Compounder Fund: Haidilao/Super Hi Sell Thesis - 18 Mar 2026

Data as of 17 March 2026

We first invested in Haidilao (SEHK: 6862) for Compounder Fund’s portfolio in July 2020. Our investment thesis for the company can be found here. In December 2022, Haidilao spun off its international operations into a separate entity named Super Hi International (SEHK: 9658) and Haidilao shareholders at that point in time were distributed Super Hi shares. We described our “inheritance” of Super Hi in the “Portfolio changes” section of Compounder Fund’s 2022 fourth-quarter letter. In early-January 2026, we completely exited Haidilao and Super Hi. This article describes our Sell thesis for both companies.

When we invested in the hotpot restaurant operator Haidilao, we were first and foremost impressed with its co-founder and executive chairman, Zhang Yong. We thought he was managing Haidilao in a unique and extraordinary way. For example, Haidilao provided (1) industry-leading compensation for employees, (2) a great level of autonomy to restaurant staff to delight customers, (3) a strong culture of promotion from within, and (4) profit-sharing arrangements for restaurant managers to fully align their incentives with those of the company. We thought Haidilao had “a near unreplicable competitive advantage” because of Zhang’s presence. We explained:

“As much as its competitors try to copy the form of Haidilao’s service, they can’t seem to get its substance. And we think there’s only a tiny sliver of a chance that Haidilao’s competitors can ever truly imitate the company. Haidilao’s substance comes directly from Zhang’s worldview, and it is something that is unlikely to be replicable, since no two humans are ever identical. This means that Haidilao has a near unreplicable competitive advantage.

Haidilao’s competitors have copied the company’s service standards. But in our view, Haidilao’s daring empowerment of its restaurant staff, along with management’s clever preference for evaluating restaurant managers primarily based on customer satisfaction, means that Haidilao is likely to always be the first in creating new ways to delight customers.”

In our view, Zhang’s leadership was the reason for the outstanding growth rates in Haidilao’s historical financials at the time of our investment. From 2015 to 2019, Haidilao’s revenue and net profit compounded at annual growth rates of 46.6% and 71.2%, respectively. Haidilao’s business performance in the first half of 2020 was hurt badly by the emergence of COVID-19 but we thought the difficulties would be temporary when we invested.

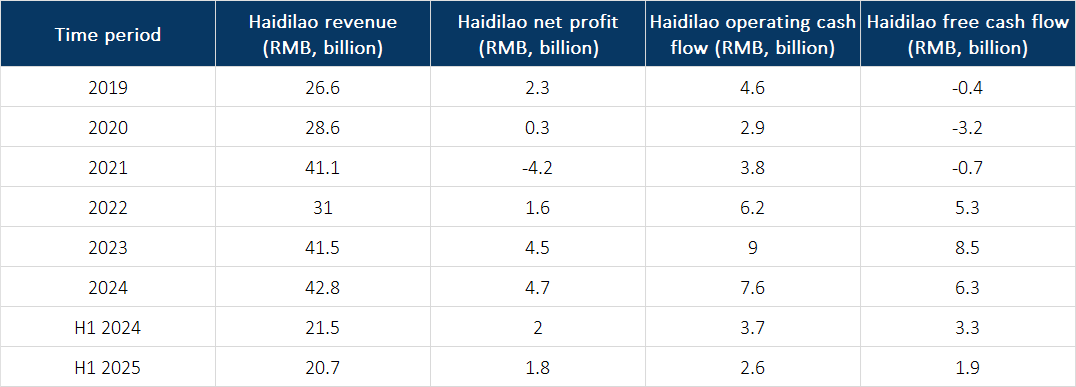

It turned out that Haidilao’s business results would remain under pressure till 2022. This was partly because of the Chinese government’s stringent anti-COVID measures (see note below) and partly because management over-expanded the business too rapidly (more on the over expansion shortly). In 2023, Haidilao staged a comeback. But unfortunately, the company’s results took a dive again in 2024 and the first half of 2025 as a result of intense competition. Haidilao’s revenue, net profit, operating cash flow, and free cash flow for 2019 to 2024, and the first half of 2025, are shown in Table 1 below.

Table 1; Source: Haidilao quarterly earnings updates and annual reports

To be clear, Haidilao’s management did not sit still when the company’s business results were deteriorating. For example:

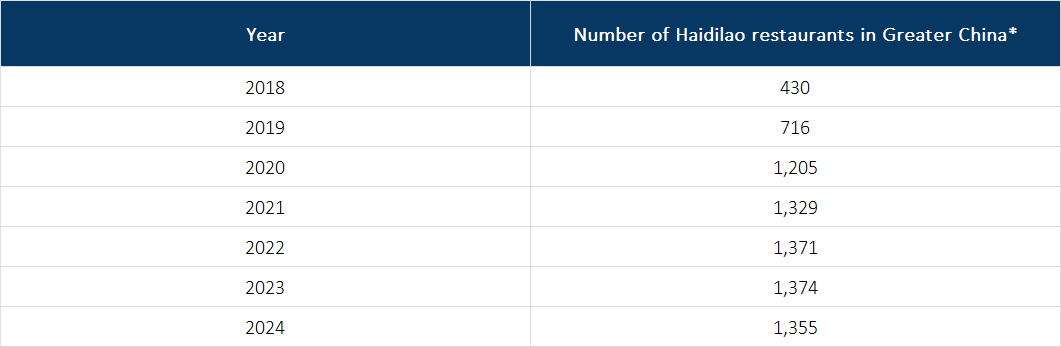

- They launched the Woodpecker plan in November 2021 to identify under-performing restaurants and either close them or restructure their operations, after realising that the rapid growth in restaurant-openings in 2020 and the earlier parts of 2021 was a mistake. The Woodpecker plan was still in force when we sold Compounder Fund’s Haidilao shares. Because of Woodpecker, Haidilao’s pace of restaurant openings has slowed down significantly, as can be seen from Table 2, which shows the number of restaurants Haidilao was operating in the Greater China region (this includes Taiwan, Macau, and Hong Kong) from 2018 to 2024.

- They launched the Pomegranate plan in the first half of 2024, which encourages Haidilao employees to explore entrepreneurial ideas within the food & beverage industry. In the first half of 2025, the company’s non-Haidilao-branded restaurants experienced a 227% year-on-year increase in revenue to RMB 596.5 million. This was mostly driven by restaurants from the Pomegranate plan. As of 30 June 2025, Haidilao has created 14 new restaurant brands, such as Yeah Qing BBQ (焰請烤肉鋪子), and Xiaohai Huoguo (小嗨火鍋), under the Pomegranate plan; there were 126 outlets with the new brands, up from 74 at the end of 2024.

- They launched a franchising model for the company in the first half of 2024, with the aim of using franchisees to penetrate lower-tier markets in China. Haidilao ended the first half of 2025 with 41 franchised restaurants, up from just 13 at the end of 2024.

Table 2; Source: Haidilao quarterly earnings updates and annual reports

*Numbers for 2018-2021 refer only to Mainland China

But despite management’s efforts, Haidilao’s results in 2024 and the first half of 2025 were still lacklustre, as illustrated in Table 3. We now think we were wrong in our initial assessment of the company possessing a near unreplicable competitive advantage – Zhang Yong’s unique worldview was not sufficient to create a moat that protected Haidilao’s turf from encroaching competitors. Because of this, we decided to sell Compounder Fund’s Haidilao shares.

Table 3; Source: Haidilao quarterly earnings updates and annual reports

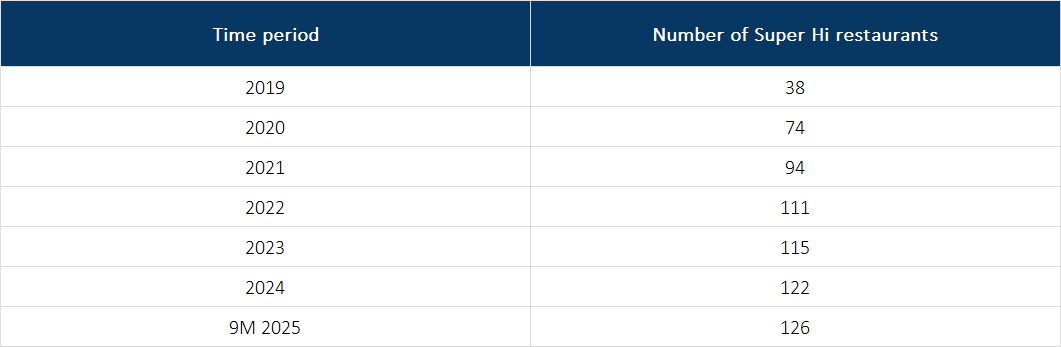

Coming to Super Hi, it also expanded too quickly in 2020 and 2021 in a similar way as Haidilao and subsequently adjusted the pace of its restaurant openings. Table 4 below shows the company’s restaurant count from 2019 to the third quarter of 2025 and the slowdown in openings starting from 2022 is apparent.

Table 4; Source: Super Hi quarterly earnings updates and annual reports

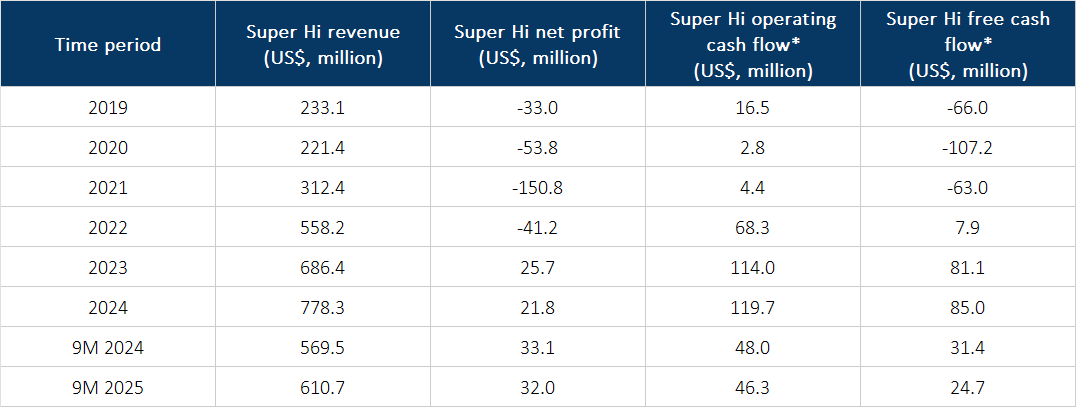

In another similarity to Haidilao, Super Hi also adopted the Pomegranate plan to incubate new restaurant brands. But in yet another similar way to Haidilao, Super Hi’s management was unable to accelerate the company’s growth in recent times. This is shown in Table 5, which contains Super Hi’s revenue, net profit, operating cash flow, and free cash flow for 2019 to 2024, and the first nine months of 2025.

Table 5; Source: Super Hi earnings updates

*For the first half of 2025

We have been viewing Super Hi and Haidiliao as effectively one entity since the former was spun-off from the later. So with us parting ways with Haidilao, Super Hi was also a natural Sell-target. It did not help Super Hi’s case that its recent growth rates, as mentioned earlier, have been lacklustre.

We made our initial investment in Haidilao at an average split-adjusted price of HK$35 per share and sold at an average price of HK$15. Super Hi’s shares closed at HK$10 on its trading-debut and we sold at an average price of HK$13. Part of the capital from the sale of Compounder Fund’s Haidilao and Super Hi shares was redeployed to some existing companies in the portfolio (in this case, the companies were Amazon, MercadoLibre, Shinhan Financial Group, and Tencent).

Note: China only fully loosened COVID-19-related restrictions in late-2022, which was much later than other major economies did.

And here’s an important disclaimer: None of the information or analysis presented is intended to form the basis for any offer or recommendation; they are merely our thoughts that we want to share. Of all other companies mentioned in this article, Compounder Fund owns shares in Amazon, MercadoLibre, Shinhan Financial Group, and Tencent. Holdings are subject to change at any time.