Compounder Fund: Portfolio Update (April 2022) - 13 Apr 2022

Jeremy and I intend to share frequent but non-scheduled updates on how Compounder Fund’s portfolio looks like. The last time we shared an update on this was for Compounder Fund’s portfolio as of 9 January 2022. In the update, I shared all 50 holdings that were in the fund’s portfolio at that time. Since then, there have been a few changes to the fund’s holdings.

First, Afterpay is no longer in Compounder Fund’s portfolio. I shared in the a previous update that Block – which was previously known as Square – announced in August 2021 that it would be acquiring Afterpay by issuing new shares of itself to existing Afterpay shareholders. The deal was completed on 31 January 2022. In the aforementioned previous update, I wrote that our intention was to hold onto all of Compounder Fund’s Afterpay shares and have them be automatically converted to Block shares. This was exactly what happened. We’ve also not sold any Block shares that Compounder Fund received. Jeremy and I are eager to observe the growth of the combined entity.

Second, JD.com appeared in Compounder Fund’s portfolio in late-March this year but was sold in early-April. In the January 2022 update, I discussed Tencent’s partial distribution of its JD.com shares to its shareholders; Compounder Fund’s JD.com shares arrived as a result of Tencent’s distribution. I also mentioned that Jeremy and I were still deciding what to do with the JD.com shares. We eventually made the call to sell the shares and we will be explaining in detail our reasons for doing so in the coming months on Compounder Fund’s website.

Third, Jeremy and I have sold all of Compounder Fund’s a2 Milk shares. We first sold some a2 Milk shares in July 2021 to provide some of the capital for Compounder Fund’s initial investment in Upstart. Earlier this month, we sold the remaining a2 Milk position. Similar to JD.com, we will publish our sell-thesis for a2 Milk in the coming months.

Fourth, two new companies have been added to Compounder Fund’s portfolio and they are Adyen and Taiwan Semiconductor Manufacturing Company (TSMC). Compounder Fund is able to accept new subscriptions once every quarter with a dealing date that falls on the first business day of each calendar quarter. In the middle of March 2022, Jeremy and I successfully closed Compounder Fund’s sixth subscription window since its initial offering period (which ended on 13 July 2020). This new capital – along with the capital raised from the sale of a2 Milk and JD.com – was deployed quickly in the days after the last subscription window’s dealing date of 1 April 2022. Jeremy and I invested the new capital in Adyen and TSMC alongside three existing Compounder Fund holdings. They are (in alphabetical order): Alphabet, Facebook, and Shopify.

In Compounder Fund’s Owner’s Manual, we mentioned that “if Compounder Fund receives new capital from investors, our preference when deploying the capital is to add to our winners and/or invest in new ideas.” Not all of the three existing holdings in Compounder Fund’s portfolio that we added capital to have seen their stock prices rise strongly after we initially invested in them. But all of them have executed well since our investments and they’ve produced great results. They are winners, according to our definition.

We will publish our investment theses for Adyen and TSMC in the weeks ahead. But meanwhile, here’s a brief description of both companies:

- Adyen is a Surinamese word for “start over again”. It’s an apt name for the Netherlands-based company. Adyen’s founders were founders of and senior executives in an international payment service provider named Bibit that was sold to the Royal Bank of Scotland in 2004. In 2006, Adyen was founded with the aim of facilitating digital payments by building a modern – and better – payments infrastructure that connects directly with card networks and local payment methods. Today, Adyen runs a fully integrated global payments platform, covering gateway, risk management, processing, issuing, acquiring, and settlement activities. Whatever Adyen has built has resonated with merchants that include some of the biggest companies in the world, from tech-giant Microsoft to fast-food chain McDonald’s. From 2015 to 2021, the payment volume processed by Adyen had compounded at an impressive rate of 58.8% per year from €32.2 billion to €516 billion. This drove excellent annual net revenue growth of 47.2% from €0.09 billion to €1.0 billion over the same period. Simultaneously, Adyen’s free cash flow margin (free cash flow as a percentage of net revenue) increased from an already outstanding 36.8% in 2015 to a remarkable 56.6% in 2021.

- Given TSMC’s name (Taiwan Semiconductor Manufacturing Company), it would not come as a surprise that its business is about manufacturing semiconductor chips, mostly in Taiwan. To be even more precise, TSMC is a foundry, which is a contract-manufacturer of semiconductor chips. The company’s customers include fabless semiconductor companies (companies that design but do not manufacture semiconductor chips), integrated device manufacturers (companies that design and manufacture semiconductor chips), and consumer-electronics companies such as Apple. In the 1960s and 70s, the legendary co-founder of Intel, Gordon Moore, gave the world Moore’s Law, his observation that the number of transistors in an integrated circuit – or semiconductor chip – would double every two years. Moore’s Law has been a driving force in global technological innovation because a chip becomes faster and more powerful with more transistors on it. TSMC is a key player helping to power Moore’s Law today. According to data from Capital Economics cited by a June 2021 Wall Street Journal article, TSMC manufactures 92% of the world’s most advanced chips; Samsung from Korea accounts for the rest. The most advanced chips in the world currently are those that have structures with geometries of 5 nanometers (nm); these structures are effectively transistors, which are tiny electrical switches. For perspective, a human hair’s diameter is around 75,000 nm, and a 5 nm chip designed by Apple (and manufactured by TSMC) that goes into its laptops contains up to 57 billion transistors. TSMC has experienced revenue growth in each year going back to 2010, is very profitable, and also generates strong free cash flow; its average net profit and free cash flow margins from 2016 to 2021 were 35.8% and 20.9%, respectively. To meet growing customer demand, maintain TSMC’s technological leadership, and to break new grounds, management said in the 2021 fourth-quarter earnings call that TSMC’s capital expenditure for 2022 would be a staggering US$40 billion to US$44 billion. Even so, this is a sum TSMC can afford without breaking the bank; the company ended 2021 with US$39.8 billion in operating cash flow and US$12.1 billion in net-cash on its balance sheet. In the same earnings call, TSMC’s management also guided to annualised revenue growth of between 15% and 20% “over the next several years”. This is significantly faster than the revenue growth of 9.6% per year TSMC experienced from 2015 to 2020. The company appears to be on the right track so far; its revenue numbers for the first quarter of 2022 showed year-on-year growth of 35.5%.

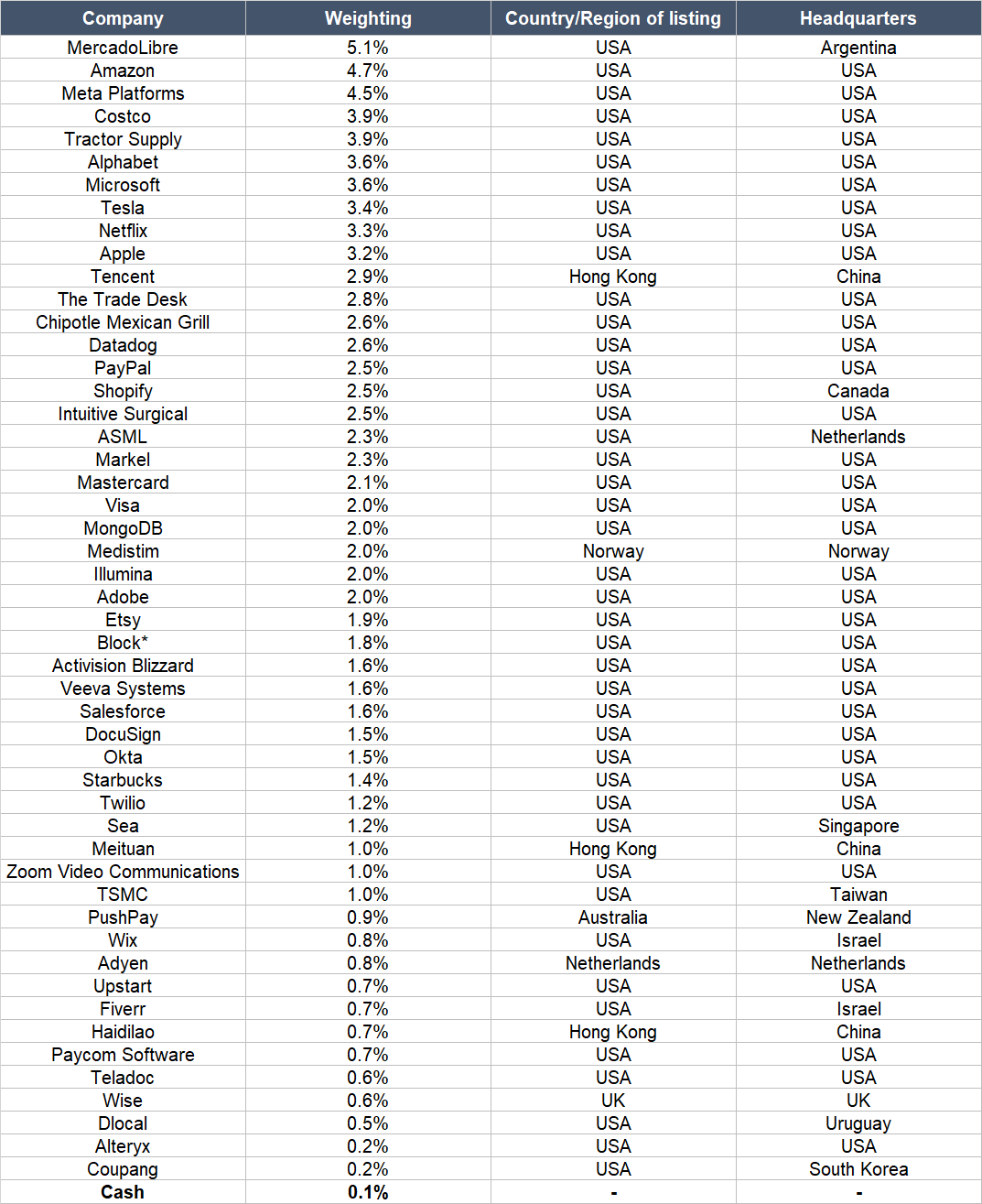

All told there are now 50 companies in Compounder Fund’s portfolio. Here’s how the portfolio looks like as of 10 April 2022:

Table 1

*0.4% of the Block position comes from Block shares that are listed in Australia; but for all intents and purposes, we see the Australia-listed Block shares as being identical to the US-listed variety

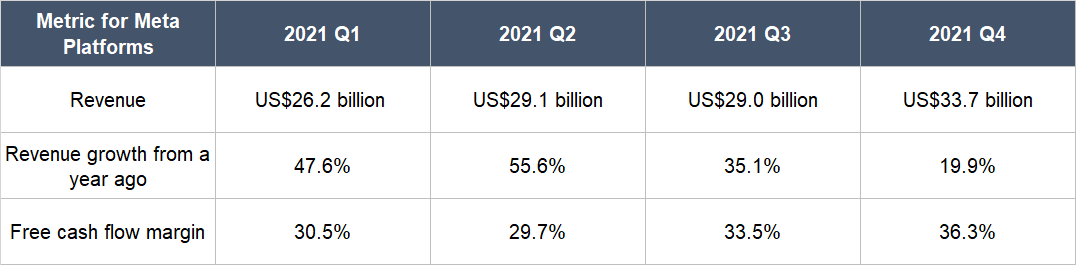

Our biggest addition in early-April 2022 was to Meta Platforms. As of 10 April 2022, Meta Platforms’ stock price had fallen by 42% from its 52-week closing-high of US$382 that was reached in September 2021. Table 2 below shows the company consistently putting up double-digit revenue growth – a remarkable feat given the high revenue base – and strong free cash flow margins over the past year. This makes the stock price decline baffling on the surface. But under the hood, the company’s business has been under significant pressure because of Apple’s changes to its privacy policy for digital advertising tracking that took effect in April 2021; this has hurt Meta Platforms’ accuracy in ad-targeting and ability to measure advertising outcomes. Meta Platform’s management team has said that they expect the company’s revenue in 2022 to be lowered by US$10 billion as a result of Apple’s changes.

Table 2

Source: Company earnings updates

I first discussed Apple’s privacy policy in an April 2021 update. In it, I mentioned that Meta Platforms – then called Facebook – was the biggest addition to our existing holdings. I also wrote:

“We added to our position in [Facebook] despite Apple’s much-publicised change to the privacy policy for its IDFA (Identifier for Advertisers). Without going into detail (see here for more), Apple’s new upcoming policy will require apps to get users’ permission to track their data across apps or websites owned by other companies…

…In short, changes to the IDFA would make it difficult for Facebook to know the shopping behaviour of Facebook users outside of the company’s own platforms. This would diminish the value of Facebook’s digital advertising services. But the company has not been lying still. It has been actively encouraging commerce activities to take place directly on its own platforms and one such initiative is the launch of Facebook Shops in 2020. Last month, during a Clubhouse session with Josh Constine, Facebook’s CEO and co-founder, Mark Zuckerberg, revealed that Facebook Shops now has more than 1 million active stores and 250 million active users. During the same Clubhouse session, Zuckerberg also shared how Facebook could emerge from Apple’s IDFA issue even stronger than before:

“When it comes to the iOS 14 changes [for IDFA], for example, and their impact on our business, I think the reality is that I’m confident that we’re gonna be able to manage through that situation. And we’ll be in a good position. I think it’s possible that we may even be in a stronger position. If Apple’s changes encourage more businesses to conduct commerce on our platforms, by making it harder for them to basically use their data in order to find the customers that would want to use their products outside of our platforms.”

There are three other reasons for our decision to add to Facebook.

First, the company grew revenue by an impressive 33.2% in the fourth quarter of 2020 while improving its free cash flow margin from an already strong 21.5% a year ago to 33.6%. It’s worth noting too that Facebook spent US$4.6 billion on capital expenditures during the quarter, up 12.5% from a year ago.

Second, the chance of Facebook creating a massive business in the AR/VR (augmented reality and virtual reality) space now looks higher to us than before. Last month, The Verge reported that Facebook has nearly 10,000 employees – around 15% of its total headcount of 58,604 at the end of 2020 – working on AR/VR technology. For perspective, this is a significant increase from 2017, when Facebook had more than 1,000 AR/VR employees, which was around 5% of its total workforce then.

Third, Facebook’s shares had a trailing price-to-free cash flow ratio of 37 at the end of March 2021. We think this is an undemanding valuation for a company that (1) could compound its revenue at north of 20% annually over the next five years, (2) fetched an excellent free cash flow margin of 27% in 2020, and (3) has a fortress of a balance sheet with zero debt and nearly US$62 billion in cash and investments.”

Since the excerpts above were published, a few things have happened to the company:

- Meta Platforms’ user base across its platforms – Facebook, Instagram, Messenger, and Whatsapp – had increased from an already-staggering 2.6 billion unique daily users in the fourth quarter of 2020 to 2.82 billion in the fourth quarter of 2021.

- Meta Platforms has continued to build tools and services for consumers to shop directly on its various platforms.

- The company’s revenue growth and free cash flow margins were both strong throughout each quarter in 2021, as shown in Table 5.

- There are ongoing improvements to Meta Platforms’ digital advertising services, such as the introduction of the Aggregated Event Measurement solution. The Information, a digital news outlet that reports on technology businesses, published an article late last month sharing anecdotes that advertisers are seeing an improvement in Meta Platforms’ advertising performance after an initial decline because of Apple.

- Meta Platforms announced a few months ago that it would be investing at least US$10 billion per year on technology infrastructure that’s related to the metaverse; an example of these investments is Meta Platforms’ AI Research SuperCluster, a supercomputer for artificial intelligence. The supercomputer will be the world’s fastest when it is completed in the middle of this year. We think these investments would help with Meta Platforms’ chances of success in developing the metaverse, which would almost certainly involve AR/VR.

- Meta Platforms’ trailing price-to-free cash flow (P/FCF) ratio had declined from 37 at the end of March 2021 to just 16 at the end of March 2022. Meanwhile, the free cash flow margin increased from 27% in 2020 to 33% in 2021, and the balance sheet remains a fortress with nearly US$48 billion in cash and investments and zero debt as of 31 December 2021.

These are all positive developments from our vantage point as a long-term investor in Meta Platforms. But the company’s management expects revenue growth of only 3%-11% year-over-year in the first quarter of 2022 because of “headwinds to both impression and price growth.” The good thing is these headwinds are somewhat self-inflicted. Meta Platforms has begun to prioritise Reels – a short-form video service – on its key social media platforms, Facebook and Instagram. This was done – correctly, in our view – by Meta Platforms’ management to combat the threat of TikTok, a social network that focuses on short-form videos. For now, Reels monetises at a lower rate than Facebook and Instagram’s other services. But management is optimistic about the future of Reels and we share this enthusiasm – Meta Platforms’ leaders have a history of executing successful transitions, such as the company’s shift from web to mobile and from the Feed service to Stories. During a March 2022 investor conference, Meta Platforms’ CFO David Wehner said (emphases are mine):

“Yes. I mean, look, we believe the Reels and short-form video provides a big opportunity for time-spent growth across our Family of Apps and others, incrementally making the opportunity bigger for us. So we do think there are Reels incremental growth opportunities here.

I think one of the best way to, sort of, frame, kind of, looking through COVID and all of that, is that video and short-form, both on our platform and obviously with others, has taken the bulk of the growth in the mobile app ecosystem over the last couple of years. And we think we’re well positioned now to participate in that growth, going forward.

And so with Instagram Reels, we think we already have a strong position in the short — in short-form. Obviously, we’re well behind TikTok. In India, where they’re not operating, we’re clearly much bigger. For context, Reels is our fastest-growing format. It’s growing faster than Stories at a comparable time in 2018.

We think that the market for short-form is large enough that there will be an opportunity for multiple players. And while it’s a headwind for impression and revenue growth, as we ramp in 2022, longer term, we think it’s going to be a tailwind. We’re — now, we’re pulling time away from other services, but adding to overall engagement. So it is incremental.

Longer term, we think the big picture is, the opportunity for Family of Apps is bigger with short-form as part of it. And then, in addition to the success that we’re having with Reels on Instagram, last month, we launched Reels globally on Facebook in over 150 countries. It’s much earlier days on Facebook, but we’re excited about the early engagement there as well.”

To summarise, Jeremy and I think that Meta Platforms’ management team is likely capable of solving the problems that Apple has thrown at the company while at the same time, growing the Reels short-form-video service into an important pillar of the company’s advertising business. With a trailing P/FCF ratio of just 16 at the end of March 2022, Meta Platforms looks like good value to us.

After the acquisition of Afterpay by Block, another involuntary change could soon happen to Compounder Fund’s portfolio. Activision Blizzard and Microsoft jointly announced on 18 January 2022 that the latter would be acquiring the former. The all-cash deal, which is expected to be completed in the year ending 30 June 2023, will see Microsoft buy Activision for US$95 per share. We’re disappointed that we can no longer participate directly in Activision’s future business growth if and when it becomes a part of Microsoft. But we think this is a smart move by the acquirer. Activision has a stable of excellent games (see our thesis on the company for a discussion on its games portfolio) that could significantly enhance the value of Microsoft’s subscription-based gaming service, Game Pass. Currently, for a price of up to US$14.99 per month (in the USA), Game Pass subscribers can access over 100 high-quality games across various gaming platforms such as the personal computer, consoles, and mobile devices. Microsoft’s overall Gaming business, which includes Game Pass, is already sizeable, accounting for US$16.3 billion in revenue, or 9% of Microsoft’s total revenue, in the last 12 months. Activision’s US$8.8 billion in annual revenue (the figure seen in 2021) will increase the heft of Microsoft’s Gaming business.

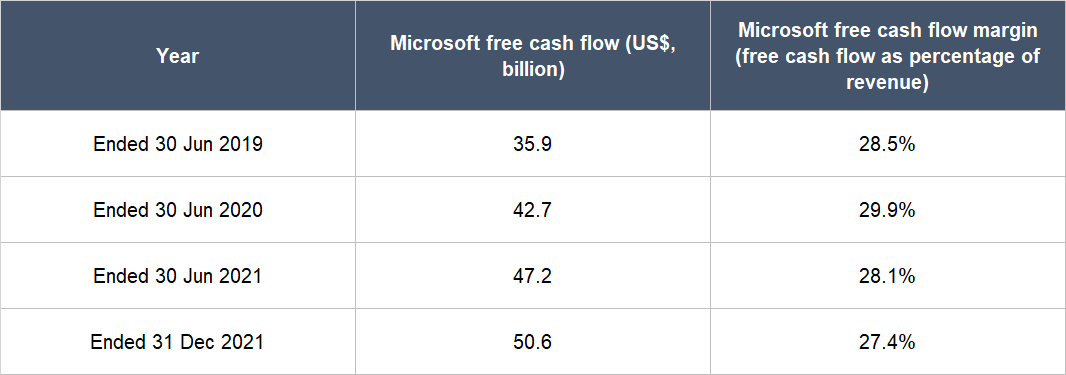

At the time of the announcement, Activision had an enterprise value (market capitalisation minus cash plus debt) of US$68.7 billion at the acquisition price of US$95 per share. If and when the deal is completed, Activision’s enterprise value is likely to be slightly lower since the company has a long track record of generating free cash flow, which should increase its net cash position; for perspective, Activision ended 2021 with US$6.8 billion in net cash and US$2.3 billion in free cash flow. But no matter how we slice it, Microsoft will still require a huge slug of cash to acquire Activision. The good thing is Microsoft should have no trouble with financing. Table 3 below shows Microsoft’s formidable free cash flows over the past few years and as of 31 December 2021, the company had a massive net cash position of US$72.1 billion.

Table 3

Source: Microsoft annual reports and earnings updates

Our current intention – which is subject to change depending on developments at Microsoft/Activision and the stock market in general – is for Compounder Fund to hold onto its Activision shares and receive the cash from Microsoft once the acquisition is completed. In this way, we save on unnecessary trading fees. Moreover, Activision’s stock price of US$80 as of 10 April 2022 is far from the acquisition price of US$95; selling in the open market now would mean forfeiting a gain of nearly 19%. There’s no guarantee, however, that the deal would proceed; it’s subject to regulatory approval by US authorities, and the long timeline for the completion of the acquisition does raise our eyebrows. We don’t see any antitrust issues – according to SuperData, the global gaming market was nearly US$140 billion in 2020, a figure which dwarfs the collective revenues of Activision and Microsoft’s Gaming business – but we don’t have any special insight into the regulatory review process. There were also news reports released earlier this month stating that US regulators would be looking into the impacts that Microsoft’s acquisition of Activision could have on consumer data and the game development labour market, among other areas. If regulators give the green light, we’re eager to observe the growth of Microsoft’s Gaming business with Activision under its umbrella.

We’re sharing all this information with the public and with the fund’s investors for two reasons. First, we believe deeply in investor education and want Compounder Fund’s return and actions to be a source for people to learn about investing. Second, we believe that this transparency will help investors of Compounder Fund develop comfort with our investing process over time, which is great; in turn, this will also free us from the time-consuming activity of dealing with questions on how we invest, and thus give us more to invest better for our investors.

And here’s an important disclaimer: None of the information or analysis presented is intended to form the basis for any offer or recommendation; they are merely our thoughts that we want to share. Holdings are subject to change at any time.