Compounder Fund: dLocal Investment Thesis - 28 Oct 2021

Data as of 25 October 2021

dLocal (NASDAQ: DLO), which is based in Uruguay but listed in the USA, is a company in Compounder Fund’s portfolio that we invested in for the first time in October 2021. This article describes our investment thesis for the company.

Company description

Handling online payments in emerging economies can often be a complicated affair for global enterprises. Here’s how dLocal describes the problem in its IPO prospectus (the company was listed only in June this year):

“However, global merchants face many challenges when trying to gain access or further penetrate emerging markets. Banking penetration remains low in these countries, falling below 20% of the adult population in some cases, according to a report commissioned by us and prepared by Americas Market Intelligence, or AMI. As opposed to developed economies where card-based transactions relying on international card schemes are prevalent, local card, bank transfer-based payment methods, digital wallet, and cash-like payments, such as using Boleto in Brazil or UPI in India, and making payments at Oxxo in Mexico, are the predominant payment methods for end users in emerging markets. Furthermore, in order to gain access to emerging markets, merchants also need to:

- adhere to local compliance, regulatory, and tax frameworks,

- offer transparency and security for their end users,

- address inherent fraud risk while maximizing acceptance and conversion,

- gain insights from their transaction data, and

- identify and engage with partners that can scale as their emerging markets operations expand.”

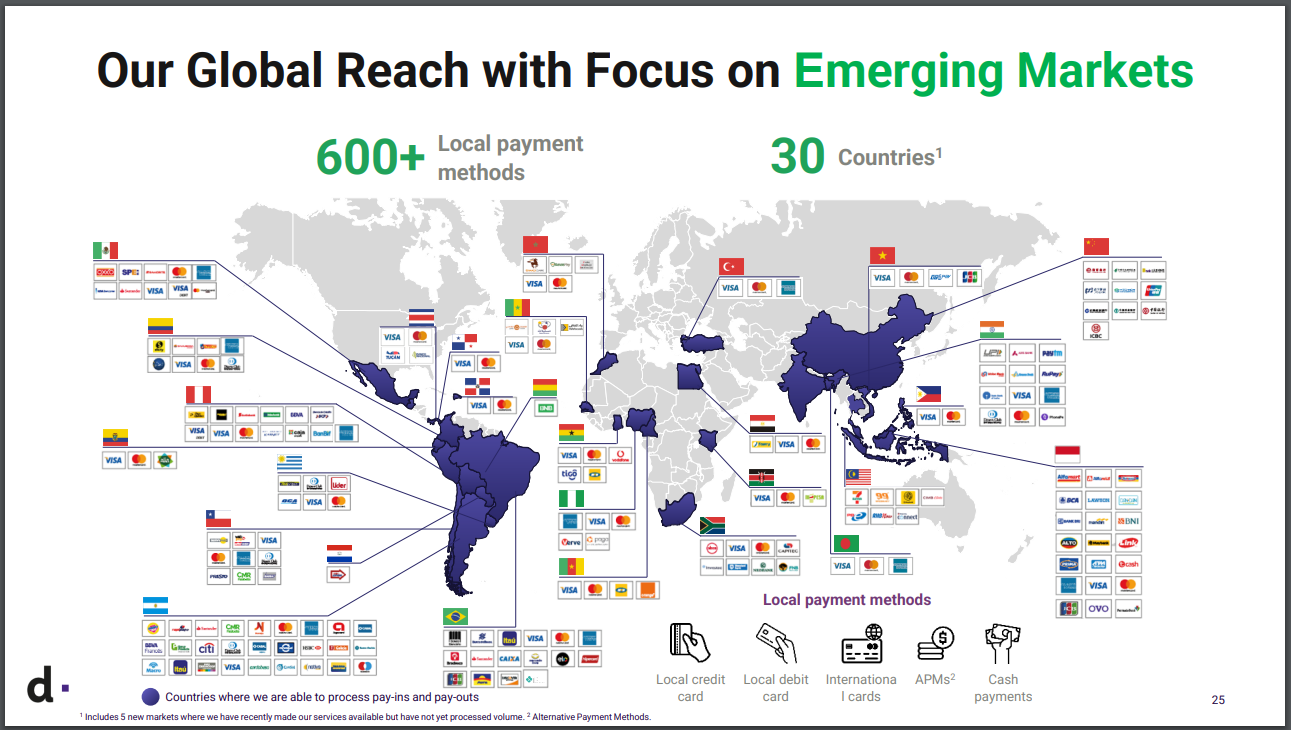

Through the One dLocal model – which features one direct API (application programming interface), one technology platform, and one contract – dLocal helps global enterprises cut through this complexity and get paid (pay-in) and make payments (pay-out) online safely and efficiently in emerging markets. dLocal’s platform provides global enterprises with a wide-variety of services that are related to pay-ins and pay-outs, including payment processing, FX management, fund collection, fund settlement, fund disbursement, fraud prevention, tax withholding management, and more. Currently, the company’s cloud-based payments platform is connected with over 600 local payment methods and allows global enterprises to conduct cross-border and local-to-local transactions in 30 countries. dLocal also recently launched a new service, named Direct Issuing, that allows global merchants to issue their own branded prepaid cards for online and in-store shopping in local currencies. Figure 1 below illustrates how dLocal’s platform works while Figure 2 shows all 30 countries that dLocal’s platform is in. These 30 countries include Mexico, Argentina, Colombia, and Chile in Latin America, India and Indonesia in Asia, and Egypt, Nigeria, and South Africa in Africa.

Figure 1; Source: dLocal 2021 second-quarter earnings presentation

Figure 2; Source: dLocal 2021 second-quarter earnings presentation

In the first half of 2021, dLocal had 340 enterprises as customers, including companies such as Didi, Microsoft, Mailchimp, Wix, Wikimedia, and Kuaishou. During the period, dLocal’s platform was used in an average of 7 countries and 65 payment methods for each customer with at least US$6 million in annual payment volume on the platform. dLocal’s customers come from many different verticals, but the company’s key verticals include retail, streaming, ride-hailing, financial institutions, advertising, SaaS (software-as-a-service), travel, e-learning, and gaming. The following are examples of the use-cases of dLocal’s payments platform:

- “One of the largest video streaming companies in the world” uses dLocal to accept local payment methods in Peru

- Didi uses dLocal in Argentina for a pay-out solution that enables bank transfers, split payments, and tax withholding functionalities for drivers to collect fares

- A “leading global internet search engine” uses dLocal in Brazil for dynamic transaction routing – traffic is automatically directed to payments providers with the highest probability of success

dLocal charges fees for each approved transaction on either a fixed fee per transaction basis, or a fixed percentage per transaction. These fees depend on a number of factors, including the solution used, the applicable geographical markets, the overall volume processed, and the functionalities required.

Based on the region where payments from/to dLocal’s customers are processed, the company currently has a heavy reliance on Latin America for revenue. In 2020, the region accounted for 89.4% of dLocal’s total revenue of US$104.1 million with the remaining 10.6% coming from what the company collectively terms “other emerging markets.” For the first half of 2021, when dLocal’s revenue was US$99.2 million, the self-same percentages are 90.3% and 9.7%, respectively. For a more granular view of dLocal’s geographical exposure, the company counts Brazil, Mexico, Argentina, Chile, Colombia, and India as its key markets.

Investment thesis

We have laid out our investment framework in Compounder Fund’s website. We will use the framework to describe our investment thesis for dLocal.

1. Revenues that are small in relation to a large and/or growing market, or revenues that are large in a fast-growing market

There’s a vast payments opportunity for dLocal to capture. According to Americas Market Intelligence (AMI), total e-commerce pay-in and pay-out volume in the countries that dLocal currently operates in, excluding China, was US$1.2 trillion in 2020. Pay-in volume was US$428 billion and is expected to grow by 27% annually to reach US$1.1 trillion by 2024. AMI also expects the pay-out volume to exhibit similarly strong growth “on the back of strong tailwinds associated with an expected recovery in the next 24 months from the COVID 19 pandemic, which fueled a rise in remote work and initially dampened travel, ride hailing and remittances, but which are expected to recover following the pandemic.” For context, dLocal processed total payment volume (TPV) of merely US$3.71 billion in the 12 months ended 30 June 2021, leading to revenue of US$164.7 million.

We think dLocal has a good chance of capturing significantly more share of the payments opportunity in emerging markets. In the “Company description” section of this article, we already gave an idea of how handling online payments in these countries can be a knotty affair. Here’re more statistics from AMI, based on 2020 numbers, that flesh out the complexity involved:

- Local payment methods represented 83% of total e-commerce spending in the 14 core emerging markets that were studied.

- Internationally-enabled credit cards accounted for only 10% of total e-commerce payment volume in Brazil, compared to 55%, 14%, and 12% for domestic-only credit cards, cash-based methods, and alternative payment methods, respectively.

- In India, just 30% of total e-commerce payment volume came from internationally-enabled credit cards while debit cards made up 19% and volume from bank transfers was 14%.

- In Nigeria, internationally-enabled credit cards only had a 13% share of the country’s total e-commerce payment volume, lower than the 28% and 27% shares that debit cards and bank transfers held, respectively.

The aforementioned prevalence of local payment methods in emerging markets creates a fragmented payment system that requires global enterprises to rely on numerous legacy payment providers. In contrast, the One dLocal model – with one API, one contract, and one platform – provides a superior experience, as it can act as a single point of interaction for these enterprises’ payment-related needs.

2. A strong balance sheet with minimal or a reasonable amount of debt

As of 30 June 2021, dLocal has US$266.0 million in cash on its balance sheet while having zero debt. This is a robust balance sheet, in our view. For the sake of conservatism, we do note that dLocal has total lease liabilities of US$4.1 million, but this is still dwarfed by the amount of cash that the company has.

It also helps that dLocal has already been generating free cash flow for at least two years. This is something we’ll cover in the “A proven ability to grow” sub-section of this article.

3. A management team with integrity, capability, and an innovative mindset

dLocal was founded in 2016 as a division of AstroPay, which is a global payment solutions provider with operations in emerging markets. dLocal’s founding management team includes Sebastián Kanovich and Jacobo Singer, the company’s current CEO and president, respectively. Kanovich, who’s 31, has been in the CEO role since dLocal’s formation while Singer, who’s even younger at 30, was previously the company’s chief technology officer and chief operating officer before he assumed his current role in March this year. We appreciate the fact that even though Kanovich and Singer are both young, they each have a few years under their belt in important leadership roles at the company.

On integrity

dLocal has not revealed much details about the compensation structure for its management team. But what we do know is that in 2019, 2020, and the first half of 2021, the total compensation of dLocal’s management team (this includes Kanovich, Singer, and the company’s chief operating officer, chief financial officer, and chief technology officer) were US$2.8 million, US$8.1 million, and US$3.2 million respectively. Table 1 below shows the compensation of the management team and dLocal’s financial results for these time periods. There are two good signs from the table on the integrity of the management team:

- Compared to the scope of dLocal’s business, the compensation of the management team is not egregious.

- There was a decline in the compensation in the first half of 2021 despite significant growth in the business.

Table 1; Source: dLocal IPO and secondary offering prospectuses

Another positive point on the integrity of dLocal’s management team is the skin in the game that Kanovich and Singer have. As of 25 October 2021, Kanovich owns 12.629 million dLocal shares. These shares have a collective value of more than US$617 million based on the company’s share price of US$49 on the same date. Meanwhile, Singer’s stake of 6.167 million dLocal shares (also as of 25 October 2021) have a total monetary value of US$301 million.

We do have some question marks over the integrity of dLocal’s leadership team, but we don’t see them as a dealbreaker. The integrity issues are related to the links between dLocal and AstroPay. Here are the important points:

- Earlier in this sub-section of this article, we mentioned that dLocal was founded as a division of AstroPay in 2016. In our view, AstroPay is a somewhat questionable company. It operates mostly in Brazil, India, and Latin America and processes payments mainly for merchants that are involved with online gambling, forex trading, binary options trading, and adult entertainment. These activities are legally grey (and in our view, morally grey too) and may even be considered to be illegal in some jurisdictions. Prior to 1 January 2016, Kanovich was the CEO of AstroPay while Singer held leadership roles there. The good things are that (1) dLocal and AstroPay separated on 1 August 2018, (2) dLocal has large global enterprises with legitimate businesses as customers and these enterprises often subject dLocal to stringent vetting processes, and (3) Kanovich and Singer no longer have links with AstroPay – save for a 1% equity interest held by Kanovich – as far as we know.

- dLocal has two share classes: Class B, which are not traded and hold 5 voting rights per share; and Class A, which are publicly traded and hold just 1 vote per share. Kanovich and Singer’s shares are all of the Class B variety. And even though dLocal’s CEO and president have what we think are significant monetary stakes in the company, they collectively controlled just 11.3% of its voting power as of 25 October 2021. There are at least two directors of dLocal – Andres Bzurovski Bay and Sergio Enrique Fogel Kaplan – who are major shareholders of AstroPay. And they also held a total of 58.6% of dLocal’s voting power as of 25 October 2021 as a result of owning 97.437 million dLocal Class B shares. The presence of Bay and Fogel Kaplan as major holders of dLocal’s shares and voting power did raise our eyebrows. But the saving grace here is that Bay and Fogel Kaplan’s dLocal shares are worth US$4.76 billion based on the company’s 25 October 2021 share price – this is a substantial stake which is likely to put them in the same boat as dLocal’s other shareholders.

On capability and innovation

We think Kanovich and his team shines on this front and there are a few things we want to discuss.

First, there’s dLocal’s strong history of innovation and geographical expansion. dLocal started life with only a single product to support pay-in cross-border payments in Brazil. But the company rapidly expanded its geographical coverage and has added new countries over the years since as shown in Figure 3 below. As we mentioned in the “Company description” section of this article, dLocal is currently in 30 countries. Here are two important examples of dLocal’s successful product innovation:

- dLocal developed a pay-out solution at the request of one customer during the 2016 Olympic Games in Rio Janeiro, Brazil, and was soon able to release the solution to all its customers.

- We briefly shared dLocal’s latest product, Direct Issuing, in the “Company description” section of this article. Through Direct Issuing, global enterprises are able to issue their own branded prepaid cards to end users for online and in-store shopping in local currencies. But there’s more. Direct Issuing can also be used by global enterprises for pay-outs. For example, global enterprises that run marketplace services (such as connecting drivers with passengers, or homeowners with short-term renters, or gig-economy suppliers with people looking for services) can issue revenue-share payments in the form of prepaid cards. Recipients of the prepaid cards can then use the funds within for groceries, petrol, ATM withdrawals, utility bills, and more, without the need for a bank account.

Figure 3; Source: dLocal 2021 second-quarter earnings presentation

Second, dLocal has found great success in growing its customers’ usage of its products over time. In one example, illustrated in Table 2, the average number of countries and payment methods that dLocal’s platform is used in per customer has increased materially over the past few years. In another instance, Table 3 shows that dLocal’s recent net retention rates (NRRs) have been very impressive. The NRR measures the change in revenue from all of dLocal’s customers from a year ago compared to today; it includes positive effects from upsells and cross-sells as well as negative effects from customers who leave or downgrade. The NRR of 171% achieved in 2020 means that all of dLocal’s customers in 2019 had collectively spent 71% more with the company in 2020. A third example is found in Table 4, which shows the impressive growth in the total payment volume (TPV) processed by dLocal since 2016.

Table 2; Source: dLocal IPO prospectus and quarterly earnings update

Table 3; Source: dLocal IPO prospectus and quarterly earnings update

Table 4; Source: dLocal IPO prospectus and quarterly earnings update

The third thing we want to discuss about dLocal’s management team is that the company appears to have an interesting culture and has also been run in an impressive boot-strapped manner since its inception. Kanovich explained these in a July 2020 episode of the Wharton Finance podcast:

“Miguel, it’s a great question. The first thing I need to say is that I’m super proud of the culture we have. I think the fact that we took a slightly different path from the average VC-backed, probably US company. So we are bootstrapped 100%. Only last December we brought our first institutional investor. And so we always knew that we would build our company with our own tools and listening very closely to our customers and with our feet on the ground. We were always making sure that we were profitable. We always cared about being profitable. We always cared about having people who were looking for a challenge and who really cared about what we were doing. We were always very pro-giving opportunities to people that otherwise probably wouldn’t have had them, either because they were born in Uruguay or Nigeria, or because they were younger because they have some sort of weird studies or no studies. And so, we came to this culture more by trying, by doing multiple mistakes and seeing what we liked and we didn’t like. The fact that both me and the management team were very young meant that we did a lot of mistakes. But I think today we are very comfortable in our own skin. We know who we are as a company, we know who we are not as a company. And I think that’s something when you walk into any of our offices, you can feel very fast.”

Somewhat backing up our positive view on dLocal’s culture is the company’s Glassdoor score. Glassdoor is a website that allows a company’s employees to rate it anonymously. dLocal currently has a 4.2-star rating out of 5 at Glassdoor, and 84% of dLocal-raters would recommend a friend to work at the company. But we do note that the usefulness of the Glassdoor ratings is limited in dLocal’s case, since there are only 33 reviews on the company at the moment.

And lastly, we think Kanovich and his team deserves credit for building a payments platform for its customers that removes nearly all of the complexities involved with handling online payments in emerging markets. This is not an easy task as it requires deep local knowledge and ties.

4. Revenue streams that are recurring in nature, either through contracts or customer-behaviour

We see dLocal’s revenue as highly-recurring in nature. Its revenue, as we have discussed in the “Company description” section of this article, comes from fees that it charges global enterprises for processing transactions (of both the pay-in and pay-out variety) that flow through its platform. These transactions are likely to be repeated often, which then creates a stream of recurring revenue for dLocal. Lending further weight to our view that dLocal has a high level of recurring revenue is something we have discussed earlier in this article: The company’s excellent NRRs in recent times.

But some of dLocal’s key verticals (such as retail, ride-hailing, advertising, travel, and gaming) are likely to be sensitive to economic conditions since they depend heavily on consumer spending. So dLocal’s transaction volume could still decline temporarily when economic conditions turn rough, thus hurting the company’s revenue. This said, our eyes are fixed on the long-term opportunity with dLocal and we think the company does have strong recurring revenue over the long run.

5. A proven ability to grow

dLocal has a short history as a public-listed company (its IPO was only in June this year) so we don’t have much financial data to study. But we like what we see. Table 5 below shows the key annual financial figures for dLocal that we can obtain:

Table 5; Source: dLocal IPO prospectus

A few key things to highlight from dLocal’s historical financials:

- Revenue grew by an impressive 88.6% in 2020.

- We appreciate the fact that dLocal was profitable for the time period under study and that its net income margin was strong in both years (28.2% in 2019 and 27.1% in 2020).

- The company also produced positive operating cash flow and free cash flow in both years, with very strong margins in the two years for both numbers. dLocal’s operating cash flow margin (operating cash flow as a percentage of revenue) climbed from 55.6% in 2019 to 85.0% in 2020. The company’s free cash flow margins (free cash flow as a percentage of revenue) for the same years were 52.5% and 81.2%, respectively.

- dLocal maintained a robust balance sheet in both 2019 and 2020 as it had zero debt in both years while holding a healthy amount of cash.

- We usually look at changes in a company’s share count over time to determine if there has been egregious shareholder dilution in the past. In the case of dLocal, we did not look at its share count since the company was listed only in June 2021. We do note that dLocal had a share count of 292.9 million right after its listing and we will be comparing dLocal’s future share counts with this number. Ultimately, what we want is to see dLocal produce business growth that significantly outweighs increases in its share count, if any.

dLocal has managed to continue producing strong results in 2021 thus far. Table 6 shows the impressive growth in dLocal’s revenue, net income, and operating cash flow in the first half of 2021.

Table 6; Source: dLocal IPO prospectus and quarterly earnings update

6. A high likelihood of generating a strong and growing stream of free cash flow in the future

We think dLocal aces this criterion for a few reasons:

- First, there is a high likelihood, in our view, that dLocal’s revenue can continue to grow at a high double-digit rate in the years ahead. The company’s One dLocal model is an attractive proposition for global enterprises that are looking for a good solution for handling online payments in emerging markets. Moreover, dLocal has done an excellent job over the years in product development and expanding into new geographies. If the company keeps up with this, its payments platform is likely to become increasingly attractive to global enterprises over time.

- Second, dLocal has already been generating free cash flow since at least 2019. Moreover, the company’s free cash flow margins in 2019 and 2020 were both impressive at 52.5% and 81.2%. We don’t think a free cash flow margin of 81.2% is anywhere near a sustainable level. But there’s also no reason for us to believe that dLocal cannot maintain its free cash flow margin at a robust double-digit percentage range in the future.

Valuation

Our initial purchases of dLocal shares were completed in early-October 2021. Our average purchase price was US$52 per share. At our average price and on the day we completed our purchases, dLocal’s shares had a trailing price-to-free cash flow (P/FCF) ratio and trailing price-to-sales (P/S) ratio of around 241 and 147, respectively.

We like to keep things simple in the valuation process. In dLocal’s case, we think the P/FCF and P/S ratios are appropriate metrics to gauge the value of the company. For the P/FCF ratio, it is because dLocal has been producing free cash flow for a number of years, and its free cash flow margin has been really high in recent times. For the P/S ratio, it’s useful when dLocal’s free cash flow becomes light in the future because it is reinvesting into its business for future growth.

The P/FCF and P/S ratios of 241 and 147 are really high and that’s a risk. But we’re willing to pay a premium for a few reasons. First, despite dLocal’s rapid revenue growth in 2020 and the first half of 2021, its share of the total e-commerce pay-in and pay-out volume in most of the countries that it’s operating in is still tiny. Second, because dLocal’s One dLocal model is attractive for global enterprises that are looking for solutions to handle online payments in emerging markets, we believe the company has a high chance of being able to increase its market share significantly over time. Third, we think that dLocal can maintain strong free cash flow margins as its business grows.

For perspective, dLocal carried P/FCF and P/S ratios of around 225 and 137 at its 25 October 2021 share price of US$49.

The risks involved

We see a few key risks that could make our investment in dLocal become a debacle:

- One that we mentioned earlier in the “Revenue streams that are recurring in nature, either through contracts or customer-behaviour” sub-section of this article is the high likelihood of some of dLocal’s key verticals being sensitive to economic conditions.

- There’s also customer-concentration risk. In 2019, 2020, and the first half of 2021, dLocal’s top 10 customers accounted for 70%, 64% and 62% of its total revenue, respectively. The good thing is that the level of customer concentration has been declining.

- dLocal’s heavy exposure to emerging markets brings currency and political risk. The company reports its financials in the US dollar, but it conducts business mostly in the prevailing currencies of the emerging markets it’s in. Unfortunately, these currencies have historically been weak. Moreover, the Latin American region has been no stranger to political instability in the past. There’s a chance that massive political upheavals in the region could occur in the future and hurt dLocal’s business.

- The connections, both past and present, that dLocal has with AstroPay brings reputational risk into the picture. As we explained in the “A management team with integrity, capability, and an innovative mindset” sub-section of this article, AstroPay processes payments mainly for merchants that are involved with legally and morally questionable activities such as online gambling, forex trading, binary options trading, and adult entertainment. dLocal’s future growth could be stunted if there’s a widespread view that the two companies are still heavily linked.

- The last important risk we’re keeping our eyes on is valuation risk. We think dLocal’s business is likely to grow at a rapid clip for many years. But it has a really high valuation. So if there are any hiccups in dLocal’s business – even if they are temporary – there could be a painful fall in the share price. This is a risk we’re comfortable taking as long-term investors.

Summary and allocation commentary

To summarise dLocal, it has:

- Huge global e-commerce pay-in and pay-out transaction volumes to capture.

- A robust balance sheet with healthy cash levels and zero debt.

- A management team that has an excellent multi-year track record with execution and innovation.

- High levels of recurring revenues through (1) taking a small cut of transactions that are likely to be repeated often, and (2) high customer-retention.

- A track record, albeit a short one, of impressive growth in revenue, net income, and free cash flow.

- A good chance of being able to produce strong free cash flow in the future.

As it is with every company, there are risks to note for dLocal. The main ones we’re watching include: The sensitivity of dLocal’s key verticals to economic conditions; customer-concentration risk; exposure to emerging markets that have experienced significant currency devaluations and political volatility; reputational risk that is related to dLocal’s ties with AstroPay; and the company’s high valuation.

After weighing the pros and cons, we decided to initiate a position of around 0.5% in dLocal in early-October 2021. Our initial position in dLocal can be considered to be a small-sized allocation. We appreciate all the strengths we see in dLocal’s business, but our enthusiasm is currently tempered by the company’s sky-high valuation and the associations that dLocal has with AstroPay.

And here’s an important disclaimer: None of the information or analysis presented is intended to form the basis for any offer or recommendation; they are merely our thoughts that we want to share. Compounder Fund does not own shares in any other companies mentioned in this article. Holdings are subject to change at any time.