Compounder Fund: PayPal Sell Thesis - 13 Apr 2026

Data as of 12 April 2026

We first invested in PayPal (NASDAQ: PYPL) for Compounder Fund’s portfolio in July 2020. Our investment thesis for the company can be found here. In early-February 2026, we completely exited PayPal. This article describes our Sell thesis for the company.

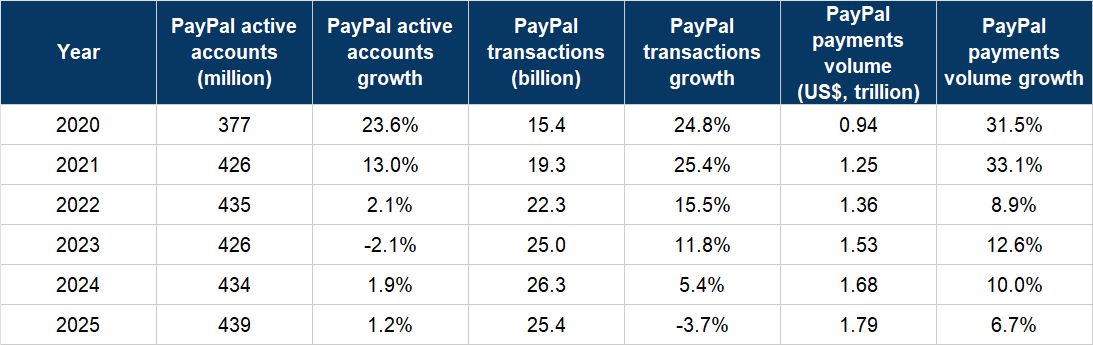

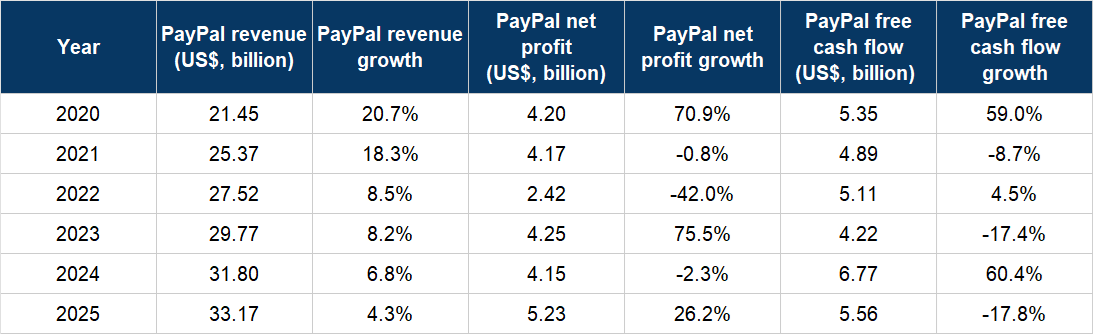

When we invested in PayPal, the digital and mobile payments company had grown its transactions and payments volume at 20% or more each year for multiple years. Meanwhile, its number of active accounts had increased by a low- to high-teens range, also in each year. The company translated these into respectable financial results. From 2012 to 2019, PayPal’s revenue, net profit, and free cash flow compounded at 17.8%, 17.9%, and 20.4% annually. With a payments opportunity pegged at US$110 trillion as of 2018 and payments volume of ‘only’ US$712 billion in 2019, we thought PayPal would be capable of producing strong double-digit growth in revenue, net profit, and free cash flow for many years into the future, driven by commensurate growth in active accounts, transactions, and payments volume.

In the first two years after our investment (2020 and 2021), PayPal produced pleasing growth in most of the important metrics mentioned in the paragraph above, as shown in Tables 1 and 2 below. But as the tables also illustrated, PayPal’s growth rates started faltering in 2022 onwards. Part of the slowdown in PayPal’s growth was weakness in the e-commerce market in 2022. Part of it was the result of Alex Chriss’s deliberate move to pull the brakes on volume-growth in the lower-margin PSP (Payment Service Provider) segment and focus on profitability instead. Chriss became CEO of PayPal in September 2023 and made the PSP-decision a few months after taking the helm. At the time, we thought it was the right call to make.

Table 1; Source: PayPal quarterly earnings updates and annual reports

Table 2; Source: PayPal quarterly earnings updates and annual reports

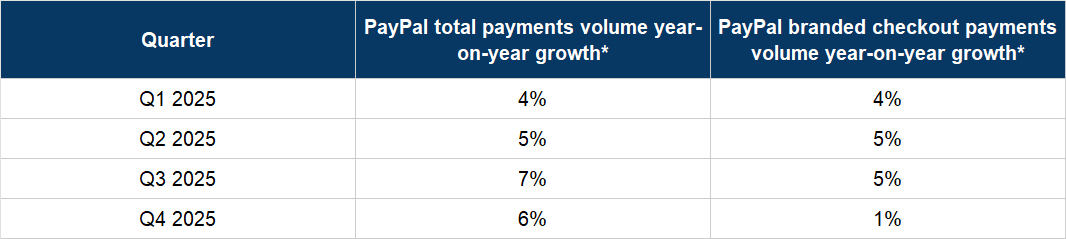

But as PayPal’s results for 2025 came in, we became increasingly concerned and concluded that (1) the company’s competitive position in the digital payments market had weakened, and (2) management was either ignorant of the actual problem or turning a blind eye, neither of which are positive scenarios. There are two reasons for our stance.

Firstly, there was the lacklustre growth in PayPal’s branded checkout volumes throughout 2025 shown in Table 3 below. Branded checkout refers to the PayPal payments button seen on e-commerce websites and which carries higher margins for the company. It also accounts for a material portion (30% in 2025) of PayPal’s overall payments volume.

Table 3; Source: PayPal quarterly earnings updates;

*Growth rates are calculated on a currency-neutral basis

Secondly, PayPal’s management repeatedly blamed macro-economic issues for branded checkout’s humdrum and deteriorating numbers… :

[From PayPal’s 2025 second-quarter earnings presentation]

“Branded checkout TPV up mid-single-digits despite some tariff headwinds on retail spending”

[From PayPal’s 2025 third-quarter earnings presentation]

“Branded checkout up mid-single digits despite mixed global macro trends”

[From PayPal’s 2025 fourth-quarter earnings presentation]

“Branded checkout deceleration driven by weakness in US retail, international headwinds and tough compares in high-growth verticals”

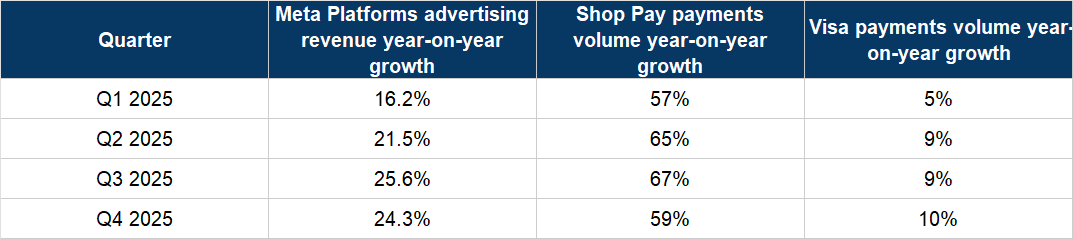

… when other important entities in the e-commerce and digital payments ecosystem were posting healthy growth throughout 2025. For example:

- Meta Platforms’ digital advertising revenue posted year-on-year growth rates of between 16.2% and 25.6% in each quarter of 2025, with the online commerce vertical being the largest growth-contributor.

- Shopify saw outstanding growth in payments volume for its Shop Pay button of 57%-67% in each quarter of 2025; the Shop Pay button is a direct competitor of the PayPal branded checkout button and it’s worth noting that the former handled US$121 billion in payments volume in 2025, which is at the same order of magnitude as the latter’s US$537 billion in the same year

- Visa saw accelerating payment volume growth through 2025 and management cited e-commerce as being one of the important pillars of its volume-growth.

Table 4 below shows the growth rates in each quarter of 2025 for Meta Platforms’ advertising revenue, and Shop Pay’s and Visa’s payments volumes.

Table 4; Source: Meta Platforms, Shopify, Mastercard, and Visa’s quarterly earnings updates

There was also a leadership change at PayPal that we saw as a negative development. On 3 February 2026 (the same day PayPal released its 2025 fourth-quarter results) the company announced that Enrique Lores would replace Chriss as CEO. We see two major problems with Lores’ appointment:

- Although he has been on PayPal’s board of directors since June 2021, he has no prior executive experience in the digital payments industry, having spent his entire career at HP.

- He was CEO of HP from November 2019 to February 2026 and the company’s business results during his tenure do not inspire confidence. From HP’s financial year ended 31 October 2020 (FY2020) to FY2025, revenue declined from US$56.6 billion to US$55.3 billion. Meanwhile, HP’s operating and free cash flow margins both fell, from 7.3% to 6.6%, and from 6.6% to 5.1%, respectively.

It did not help Lores’ case that PayPal’s 2027 targets – given just a year ago in the February 2025 Investor Day event – have been withdrawn. PayPal’s then-interim CEO and current CFO and COO, Jamie Miller, said during the 2025 fourth-quarter earnings conference call:

“We are no longer committing to the specific outlook for 2027 we laid out at Investor Day last year…

…We think it’s prudent for now to provide financial guidance one year at a time.”

The withdrawn targets included 8%-10% annual branded checkout volume growth by 2027, and low-teens growth in non-GAAP (generally accepted accounting principles) earnings per share growth by the same year, followed by 20%-plus growth over the longer-term. We were happy to stay invested if we had confidence in PayPal meeting or exceeding these targets. But in the withdrawn-targets’ place was tepid guidance for 2026, which included a low-single digit percentage decline to slight growth in non-GAAP EPS. Miller shared in the 2025 fourth-quarter earnings conference call that Lores had substantial input towards PayPal’s latest guidance:

“With respect to Enrique’s involvement from a strategy perspective, look, he’s deeply involved in it. He has helped shape and reviewed not only the capital allocation strategy, the investment priorities that support them, but also the 2026 guidance.”

We decided to sell Compounder Fund’s PayPal shares because of (1) the deterioration in the company’s business results starting in 2022, (2) our view that management is either unable or unwilling to diagnose the problems accurately, and (3) a new CEO that we don’t think is the right candidate to lead the company forward.

We made our initial investment in PayPal at an average price of US$184 per share and sold at an average price of US$41. The capital from the sale of Compounder Fund’s PayPal shares was redeployed to some existing companies in the portfolio (in this case, the companies were Meta Platforms, MercadoLibre, and TSMC).

And here’s an important disclaimer: None of the information or analysis presented is intended to form the basis for any offer or recommendation; they are merely our thoughts that we want to share. Of all other companies mentioned in this article, Compounder Fund owns shares in Meta Platforms, MercadoLibre, and TSMC. Holdings are subject to change at any time.