Compounder Fund: Intuitive Surgical Investment Thesis - 21 Aug 2020

Data as of 19 August 2020

Intuitive Surgical (NASDAQ: ISRG) is one of the 40 companies in Compounder Fund’s initial portfolio. This article describes our investment thesis for the company.

Company description

In recent years, there have been news reports on the da Vinci robotic surgical systems being used in some of Singapore’s major hospitals. The da Vinci systems are the handiwork of Intuitive Surgical, a company that is based and listed in the US.

Founded in 1995, Intuitive Surgical is a pioneer in robotic surgical systems. Today, the company primarily manufactures and sells its da Vinci family of robot systems and related instruments and accessories. The robots are used by surgeons around the world to perform minimally invasive surgical procedures across a variety of surgical specialties, including general surgery, urologic, gynecologic, cardiothoracic, and head and neck.

The da Vinci system, which costs between US$500,000 and US$2.5 million each depending on the model and geography, acts as an extension of a surgeon’s hands – surgeons operate the system through a console that is situated near a robot. But it is more than just an extension. The da Vinci system is tremor free, has a range of motion analogous to the human wrist, and has the ability to move at smaller length-scales with greater precision.

The US is currently Intuitive Surgical’s largest geographical market, accounting for 70% of the company’s US$4.48 billion in total revenue in 2019.

Investment thesis

We have laid out our investment framework in Compounder Fund’s website. We will use the framework to describe our investment thesis for Intuitive Surgical.

1. Revenues that are small in relation to a large and/or growing market, or revenues that are large in a fast-growing market

Intuitive Surgical is a great example of a company with revenue that is large in a fast-growing market. In 2019, the company’s revenue of US$4.48 billion accounted for a significant share of the global surgical robot market; according to Mordor Intelligence, the market was US$4.97 billion then. Mordor Intelligence also expects the market to compound at nearly 22% per year from 2020 to 2025.

We believe the projection for high growth in the global robotic surgical market is sound for two key reasons.

First, minimally invasive surgeries lead to better patient outcomes as compared to open surgery, such as lesser pain, faster post-surgery recovery, and lesser scarring. The da Vinci system is used to perform minimally invasive surgeries. Furthermore, the system “combines the benefits of minimally invasive surgery for patients with the ease of use, precision, and dexterity of open surgery.” We think these traits are likely to lead to long-term growth in demand for surgical robot systems from both patients and surgeons. As of 2019, there are over 21,000 peer-reviewed medical research papers published on Intuitive Surgical’s robotic surgery systems.

Second, of the 50-plus million surgeries performed each year across the world, just 2% are conducted with robots, according to a September 2019 investor presentation from medical device company Medtronic. Even in the US, which is Intuitive Surgical’s main market, only 10% of surgical procedures involve the use of robots. These data suggest that surgical robots have yet to make their way into the vast majority of surgical theatres across the globe.

The current COVID-19 pandemic has caused operational difficulties for hospitals around the world, causing elective surgical procedures to be deferred and pressuring hospitals’ capital spending. This has interrupted the growth of the robotic surgery market, as reflected by Intuitive Surgical’s 5.8% decline in revenue in the first half of 2020 compared to a year ago. But we see COVID-19 as merely a bump in the road for robotic surgery because we believe that (a) a majority of the delayed-procedures eventually need to be conducted, and (b) the advantages of robotic surgery over traditional methods remain intact even in the face of the pandemic.

2. A strong balance sheet with minimal or a reasonable amount of debt

Intuitive Surgical has a formidable balance sheet, with US$4.49 billion in cash, short-term investments, and long-term investments against zero debt (as of 30 June 2020).

Another big plus-point is that the company has been stellar at producing free cash flow over the years. We’ll discuss this soon.

3. A management team with integrity, capability, and an innovative mindset

On integrity

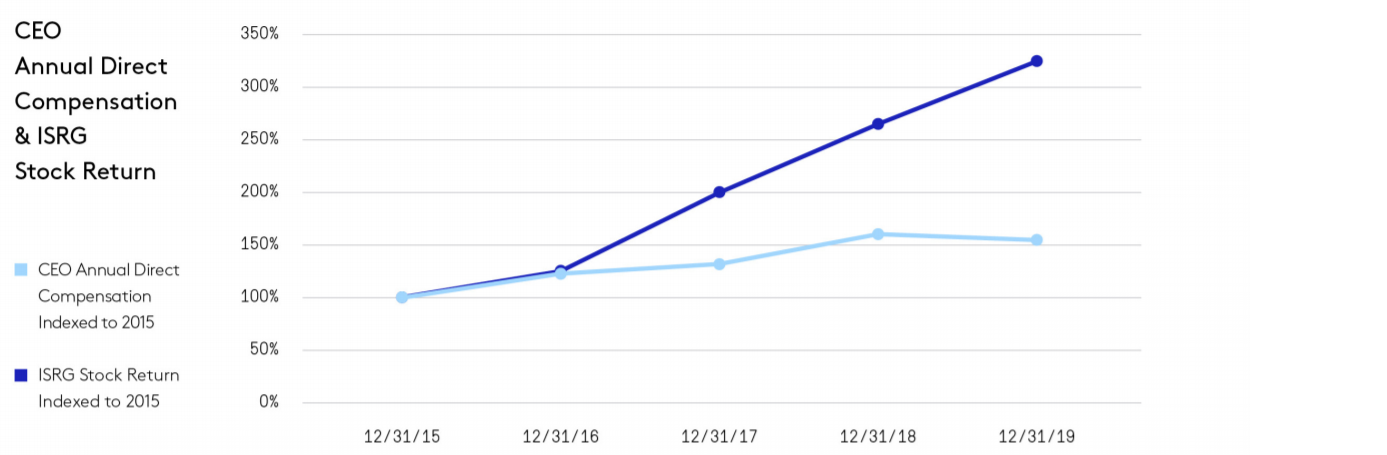

Intuitive Surgical is led by CEO Gary Guthart, Ph.D., who is currently 54. In 2019, his total compensation was US$6.47 million, which is less than 1% of the company’s profit of US$1.38 billion in the same year. There are two other big positives about the compensation structure for Guthart and the other key leaders of Intuitive Surgical.

First, 75% of Guthart’s total compensation in 2019 came from restricted stock units (RSUs) and stock options that vest over periods of 3.5 years to 4 years. It’s a similar story with other members of Intuitive Surgical’s senior management team – 74% of their total compensation in 2019 was directly tied to the long-term growth in the company’s share price through the use of RSUs and stock options that vest over multi-year periods. We typically frown upon compensation plans that are linked to a company’s short-term stock price movements. In Intuitive Surgical’s case, the compensation for its key leaders is tethered to multi-year changes in its stock price, which in turn is driven by the company’s business performance. So we think this aligns the interests of Intuitive Surgical’s leaders and the company’s shareholders.

Staying on the topic of alignment of interests, we also want to point out that as of 31 December 2019, Guthart directly controlled nearly 372,000 Intuitive Surgical shares (not counting shares that would be vesting within 60 days, and options that he could exercise shortly after end-2019) that are worth around US$257 million at the company’s stock price of US$691 on 19 August 2020. This is a large ownership stake that likely also puts Guthart in the same boat as other Intuitive Surgical shareholders.

Second, the chart below shows that the growth in Guthart’s total compensation from 2015 to 2019 has been significantly lower than the increase in Intuitive Surgical’s stock price over the same period.

Source: Intuitive Surgical proxy statement

On capability and innovation

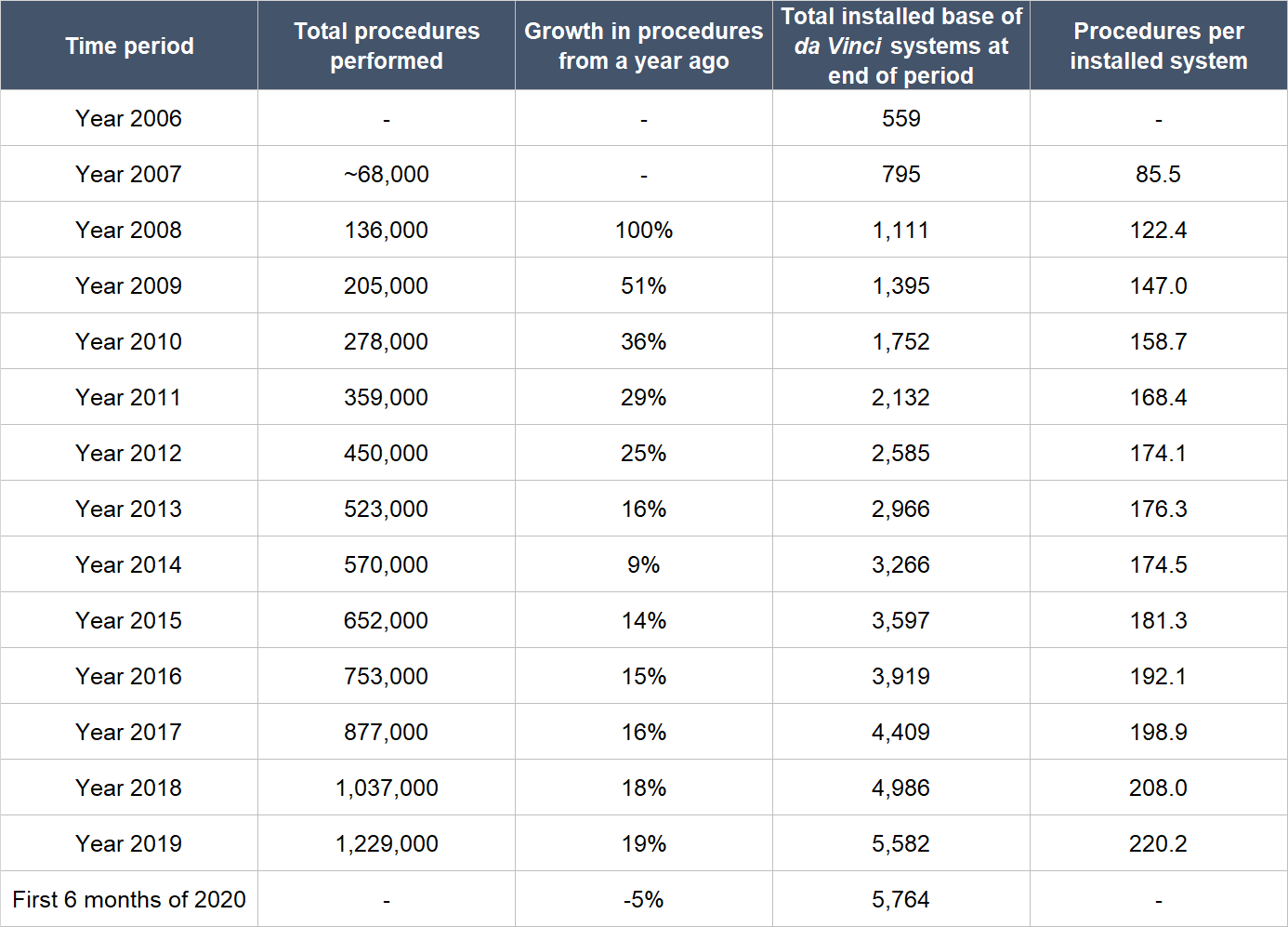

There are three crucial figures for us when we assess the level of demand for Intuitive Surgical’s robots: The installed base of the da Vinci systems; the number of surgical procedures conducted with the systems; and the average number of procedures performed per installed system per year. The table below shows the growth of these three figures since 2006, and point to the tremendous job that Intuitive Surgical’s management has done in this area. The first half of 2020 saw negative procedure growth because of COVID-19.

Source: Intuitive Surgical annual reports and earnings updates

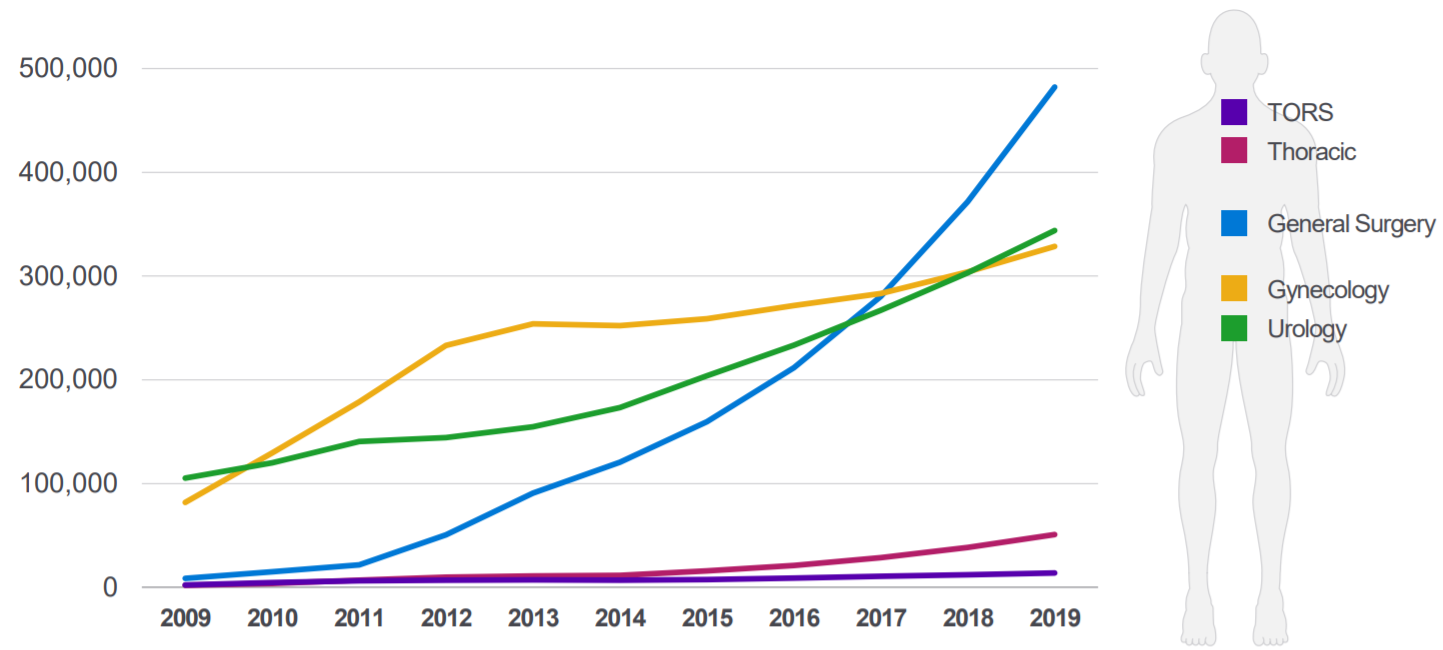

Management has also been innovative in expanding the range of surgical procedures that Intuitive Surgical’s systems can reach – see the chart below for how fast the global procedure-count for general surgery grew from 2012 to 2019 even as the gynecology procedure-count (the core of the company’s business in 2012) saw a deceleration in the growth rate.

Source: Intuitive Surgical investor presentation

Staying with the theme of innovation, Intuitive Surgical has already commercialised four generations of its da Vinci family of surgical robots since its founding, so it has a strong history of improving its flagship product. There are also some interesting recent developments:

- Intuitive Surgical is in the early stages of its rollout of the da Vinci Sp system, which was commercialised only in the third quarter of 2018. The new system is already used in urology, gynecology, general, and head and neck surgical procedures in South Korea. But it was only cleared by US regulators in 2019 for use in urologic and transoral surgical cases in the country. Intuitive Surgical is seeking approval for more use cases for the da Vinci Sp system in the US, but the COVID-19 pandemic has severely hampered the company’s efforts. At the end of 2020’s second quarter, the total installed base of the da Vinci Sp was just 52. But there are promising signs. Intuitive Surgical’s management said in the earnings conference call for 2020’s second quarter that “average monthly utilization for Sp in Korea continues to exceed that of Xi [launched in 2014], a strong positive that speaks to early interest in the platform by surgeons and their patients.”

- The Ion platform, Intuitive Surgical’s flexible robotics system for performing lung biopsies to detect and diagnose lung cancers, received 510(k) FDA (Food & Drug Administrattion) clearance in the US in 2019’s first quarter. “Hundreds” of procedures had been performed with the Ion platform as of 2019’s third quarter ,and as of 2019’s fourth quarter, the initial rollout had met management’s expectations and received “strong” user feedback. But lately, the Ion platform appears to have faced some setbacks. Even though Intuitive Surgical’s management commented in the earnings conference call for 2020’s second quarter that the “Ion program continues to march forward in the face of COVID headwinds,” the number of Ion platforms that are placed in hospitals for commercial use had declined from 18 in 2020’s first quarter to just three in the second quarter. Nonetheless, we’re still intrigued by the opportunity. Lung cancer is one of the most common forms of cancer in the world. If the Ion platform is successful, it could open a previously untapped market for Intuitive Surgical.

- The company acquired an existing supplier of 3D robotic endoscopes, Schölly Fiberoptic, in August 2019. The acquisition boosts Intuitive Surgical’s capabilities in the areas of imaging manufacturing, design, and processing, which are important for surgeries of the future, according to the company’s management.

- Intuitive Surgical received 510(k) FDA clearance for its Iris product in 2019’s first quarter. Iris is the company’s augmented reality software which allows 3D pre-operative images to be naturally displayed in a surgeon’s da Vinci console for use in real-time during an actual surgery. The company is currently in the early stages of an Iris pilot study in a few US hospitals.

- We first learnt in October 2019 that Intuitive Surgical was looking to hire software engineers who have skills in artificial intelligence (AI) for its imaging and intelligence group. And in the past two months, Intuitive Surgical has continued to post job offers that are related to machine learning and AI. We see this as a sign that the company is working with AI to improve its product features.

- In the fourth quarter of this year, Intuitive Surgical will introduce surgical instruments for its da Vinci systems that have longer lifespans compared to past iterations. In addition, Intuitive Surgical will also be lowering prices for some of its surgical instruments that are used mostly in lower acuity procedures. One of Intuitive Surgical’s core aims is to lower the overall cost of patient-treatment compared to traditional methods; the company’s moves to extend the lives and lower the prices of surgical instruments is inline with this aim. Intuitive Surgical also believes that although these moves will lower its near-term revenue, they will have long-term benefits for the company. We agree, and think this is a smart initiative by management.

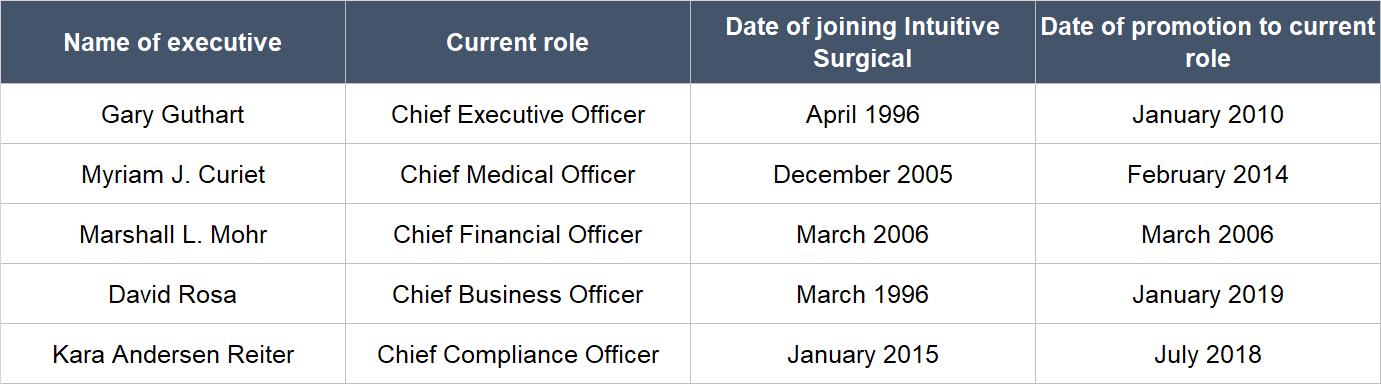

We want to highlight that Guthart joined Intuitive Surgical in 1996 and became COO (Chief Operating Officer) in 2006. In January 2010, he became CEO. In other words, much of Intuitive Surgical’s excellent track record in growing its installed base and procedure-count that we mentioned earlier had occurred under Guthart’s watch.

Source: Intuitive Surgical proxy statement

Many of Intuitive Surgical’s other key leaders have also been with the company for years, as shown in the table above, and we appreciate their long tenures. Some last words from us on Intuitive Surgical’s management: In our view, it’s a positive sign on the company’s culture for it to promote from within, as has happened with many of the C-suite roles, including Guthart’s case.

4. Revenue streams that are recurring in nature, either through contracts or customer-behaviour

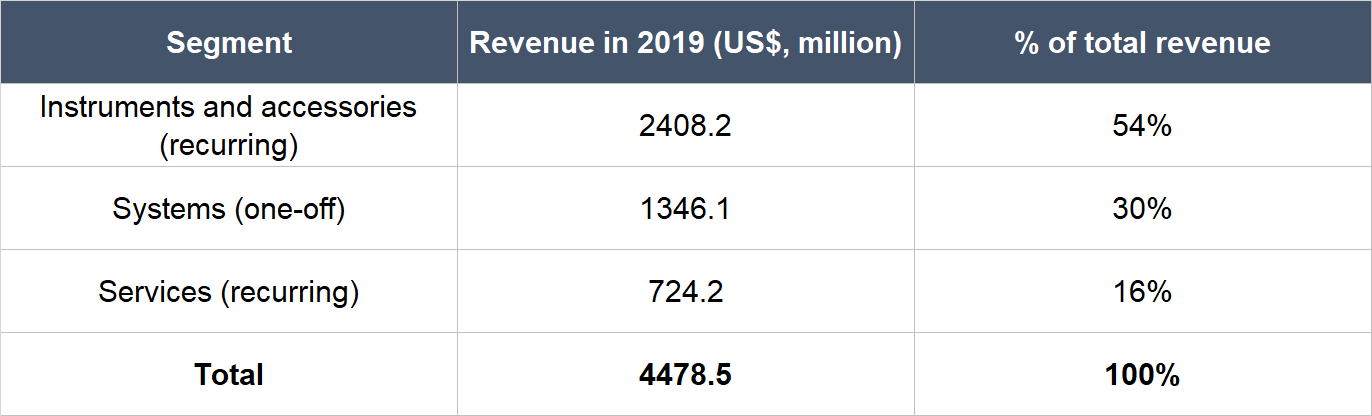

You may be surprised to know that the one-time sale of robotic surgical systems accounts for only a relatively small portion of Intuitive Surgical’s business despite their high price tag – just 30% of the company’s total revenue of US$4.48 billion in 2019 came from systems sales.

This is because the surgical robots bring with them recurring revenues through a classic razor-and-blades business model. Each surgery using a da Vinci robot results in US$700 to US$3,500 in sales of surgical instruments and accessories for Intuitive Surgical. Moreover, the robots also each generate between US$80,000 and US$190,000 in annual maintenance revenue for the company. The table below shows the breakdown of Intuitive Surgical’s revenue in 2019 according to recurring and non-recurring sources:

Source: intuitive Surgical annual report

There is also an important and positive development at Intuitive Surgical in recent years: The proportion of the company’s robots that are sold on leases has been increasing. In 2019, 34.3% of the systems that were shipped by Intuitive Surgical were based on operating leases, up from 24.7% in 2018 and 15.8% in 2017. For more context, operating lease revenue at Intuitive Surgical has quadrupled from US$25.9 million in 2017 to US$106.9 million in 2019.

Intuitive Surgical’s management believes that providing leasing – an alternative to outright purchases of the da Vinci systems – accelerates market adoption of the company’s surgical robots by lowering the initial capital outlay for customers. We agree, and we think the introduction of leasing – which started in 2013 – is another sign of management’s capability. Leasing also boosts recurring revenue for Intuitive Surgical, leading to more stable financial results. If leasing revenue was included, 72% of Intuitive Surgical’s total revenue in 2019 was recurring in nature.

5. A proven ability to grow

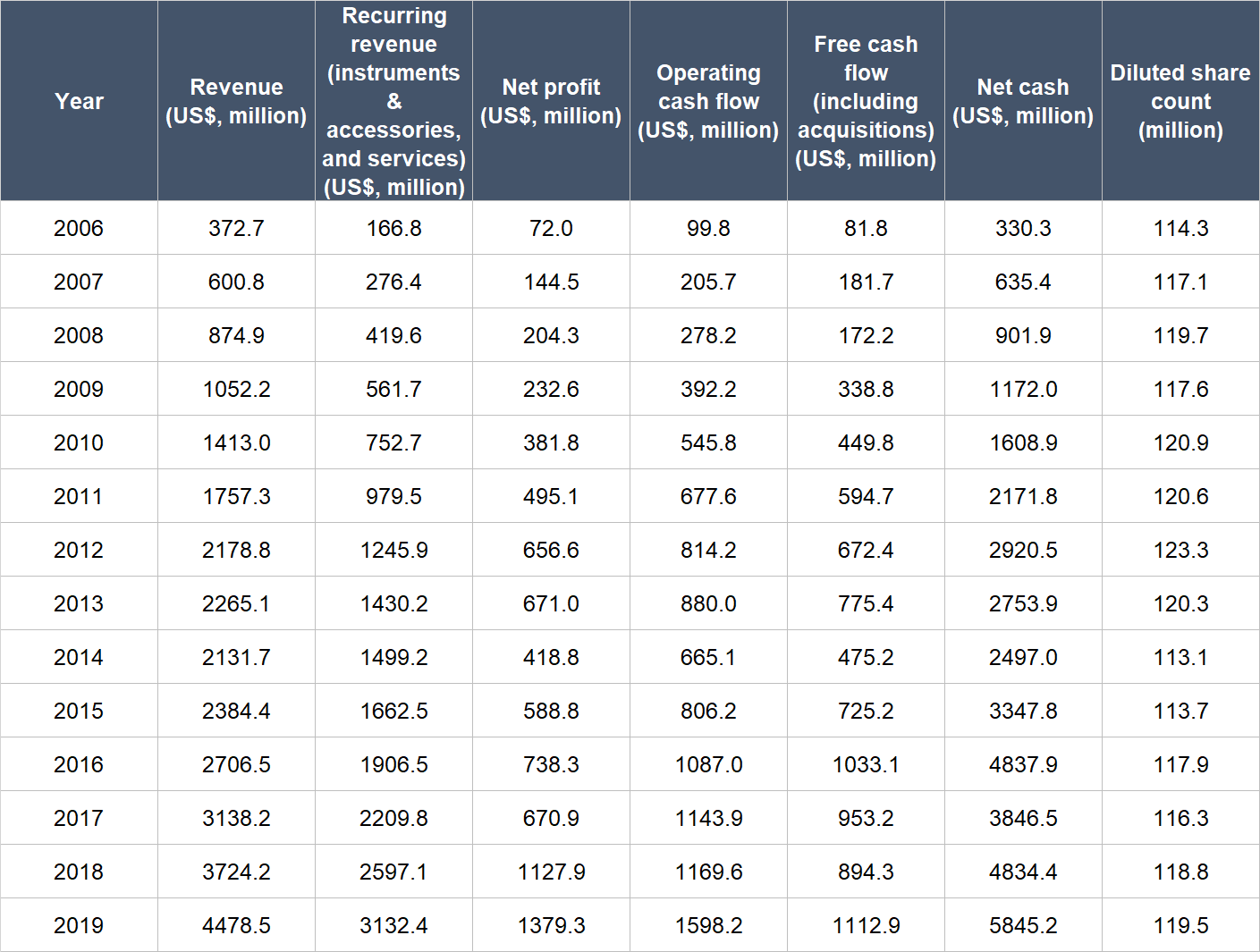

The aforementioned growth in the adoption of da Vinci robots by surgeons over time has led to a healthy financial picture for Intuitive Surgical. The table below the company’s important financial figures from 2006 to 2019:

Source: Intuitive Surgical annual reports

A few key points about Intuitive Surgical’s financials:

- Revenue has compounded impressively at 21.1% per year from 2006 to 2019; over the last four years from 2015 to 2019, the company’s annual topline growth was slower but still strong at 16.0%. (2014 was an anomalous year for Intuitive Surgical, so using the year as the base for counting growth rates will lead to skewed results; we discuss 2014 in greater detail in the risk-section of this article)

- The company also managed to produce strong revenue growth of 45.6% in 2008 and 20.3% in 2009; these were the years when the global economy was rocked by the Great Financial Crisis.

- Recurring revenue (excluding leasing) grew in each year from 2006 to 2019, and had climbed from 44.8% of total revenue in 2006 to 70% in 2019.

- Net profit jumped by 25.5% per year from 2006 to 2019, and the annual growth rate was also excellent at 23.7% over the past four years (2015 to 2019).

- Operating cash flow has similarly shown a marked increase from 2006 to 2019, with annual growth of 23.8%. The growth rate from 2015 to 2019 is just a tad slower at 18.7% annually.

- Free cash flow, net of acquisitions, has consistently been positive and has also stepped up significantly from 2006 to 2019 at 22.2% per year. The annual growth in free cash flow has slowed to 11.3% from 2015 to 2019, but we’re not worried. The absolute amount of free cash flow is still robust, and the growth rate picked up in 2019 (24.4%).

- The net-cash position on the balance sheet was positive in every year from 2006 to 2019, and has also increased significantly. In fact, Intuitive Surgical has consistently had zero debt.

- Dilution has also been negligible for Intuitive Surgical’s shareholders from 2006 to 2019 with the diluted share count barely rising in that period.

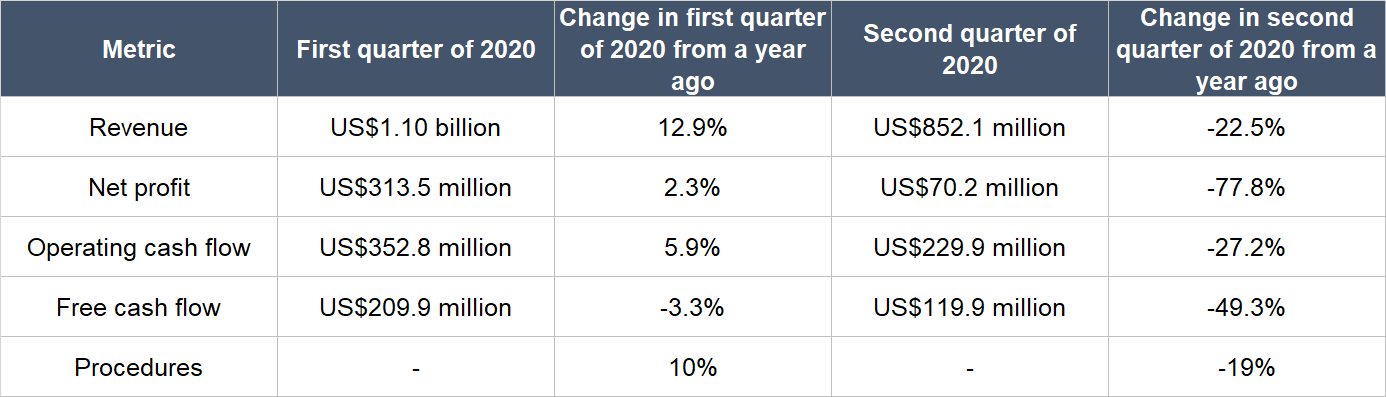

The first half of 2020 has not been kind to Intuitive Surgical. The table below shows the changes in the company’s revenue, net profit, cash flows, and procedure-count for the first and second quarters of 2020:

Source: Intuitive Surgical earnings update

Intuitive Surgical experienced growth in its business (in the form of procedures) early in the first quarter of 2020. But as COVID-19 started spreading across the world during the quarter, Intuitive Surgical’s business started getting hurt because the company’s customers – hospitals – had to divert resources to treat COVID-19 patients, in the process deferring elective surgical procedures. The pain extended through to the second quarter of 2020.

But we think the negative impacts to Intuitive Surgical’s business from COVID-19 is very likely to be transitory in nature. For example, in the second quarter of 2020, Intuitive Surgical saw its procedures in China recover to the pre-pandemic level seen in early-January 2020 as COVID-19 subsided in the country. For perspective, the procedure-count in China in early-February 2020 was 90% below what it was in early-January 2020. Intuitive Surgical’s current rock-solid balance sheet also gives us confidence that it has a very high chance of being able to tide through the current difficulties and come out ahead.

6. A high likelihood of generating a strong and growing stream of free cash flow in the future

There are two reasons why we think Intuitive Surgical excels in this criterion.

First, the company has done very well in producing free cash flow from its business for a long time. Its free cash flow margin (free cash flow as a percentage of revenue) was in a healthy range of 19.7% to 38.2% from 2006 to 2019, and it came in at 24.9% in 2019.

Second, there’s still tremendous room to grow for Intuitive Surgical. This should lead to a higher installed base of surgical robots for the company over time. It’s also reasonable to assume that the utilisation of the robots (procedures performed per installed robot) will climb steadily in the years ahead; it has increased in every year from 2007 to 2019, as shown earlier. These assumptions mean that Intuitive Surgical should see robust growth in its recurring revenues (instruments & accessories; services; and leasing) – and the company’s recurring revenue streams likely come with high margins.

Valuation

We like to keep things simple in the valuation process. Since Intuitive Surgical has a long history of producing solid and growing streams of profit and free cash flow, we think both the price-to-earnings (P/E) ratio and price-to-free cash flow (P/FCF) ratio are suitable gauges for the company’s value.

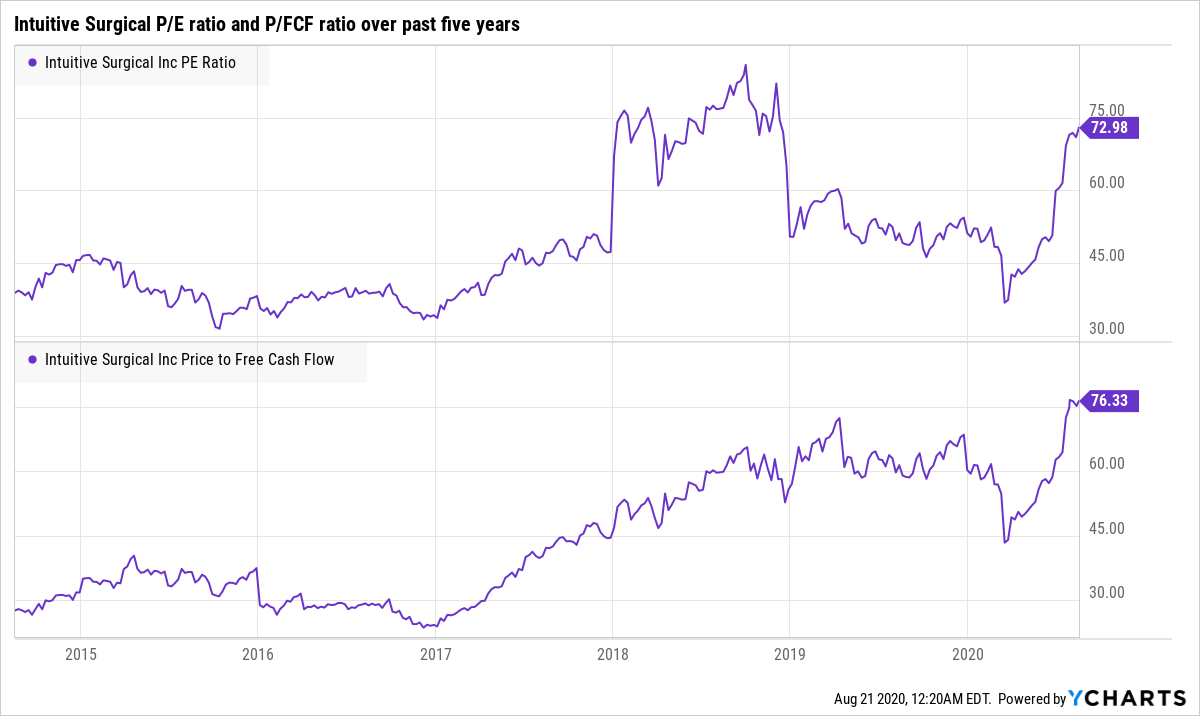

Intuitive Surgical’s valuation ratios are high at Compounder Fund’s average purchase price of US$677 per share: The P/E ratio is around 71, while the P/FCF ratio is around 82. The chart below illustrates the two ratios over the past five years (P/E at the top, P/FCF at the bottom), and they are clearly near five-year highs.

The current COVID-19 pandemic has pinned down Intuitive Surgical’s trailing profit and cash flow numbers. But even before the virus started spreading across the world, the company already carried premium valuations, and justifiably so. Intuitive Surgical has (a) high levels of recurring revenue that lead to relatively predictable streams of earnings and cash flows, and (b) an excellent track record and huge growth opportunities ahead. The company’s growth prospects may be temporarily muted because of COVID-19, but as we had mentioned earlier, we think the virus is only a temporary setback for Intuitive Surgical.

We also want to highlight that Intuitive Surgical has built a strong competitive position in our eyes because of its first-mover advantage in the surgical robot market. Hospitals and doctors need to invest time and resources in order to use the da Vinci robots. The more da Vinci systems that are installed in hospitals, the harder it is for competitors to unseat Intuitive Surgical – so it’s good to know that there are more than 5,700 da Vinci systems installed worldwide today.

The risks involved

There are three key risks with Intuitive Surgical that we’re watching.

The first is any future changes in healthcare regulations. Intuitive Surgical’s revenue-growth slowed dramatically in 2013 (up just 4%, compared to a 24% increase in 2012); revenue even declined in 2014. Back then, uncertainties related to the Affordable Care Act (ACA) – the US’s national health insurance scheme set up by then-US president Barack Obama – caused hospitals in the US to pull back spending.

Current US president, Donald Trump, made changes to the ACA as early as 2017. Trump’s meddling with the ACA has so far not dented Intuitive Surgical’s growth. But if healthcare regulations in the US and other countries Intuitive Surgical is active in (such as Germany, China, Japan, and South Korea) were to change in the future, the company’s business could be hurt.

The second key risk is competition. Intuitive Surgical name-dropped 13 current and would-be competitors in its latest 2019 annual report, including corporate heavyweights with deep pockets such as Johnson & Johnson and Samsung Corporation. Intuitive Surgical is currently the runaway leader in the field of robotic surgery systems, but there’s always a risk that someone else could come up with a more advanced and more cost-effective surgical robot. This said, we’re encouraged by recent developments that suggest it is incredibly tough for competitors to emerge:

- Johnson & Johnson is one of Intuitive Surgical’s would-be competitors to watch. In 2019, it acquired Auris Healthcare (named as one of Intuitive Surgical’s competitors under Johnson & Johnson) for at least US$3.4 billion, and announced the full acquisition of Verb Surgical (also named as a competitor under Johnson & Johnson) in December. Verb Surgical was previously a joint venture between Johnson & Johnson and Alphabet, the parent company of Google and also one of Compounder Fund’s holdings. In July 2020, Johnson & Johnson announced that human trials for its surgical robots will be delayed till 2022.

- Medical devices company Medtronic is another high-profile would-be competitor of Intuitive Surgical, with revenue of US$29 billion in revenue over the last 12 months. In the third quarter of 2019, the company said that it will be launching its own suite of surgical robots in the near future. But in May 2020, Medtronics announced that it will be delaying the launch of its surgical robots because COVID-19 has slowed down the progress of its clinical trials.

Even if competition for Intuitive Surgical were to heat up in the future, we’re not worried. We mentioned earlier that Intuitive Surgical has already carved out a strong competitive position for itself. Moreover, we think the real battle is not between Intuitive Surgical and other makers of robotic surgery systems. Instead, it is between robotic surgery and traditional forms of surgery. As we had already mentioned, only 2% of surgeries worldwide are conducted with robots today, so there’s likely plenty of room for more than one winner among makers of surgical robots. It’s worth noting too that Intuitive Surgical is not sitting still. At the end of 2019, the company had over 3,500 patents and 2,000 patent applications around the world, up from 2018 (over 3,000 patents and 2,000 patent applications) and from 2012 (over 1,300 and 1,100, respectively). Nonetheless, we’ll still be keeping an eye on competitive forces in Intuitive Surgical’s market. We’ll be worried if we see a prolonged deceleration in growth or decline in the number of surgical procedures that the da Vinci robots are used in.

The last risk we’re watching is COVID-19. Intuitive Surgical’s management commented in the latest earnings call (for 2020’s second-quarter) that the “recovery tail of surgery will be a long one, likely to last many quarters.” We said earlier that we think COVID-19’s negative impact to Intuitive Surgical’s business will likely be transitory and management’s comments fit our timeline as patient investors. Furthermore, Intuitive Surgical has a remarkably strong balance sheet that we think can allow the company to withstand tough market conditions for some time. But if the recovery from COVID-19 were to drag on for years, we will have to reassess the situation with Intuitive Surgical, since there’s an opportunity cost with Compounder Fund’s capital.

Summary and allocation commentary

Intuitive Surgical shines when seen through the lens of our investment framework for Compounder Fund:

- It is a leader in the fast-growing surgical robot market. In addition, we think it has also carved out a strong competitive position in its space.

- Its balance sheet is debt-free and has billions in cash and investments.

- The management team is sensibly incentivised. They also have excellent track records in innovation and growing the key business metrics of the company (such as the installed base of the da Vinci robots and the number of procedures conducted with the robots).

- The company has an attractive razor-and-blades business model that generates high levels of recurring revenues with strong profit margins.

- Intuitive Surgical has a robust long-term history of growth – its revenue, profit, and free cash flow even managed to soar during the Great Financial Crisis.

- It has historically been adept at generating free cash flow, and likely can continue doing so in the years ahead.

There are important risks to watch, as it is with any other investment. In Intuitive Surgical’s case, the key risks for us are future changes in healthcare regulations, potential for competition to emerge, and COVID-19. On the last risk, we’re mindful that the virus has already hurt Intuitive Surgical’s business in the first half of 2020.

After weighing the pros and cons, including the company’s seemingly high P/E and P/FCF ratios, we initiated a 2.5% position in Intuitive Surgical – a medium-sized allocation – with Compounder Fund’s initial capital. To us, if COVID-19 is out of the equation, Intuitive Surgical is a company with (1) a huge addressable market, and (2) a high probability of being able to grow at a strong clip for many years in the future. But with COVID-19 in the picture now, Intuitive Surgical’s growth prospects look a little murkier to us (though to be clear, we still think the chances are high that the company can grow at high rates over the long run). Hence, we’re only staking a medium-sized allocation to the company for now.

And here’s an important disclaimer: None of the information or analysis presented is intended to form the basis for any offer or recommendation; they are merely our thoughts that we want to share.