Compounder Fund: Fiverr Sell Thesis - 11 Jul 2025

Data as of 10 July 2025

We first invested in Fiverr International (NASDAQ: FVRR) for Compounder Fund’s portfolio in January 2021. Our investment thesis for the company can be found here. In late-March this year, we completely exited Fiverr. This article describes our Sell thesis for the company.

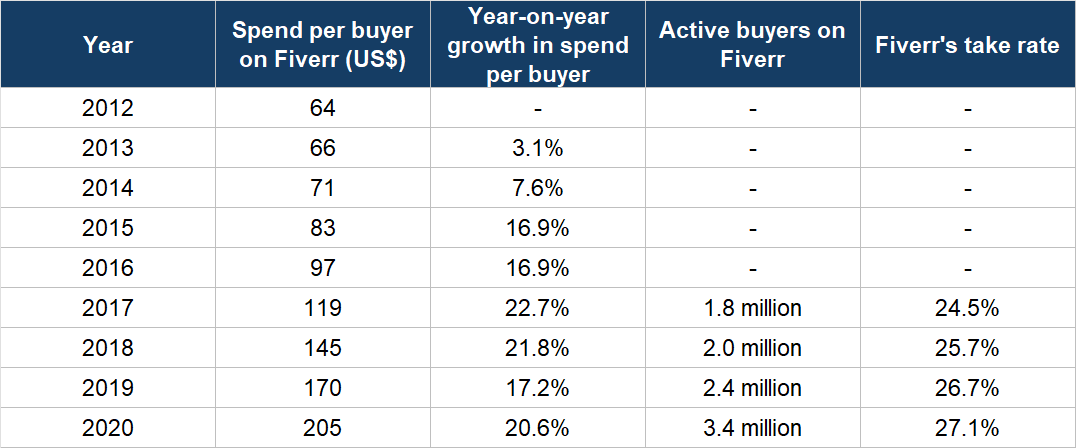

Fiverr operates an online marketplace to connect freelancers with individuals and companies who need the freelancers’ services. When we invested, Fiverr had produced impressive growth in its spend per buyer, active buyers, and take rate (the amount of revenue earned by the company per dollar of transaction), over multiple years as shown in Table 1 below. This gave us confidence that Fiverr could grow its business materially in the years ahead, given that its platform’s gross merchandise value (GMV) of just US$699.3 million in 2020 was dwarfed by its estimated serviceable addressable market of US$115 billion.

Table 1; Source: Fiverr investor presentations, annual reports, and IPO prospectus

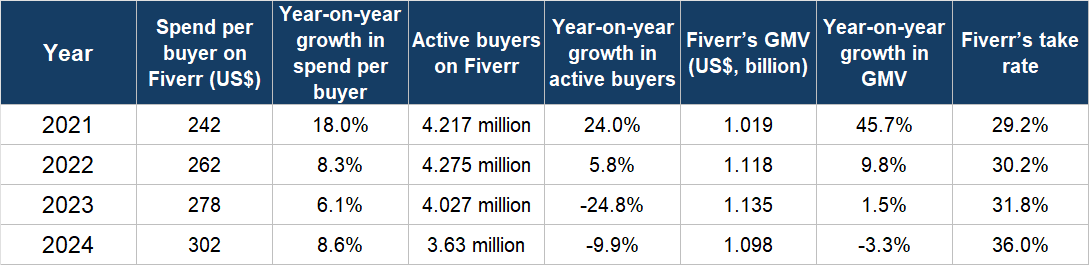

But in the years since our investment, Fiverr’s active buyers started to shrink, so much so that the company’s GMV had also begun to decline. These are shown in Table 2 below, alongside Fiverr’s spend per buyer and take rate, which, to the company’s credit, had continued their impressive climbs.

Table 2; Source: Fiverr shareholder letters and annual reports

Some portion of the decline in active buyers in recent years can be traced to management’s strategy to move upmarket and serve larger enterprises through initiatives such as Fiverr Pro, the company’s subscription plan for enterprises with higher spend on the platform. Management has also singled out weak macroeconomic conditions as a culprit for the decline in active buyers. But whatever is the cause, an inability to grow active buyers will be a serious headwind for Fiverr’s future GMV growth. Compounding the problem is Fiverr’s take rate, which has increased to 36% in 2024. The ceiling for the take rate is unclear, but we think it’s going to be harder for Fiverr to raise the take rate in the future compared to the past. On this front, management commented in the 2024 third-quarter earnings call that although Fiverr’s take rate is expected to continue growing in the next few quarters, the uplift will be modest.

We also have concerns about Fiverr’s future prospects with the emergence of artificial intelligence (AI), as we see the possibility of chatbots such as OpenAI’s ChatGPT and Anthropic’s Claude to significantly reduce demand for freelancing work in various domains. In multiple earnings calls, Fiverr’s management has repeatedly assured that AI is a boon for the company, not a bane. Here are some examples:

“[From 2023 first-quarter earnings call] We haven’t seen AI negatively impact our business. On the contrary, the categories we open to address AI-related services are booming. The number of AI-related gigs has increased over tenfold and buyer searches for AI have soared over 1,000% compared to 6 months ago, indicating a strong demand and validating our efforts to stay ahead of the curve in this rapidly evolving technological landscape. We are witnessing the increasing need for human skills to deploy and implement AI technologies, which we believe will enable greater productivity and improved quality of work when human talent is augmented by AI capabilities. In the long run, we don’t anticipate AI development to displace the need for human talent. We believe AI won’t replace our sellers; rather sellers using AI will outcompete those who don’t.

[From 2023 third-quarter earnings call] So I did address this also in how we think about next year and the fact that AI both impact the efficiency of how we work allows us to do pretty incredible things in our product. It also has an impact — positive impact on the categories that we can introduce. So again, we’re not getting into specific category breakdown. But what we’re seeing on the buyer side, I think we’ve introduced these categories, these categories continue growing.

[From 2024 first-quarter earnings call] AI continued to have a net positive impact on our business, as complex services continue to grow faster and represent a bigger portion of our business. Demand for AI-related services remained strong, as evidenced by 95% year-over-year growth in GMV from AI service categories. Chatbot development was especially popular this quarter as businesses look for ways to lean into GenAI technology to better engage with customers. For example, we have seen a hospitality company building a conversational tool for customers to manage bookings or an online learning platform creating a personalized learning menu and tutoring sessions for children. With an over 10,000 and growing AI expert pool, Fiverr has become the destination for businesses to get help implementing GenAI and take their business to the next level.

[From 2024 second-quarter earnings call] We are in the early innings of unleashing the full potential of AI in our marketplace, and we believe it will be a multiyear tailwind for us to drive product innovation and growth.”

But the declines in Fiverr’s active buyers and GMV have cast doubt in our minds on management’s view on how AI would impact the company.

We initially invested in Fiverr on the premise that its active buyers and GMV would have a long run way to grow – these would provide the foundation for the company’s free cash flow to flourish in the future. Now it appears our premise was wrong and so we decided to part ways with Fiverr. We made our initial investment in Fiverr at an average price of US$210 per share, but sold at a much lower average price of US$24. The big decline in Fiverr’s stock price might lead someone reading this to ask: “Couldn’t you have sold Fiverr earlier?” It’s a valid question. Our response will be something we shared in Compounder Fund’s Owner’s Manual:

“And on the topic of selling stocks, we will typically sell a stock in Compounder Fund’s portfolio if we find that the investment thesis is completely broken, or we have made a big mistake in our analysis. But we will be very slow to sell. The slowness is by design – it strengthens our discipline in holding onto the winners in Compounder Fund. Holding onto the winners will be a very important contributor to Compounder Fund’s long run performance.”

Part of the capital from the sale of Compounder Fund’s Fiverr shares was redeployed to some existing companies in the portfolio (in this case, the companies were Alphabet, Amazon, and The Trade Desk).

And here’s an important disclaimer: None of the information or analysis presented is intended to form the basis for any offer or recommendation; they are merely our thoughts that we want to share. Of all other companies mentioned in this article, Compounder Fund owns shares in Alphabet, Amazon, and The Trade Desk. Holdings are subject to change at any time.