Compounder Fund: Netflix Investment Thesis - 07 Aug 2020

Data as of 1 August 2020

Netflix (NASDAQ: NFLX) is one of the 40 companies in Compounder Fund’s initial portfolio. This article describes our investment thesis for the company.

Company description

Netflix is based and listed in the US. When it IPO-ed in 2002, the company’s main business was renting out DVDs by mail. It had 600,000 subscribers back then, and an online website for its members to access the rental service.

Today, Netflix’s business is drastically different. In 2019, Netflix pulled in US$20.2 billion in revenue, of which 98.5% came from streaming; the remaining is from the legacy DVD-by-mail rental business. The company’s streaming content includes TV series, documentaries, and movies across a wide variety of genres and languages. These content are licensed from third parties or produced originally by Netflix.

Many of you reading this likely have experienced Netflix’s streaming service, so it’s no surprise that Netflix has an international presence. In 2019, 47% of Netflix’s revenue came from the US, with the rest spread across the world (Netflix operates in over 190 countries). The company counted 192.95 million subscribers globally as of 30 June 2020.

Investment thesis

We have laid out our investment framework in Compounder Fund’s website. We will use the framework to describe our investment thesis for Netflix.

1. Revenues that are small in relation to a large and/or growing market, or revenues that are large in a fast-growing market

Netflix already generates substantial revenue and has a huge base of nearly 193 million subscribers. But we think there’s still plenty of room for growth.

According to Statista, there are 1.05 billion broadband internet subscribers worldwide in the first quarter of 2019. Netflix started testing lower-priced mobile-only streaming plans in late 2018. The countries where the mobile plans are currently available are India, Malaysia, Indonesia, Thailand, and the Philippines. The mobile plans have driven subscriber growth and performed as management have expected. Data from GSMA showed that there were 3.5 billion mobile internet subscribers globally in 2018.

We’re not expecting Netflix to sign up the entire global broadband or mobile internet user base – Netflix is not in China, and we doubt it will ever be allowed into the giant Asian nation. But there are still significantly more broadband and mobile internet subscribers in the world compared to Netflix subscribers, and this is a growth opportunity for the company. It’s also likely, in our view, that the global number of broadband as well as mobile internet users should continue to climb in the years ahead. This grows the pool of potential Netflix customers.

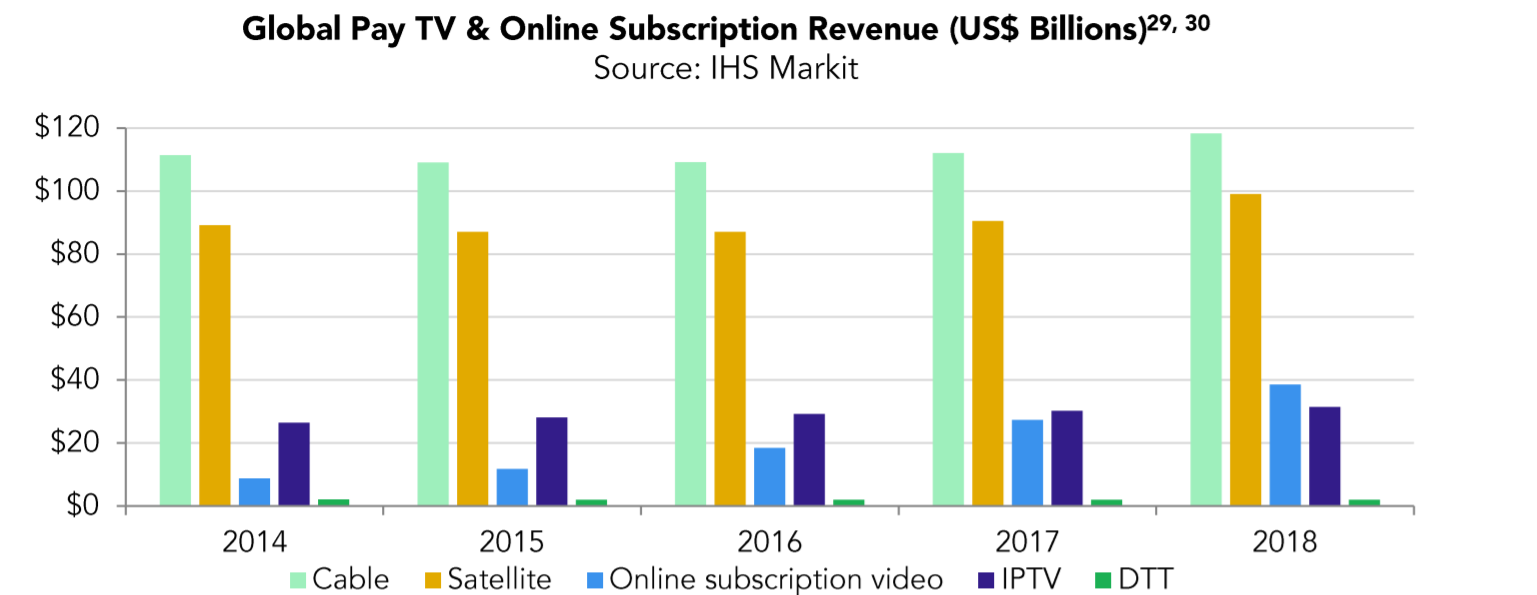

For another perspective, the chart immediately below illustrates clearly that cable subscriptions still account for the lion’s share of consumer-dollars when it comes to video entertainment. This is again, an opportunity for Netflix.

Source: MPAA 2018 THEME report

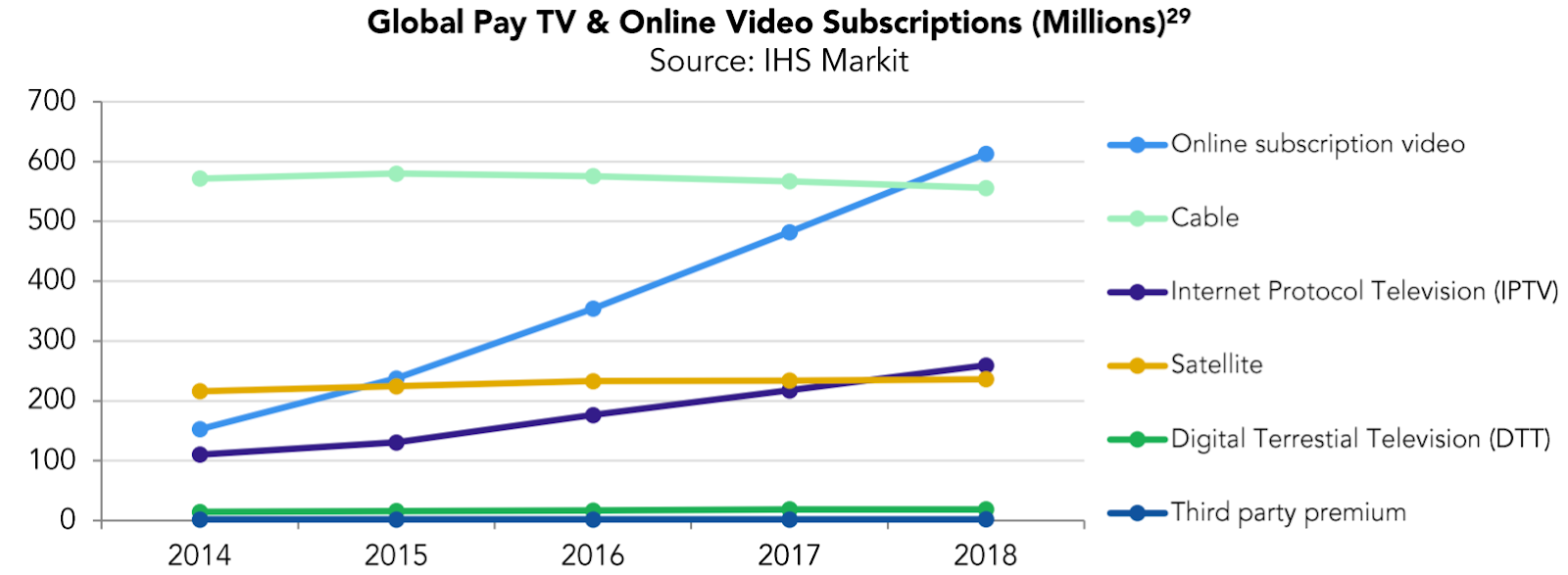

The number of subscribers to online subscription video services across the world has also exploded in the past few years. This shows how streaming is indeed a fast-growing market – and in our opinion, the way of the future for video entertainment.

Source: MPAA 2018 THEME report

As a last point on the market opportunity for Netflix, as large as the company already is in the US, the company mentioned in its 2019 second-quarter shareholders’ letter that it still accounts for only 10% of consumers’ television viewing time in the country, and even less of their mobile screen time.

2. A strong balance sheet with minimal or a reasonable amount of debt

At first glance, Netflix does not cut the mustard here. As of 30 June 2020, Netflix’s balance sheet held US$15.8 billion in debt and just US$7.1 billion in cash. This stands in sharp contrast to the end of 2014, when Netflix had US$900 million in debt and US$1.6 billion in cash. Moreover, Netflix has lost US$10.8 billion in cumulative free cash flow from 2014 to 2019.

But we’ll explain later why we think Netflix has a good reason for having so much debt on its balance sheet.

3. A management team with integrity, capability, and an innovative mindset

On integrity

Netflix is led by co-CEO Reed Hastings, 59, who also co-founded the company in 1997. The long-tenure of Hastings in Netflix is one of the things we like about the company.

Although Hastings is paid a tidy sum to run Netflix – his total compensation in 2019 was US$38.6 million – his pay has reasonably tracked the company’s revenue growth. From 2014 to 2019, Netflix’s revenue increased by 266% from US$5.5 billion to US$20.2 billion. This matches the 249% jump in Hastings’ total compensation from US$11.1 million to US$38.6 million over the same period.

Hastings also owns 5.25 million Netflix shares as of 8 April 2020, along with the option to purchase 4.01 million shares. His ownership stake alone is worth around US$2.57 billion at the share price of US$489 (as of 1 August 2020), which will very likely align his interests with other Netflix shareholders such as Compounder Fund.

On capability and innovation

Netflix was an early pioneer in the streaming business when it launched its service in 2007. In fact, Netflix probably wanted to introduce streaming even from its earliest days. Hastings said the following in a 2007 interview with Fortune magazine:

“We named the company Netflix for a reason; we didn’t name it DVDs-by-mail. The opportunity for Netflix online arrives when we can deliver content to the TV without any intermediary device.”

When Netflix first started streaming, the content came from third-party producers. In 2013, the company launched its first slate of original programming. Since then, the company has ramped up its original content budget significantly.

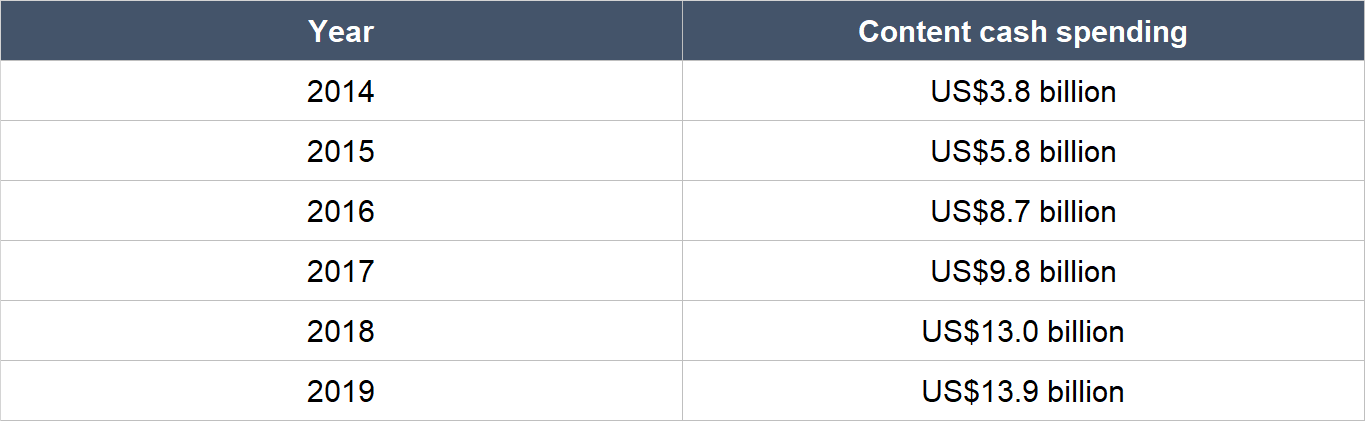

The table below shows Netflix’s total content cash spending from 2014 to 2019. There are two things to note. First, total content spending has been increasing each year and has jumped by around 266% for the entire time frame. Second, original content accounted for (a) around 85%, or US$11 billion, of Netflix’s content spending in 2018, and (b) most of Netflix’s content spending in 2019.

Source: Netflix earnings

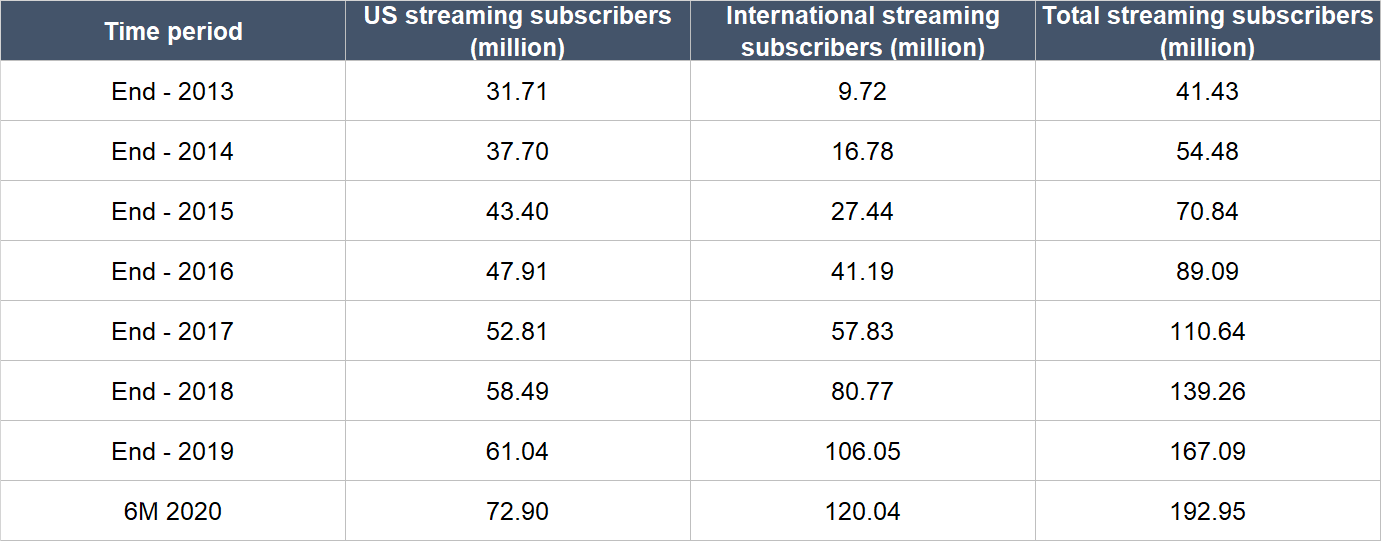

All that content-spending has resulted in strong subscriber growth, which is clearly seen from the table below. Netflix’s decade-plus head start in streaming – a move that we credit management for – has also given the company a tremendously valuable asset: Data. The data lets Netflix know what people are watching, and in turn allows the company to predict what people want to watch next. This is very helpful for Netflix when producing original content that keeps viewers hooked.

Source: Netflix earnings (6M 2020 numbers for US streaming subscribers refers to US + Canada)

And Netflix has indeed found plenty of success with its original programming. For instance, in 2013, the company became the first streaming provider to be nominated for a primetime Emmy. In 2018 and 2019, the company snagged 23 and 27 Emmy wins, respectively. Earlier this year, Neflix set a new record for 2020 Emmy nominations with 160, beating long-time rival HBO’s 137 from 2019. From a viewership perspective, here are some examples:

- The third season of Stranger Things (Ser Jing loves the show!), launched in the third quarter of 2019, had 64 million households tuning in within the first month of its release

- Adam Sandler’s comedy film, Murder Mystery, welcomed views from over 73 million households in the first month of its release in June 2019

The move into originals by management has also proved to be prescient. Netflix’s 2019 second quarter shareholders’ letter name-dropped nine existing and would-be streaming competitors – and there are more that are unnamed. We think Netflix’s aforementioned data, and its strong library of original content, should help it to withstand competition. Indeed, the launch of The Walt Disney Company’s competing streaming service, Disney+, has not dented Netflix’s subscriber growth. Disney+ launched in November 2019 in the US, Canada, and the Netherlands, and quickly amassed 54.5 million subscribers by early May. But from the third quarter of 2019 to the second quarter of 2020, Netflix’s subscriber count in the US and Canada grew from 67.11 million to 72.90 million and also increased in each sequential quarter.

The current COVID-19 pandemic has also given us useful information on the quality of Netflix’s management team. Restriction of human movement and gatherings is one of the ways that many governments around the world have used to fight the pandemic. This has resulted in operational difficulties for content producers, leading to media reports of a dearth of new content in the coming months. Netflix is also facing constraints since the start of 2020 on producing content, but it has a content slate that extends into 2021.

Speaking of content, Ted Sarandos, 55, was promoted to co-CEO of Netflix in July 2020. Sarandos has been responsible for all of Netflix’s content operations since 2000 and was a driving force in Netflix’s transition into original content production that started in 2013. Even as co-CEO, one of Sarandos’s key responsibilities lie with management of Netflix’s content. We think Sarandos is the second most important executive in Netflix after Hastings, and we think his promotion is a great development – it is likely to encourage Sarandos to continue staying at Netflix for years to come. It’s also worth pointing out that Hastings has no intention to step down any time soon – he mentioned in Netflix’s 2020 second quarter earnings conference call that he’s “in for a decade.”

We also want to point out the unique view on Netflix’s market opportunity that management has. Management sees Netflix’s competition as more than just other streaming providers. In Netflix’s Long-Term View letter to investors, management wrote:

“We compete for a share of members’ time and spending for relaxation and stimulation, against linear networks, pay-per-view content, DVD watching, other internet networks, video gaming, web browsing, magazine reading, video piracy, and much more. Over the coming years, most of these forms of entertainment will improve.

If you think of your own behavior any evening or weekend in the last month when you did not watch Netflix, you will understand how broad and vigorous our competition is. We strive to win more of our members’ “moments of truth”.”

Having an expansive view on competition lessens the risk that Netflix will get blindsided by competitors, in our view.

4. Revenue streams that are recurring in nature, either through contracts or customer-behaviour

Netflix’s business is built entirely on subscriptions, which generate recurring revenue for the company. As we already mentioned, nearly all of Netflix’s revenue in 2019 (98.5%) came from subscriptions to its streaming service, while subscriptions to the legacy DVD-by-mail service accounted for the remaining small chunk of revenue.

But just having a subscription model does not equate to having recurring revenues. If your business has a high churn rate (the rate of customers leaving), you’re constantly filling a leaky bucket. That’s not recurring income. According to a recent estimate from a third-party source (Lab42), Netflix’s churn rate is just 7%, and is much better than its competitors.

5. A proven ability to grow

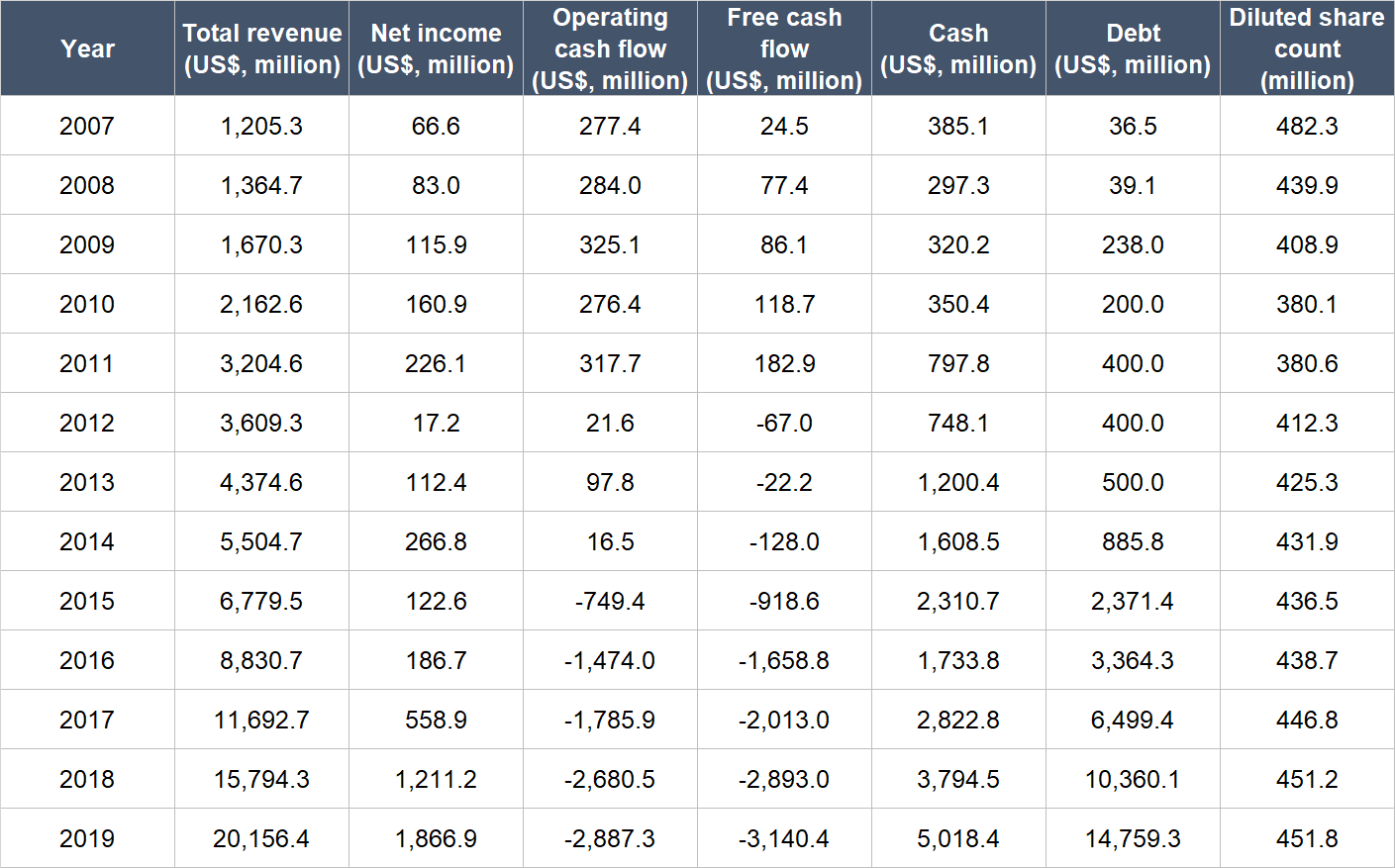

2007 was the year Netflix first launched its streaming service. This has provided the impetus for the company’s stunning revenue and net income growth since, as the table below illustrates. It’s good to note too that Netflix’s diluted share count has actually declined since 2007; this shows that the company has not been diluting shareholders.

Source: Netflix annual reports

In our explanation of this criterion, we mentioned that we’re looking for “big jumps in revenue, net profit, and free cash flow over time.” We also said that “we are generally wary of companies that (a) produce revenue and profit growth without corresponding increases in free cash flow.” So why are we investing in Netflix shares when its free cash flow has cratered over time and has been deeply negative for a number of years?

This is our view on the situation. Netflix has been growing its original content production, as mentioned earlier, and the high capital outlay for such content is mostly paid upfront. But the high upfront costs are for the production of content that (1) could have a long lifespan, (2) can be delivered to subscribers at minimal cost, and (3) could satisfy subscribers who have high lifetime value (the high lifetime value is inferred from Netflix’s low churn rate). In other words, Netflix is spending upfront for content, but has the potential to reap outsized rewards over a long period of time at low cost. The shelf-life for good content could be decades, or more – for instance, Seinfeld, a sitcom in the US, is still popular 30 years after it was produced.

In Netflix’s Long-Term View shareholder’s letter, management wrote (emphases are ours):

“People love movies and TV shows, but they don’t love the linear TV experience, where channels present programs only at particular times on non-portable screens with complicated remote controls. Now streaming entertainment – which is on-demand, personalized, and available on any screen – is replacing linear TV.

Changes of this magnitude are rare. Radio was the dominant home entertainment media for nearly 50 years until linear TV took over in the 1950’s and 1960’s. Linear video in the home was a huge advance over radio, and very large firms emerged to meet consumer desires over the last 60 years. The new era of streaming entertainment, which began in the mid-2000’s, is likely to be very big and enduring also, given the flexibility and ubiquity of the internet around the world. We hope to continue being one of the leading firms of the streaming entertainment era.”

We agree with Netflix’s management that the company is in the early stages of a multi-decade transition from linear TV to internet entertainment at a global scale. With this backdrop, along with what we mentioned earlier on Netflix’s business model of spending upfront to produce content with long monetisable-lifespans, we’re not troubled by Netflix’s negative and deteriorating free cash flow for now. Netflix’s management also said in 2019 that they expect the company’s free cash flow to improve in 2020 compared to 2019, and “to continue to improve annually beyond 2020.”

The presence of COVID-19 has given us a glimpse of Netflix’s ability to produce cash from its business. During the first half of 2020, Netflix produced US$1.1 billion in free cash flow, compared to negative free cash flow of US$1.0 billion for the same period a year ago. A pause in production has pushed Netflix’s cash spending on content into the second half of 2020 and into 2021. In Netflix’s 2020 second-quarter earnings update, management said that the company’s free cash flow margin (free cash flow as a percentage of revenue) could be around 15% at steady-state. Management also reiterated their belief that Netflix’s cash-burn had peaked in 2019:

“Due to the pause in production from the pandemic combined with higher-than-forecast paid net adds year to date, we now expect free cash flow for the full year 2020 to be breakeven to positive, compared with our prior expectation for -[US]$1 billion or better. As we indicated last quarter, in 2021 we project that full year free cash flow will dip back to being negative again, although we believe the FCF deficit will be materially better than our peak deficit level of -[US]$3.3 billion in 2019. There has been no material change in our overall estimated timetable to reach consistent annual positive FCF within the next few years.”

And speaking of the first half of 2020, Netflix has continued to produce strong revenue growth in the period – revenue was up 26.2% to US$11.9 billion from a year ago.

6. A high likelihood of generating a strong and growing stream of free cash flow in the future

We understand that Netflix’s free cash flow numbers for the past few years look horrible. But Netflix is a subscription business that enjoys a low churn rate. It is also spending plenty of capital to pay upfront for long-lived assets (the original content). We believe that these provide the potential for Netflix to generate high free cash flow in the future, if it continues to grow its subscriber base.

Valuation

“Cheap” is definitely not a good way to describe Netflix’s shares. The company has trailing earnings per share of US$5.92 against Compounder Fund’s average purchase price of US$500. That’s a price-to-earnings (PE) ratio of around 84. But Netflix has the tailwinds of expanding margins and revenue growth. The company is targeting an operating margin of 16% in 2020 and 19% in 2021; for perspective, the operating margins in 2019, 2018 and 2017 were 13%, 10%, and 7% respectively.

Let’s assume that in five years’ time, Netflix can hit 380 million subscribers worldwide (nearly twice the current subscriber count of 192.95 million, which equates to annual growth of around 15%) paying US$17 per month on average (representing annual growth of around 10% from the average revenue per user of US$10.79 seen currently).

With the assumptions above, Netflix’s revenue in five years would be US$77.5 billion. If we apply a 20% net profit margin, the company would then earn US$15.5 billion in net profit. With an earnings multiple of just 30, Netflix’s market capitalisation in five years would be US$465 billion, more than double from the market capitalisation of US$220 billion at our average purchase price. This equates to an annualised return of 16%. We think our assumptions are conservative. Higher subscriber numbers, higher average revenue per user, and fatter margins will lead to much higher upside.

The risks involved

There are four key risks that we see in Netflix.

First, Netflix’s cash burn and weak balance sheet is a big risk. We think Netflix’s strategy to produce original content is sound. But the strategy necessitates the spending of capital upfront, which has led to debt piling up on the balance sheet. We will be watching Netflix’s free cash flow and borrowing terms. For now, Netflix depends on the kindness of the debt markets – that’s a situation the company should be getting itself out of as soon as possible.

Second, there’s competition. Tech giant Apple and entertainment companies Disney, HBO, and NBC recently launched their own streaming offerings. As we mentioned earlier, we think Netflix should be able to withstand competition. In fact, we think the real victims will be cable TV companies. This is not a case of Netflix versus other streaming options – this is a case of streaming services versus cable. Different streaming services can co-exist and thrive. And even if the streaming market has a shakeout, Netflix, by virtue of its already massive subscriber base, should be one of the victors. But we can’t know for sure. Only time will tell. Netflix’s subscriber numbers in the future will show us how it’s dealing with competition.

Third, there’s key-man risk. Reed Hastings and Ted Sarandos have been phenomenal leaders at Netflix. If Hastings and/or Sarandos were to leave Netflix for whatever reason, we’ll be concerned.

The fourth risk is COVID-19. The virus’s future infection trends around the world could create material uncertainty for Netflix’s content production schedule. If there’s a long dry season for Netflix in terms of new content, subscriber retention and addition could be tricky.

Summary and allocation commentary

Despite already having nearly 193 million subscribers worldwide, Netflix still has a large market opportunity to conquer. The company also has an excellent management team with integrity, and has an attractive subscription business model with sticky customers. Although Netflix’s balance sheet is currently weak and it has trouble generating free cash flow, we think the company will be able to generate strong free cash flow in the future.

There are certainly risks to note, such as a high debt-burden, high cash-burn, and an increasingly competitive landscape. Key-man departures, if they happen, could also significantly dent Netflix’s growth prospects.

We initiated a 4.0% position in Netflix with Compounder Fund’s initial capital. Netflix effectively created the streaming market on its own, and so it is one of those rare companies that are creating tailwinds rather than just riding on them. It has also demonstrated a long history of growth. We recognise the risks involved with Netflix, but the positive traits it has make us comfortable with a 4.0% position.

And here’s an important disclaimer: None of the information or analysis presented is intended to form the basis for any offer or recommendation; they are merely our thoughts that we want to share.