Compounder Fund: The Trade Desk Sell Thesis - 13 Apr 2026

Data as of 12 April 2026

We first invested in The Trade Desk (NASDAQ: TTD) for Compounder Fund’s portfolio in July 2020. Our investment thesis for the company can be found here. In early-March 2026, we completely exited Trade Desk. This article describes our Sell thesis for the company.

When we invested in Trade Desk, the programmatic advertising platform provider had a multi-year history of impressive growth in the advertising spend flowing through its platform. The company’s platform provided better targeting, more efficient spending, and improved campaign results for advertisement buyers. This led to consistently excellent client retention rates of more than 95%, and advertising spend increasing by more than 70% annually from 2014 to 2019. Through a stable take-rate of around 20%, Trade Desk translated the growing-spend into equally-rapid revenue growth of 71.5% per year over the same period. The company’s profitability also improved materially, and it ended 2019 with a respectable net profit margin of 16%. We credited Trade Desk’s co-founder and CEO Jeff Green – who is still leading the company today – for the company’s results. We thought Trade Desk would continue to compound its revenue at a strong clip for years into the future, and produce high net profit and free cash flow margins. The programmatic advertising market looked poised for long-term growth, and Trade Desk had only captured a fraction of the opportunity.

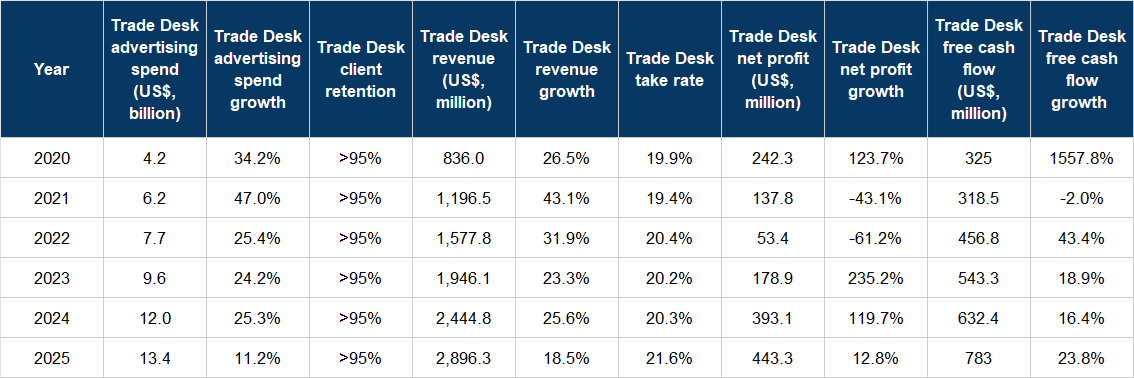

For the most part after our investment, Trade Desk continued to deliver high client retention, strong growth in advertising spend, and commensurate growth in revenue, net profit, and free cash flow, driven by a stable take rate. These are shown in Table 1 below. But Table 1 also showed that the growth rates in Trade Desk’s advertising spend and revenue slowed materially in 2025 to just 11.2% and 18.5%, respectively. This is the cause of our concern.

Table 1; Source: Trade Desk quarterly earnings updates and annual reports

During Trade Desk’s earnings conference calls for 2025, Green and other members of the management team repeatedly cited non-Trade-Desk-specific issues for a slow down in the growth rate of its advertising spend, such as macro-driven weakness in advertising by CPG (consumer packaged goods) companies, which is one of the company’s key verticals:

[From Trade Desk’s 2025 first-quarter earnings conference call]

“Q4 was relatively stable, though signs of volatility we’re building beneath the surface have made a contentious election cycle. That pressure intensified in Q1 with growing concern among clients. As you know, our primary clients are the largest brands in the world and the agencies that serve them. All of whom are navigating increasing volatility so far in 2025…

…As we turn to our second quarter outlook, we want to acknowledge the volatile macro backdrop, particularly its impact on large global brands.”

[From Trade Desk’s 2025 third-quarter earnings conference call]

“At a macro level, I describe the environment as a tale of 2 cities. On one hand, some large brands, particularly in categories like consumer products or CPG and then parts of retail are still feeling pressure from factors like tariffs and inflation.”

[From Trade Desk’s 2025 fourth-quarter earnings conference call]

“2025 was fantastic for tech spend, for travel spend, for pharma spend and for communication spend. Actually, despite a greater degree of macro uncertainty and most S&P 500 companies trying to determine what changes the evolving AI-fueled world and the geopolitical issues mean for them, most categories had a very good year. One of the clearest themes in our data and from our conversations with clients was a sustained weakness among some large consumer packaged goods companies, CPGs as well as some global auto companies. Together, these verticals represent over 1/4 of our business. But in these 2 categories, all global companies have levels of uncertainty that we haven’t seen for most of the last 15 years…

…Beginning in Q2 2025, CPG and auto companies began navigating a mix of category headwinds such as tariff uncertainty and uneven volumes in addition to persistent inflationary pressures as more consumers deal with cost of living challenges. And those trends have continued into the beginning of this year. On their own earnings calls, several global brands have talked about pulling back on advertising budgets driven by the month-to-month volatility caused by these macro forces. In the CPG sector, just last week at CAGNY, many of the large global brands spoke about consumer pressure, slower volume recovery and ongoing input cost volatility, reinforcing what we are seeing in our data…

……If you look at the impact that these 2 categories have, we would have been at least 5% higher in growth rate if you don’t include those categories or they were at parity with everybody else.”

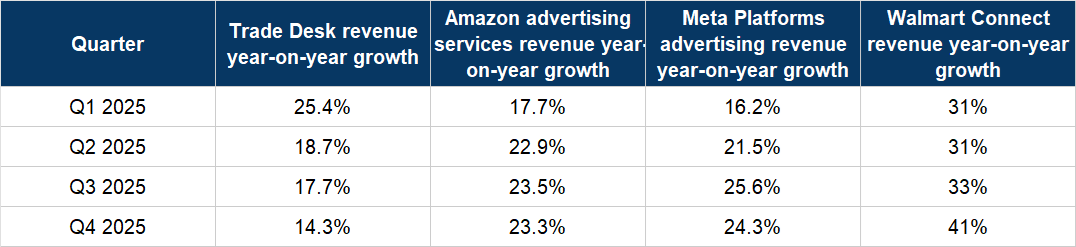

But when we looked at other major companies in the digital advertising eco-system, their experience was different to Trade Desk’s. Table 2 below shows the following for each quarter of 2025: Trade Desk’s revenue growth (there are no publicly-available quarterly advertising spend data); Amazon’s advertising revenue growth; Meta Platforms’ advertising revenue growth; and Walmart’s Walmart Connect revenue growth.

Table 2; Source: Trade Desk, Amazon, Meta Platforms, and Walmart quarterly earnings updates

Sponsored products advertising was a big driver of Amazon’s advertising revenue growth in 2025. For Meta Platforms’ advertising revenue, the online commerce vertical was the largest growth-contributor in each quarter. The Walmart Connect business is the retail media advertising division of Walmart that allows brands to engage with customers across the company’s online and physical stores. We think it’s reasonable to assume plenty of CPG-advertising content in all three cases. We mentioned earlier that Trade Desk’s management had blamed macro-driven weakness in advertising-spend by CPG companies for the company’s slowdown in growth in 2025. But as Table 2 highlighted, Amazon and Meta Platforms’ advertising revenues, and Walmart’s Walmart Connect revenue, all saw stable growth or acceleration throughout each quarter of 2025, despite our reasonable assumption that CPG-advertising spend is a major driver of these businesses. In contrast, Trade Desk’s revenue growth decelerated. Additionally, while Meta Platforms’ management is guiding for revenue growth of between 26% and 34% for the first quarter of 2026, Trade Desk’s guidance calls for a revenue-growth-floor of just 10%. Green once again cited macro-uncertainty for the slow growth rate during the 2025 fourth-quarter earnings call:

“I’d highlight the differences in verticals to provide a clearer view of our long-term opportunity and not to misunderstand unique moments of macro headwinds with the long-term prospects of our business. Without that double-click, it’s harder to understand why I’m so confident in our long-term opportunity…

…Our Q1 guide reflects the prudence from both the auto and the CPG categories and the state of the state, if you will, and what they’re dealing with. And also, it does not reflect a diminished long-term opportunity for either The Trade Desk or these categories specifically. It is just something that’s happening at a macro level at this moment in time, and it is bigger than them and bigger than us.”

It’s worth noting that Walmart Connect launched its own DSP (demand-side platform) in August 2021 in partnership with Trade Desk. The partnership saw Walmart Connect’s DSP run on Trade Desk’s technology rails exclusively. But importantly, access to Walmart’s retail data – the valuable part of a DSP – was only in the hands of Walmart Connect’s DSP. In August 2025, Walmart appeared to have backed away from using Trade Desk’s technology exclusively, according to media reports. But Trade Desk announced around the same time that its partnership with Walmart was going “from strength to strength”. Regardless of the status of the partnership, it’s a fact that Walmart Connect saw acceleration in its revenue growth in the second half of 2025 – when we think the platform has substantial CPG-content in its advertising volume – while Trade Desk’s revenue growth decelerated. We see this as an example of CPG companies being inclined to spend heavily on advertising in 2025, just less so across Trade Desk’s broader surfaces.

We think Trade Desk’s management team, especially Green, is either ignorant of the actual problem or turning a blind eye, neither of which are positive scenarios. The real issue for Trade Desk, in our view, is its programmatic advertising platform is losing market share. But if management is unable to acknowledge this for whatever reason, the problem will continue to fester. This also brings us to a mistake we made in our initial assessment of Trade Desk: We thought the company’s programmatic advertising platform would continue to win market share for a long time because of the benefits it provides, but it appears so far that we’ve been mistaken.

(Adding to our conviction on Trade Desk’s platform losing market share are two pieces of news that surfaced in March after we had sold the company’s shares. The first, involving a major Trade Desk client, the advertising agency Publicis Groupe, happened in mid-March. Adweek reported that Publicis had advised its clients to avoid using Trade Desk’s programmatic advertising platform; Trade Desk had apparently failed a third-party audit regarding its fees. Trade Desk last disclosed that at least 10% of the annual advertising spend on its platform in 2023 came from Publicis. Then in late-March, Mediapost wrote that “Omnicom is the latest holding company to launch an audit of demand-side programmatic ad platform The Trade Desk.” Omnicom, similar to Publics, is an advertising agency that funnels advertising dollars through Trade Desk’s platform.)

We were also unsettled by a recent leadership-change. Trade Desk hired Alex Kayyal as CFO in August 2025 to replace Laura Scheinken, who had been with the company for almost 12 years and became CFO only in June 2023. But Kayyal lasted just five months when Tahnil Davis was appointed as CFO in January this year. Given the importance of a CFO to most companies, we expected Green to explain Kayyal’s abrupt departure, especially when his predecessor was in the hot-seat for a relatively short span of just two-plus-years. But Green failed to discuss the CFO-change during Trade Desk’s 2025 fourth-quarter earnings conference call that took place in late-February.

Compounder Fund’s investment in Trade Desk has been especially frustrating for us. We came into the investment with a wonderful opinion of Green, but left with somewhat of a bitter taste. We made our initial investment in Trade Desk at a split-adjusted average price of US$44 per share and sold at an average price of US$24. The capital from the sale of Compounder Fund’s Trade Desk shares was redeployed to some existing companies in the portfolio (in this case, the companies were Meta Platforms, MercadoLibre, and TSMC).

And here’s an important disclaimer: None of the information or analysis presented is intended to form the basis for any offer or recommendation; they are merely our thoughts that we want to share. Of all other companies mentioned in this article, Compounder Fund owns shares in Meta Platforms, MercadoLibre, and TSMC. Holdings are subject to change at any time.