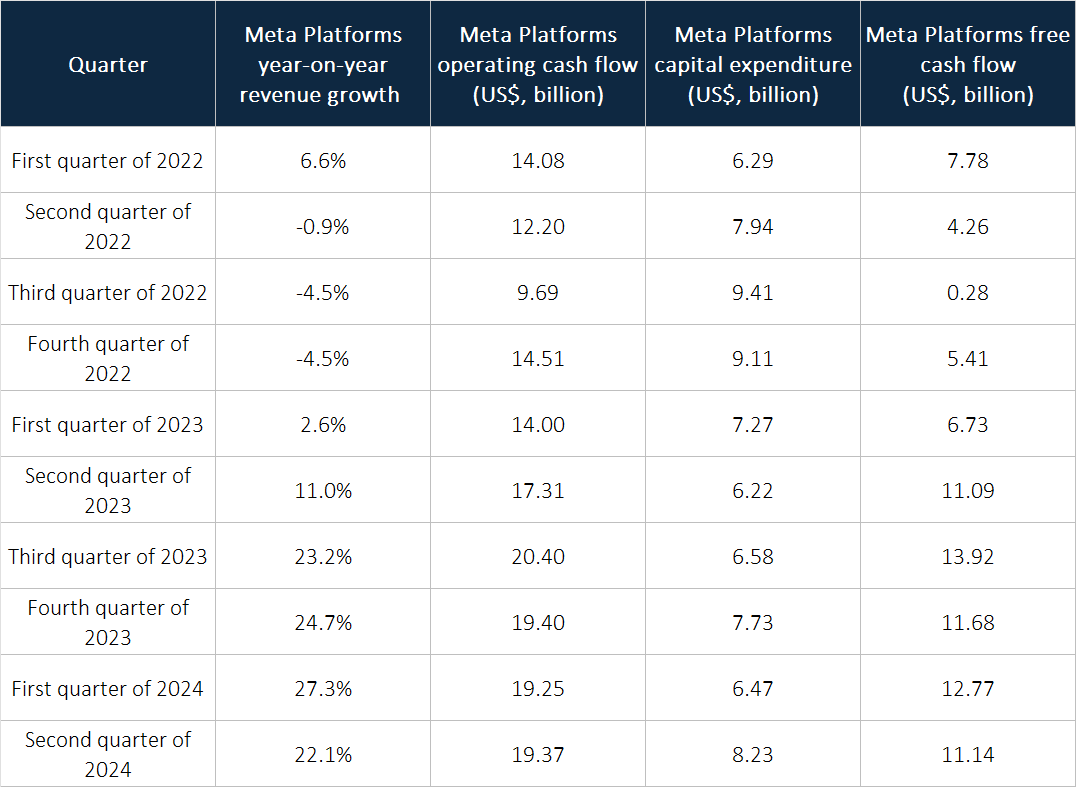

Meanwhile, social media titan Meta Platforms has clearly shown that it has overcome the difficulties its digital advertising business faced in 2022 because of Apple’s changes in its privacy policies. Moreover, the company’s ability to generate free cash flow, which was also called into question by market participants in 2022, is clearly intact, even as CEO and co-founder, Mark Zuckerberg, is driving enormous amounts of capital expenditure into the company’s AI-related infrastructure. Zuckerberg and his team expects Meta Platforms’ capital expenditure for 2024 to be between US$37 billion and US$40 billion and for 2025 to show “significant… growth.” Table 5 below shows Meta Platforms’ quarterly revenue growth, operating cash flow, capital expenditure, and free cash flow, since the first quarter of 2022:

Table 5; Source: Meta Platforms quarterly earnings updates

Meta’s AI-related investments have already delivered clear improvements in the company’s core advertising business. The company’s advertising services are infused with AI features that are undergirded by its state-of-the-art Llama family of foundation models and they not only help advertisers automate their workflows, but also drive better advertising targeting and measurement, and higher user engagement on Facebook and Instagram. Management reported in the 2024 second-quarter earnings conference call that users of the company’s AI-powered Advantage+ shopping campaigns product are enjoying a 22% higher return on advertising spending. Meta’s AI-related investments are also opening up new, potentially huge future revenue streams. For example:

- The Ray-Ban Meta smart glasses, which are embedded with Meta AI, the company’s AI assistant feature, have seen demand outpace supply.

- Meta AI has already answered billions of queries since its introduction around a year ago and it’s on track to be the most-used AI assistant globally by the end of this year.

- Meta launched AI Studio in July this year and it lets anybody create AIs for people to interact with across Meta’s family of social media and communication apps. In particular, Zuckerberg thinks that nearly all businesses in the world could benefit from having an AI agent that their customers can interact with as it improves customer-engagement; businesses used to endure high costs when engaging with customers in messaging but this is where AI agents can help dramatically reduce costs.

At the time of our addition, Meta Platforms’ shares had trailing P/E and P/FCF ratios of just 25 and 26, respectively.

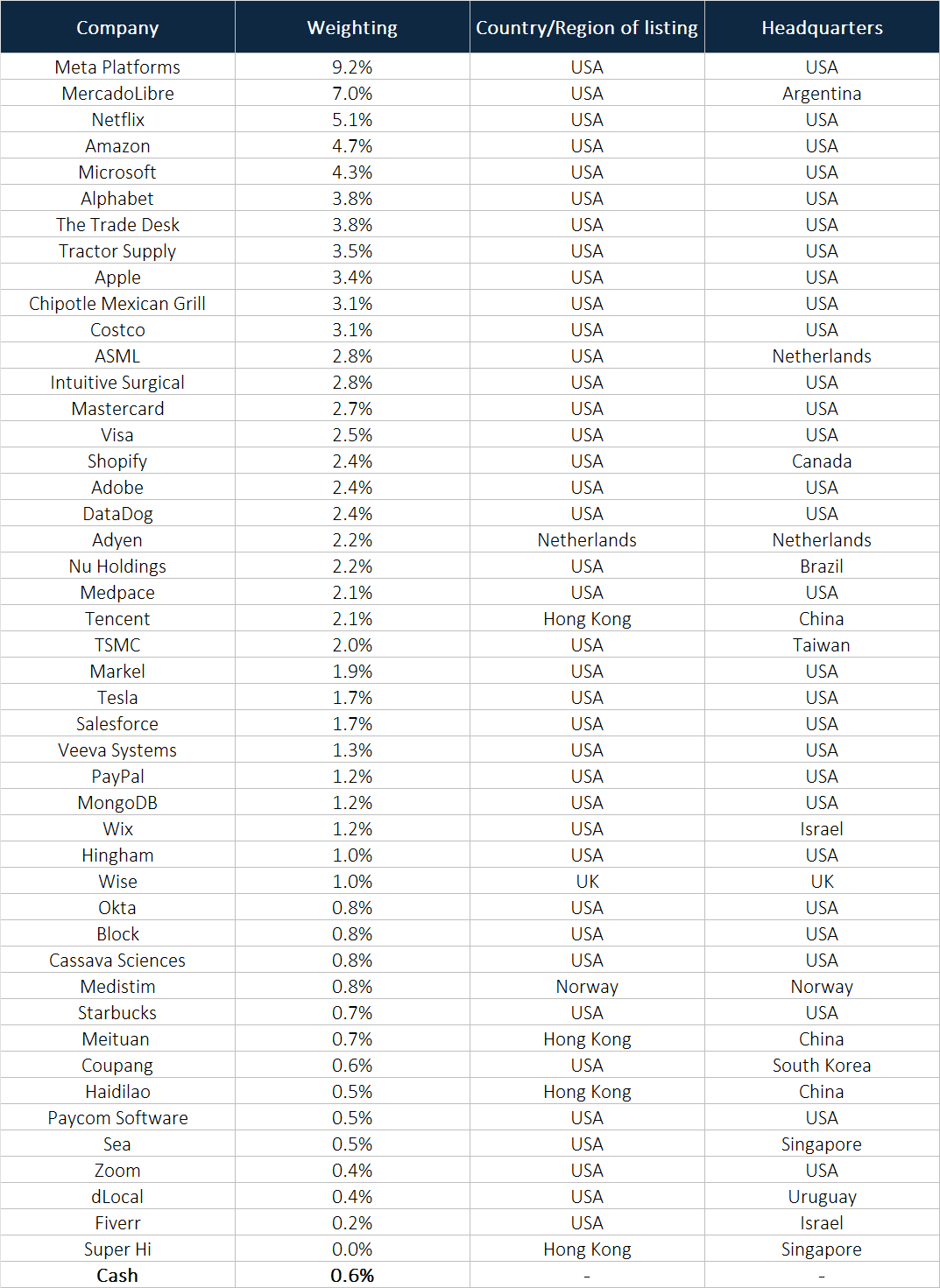

Here’s how Compounder Fund’s portfolio of 46 companies looks like as of 19 August 2024:

Table 6

We’re sharing all this information with the public and with the fund’s investors for two reasons. First, we believe deeply in investor education and want Compounder Fund’s return and actions to be a source for people to learn about investing. Second, we believe that this transparency will help investors of Compounder Fund develop comfort with our investing process over time, which is great; in turn, this will also free us from the time-consuming activity of dealing with questions on how we invest, and thus give us more to invest better for our investors.

And here’s an important disclaimer: None of the information or analysis presented is intended to form the basis for any offer or recommendation; they are merely our thoughts that we want to share. Holdings are subject to change at any time.