Compounder Fund: Medistim Investment Thesis - 07 Aug 2020

Data as of 1 August 2020

Medistim ASA (MEDI.OL) is one of the 40 companies in Compounder Fund’s initial portfolio. This article describes our investment thesis for the company.

Company description

Founded in 1984, Medistim is the smallest company by market capitalisation (NOK 4.33 billion as of 1 August 2020, which is around S$650 million) that we have invested in so far for Compounder Fund. It is also currently the only company in Compounder Fund’s portfolio that is listed on the Oslo Stock Exchange in Norway (the company listed in Norway in 2004 and is headquartered in the country, in the city of Oslo).

The company pulled in NOK 363.7 million (around S$54.6 million) in revenue in 2019. Most of the revenue (81%) is associated with Medisitm’s medical devices. The important ones are Medisitm’s key fourth generation MiraQ platform (the latest) and the third generation VeriQ platform.

MiraQ is an integrated platform that combines high frequency ultrasound (HFUS) imaging and transit time flow measurement (TTFM) technologies to image and measure blood flow, respectively, in the human body. The platform is currently used during CABG (coronary artery bypass grafting) and vascular surgeries. VeriQ is used for the same purposes, but earlier this year, Medistim stopped the production and sale of the platform to concentrate commercial efforts on the newer generation MiraQ. Globally, there is an installed base of over 2,700 Medisitm devices in more than 60 countries at the moment.

From a geographical perspective, Europe is Medistim’s largest market, accounting for 45% of the company’s revenue in 2019. The US is the next most important market, with a 37% share. Asia and other parts of the world account for the rest.

Investment thesis

We have laid out our investment framework in Compounder Fund’s website. We will use the framework to describe our investment thesis for Medistim.

1. Revenues that are small in relation to a large and/or growing market, or revenues that are large in a fast-growing market

Cardiac and vascular disease are two of the most common diseases in the developed world. Across the globe on an annual basis, more than 700,000 patients undergo CABG surgery, while there are more than 600,000 vascular surgery procedures performed. During these surgeries, the ability to visualise and measure blood flow helps surgeons to spot surgical defects early and take the necessary steps to improve patient outcomes – this is where Medistim’s platforms come in, and where we think there is significant room for growth for the company.

Growth in market penetration within CABG surgeries

In parts of Europe, Medistim’s medical devices are already recognised as an important aspect of CABG surgical procedures. Specifically, when it comes to CABG surgeries, the company’s devices are: (1) Included in the guidelines from the European Society of Cardiology and European Association for Cardio-Thoracic Surgery as standard of care; and (2) recognised as a standard of care by the British National Institute for Health and Clinical Excellence (NICE). In 2018, NICE updated its recommendation for adopting Medistim’s devices in the UK.

But interestingly, many surgeons still use their fingertips to feel for pulse palpations as an indicator of blood flow during CABG procedures, even though a blood vessel can still pulsate without any flow of blood. In 2019, 60% of all CABG surgeries conducted annually did not use any form of quality assurance; of the 40% that do, Medistim accounted for 33% with other players taking up the remaining 7%. This also means that Medistim has a huge share of its penetrated market (82% of the pie), making it by far the largest player in its particular niche, or an effective monopoly.

In the USA, Medistim’s most important market for CABG surgeries (around 33% of global CABG surgeries are performed in the country), about 70% of procedures there are performed with no quality assurance; Medistim has a penetration rate of just 23% in the country. Within countries/regions such as Japan, Germany, and Scandinavia, Medisitm’s penetration is around 80%. We thus think there is plenty of room for the USA to catch up.

In order to increase penetration rates, Medistim is focused on getting TTFM recognised in more countries around the world as standard of care for CABG procedures.

Higher device demand and large addressable market

In 2014, Medistim launched its MiraQ platform, which combines TTFM and HFUS imagining capabilities. In 2015, the company partnered Oxford University and several other prestigious cardiac surgery centres in the West to launch a multi-year medical study named REQUEST. The study involved more than 1,000 CABG patients and was meant to investigate if the combination of TTFM and HFUS imaging will lead to better clinical outcomes during CABG surgeries. It turns out that using TTFM with HFUS imagining does indeed improve clinical outcomes and results from REQUEST were published in the April 2020 edition of The Journal of Thoracic and Cardiovascular Surgery. We think that the positive results from REQUEST could lead to higher demand for MiraQ in the future.

A year after Medistim launched the MiraQ platform, the company introduced a variant – named MiraQ Vascular – that focuses on vascular surgeries. We mentioned earlier that there are around 600,000 vascular surgeries performed in the world annually. Within the broad scope of vascular surgeries, MiraQ Vascular is focused on peripheral bypass surgery (200,000 procedures per year) and carotid endarterectomy, or CEA (225,000 procedures per year). We think there’s a large opportunity within the vascular surgery space for Medistim, as there was already demand for the company’s device from vascular surgeons from as early as before 2011 even though its products were designed for cardiac surgery. Just 12% of the company’s total revenue in 2019 came from vascular procedures.

Medistim also has a perpetual license to sell a blood-flow-measurement device worldwide that is manufactured by a third-party (em-tec). This device, which also uses TTFM technology, is an entry-level model that Medisitm named SonoQ. In 2019, SonoQ generated just NOK 2.0 million in revenue. India is one of SonoQ’s most important target markets. The country sees only 150,000 coronary artery bypass procedures performed annually, which is very low compared to its population of 1.3 billion. India is also a price-sensitive market, and thus a potentially good fit for SonoQ.

All told, in monetary terms, here are the sizes of Medisitm’s global addressable markets:

- NOK 1 billion within CABG surgeries

- NOK 1 billion for cardiac procedures outside of CABG (this addressable market is driven by MiraQ’s imaging functions, which makes it relevant in other cardiac surgical procedures)

- NOK 1 billion within vascular surgeries

For perspective, Medistim’s revenue in the 12 months ended 31 March 2020 is only NOK 378.1 million, which is less than 13% of its total market opportunity.

We think it’s also worth noting that the world population is both rising and aging. This means it is very likely that the number of cardiac and vascular surgeries performed annually in the world will at the very least remain stable over the long run. We don’t wish to downplay the human suffering that comes with disease, but our globe’s population trends provide Medistim with room for growth.

2. A strong balance sheet with minimal or a reasonable amount of debt

As of 31 March 2020, Medistim has NOK 85.4 million in cash and just NOK 6.8 million in interest-bearing debt. This makes for a robust balance sheet.

Importantly, Medistim has also been consistently generating free cash flow from its business, which we will discuss later.

3. A management team with integrity, capability, and an innovative mindset

On integrity

Medistim’s led by CEO Kari Krogstad, 55, who has been in the role since September 2009. She, along with many other members of Medistim’s senior management team, have long tenures with the company, as shown in the table below. We appreciate their years of experience.

Source: Medistim website

During Krogstad’s tenure, Medistim’s share price has increased by nearly 1,000%. Meanwhile, the company’s revenue and profit increased by 98% and 132%, respectively, from 2012 to 2019. Over the same period, Krogstad’s total compensation increased by just 57% from NOK 2.78 million to NOK 4.36 million (If you’re wondering, the earliest compensation data we could find for Medistim is for 2012). We’re comforted by the much faster growth in Medisitm’s share price and business fundamentals when compared to Krogstad’s compensation.

There is a negative in terms of alignment of interests between Medistim’s shareholders and the company’s leaders: Insider ownership is really low. As of 1 August 2020, Krogstad and Jakobsen owned just 79,302 and 40,096 Medistim shares, respectively. Based on Medistim’s share price of NOK 235 as of 1 August 2020, these translate to stakes of around S$2.8 million and S$1.4 million, respectively. We don’t think the low insider ownership is a deal-breaker, since Krogstad owned just 40,000 Medistim shares at the end of 2012; the low ownership has not stopped her from growing the business well.

On capability and ability to innovate

Medistim’s vision is for its technology to “benefit all patients and surgeons, regardless of where in the world they are located,” and that its “devices and solution represent standard clinical practice in all countries.” This is a simple but worthy vision, and one that Krogstad has worked towards.

Over the years, Medistim’s CEO and her team have done a good job at steadily growing: (1) The total installed base of Medistim devices globally; (2) the number of CABG procedures in the US that use the company’s devices; (3) Medistim’s penetration rate for CABG procedures in the US; and (4) Medistim’s penetration rate for CABG procedures worldwide. These are important numbers for us when assessing the level of demand for Medistim’s devices and they are shown in the table below:

Source: Medistim annual reports

Under Krogstad’s watch, Medistim launched its MiraQ platform (in 2014), initiated the REQUEST study (in 2015), and introduced a new specialised product for vascular surgeries (MiraQ Vascular in 2015). These are all shrewd moves that are bearing – or are likely going to bear – fruit and they gave us confidence in the leadership of Krogstad and her team.

4. Revenue streams that are recurring in nature, either through contracts or customer-behaviour

Earlier, we mentioned that 81% of Medistim’s NOK 363.7 million in revenue in 2019 was associated with Medistim’s medical devices. The key products in Medistim’s portfolio are its MiraQ and VeriQ platforms. These two platforms bring recurring revenues to Medistim in two ways:

- Medistim sells the MiraQ and VeriQ platforms for a one-time charge in countries outside of the USA. But use of the platforms require probes, which have to be replaced after a certain number of uses (50 times for blood-flow-measurement probes, and 100 times for the imaging probes), thus bringing recurring revenues for Medistim. The platforms cost between €45,000 and €90,000 each (around S$73,000 to S$146,000), while the probes cost between €1,8000 and €2,000 each for blood-flow-measurement, and €10,000 each for imaging.

- In the USA, Medistim also has an alternate business model where it leases its machines to hospitals, or puts its machines in hospitals for free. The company then earns revenue through monthly lease payments or a pay-per-use model. Under the lease model, Medistim also earns revenue from the sale of blood-flow-measurement and imaging probes to hospitals. Under the pay-per-use model, the cost of the probes are already included in the per-use fee; the pay-per-use model also comes with a minimum use clause.

We estimate that 57% of Medistim’s total revenue in 2019 came from the sale of probes, lease revenue, and pay-per-use revenue.

19% of Medistim’s total revenue in 2019 (NOK 68.1 million out of NOK 363.7 million) came from the distribution of third-party products in Norway and Denmark. The products consist mainly of instruments and consumables used in surgery. But we can’t determine exactly how much of Medistim’s revenue from the distribution of third-party products is recurring in nature.

5. A proven ability to grow

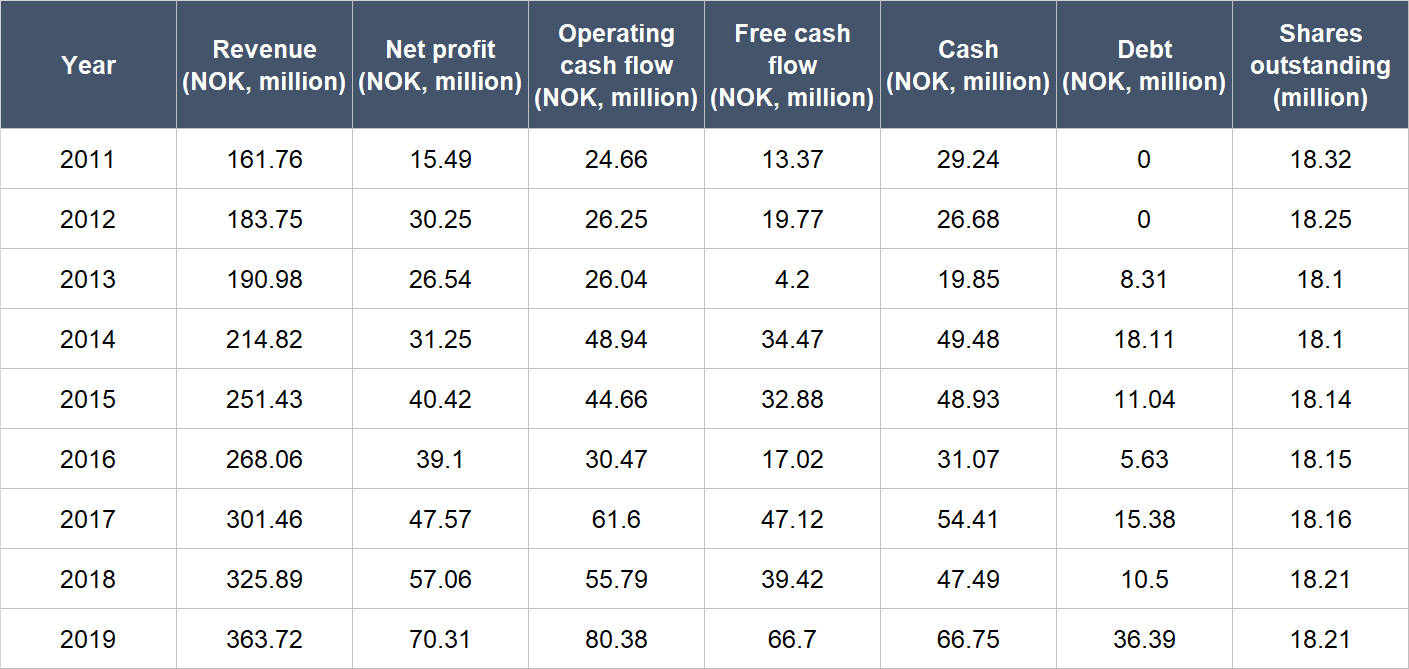

The table below shows the important financial figures for Medistim from 2011 to 2019 (2011 is our starting point because we couldn’t find complete financial numbers for the company from earlier):

Source: Medistim annual reports

A few key points about Medistimo’s financials:

- Net revenue compounded at a decent rate of 10.7% per year from 2011 to 2019; over the last five years from 2014 to 2019, the company’s annual topline growth was similar at 11.1%.

- Net profit surged by 20.8% per year from 2011 to 2019, and grew in most years (only 2013 and 2016 saw declines). Medistim’s net profit growth from 2014 to 2019 was similarly healthy at 17.7%.

- Medistim’s operating cash flow is a tad bumpy, but it was consistently positive and climbed at a healthy clip of 15.9% annually from 2011 to 2019. The growth rate from 2014 to 2019 was still decent at 10.4% per year.

- Free cash flow was consistently positive too, and had stepped up from 2011 to 2019 at a rapid clip of 22.3% per year. The annual growth in free cash flow from 2014 to 2019 was 14.1% – not too shabby.

- Medistim kept its balance sheet strong throughout from 2011 to 2019, with a significantly higher cash position compared to debt.

- There’s effectively been no dilution at Medistim for the entire time frame we’re studying. In fact, the company’s share count even declined slightly from 18.32 million in 2011 to 18.21 million in 2019.

Medistim continued to grow in the first quarter 2020. Revenue was up 16.2% to NOK 103.1 million, driving a 32.2% jump in net income to NOK 21.1 million (diluted earnings per share grew 31.8% to NOK 1.16). Operating cash flow and estimated free cash flow came in at NOK 22.6 million and NOK 21.0 million, respectively, and were up 107.6% and 175.7% from a year ago. The balance sheet, as mentioned earlier, still remains strong – the cash position at the end of 2020’s first quarter was significantly higher than the debt position.

6. A high likelihood of generating a strong and growing stream of free cash flow in the future

There are two reasons why we think Medistim excels in this criterion.

First, the company has done well in producing free cash flow from its business for a long time. Its free cash flow had been consistently positive from 2011 to 2019, and the free cash flow margin (free cash flow as a percentage of revenue) averaged at 11.4% from 2011 to 2019. In the first quarter of 2020, Medistim’s free cash flow margin was 20.4%

Second, there’s still plenty of room to grow for Medistim, as we discussed earlier. This should lead to a higher installed base for the company’s platforms over time. In turn, the higher installed base should drive robust growth in the company’s revenue and thus free cash flow.

Valuation

We bought Medistim shares for Compounder Fund at an average price of NOK 231.98 each. This translates to trailing price-to-earnings and price-to-free cash flow ratios of 56 and 53, respectively, at our average purchase price. The chart below shows the two ratios over the past five years. You can see that the valuations we bought our shares at are high relative to history.

But there are a few reasons why we think Medistim deserves a premium valuation:

- The company has a long runway for growth ahead. Moreover, the nature of its business (medical devices that improve surgical outcomes and that come with recurring revenues) and its effective monopoly position, make us think that Medistim can continue growing reliably.

- There is a strong possibility that the company’s revenue growth rates in the years ahead could be materially higher than what was achieved from 2014 to 2019, because of the recent publication of the results from the REQUEST study.

The risks involved

COVID-19 is the biggest risk we’re watching with Medistim. In the first quarter of 2020, Medistim was largely unaffected by the new respiratory virus: Only third-party sales in Norway to hospitals were affected. Otherwise, the company’s employees were healthy and its supply chain and production activities were intact.

But Medistim also commented in its 2020 first quarter earnings update in late April that it anticipates COVID-19 to have negative impacts on its revenue for the second quarter of 2020. The virus has caused many healthcare facilities around the world to defer elective surgeries to conserve resources to combat the virus; if the reduced activity level were to continue for a long time, Medistim’s consumables business would be impacted. But the company also mentioned that hospitals are starting to open up for regular practice. Most importantly, “serious medical conditions such as heart disease and risk of stroke cannot be left untreated for too long” – this means that CABG and vascular surgeries still have to be conducted, which benefits Medistim. Our current assumption is that COVID-19 will at the most be a bump in the road for Medistim, but we’re watching how the situation plays out.

Competition is another risk we’re watching. Medistim is currently a leader in its field. We mentioned earlier that Medistim’s market opportunity is NOK 3 billion, which is around S$450 million. We think the market opportunity is large enough to provide significant room for growth for Medistim, but it is small enough to deter many large companies from entering. Moreover, Medistim’s current commanding position – the company enjoyed an 82% share of the penetrated market in 2019, as discussed earlier – also acts as a deterrent. Although we think the odds of Medistim having to face significant new competition is low, the risk is not zero. If competition should heat up in the future, it could erode Medistim’s margins as well as slow the company’s growth.

It is also hard to ignore Medistim’s premium valuation – this is the third risk we’re keeping an eye on. Any slowdown in growth or hiccups along the way could easily lead to a lower P/E ratio for Medistim and thus a steep decline in the company’s share price.

Summary and allocation commentary

Medistim’s penetration rate in the CABG market worldwide is currently low, considering that its machines are already recognised as a standard of care in Europe. Education of cardiac surgeons in the US on the benefits of using Medistim’s systems should see the company’s penetration rate in CABG procedures in the country grow. The recent publication of the results from the REQUEST study in the Journal of Thoracic and Cardiovascular Surgery should help improve the adoption rate of Medistim’s machines around the world. Another important pillar of growth is Medistim’s relatively newer foray into vascular surgery.

We also favour companies that have high levels of recurring revenues. Medistim’s business model includes the sale of consumables as well as charging for its machines on a leasing or pay-per-use model; these generate recurring revenues for the company. In 2019, 57% of the company’s revenue came from recurring sources.

Medistim’s CEO, Kari Krogstad, has fair compensation and has overseen the company for more than a decade, producing solid growth over the years while keeping the balance sheet strong.

There are risks to note, as it is with any investment. COVID-19, competition, and a high valuation are the key ones we’re watching with Medistim.

We initiated a 2.5% position in Medistim with Compounder Fund’s initial capital. The company has all the traits that we want in Compounders. But in balancing its stable growth profile with its high valuation, we think this weighting is appropriate from a risk/reward perspective.

And here’s an important disclaimer: None of the information or analysis presented is intended to form the basis for any offer or recommendation; they are merely our thoughts that we want to share.