Compounder Fund: Wise Investment Thesis - 20 Oct 2021

Data as of 19 October 2021

Wise (LSE: WISE), which is based and listed in the UK, is a company in Compounder Fund’s portfolio that we invested in for the first time in October 2021. This article describes our investment thesis for the company.

Company description

Wise was founded in 2011 by two Estonian friends, Kristo Käärmann and Taavet Hinrikus, with an idea they developed to solve a problem they both faced. Some time prior to Wise’s founding, both Käärmann and Hinrikus were living in London. At that time, Hinrinkus was working for Skype’s Estonian office and was paid in Estonian kroons. But he needed British pounds, as he was living in London. Meanwhile, Käärmann was working at Deloitte’s UK office and was paid in pounds. But he had a mortgage in Estonia that needed to be serviced with kroons. For a while, the two friends used banks to handle their international money transfers. But the transfers were both expensive and slow. So the two friends came up with an elegantly ingenious solution.

At a particular day each month, they would check the day’s mid-market rate to find a fair exchange rate for kroons and pounds. Käärmann would then deposit pounds into Hinrinkus’s UK bank account while Hinrinkus would put kroons into Käärmann’s Estonian account. And voila – the two friends got the currencies they needed, while not paying a single cent in hidden bank charges! Today, Wise’s core international money transfer product – named Wise Transfer – still works on a very similar premise.

Wise Transfer is a way for users to send money to more than 80 countries, covering over 85% of the world’s bank accounts. It works in three simple steps:

- To send money, the sender – an individual or a business – sets up a payment order on Wise’s website or app and specifies the amount, the source, and the target currency. Wise will show the relevant fees upfront before the transfer is initiated. The sender then funds the transfer by putting money into a local bank account of Wise’s. Depending on the payment currency, the sender can pay with a variety of methods, such as bank transfers, payment cards, or through open banking.

- In the currency-conversion process, Wise carries out the necessary due diligence checks in areas such as identity verification, fraud, and money laundering. Once these checks are completed and payment is received from the sender, Wise converts the money that was paid in. On most transfers, Wise guarantees senders the mid-market rate – sourced from Refinitiv – for a limited period to allow senders to fund their transfers.

- After the currency conversion, Wise pays out from its local account to the recipient’s local account. Wise is able to pay out in a variety of ways, including bank transfers and paying-out to cards.

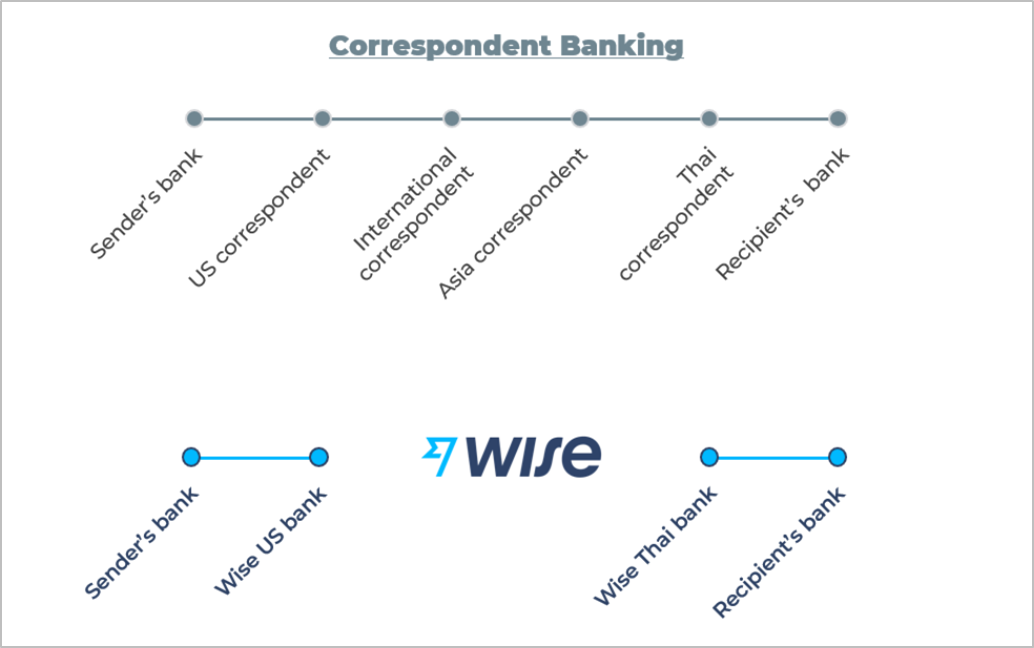

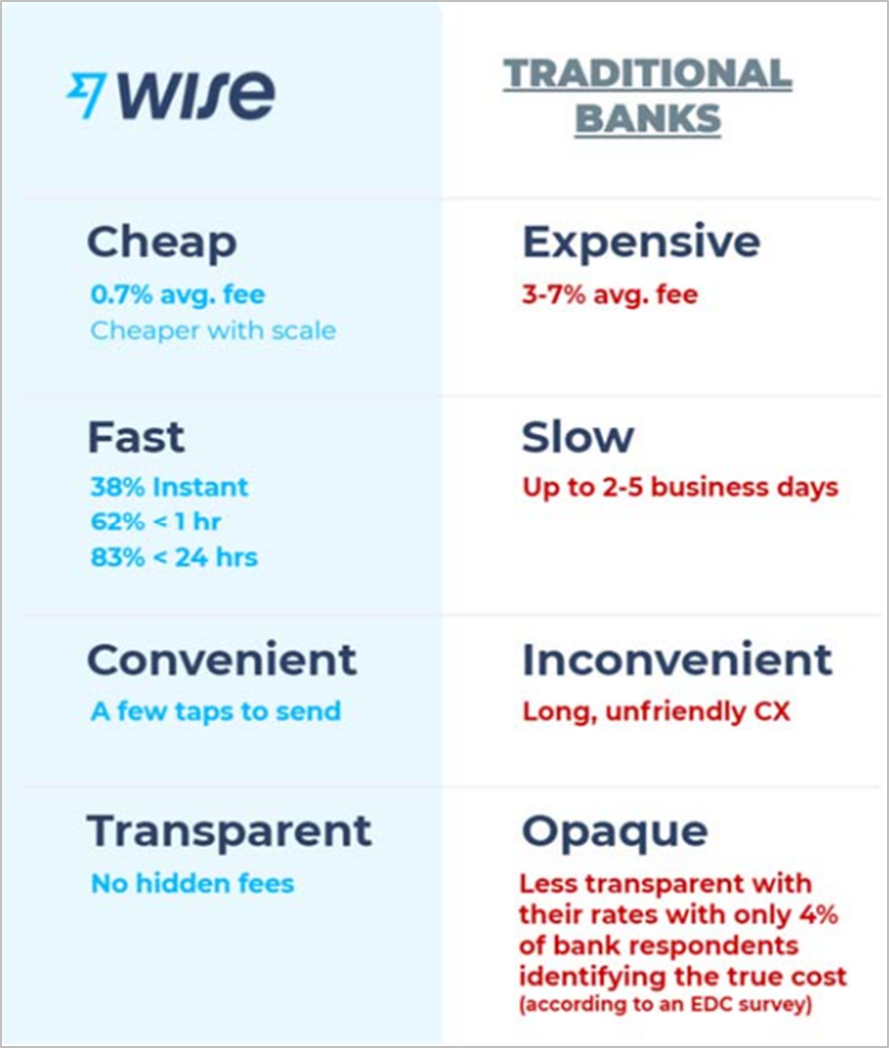

It’s important to note that in processing Wise Transfers, Wise ensures that money does not cross borders as much as possible. Wise’s money-transfer infrastructure stitches local payment systems together and eliminates intermediaries and manual processes (see Figure 1). This allows Wise to process money transfers by using its own local pools of money. Wise’s bank accounts hold currency from around the world from the local payments made by senders. When needed, Wise purchases currencies in the open market at very low costs. The company’s infrastructure makes Wise Transfers much faster and cheaper than traditional money transfers. Figure 2 shows a comparison of the current user-experience between a Wise Transfer and an international money transfer made with a traditional bank; note the superior cost, speed, convenience, and fee-transparency that Wise Transfer provides to users.

Figure 1; Source: Wise IPO prospectus

Figure 2; Source: Wise IPO prospectus

Wise has three more products:

- Wise Account is free to sign up for individuals, and has no subscription fee. It allows people to manage their money around the world as though they hold local bank accounts (with the traditional foreign transaction fees removed). Wise Account users are able to: Send money internationally with Wise Transfer; add money to their accounts in 19 currencies; receive money in 10 currencies; hold 56 currencies and convert money between any of these currencies at the mid-market rate; and spend their money with a Wise debit card that can be used in more than 176 countries.

- Wise Business carries all the features of Wise Account plus other features that are tailored to small and medium businesses. The additional features include invoicing, multi-user accounts, enhanced benefits when spending with the Wise Business debit card, scheduled recurring payments, API-based payment automation workflows, and more.

- With Wise Platform, financial institutions and other enterprises (such as core banking software and technology services providers) can integrate Wise’s payments network into their own services. The integrations are free for Wise Platform clients. At the end of FY2021 (fiscal year ended 31 March 2021), Wise has performed Wise Platform integrations with 14 banks (including neo banks and traditional banks) in 10 countries across four continents.

In FY2021, Wise earned revenue of £421.0 million while processing £54.4 billion in payment volume. No numbers are given as far as we know, but a “majority” of Wise’s revenue comes from the upfront fees Wise charges for international money transfers. Other revenue sources for Wise are fees from domestic same-currency transactions, interchange fees associated with the use of Wise debit cards, and other fees that are linked to Wise Account and Wise Business.

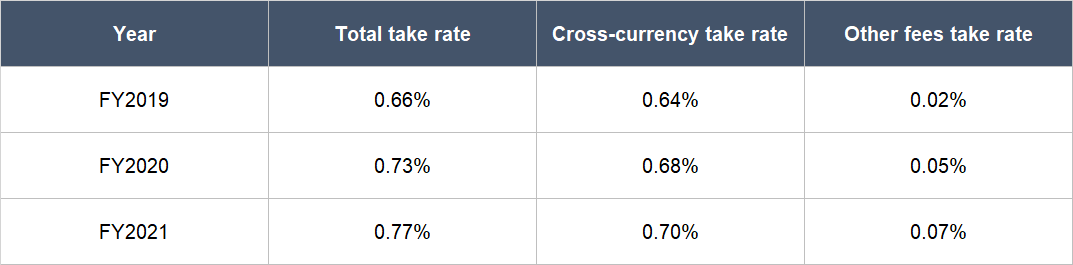

On most transactions with Wise Transfer, Wise’s core international money transfer product, the company charges a single low upfront fee that consists of a fixed fee and a variable fee. The amount for the fixed and variable fees depend on a number of factors, such as the currency route, the amount of money to be transferred, the type of transaction, and the payment method used. As an example, at the end of FY2021, a transfer of £1,000 into euros with Wise Transfer would have a £0.20 fixed fee and a 0.35% variable fee (£3.49), which brings the total fee to £3.69, or a 0.369% take rate. In FY2021, Wise’s overall cross-currency take rate was 0.70% (the cross-currency take rate is Wise’s total fees on international transfers as a percentage of the company’s payment volume). The company’s total take rate for FY2021, though, was 0.77% (the total take rate is Wise’s total fees earned for all customer activity as a percentage of the company’s payment volume). This means that Wise’s revenues that are not associated with international money transfers accounted for the other 0.07% of Wise’s total take rate for the year.

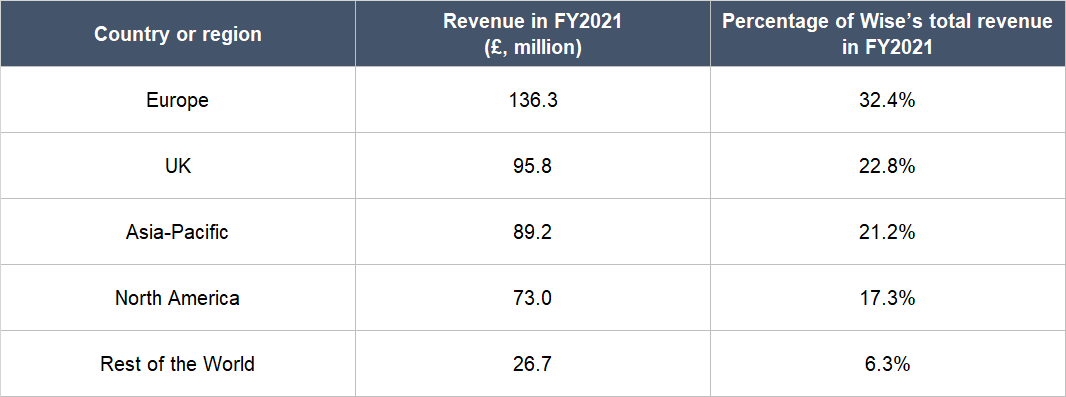

From a geographical perspective, Wise has heavy exposure to the European continent (including its home market of the UK), although it still has substantial business operations in other parts of the world. Table 1 below shows the geographical breakdown of the company’s revenue for FY2021:

Table 1; Source: Wise FY2021 annual report

Investment thesis

We have laid out our investment framework in Compounder Fund’s website. We will use the framework to describe our investment thesis for Wise.

1. Revenues that are small in relation to a large and/or growing market, or revenues that are large in a fast-growing market

Earlier in the “Company description” section of this article, we mentioned that Wise processed total payment volume of £54.4 billion and earned revenue of £421.0 million in FY2021. If the numbers from the company’s trading update for the first and second quarters of FY2022 are included, Wise’s total payment volume and revenue for the 12 months ended 30 September 2021 would be £64.9 billion and £485.1 million, respectively. These numbers are a drop in the ocean compared to the total amount of international money transfers that are conducted across the world.

In 2020, the global cross-border payments market was a staggering £18 trillion, according to payments consulting firm Edgar, Dunn & Company (EDC). This can be split into £9 trillion from large enterprises, £7 trillion from SMBs (small/medium businesses), and £2 trillion from consumers. Enterprises and businesses move money internationally for B2C (business-to-consumer) and B2B (business-to-business) purposes, such as for salaries and payments to contractors, suppliers, and service providers. For consumers, there are C2C (consumer-to-consumer) and C2B (consumer-to-business) use cases, such as personal remittances, e-commerce payments, real estate investments, and more.

Wise is targeting only cross-border payments from SMBs and consumers, but the two segments still represent massive room for growth for the company. For further perspective, in the consumer segment, Wise processed total payment volume of £49.4 billion in the 12 months ended 30 September 2021 while the market opportunity was £2 trillion in 2020. Within the SMB segment, the self-same figures were £15.6 billion and £7 trillion, respectively. Moreover, EDC estimates that the £9 trillion of cross-border payments from SMBs and consumers will grow to £13 trillion by 2026, driven by 5% annual growth in SMB payments to £10 trillion and 11% annual growth in consumer payments to £3 trillion. Underpinning this growth are a number of important trends, including “globalisation and internationalisation, increased migration and the rise of mobile and technological developments providing access to previously unbanked parts of the world.”

It’s smart for Wise – and aligned with its mission – to target cross-border payments for the SMB and consumer segments (we will discuss Wise’s mission in the “A management team with integrity, capability, and an innovative mindset” sub-section of this article). Although the two segments accounted for around 50% of the total global cross-border payments market in 2020, they made up around 95% of the total fees paid (large enterprises are charged relatively low fees to move money around internationally).

We think there’s a high chance that Wise can increase its market-share significantly in the years ahead. We showed earlier in Figure 2 that the company offers much better cost, speed, convenience, and fee-transparency compared to what traditional banks offer. Banks take up the lion’s share of the global cross-border payments market (95% of the SMB segment and 66% of the consumer segment) so this means that Wise is significantly better than its largest competitors. The company explained in its July 2021 IPO prospectus (Wise was listed in the same month) why it has an advantage over incumbent banks in the cross-border payments market (emphasis is ours):

“Moving money internationally is broken. Traditional banks are reliant on an outdated network of correspondent parties and held back by complex infrastructure. This means that both people and businesses have been overpaying for slow transfers, inconvenient customer experiences and are hit with opaque and hidden fees when moving money internationally…

…People and businesses are demanding transparency and cheaper fees alongside more convenient solutions with instant transfers ultimately becoming the norm.

But there are structural problems that are getting in the way of banks and traditional market participants. They are reliant on an outdated correspondent banking network for international transfers. Fees need to be high enough to cover the costs associated with this intermediary-heavy network which is also unreliable, hard to monitor and has manual or semi-automated processes. Further, the lack of transparency on fees means that there are limited pressures to solve this problem from within.

We have spent ten years building a replacement infrastructure for correspondent banking and have already made great progress in fixing the important problem of moving money across borders cheaply, conveniently and with transparent fees.”

Furthermore, Wise has been lowering its fees over time and will likely continue to do so, which would make it increasingly difficult for banks to compete against. We will discuss Wise’s fees, and why it is likely that the company will continue to lower them in the future, in greater detail in the “A management team with integrity, capability, and an innovative mindset” sub-section of this article.

2. A strong balance sheet with minimal or a reasonable amount of debt

As of 31 March 2021, Wise has £286.1 million in cash on its balance sheet while having just £98.7 million in total debt. This is a robust balance sheet, in our view.

It also helps that Wise has already been generating free cash flow for a few years. This is something we’ll cover in the “A proven ability to grow” sub-section of this article.

3. A management team with integrity, capability, and an innovative mindset

We mentioned earlier in the “Company description” section of this article that Wise was founded by Kristo Käärmann and Taavet Hinrikus. Both of them are still leading the company, with Käärmann as CEO and Hinrikus as executive chairman, although Hinrikus would be stepping down from his role sometime by July 2022 and be replaced by former long-time Netflix CFO, David Wells (Wells first joined Wise’s board in 2019). Another key leader of Wise is CFO Matthew Briers, who joined the company as CFO in 2015. We appreciate the fact that even though Käärmann and Briers are both young (they are 40 and 44, respectively), they each have years of experience leading the company.

On integrity

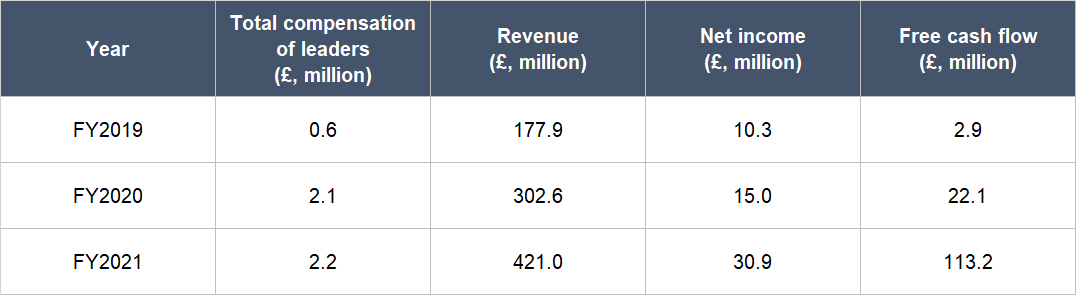

Wise has not shared much details on how its leaders are compensated. But what we do know is that in FY2019, FY2020, and FY2021, the total compensation of Wise’s leadership team (this includes the company’s CEO, CFO, and other directors) in each year were £2.2 million, £2.1 million, and £0.6 million, respectively. Compared to the scope of Wise’s business (see Table 2), these sums are nowhere near egregious and we think this is a good sign of the integrity that the company’s management team possesses.

Table 2; Source: Wise IPO prospectus

Another positive point on the integrity of Wise’s leaders is the skin in the game that Käärmann and Briers have. Before we get there, it’s worth discussing Wise’s dual share- class structure. The company has two share classes: (1) Class B shares, which are not traded and are not entitled to economic rights in Wise, but hold 9 voting rights per share; and (2) Class A shares, which are publicly traded and are entitled to economic rights in Wise, but hold just 1 vote per share. Each Wise Class B share also corresponds to one Wise Class A share. But this Wise Class A share is in a “dematerialised” form and so cannot be freely traded – it can only be freely traded when it “materialises,” in which case the corresponding Wise Class B share will cease to carry any voting right (and thus become effectively worthless since the Class B share in question will no longer have any voting nor economic rights in Wise). A “materialisation” can happen at any time when a Class B shareholder makes a request to Wise’s registrar (the entity responsible for recordkeeping of Wise’s shareholders). It’s important to note that each Wise Class A share that corresponds to one Class B share already exists – there’s no conversion needed to be done, it’s just that these Class A shares can’t be freely traded until they “materialise.”

Coming back to the topic of skin in the game, Käärmann owns 186.80 million Wise Class B shares, as of 7 July 2021, which gives him ownership of the exact same number of Class A shares because of the aforementioned 1-to-1 corresponding relationship between the two share classes. Based on Wise’s 19 October 2021 share price of £8.58, Käärmann’s Class A shares are worth £1.60 billion, which is a significant stake. Because Wise’s Class B shares carry no economic rights and will become worthless upon the “materialisation” of their corresponding Class A shares, we don’t think Käärmann’s Class B shares have any independent monetary value. Meanwhile, Briers owns 3.766 million Wise Class A shares as of 2 July 2021, which are worth £32.3 million.

We want to highlight that as a result of owning Wise’s super-voting Class B shares, Käärmann controls 40.75% of Wise’s voting power (as of 7 July 2021) despite holding only 18.78% of Wise’s total economic rights. Moreover, Käärmann owns the most number of Class B shares among Wise’s other shareholders, so he is the shareholder with the most voting rights by a wide margin (there are a total of 398.89 million Class B shares at the time of Wise’s listing, and the next largest holder – Hinrikus – owns just 53.97 million). A manager having significant control over the company can potentially be bad for shareholders. This concentration of Wise’s voting power in the hands of Käärmann means that we need to be comfortable with him at the company’s helm. We are.

Adding to our trust in Käärmann is Wise’s voting policy. If any of the other Wise Class B shareholders “materialise” their corresponding Class A shares, their Class B shares will lose their voting rights. In such an event, Käärmann’s voting power would increase. But if Käärmann’s the CEO and his voting power exceeds 50% because of the Class B shares he owns, the company’s voting policy will restrict his voting power to one vote below 50% (the threshold drops to 35% if Käärmann’s no longer the CEO).

We do note that Käärmann was embroiled in a minor controversy recently. Last month, he was fined £365,651 by the UK tax authority for a late submission of his personal tax returns for the 2017/2018 tax year. It’s never a good look from an integrity perspective for a company’s leader to be punished because of personal tax issues. But this currently seems to be only an isolated incident, so it’s nowhere close to being a deal breaker for us.

On capability and innovation

We rate Käärmann and his leadership team highly when it comes to capability and innovation. There are a number of things about them that have impressed us and that we want to discuss.

Firstly, Wise was founded when its co-founders, Kristo Käärmann and Taveet Hinrikus, experienced the pain – of high costs and long waits – involved with transferring money internationally. With their leadership, Wise built its own unique payments infrastructure to replace legacy and outdated systems. We are attracted to companies that are created because their founders saw a big problem that needed fixing – to us, it’s a positive signal on the entrepreneurial drive and innovative mindset of the companies’ leaders.

Secondly, there’s Wise’s mission – which came directly from the minds of Käärmann and Hinrikus and was in place at the time of the company’s founding – to “build money without borders: instant, convenient, transparent and eventually free.” We love Wise’s mission, especially the “eventually free” portion. The company acknowledges that getting to “eventually free” is not an easy task and will take many years. But it serves as a North Star for everybody in Wise to continuously work towards voluntarily lowering prices for the company’s customers. There are three things Wise is doing to get to “eventually free.” The company explained in its IPO prospectus:

“Eventually free means we’re always working to decrease prices and over time, there are three ways we’ll seek to lower prices further:

- Scale: As Wise gets bigger, we’re able to increase the amount of money flowing through Wise while controlling costs and keeping them stable. When volume increases faster than costs, every transfer costs slightly less to process.

- Reducing costs: We cut out intermediaries by continuing to integrate directly with central payment systems, thereby lowering costs to process payments. We pass those savings back to customers.

- Improving product and support: We aim to automate how customers’ money moves, which increases the quality of the product and reduces the amount it costs to run operations and support.”

From a conversation we had with Wise’s investor relations head, Martin Adams, there’s an ethical component to Wise’s mission: The company’s leaders do not believe in charging extortionate margins. But we think Wise’s mission also makes great business sense. It not only makes Wise’s services more attractive to customers over time, but it also makes it increasingly difficult for interlopers to compete with the company. More importantly, Wise’s mission also serves as a competitive advantage for the company. The company’s mission – to voluntarily drive down the prices customers pay – goes directly against human nature and in our opinion, is not something that can be easily replicated. During our conversation with Adams, he shared an amusing anecdote: Some stock market participants have asked Wise’s executives why the company is not raising prices since its competitors have much higher rates. (Figure 2 showed that Wise’s average fee of around 0.7% today is much lower than the 3% to 7% fee that banks typically charge.)

The third thing about Käärmann and his team that impressed us is the progress they have made in fulfilling Wise’s mission. Let’s start with the time taken for Wise Transfers to arrive. Earlier in this article, Figure 2 showed that 38% of Wise Transfers arrived instantly in FY2021, while 62% arrived in 1 hour and 83% arrived within 24 hours. These numbers have improved significantly over time as Figure 3 below shows; for example, by eye-balling the chart, only 12% or so of Wise Transfers were instant in FY2018 and only around 18% arrived within the hour. Wise has continued to make progress. In the second quarter of FY2022, 40% of all transfers were delivered instantly.

![]()

Figure 3; Source: Wise IPO prospectus

When it comes to the convenience that Wise brings to its users, a great proxy is the level of customer satisfaction that the company enjoys. On this end, Wise aces it. In FY2021, the company’s net promoter score (NPS) was an impressive 76. The NPS ranges from -100 to +100 and it measures the willingness of customers to recommend a company’s product or service to others. Moreover, in FY2021, 67% of Wise’s new customers came through recommendations from their friends or family. Wise is also much more transparent than banks when it comes to the fees that users have to pay to move money abroad, as illustrated in Figure 2. According to an EDC survey, only 4% of bank customers know that the full cost for sending money abroad consists of an upfront fee and an exchange rate mark-up. In the case of Wise, the company is fully transparent with its fees; Figure 4 below illustrates what you would see if you use Wise Transfer to transfer £1,000 to euros today:

![]()

Figure 4; Source: Wise FY2021 annual report

Finally, we come to the “eventually free” portion of Wise’s mission. The company’s fees are set by adding a small but sustainable margin over its unit costs on a transaction level. And if Wise is able to bring its unit costs down – for example, through processing more volume and thus gaining economies of scale or through integration with central payment systems, as we showed earlier in this subsection of this article – it’s thus able to offer lower fees to its customers. The company explained in its IPO prospectus:

“We aim to price our products, services and features sustainably without cross-subsidising between customers, products or routes. Our fees are set by adding a sustainable margin to our underlying unit costs on a transaction level. We lower prices where and when we can sustainably reduce costs, for example, by directly integrating with local payment networks or by renegotiating lower unit costs. This is a major difference between Wise and many other businesses.

As an example, when we integrated with Magyar Nemzeti Bank (the central bank of Hungary), customers sending to a Hungarian Forint bank account saw a 14% price drop on average as our costs of processing transfers to Hungary decreased. We have a team dedicated to understanding and reviewing the price of each of our more than 2,500 currency routes and other services. We have seen that, as volumes for a specific currency route grow, we are able to reduce our costs per transfer and therefore lower our average fees, while maintaining our margins. However, whilst we lower prices when our costs go down, sometimes our costs, and therefore our prices, can also increase.”

Figure 5 below shows Wise’s cross-currency take-rate (the light blue line) and customer price (the dark blue line) in each quarter from the first quarter of FY2019 to the fourth quarter of FY2021. Earlier in the “Company description” section of this article, we mentioned that the cross-currency take rate is Wise’s total fees on international transfers as a percentage of the company’s payment volume. In the same section, we also mentioned that Wise’s total fees on international transfers depend on a number of factors, such as the currency route, the amount of money to be transferred, the type of transaction, and the payment method used. Meanwhile, the customer price is based on a fixed basket of representative currencies and so is a more accurate reflection of Wise’s progress in lowering costs for international money transfers. There was a jump in Wise’s customer price in FY2020 because the company’s unit costs increased primarily as a result of accelerated investments in its infrastructure. But in FY2021, Wise lowered prices for currency routes that are used by 76% of its customers, with an average price decrease of 15%.

Figure 5; Source: Wise IPO prospectus

In all, Wise has made great progress in lowering its fees over time. As an example, it would have cost £5 to send £1,000 to euros with Wise Transfer six years ago. Today, the cost is more than 25% lower at £3.69. During the first quarter of FY2022, Wise dropped its customer price to 0.67%, after managing to lower prices for customers on 19 currencies. This was followed by a further reduction in the customer price in the second quarter to 0.62%. And importantly, Wise’s fees are much lower than its competitors: Besides what’s shown in Figure 2, the global average total fee for money remittance was 6.51% in December 2020, according to the World Bank.

Fourthly, Käärmann and his team have done an admirable job in growing Wise’s total take rate. In the “Company description” section of this article, we described Wise’s total take rate as the total fees earned by the company for all customer activity as a percentage of its payment volume. Below, Table 3 shows Wise’s total take rate and its two components (the cross-currency take rate and the take rate from other fees) from FY2019 to FY2021. The take rate from Wise’s other fees have seen substantial growth from 0.02% to 0.07% for the same period. Growth in other fees will be increasingly important for Wise in the future because the company’s mission is to bring its fees for international money transfers to zero eventually. Other fees have increased for Wise largely as a result of the increasing adoption of the Wise Account and Wise Business products, both of which were launched in 2017. As of 31 March 2021, 1.6 million Wise debit cards that are associated with the two products have been issued and customer deposits in them have grown from less than £1 billion in FY2019 to £3.7 billion. The rising popularity of Wise Account and Wise Business is a positive signal for Wise’s future overall growth as their users are more engaged. For example, in FY2021, users of the two products were around 50% more active and converted twice as much volume as Wise Transfer-only customers.

Table 3; Source: Wise IPO prospectus

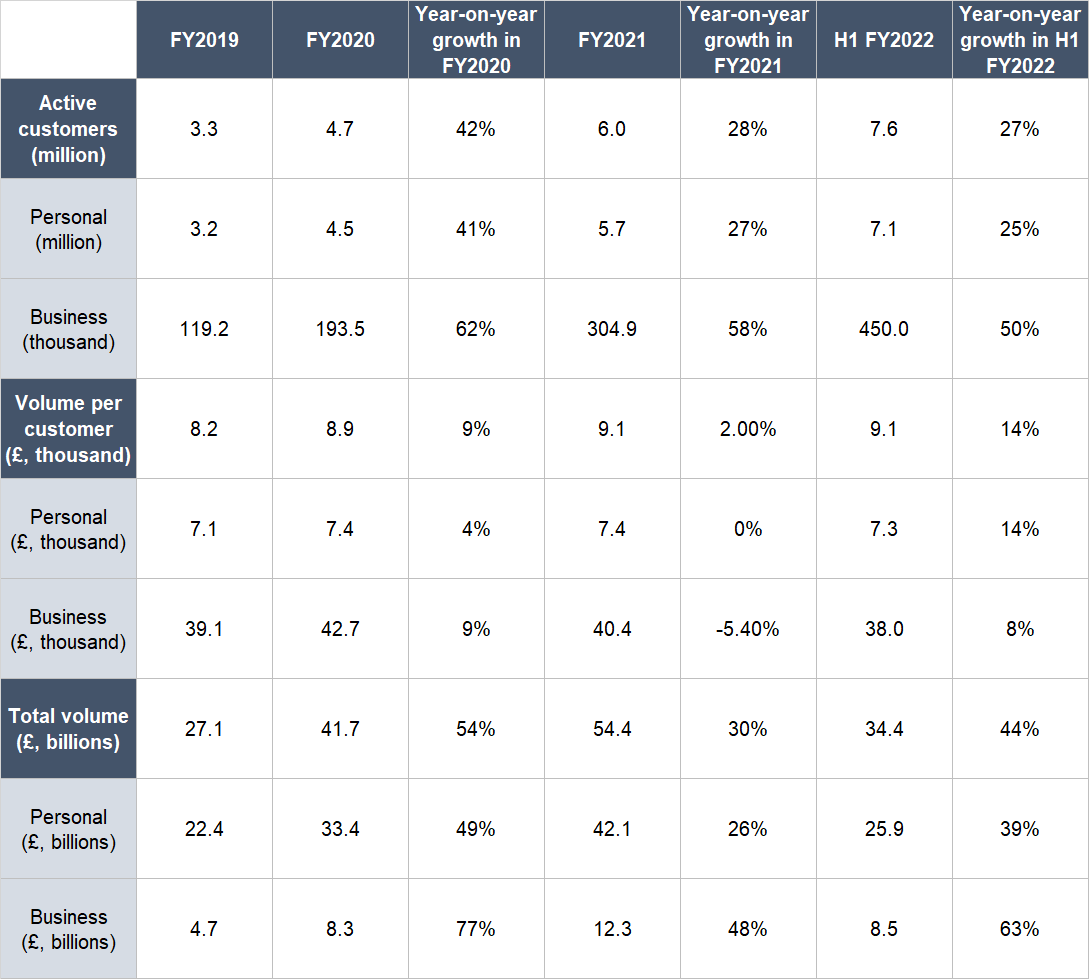

The fifth thing we want to discuss about Wise’s leaders is the company’s impressive growth in its number of active customers (for both businesses and consumers) and payment volume from FY2019 to the first half of FY2022. These are shown in Table 4 below.

Table 4; Source: Wise IPO prospectus and quarterly earnings updates

Sixth, we’re impressed with the right long-term focus that Käärmann and his team have when running Wise. Here’s the relevant part from Käärmann and Hinrikus’s excellent letter to Wise’s prospective investors that was included in the company’s IPO prospectus:

“We are working on a difficult, structural problem that will take a long time to solve. For generations, banks have been defined by borders. Traditional bank accounts trap our money in one country, making international lives more difficult and expensive than they need to be. We are building a better way, but it won’t happen overnight. Our mission has a long term horizon for success.

It can take years to increase the speed of payments and drop fees by integrating into a nation’s payment system. At the same time, we can create new features incredibly fast due to how our team and company is set up. Sometimes our progress may seem fast, but it requires patient, dedicated focus to make a lasting improvement in the fundamentals, such as the cost and speed.

Shareholders should understand that we prioritise our team’s efforts – and judge success – on the basis of mission progress. Revenue and returns are a function of our focus on our mission.”

As part of the discussion on Wise’s long-term focus, we also want to highlight that Wise has no ambition to become a super-app (an app that can fulfill all financial needs for an individual and a business), according to our conversation with Adams. Instead, Wise is concentrating its efforts to develop its infrastructure with the aim of becoming a global infrastructure-layer for money flows – management believes that the best infrastructure will win the race when it comes to moving money. We think this focus is smart and we agree with Wise’s management on the importance of owning the best infrastructure.

The seventh aspect about Wise’s management that we want to highlight is the excellent culture that Käärmann has fostered. Glassdoor is a website that allows a company’s employees to rate it anonymously. Wise currently has a 4.4-star rating out of 5 at Glassdoor, and 89% of Wise-raters would recommend a friend to work at the company. Käärmann also has an excellent 94% Glassdoor-approval rating as CEO, far higher than the average Glassdoor CEO approval rating of 69% in 2019.

4. Revenue streams that are recurring in nature, either through contracts or customer-behaviour

We see Wise’s revenue as highly-recurring in nature. Its revenue, as we have discussed in the “Company description” section of this article, comes from fees from international money transfers, domestic same-currency transactions, and use of the Wise debit card. These are activities that Wise’s customers are likely to repeat often.

But this does not mean that Wise’s customers will not reduce their activities with Wise’s products when economic conditions change. Wise has historically seen its customers move more money internationally when exchange rates are favourable for them, and hold back when rates turn against them. When the COVID-19 pandemic erupted, there was significant exchange rate volatility. For instance, the US$/€ exchange rate reached both a 12-month high and low in a single week. Wise experienced strong volume growth in March 2020 because of COVID-19-related exchange rate volatility, but then saw its volumes fall in April and May of the year. In future periods when Wise’s important currency routes see significant exchange rate volatility, the company could experience lower volume. This said, our eyes are fixed on the long-term opportunity with Wise and we think the company does have strong recurring revenue over the long run.

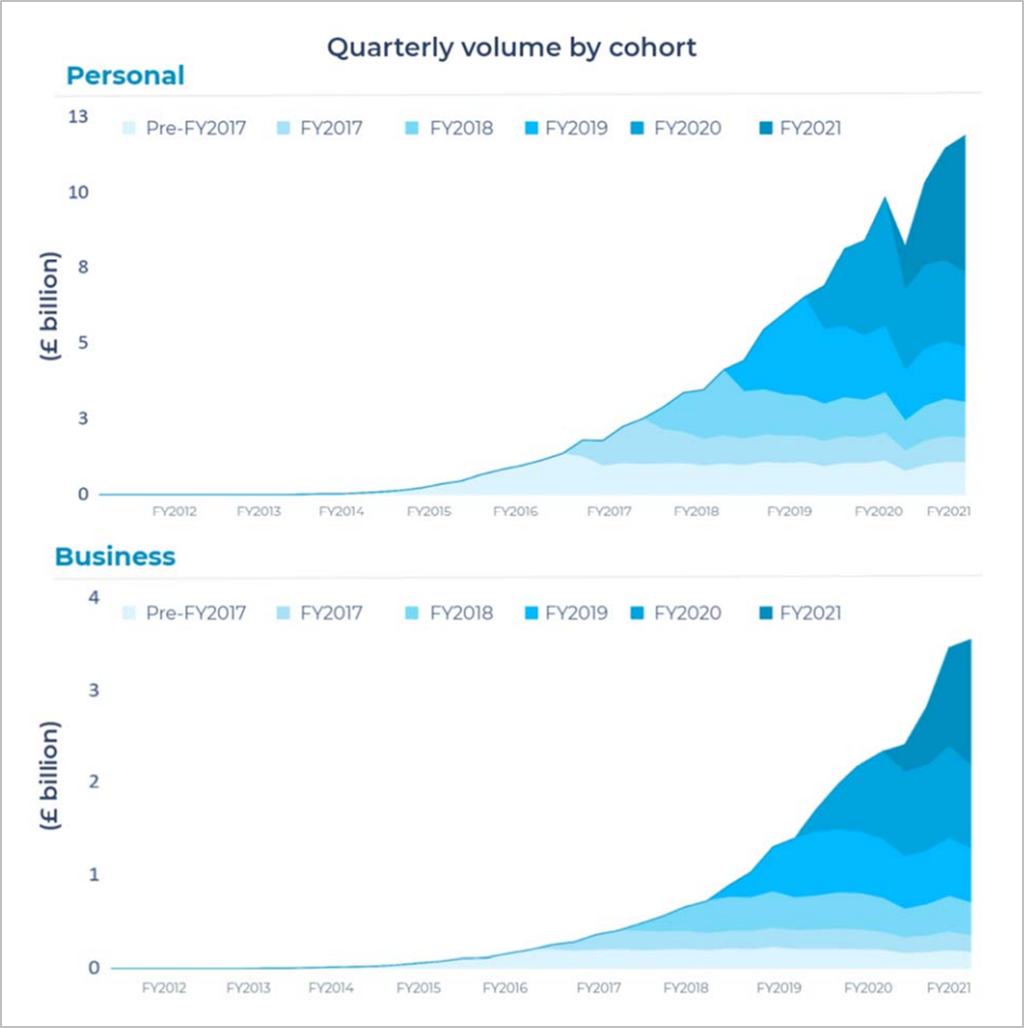

Helping build our confidence in the recurring nature of Wise’s business is the repeat behaviour of its customer cohorts. Customers typically join Wise for its low price and transparency and stay on for the company’s low price, fast transfer times, convenience, and wide currency-coverage, which are significantly better than the competition. Figure 6 below shows the company’s quarterly volume for personal and business customers by financial year cohort. It’s clear that Wise’s customers largely maintain their volumes with the company over time. The “thickness” of the blue bars for each personal customer cohort declines only slightly as the years pass, while the “thickness” of the blue bars for each business customer cohort remains roughly the same.

Figure 6; Source: Wise IPO prospectus

5. A proven ability to grow

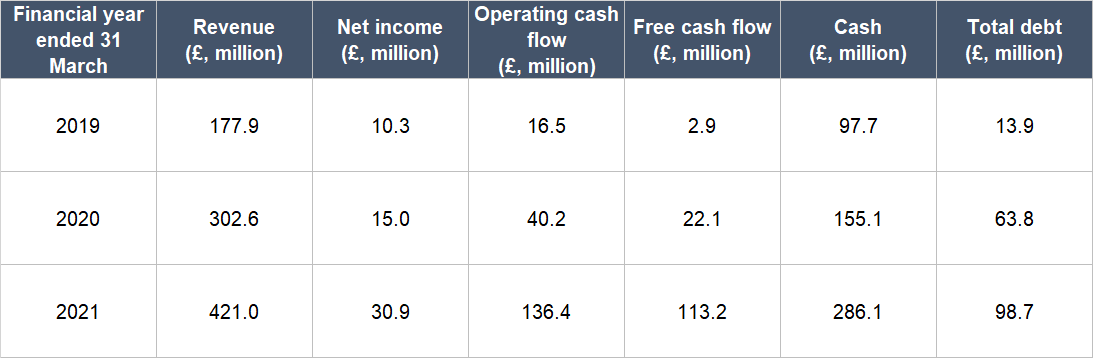

Wise has a short history as a public-listed company (its IPO was only in July 2021) so we don’t have much financial data to study for the company. But we like what we see. Table 5 below shows the key annual financial figures for Wise that we can obtain:

Table 5; Source: Wise IPO prospectus

A few key things to highlight from Wise’s historical financials:

- Revenue has compounded at an excellent annual rate of 53.8% from FY2019 to FY2021. Despite having to contend with the emergence of the COVID-19 pandemic in 2020, Wise’s revenue growth in FY2021 was still strong at 39.1%.

- We appreciate the fact that Wise was profitable for the entire period under study and that its net income margin has been trending in the right direction (from 5.8% in FY2019 to 7.3% in FY2021).

- The company also produced positive operating cash flow and free cash flow in each year from FY2019 to FY2021, with rising margins in each year for both numbers. Wise’s operating cash flow margin (operating cash flow as a percentage of revenue) climbed from 9.3% in FY2019 to 13.3% in FY2020 and to 32.4% in FY2021. The company’s free cash flow margin (free cash flow as a percentage of revenue) for the same years were 1.6%, 7.3%, and 26.9%, respectively. (The operating cash flow we’re looking at is the net corporate cash generated from operating activities. Wise’s official cash flow statement includes cash inflows from customer deposits for the Wise Account and Wise Business products as operating cash flow, but they should not be included.)

- Wise has maintained a robust balance sheet for the entire time frame we’re looking at. The company’s cash has comfortably exceeded its debt in each year. (The cash we’re looking at is Wise’s corporate cash. The cash amount found in the company’s official balance sheet include cash from customer deposits for the Wise Account and Wise Business products, which we think should be excluded, since they belong to Wise’s customers.)

- We usually look at changes in a company’s share count over time to determine if there has been egregious shareholder dilution in the past. In the case of Wise, we did not look at its share count since the company was listed only in July 2021. We do note that Wise had a share count of 994.59 million (referring only to the Class A shares) right after its listing and we will be comparing Wise’s future share counts with this number. Ultimately, what we want is to see Wise produce business growth that significantly outweighs increases in its share count, if any.

Wise has managed to continue producing strong results with revenue growing by 43.1% to £123.5 million compared to a year ago in the first quarter of FY2022, and by 25.4% to £132.8 million compared to a year ago in the second quarter. There was strong growth from both consumers (up 36.9% to £96.9 million in the first quarter and up 18.9% to £103.4 million in the second quarter) as well as business customers (up 71.6% to £26.6 million in the first quarter and up 55.6% to £29.4 million in the second quarter).

6. A high likelihood of generating a strong and growing stream of free cash flow in the future

We think Wise aces this criterion for a few reasons:

- First, there is a high likelihood, in our view, that Wise’s revenue can continue to grow at a high double-digit rate in the years ahead. The company’s core money-transfer product is much better than what banks are offering (and banks have the biggest share of the global cross-border payments market). Moreover, Wise is likely to voluntarily drive prices lower over time, in line with its mission, which would attract even more customers. This increases Wise’s volume, which makes it easier for it to continue driving down prices, thus setting up a virtuous cycle.

- Second, Wise has already been generating free cash flow for at least the past three years. Moreover, the company’s free cash flow margin in FY2021 reached an impressive 26.9%. There’s no reason for us to believe that Wise cannot sustain its free cash flow margin at a similar level in the future.

Valuation

Our initial purchases of Wise shares were completed in early-October 2021. Our average purchase price was £10.50 per share. At our average price and on the day we completed our purchases, Wise’s shares had a trailing price-to-free cash flow (P/FCF) ratio and trailing price-to-sales (P/S) ratio of around 92 and 23, respectively.

We like to keep things simple in the valuation process. In Wise’s case, we think the P/FCF and P/S ratios are appropriate metrics to gauge the value of the company. For the P/FCF ratio, it is because Wise has been producing free cash flow for a number of years, and its free cash flow margin has already increased to a strong 26.9% in FY2021. For the P/S ratio, it’s useful when Wise’s free cash flow becomes light in the future because it is reinvesting into its business for future growth.

The P/FCF and P/S ratios of 92 and 23 are high and that’s a risk. But we’re willing to pay a premium for a few reasons. First, despite Wise’s rapid revenue growth over the past few years, its share of the SMB and consumer segments of the global cross-border payments market is still tiny, suggesting huge room for growth. Second, because of Wise’s much better value proposition for customers compared to banks, we believe that the company has a high chance of being able to increase its market share significantly over time and it can thus continue growing at a rapid clip in the years ahead. Third, we think that Wise can continue commanding strong free cash flow margins as its business grows.

For perspective, Wise carried P/FCF and P/S ratios of around 75 and 18 at its 19 October 2021 share price of £8.58.

The risks involved

We see a few key risks that could make our decision to invest in Wise end up looking unwise:

- In our view, Wise’s co-founder and CEO Kristo Käärmann has been instrumental in the company’s past growth and will continue to have an outsized influence on its future. We think Wise’s ability to grow will depend heavily on its adherence to its mission, and this is something that will mostly be shaped by Käärmann since he’s setting the tone at the top as CEO. So we think there’s key-man risk with Wise. We will be watching the leadership transition if Käärmann were to leave the company for any reason.

- Since Wise’s mission is to eventually make international money transfers free for its customers, the growth in the company’s other fees will be important for the company’s future overall business growth (we explained this in the “A management team with integrity, capability, and an innovative mindset” sub-section of this article). But there’s no guarantee that Wise’s growth in other fees can make up for declines in its cross-currency fees, so this is a key risk we’re keeping an eye on.

- In the “ Revenue streams that are recurring in nature, either through contracts or customer-behaviour” sub-section of this article, we explained that Wise’s business could be negatively impacted by periods of wild fluctuations in its key currency routes. If there are prolonged periods of heightened currency-volatility, Wise’s growth could be stunted for a long time.

- Wise’s products may be much better than what banks are offering, but the company is not just competing against banks. Wise is also crossing swords with other fintech players that at times offer similar fees for users (here’s a comparison of Wise with other fintech competitors for Singapore-based users). There’s a possibility that other fintech players could build much better products than what Wise can in the future. But given that banks hold the lion’s share of the cross-border payments market, there could be multiple winners in the collective fight against banks, and our bet is that Wise will be among them.

- As if competition with other fintech companies isn’t enough, there are also cryptocurrencies that are jostling for room with Wise in the cross-border payments market. In particular, we’re paying attention to country-led efforts in cryptocurrencies. China is one of the first few countries in the world that are experimenting with central bank digital currencies (CBDCs). The technology underlying CBDCs will be blockchain, which is the same technology behind cryptocurrencies. Citizens will hold digital wallets that contain the digital code for each CBDC unit. If CBDCs do take off, a citizen in one country could conveniently transfer and convert currency into the digital wallet of a citizen in another country, likely for or nearly free. This could make the core international money-transfer product of Wise obsolete.

- The last important risk we’re keeping our eyes on is valuation risk. We think Wise’s business is likely to grow at a rapid clip for many years and so it deserves its premium valuation. But if there are any hiccups in Wise’s business – even if they are temporary – there could be a painful fall in the share price. This is a risk we’re comfortable taking as long-term investors.

Summary and allocation commentary

To summarise Wise, it has:

- Massive room for growth in the SMB and consumer segments of the global cross-border payments market

- A robust balance sheet with significantly more cash than debt

- A management team that came up with a wonderful mission and has an excellent track record in execution and innovation (such as by building out its own infrastructure for international money flows and by growing the adoption of its products)

- High levels of recurring revenues through repeat customer behaviour and also high customer-retention

- A history of impressive revenue, net income, and free cash flow growth for a number of years

- A good chance of being able to produce strong free cash flow in the future given its long growth-runway

As it is with every company, there are risks to note for Wise. The main ones we’re watching include key-man risk; the possibility that Wise’s other fees fail to grow materially; the chance that Wise’s business could be hurt in prolonged episodes of currency volatility; competition from other fintech companies and cryptocurrencies such as government-led efforts with CBDCs; and Wise’s high valuation.

After weighing the pros and cons, we decided to initiate a position of around 1% in Wise in early-October 2021. Our initial position in the company can be considered to be a small-sized allocation. We appreciate all the strengths we see in Wise. But our enthusiasm is currently tempered by the company’s high valuation and the question marks that lie around the growth of Wise, especially in relation to the other fees component of the business and the threat from CBDCs.

And here’s an important disclaimer: None of the information or analysis presented is intended to form the basis for any offer or recommendation; they are merely our thoughts that we want to share. Of all the other companies mentioned in this article, Compounder Fund also owns shares in Netflix. Holdings are subject to change at any time.