Compounder Fund: dLocal Sell Thesis - 11 Jul 2025

Data as of 10 July 2025

We first invested in dLocal (NASDAQ: DLO) for Compounder Fund’s portfolio in Ocrtober 2021. Our investment thesis for the company can be found here. In late-March this year, we completely exited dLocal. This article describes our Sell thesis for the company.

dLocal was a company specialising in payments services in emerging economies in Latin America, Asia, and Africa, when we first invested. Handling payments in emerging economies appeared to be a complicated affair as merchants needed to navigate low banking-penetration rates in the resident populations and a myriad of local payment methods. dLocal aimed to reduce the complexity through its One dLocal model – which featured one direct API (application programming interface), one technology platform, and one contract – to help merchants get paid and make payments in emerging economies. The value proposition of dLocal’s solution seemed to be well-received by merchants, as the total payment volume (TPV) processed by the company surged from US$136 million in 2016 to US$2.07 billion in 2020. dLocal had become a public-listed company for only four months when we invested in it, so we did not have a long financial history to study. But what we could find showed that TPV growth of 60.3% in 2020 had translated into even better gross profit growth of 67.5%. We also saw a vast payments opportunity for dLocal to capture, with around US$2 trillion in pay-in (where merchants get paid) and pay-out (where merchants make payments) volume in the countries the company was operating in back then.

The combination of all the factors in the paragraph above made us think dLocal could grow its gross profit substantially over a five to 10-year period. Implicit in this thought was the important assumption that dLocal’s net take rate – its gross profit as a percentage of TPV – can be maintained.

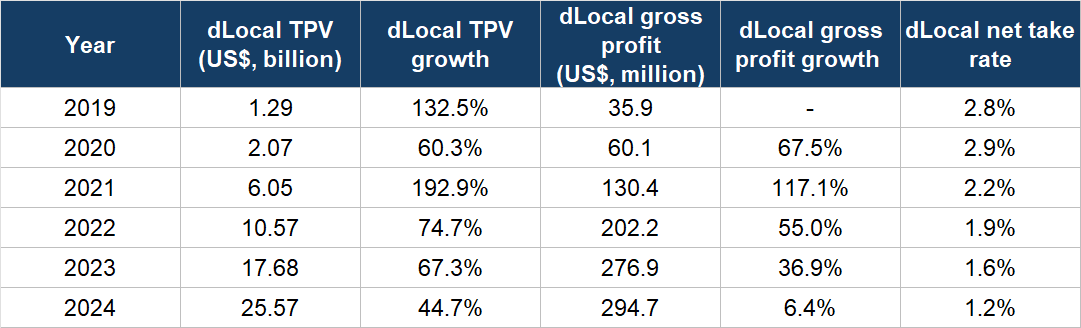

From the time we invested in dLocal till our sale, the company had continued to achieve good growth in TPV, as Table 1 below shows. But we got our net take rate assumption wrong. Table 1 also shows dLocal’s gross profit growth, and net take rate from 2019 to 2024. The company’s gross profit growth has suffered in more recent years as a result of the compression in its net take rate, which management had attributed largely to changes in the company’s business mix and large merchants increasing payment volumes which drive take rates lower. Unfortunately, in the most recent earnings conference call before our sale of Compounder Fund’s dLocal shares, management had guided for the net take rate to further narrow in 2025 and perhaps beyond:

“If you consider all those assumptions, we should expect a net take rate compression while delivering high TPV growth even at the scale we’ve already attained. Over the midterm, we will work diligently to maintain that strong TPV growth while recognizing that given the extremely strong levels of retention that we’re able to deliver, our larger merchants will continue to attain lower pricing tiers and contracts. We will focus on offsetting this take rate compression through growth in higher take rate new verticals that we’re pursuing, natural mix shift towards higher take rate frontier markets away from Brazil and Mexico despite still growing well in those large markets and new revenue streams through new product launches and constant innovation.”

Table 1; Source: dLocal annual reports

The negative impact of falling net take rates on gross profit growth can be mitigated by rapid increases in payment volume. But dLocal’s TPV growth, while good, has not been especially impressive. For perspective, Adyen’s TPV in 2024 was €1.4 trillion, and was up 33%, whereas dLocal’s TPV in the same year was an order of magnitude lower at US$26 billion while growth was ‘just’ 45%.

dLocal’s current chief executive officer, Pedro Arnt, has an excellent resume. Prior to joining dLocal in August 2023 as co-CEO (he became sole CEO in March 2024), he had been chief financial officer of Latin American e-commerce and digital financial services powerhouse MercadoLibre since June 2011 (MercadoLibre is one of Compounder Fund’s largest holdings). We thought Arnt’s presence would galvanise dLocal and accelerate its TPV growth and/or stabilise its net take rate. Unfortunately, as we showed earlier, these did not happen.

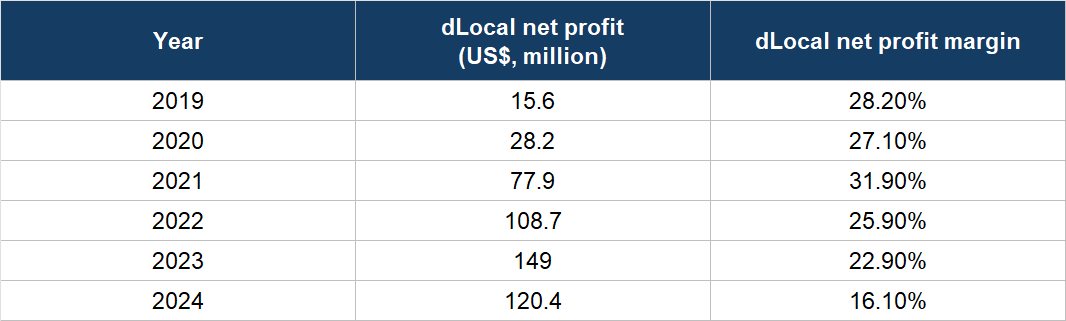

The headwind for dLocal’s gross profit growth, in the form of lower net take rates, has also resulted in severe compression in its net profit margin in recent years, as shown in Table 2 below:

Table 2; Source: dLocal annual reports

Since it looks like we have been badly mistaken with our important assumption that dLocal would be able to maintain its net take rate, we decided to part ways with the company. Even if dLocal can continue enjoying good double-digit growth in TPV, further compression in its net take rate would present a headwind to commensurate growth in gross profit and net profit.

We made our initial investment in dLocal at an average price of US$52 per share, but sold at a much lower average price of US$8. The big decline in dLocal’s stock price might lead someone reading this to ask: “Couldn’t you have sold dLocal earlier?” It’s a valid question. Our response will be something we shared in Compounder Fund’s Owner’s Manual:

“And on the topic of selling stocks, we will typically sell a stock in Compounder Fund’s portfolio if we find that the investment thesis is completely broken, or we have made a big mistake in our analysis. But we will be very slow to sell. The slowness is by design – it strengthens our discipline in holding onto the winners in Compounder Fund. Holding onto the winners will be a very important contributor to Compounder Fund’s long run performance.”

Part of the capital from the sale of Compounder Fund’s dLocal’s shares was redeployed to some existing companies in the portfolio (in this case, the companies were Alphabet, Amazon, and The Trade Desk).

And here’s an important disclaimer: None of the information or analysis presented is intended to form the basis for any offer or recommendation; they are merely our thoughts that we want to share. Of all other companies mentioned in this article, Compounder Fund owns shares in Adyen, Alphabet, Amazon, MercadoLibre, and The Trade Desk. Holdings are subject to change at any time