Compounder Fund: Tractor Supply Investment Thesis - 19 Aug 2020

Data as of 17 August 2020

Tractor Supply Company (NASDAQ: TSCO) is one of the 40 companies in Compounder Fund’s initial portfolio. This article describes our investment thesis for the company.

Company description

Tractor Supply, which is listed and based in the US, is the largest retailer in the country that caters to recreational farmers, ranchers, and people who enjoy the rural lifestyle. Unlike what Tractor Supply’s name suggests, the company does not sell tractors. Here’s Tractor Supply describing its own business:

“At TSC [Tractor Supply Company], customers find everything they need to maintain their farms, ranches, homes and animals. As the inventors of the “do it yourself” trend, our customers handle practically every chore themselves, from repairing wells to building fences, welding gates together, constructing feed bins, taking care of livestock and pets, repairing tractors and trucks and building trailers for hauling.

TSC’s [Tractor Supply Company’s] products include: clothing, equine and pet supplies, tractor/trailer parts and accessories, lawn and garden supplies, sprinkler/irrigation parts, power tools, fencing, welding and pump supplies, riding mowers and more.”

As of 27 June 2020, Tractor Supply operates an e-commerce website and 1,881 Tractor Supply stores across 49 states in the US. In addition, the company also owns and runs 180 PetSense stores in 25 states in the country. Petsense, acquired in late 2016 by Tractor Supply, is a small-box specialty retailer focusing on pet products for small and mid-size communities. Tractor Supply’s stores are mostly located outside of metropolitan cities.

In fiscal 2019 (fiscal year ended 28 December 2019), Tractor Supply pulled in US$8.35 billion in total revenue from the following product-categories: Livestock and pet (47%); Hardware, tools and truck (21%); Seasonal, gift and toy products (20%); Clothing and footwear (8%); and Agriculture (4%).

Investment thesis

We have laid out our investment framework in Compounder Fund’s website. We will use the framework to describe our investment thesis for Tractor Supply.

1. Revenues that are small in relation to a large and/or growing market, or revenues that are large in a fast-growing market

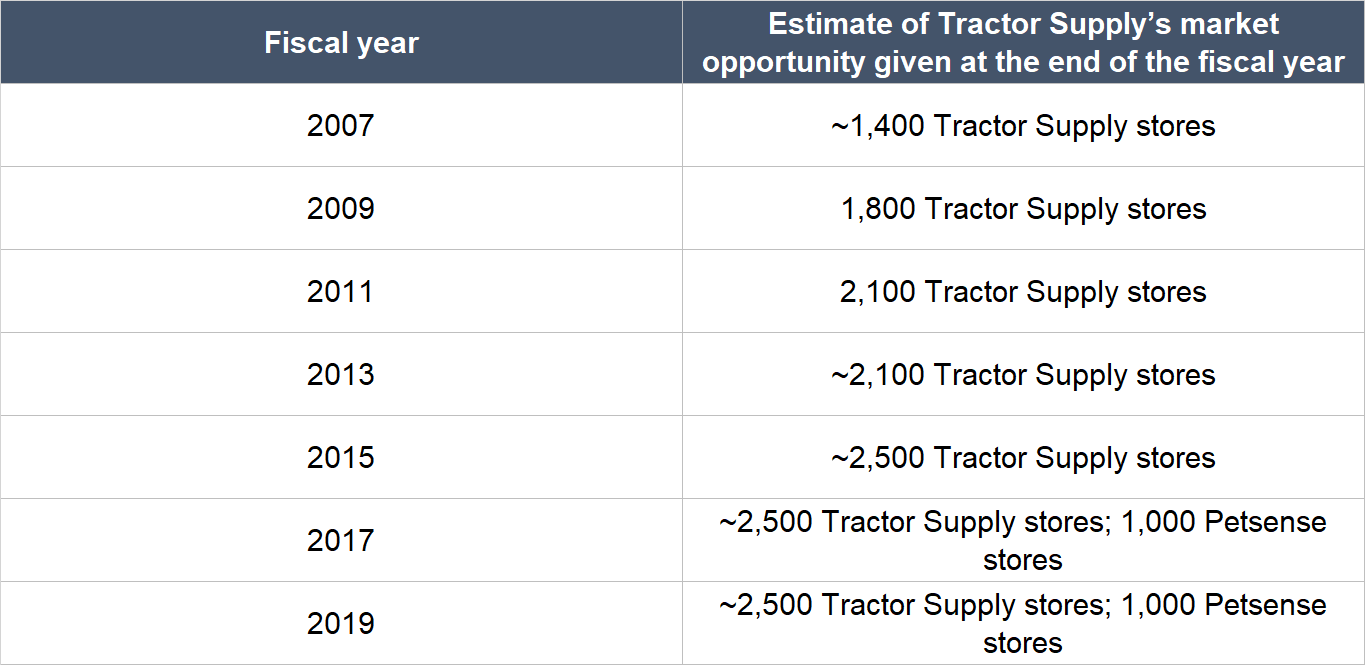

Based on their own estimates given the size of Tractor Supply’s target-communities, the company’s management team believes that there is room for 600 additional new Tractor Supply stores. This is equivalent to an increase in store-count of around 30% from where Tractor Supply stands now. Importantly, the existing stores that Tractor Supply operates are also growing, as demonstrated by the company’s long history of achieving positive comparable store sales growth. Comparable store sales measures the change in revenue from all of Tractor Supply’s stores – including its online store – that were open for at least a year at the reporting date. We will have more discussion of Tractor Supply’s comparable store sales later. Tractor Supply also believes that there is an opportunity for up to 1,000 Petsense stores, which is more than five times as many as the company has now.

The company’s estimates of its market opportunity sound sensible to us. According to the 2019 edition of the United States Department of Agriculture’s Rural America at a Glance report, there were more than 46 million Americans (a sizeable population) who lived in non-metropolitan areas of the country in July 2018; this compares with the current overall US population of 330 million. Meanwhile, the pet products market in the US was US$95.7 billion in 2019, based on data from the American Pet Products Association. For perspective, Tractor Supply’s total revenue in the 12 months ended 27 June 2020 was ‘only’ US$9.31 billion, with Petsense taking up only a small share (8.7% of Tractor Supply’s current total store count of 2,061 are Petsense stores).

We wouldn’t be surprised too if, in the future, Tractor Supply’s management increases their estimate of the total number of the company’s stores that the US can support. The company’s management has steadily increased this estimate over time as the table below illustrates:

Source: Tractor Supply annual reports

2. A strong balance sheet with minimal or a reasonable amount of debt

As of 27 June 2020 (the second quarter of fiscal 2020), Tractor Supply had US$1.21 billion in cash and cash equivalents, and US$952.5 million in total debt. This gives the company a strong net-cash position.

Moreover, Tractor Supply also has a long history of generating free cash flow, which we will cover later.

3. A management team with integrity, capability, and an innovative mindset

On capability and innovation

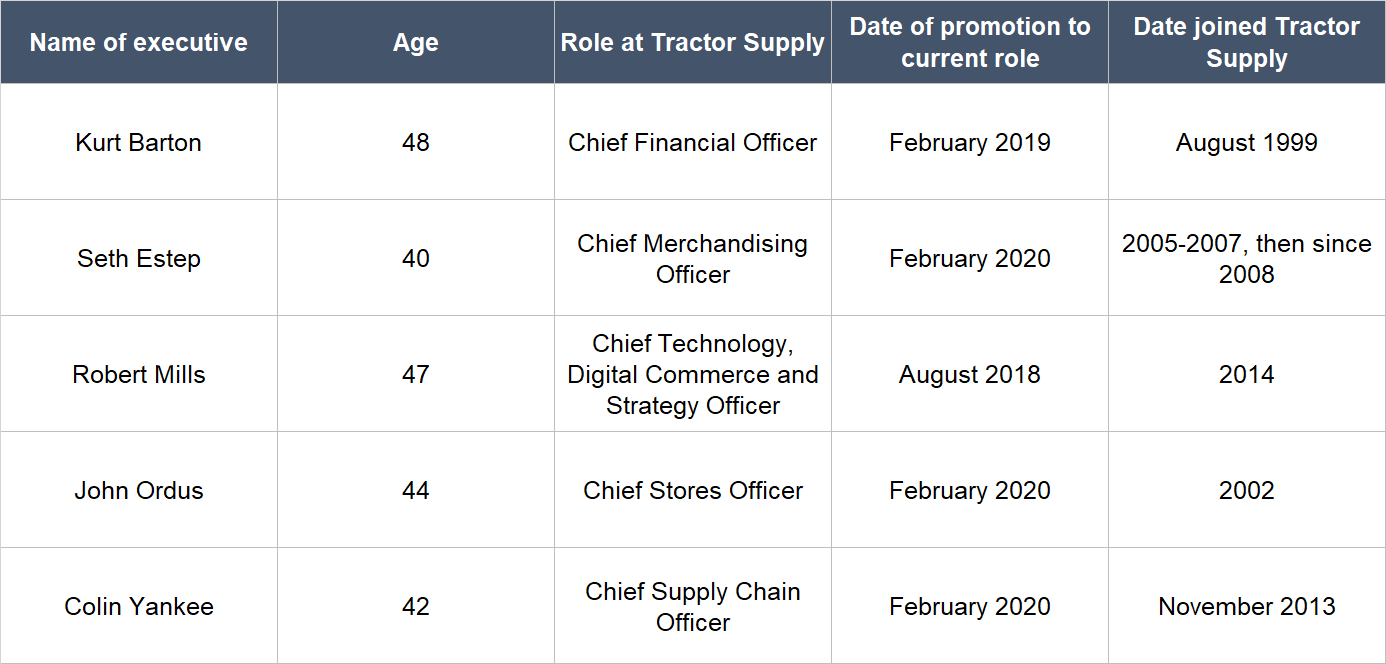

Hal Lawton, 45, joined Tractor Supply on 13 January 2020 as CEO, replacing Greg Sandfort, who joined the company in 2007 and served as CEO since December 2012. Before joining Tractor Supply, Lawton was the president of the departmental store chain Macy’s and a senior vice president of eBay prior to his Macy stint. Although Lawton is new at Tractor Supply, he’s supported by a team who are relatively young and who each have years of experience at the company. Some members of this team are shown in the table below.

Source: Tractor Supply annual report and website

Lawton has enjoyed a great start to his career at Tractor Supply, with the company reporting stellar results in the first half of 2020, despite the US being one of the worst-hit countries in the world from the current COVID-19 pandemic:

- Revenue in the first quarter of fiscal 2020 came in at US$1.96 billion, up 7.5% from a year ago, supported by a 4.3% increase in comparable store sales. Net profit grew 9.0% to US$83.8 million while diluted earnings per share climbed 12.7% to US$0.71. Operating cash flow improved from a negative US$13.0 million a year ago to a positive US$83.9 million, and free cash flow stepped up from a negative US$41.8 million to a positive US$54.3 million.

- The second quarter of 2020 had significantly stronger results. Revenue surged 35.0% higher from a year ago to US$3.18 billion, underpinned by “triple-digit e-commerce growth” and comparable store sales growth of 30.5%. Net profit soared 54.5% from a year ago to US$338.7 million and diluted earnings per share was up 61.1% to US$2.90. Operating cash flow jumped by 151.2% to US$909.2 million and free cash flow rose 177.5% to US$852.2 million.

Beginning in March 2020, COVID-19 started to have a significant positive impact on consumer demand across all of Tractor Supply’s product categories and geographic regions, as the company’s customers focused on the care of their homes, land, and animals. For the first half of fiscal 2020, Tractor Supply enjoyed an “unprecedented demand for spring and summer seasonal categories along with exceptional growth in everyday merchandise, including consumable, usable and edible products.”

The emergence of COVID-19 and the subsequent boost in demand at Tractor Supply, has obviously nothing to do with Lawton. Meanwhile, there’s a case to be made that Tractor Supply could do so well in the first half of fiscal 2020 because of great initiatives that were already in place before Lawton’s arrival. For instance:

- As early as 2019’s first quarter, 70% of e-commerce orders from Tractor Supply’s customers were fulfilled at the company’s stores, partly because of a well-executed BOPIS (Buy Online Pickup in Store) programme. By the fourth quarter of 2019, Tractor Supply had enjoyed 30 consecutive quarters of double-digit online sales growth.

- Tractor Supply ended 2019 with nearly 15 million Neighbor’s Club members (Neighbor’s Club is the company’s loyalty programme) and a retention rate of 80%. According to a May 2019 investor presentation by Tractor Supply’s management, Neighbor’s Club members accounted for more than 50% of the company’s sales. Moreover, when compared to non-members, members typically spent three to four times more and transactions were three times higher.

But we think it’s still to Lawton and his team’s credit that Tractor Supply could build on its past foundations for its results in the first half of fiscal 2020. We’re also impressed by the moves that Lawton and his team have taken this year. In all, we think Lawton’s tenure as Tractor Supply’s CEO thus far deserves an “A” rating for the following reasons:

- In early 2020, when COVID-19 started becoming a really serious issue in China, Tractor Supply’s management set up a cross-functional team that focused on solving potential problems in the company’s supply chain. Then as the COVID-19 situation evolved and it became clear that the US would be impacted too, a global pandemic response team was created to help the company navigate the crisis; the team included employees from Tractor Supply as well as third-party members who can help the company on medical and risk issues.

- Again in early 2020, Tractor Supply’s management raised its team members’ wages (Tractor Supply calls its employees team members, a sign that the company places high importance on its human capital), extended sick pay leave for team members, installed plexiglass barriers at cashier stands to protect the health of team members, and accelerated the rollout of contactless payment solutions in-store.

- Compensation and benefits for Tractor Supply’s team members were permanently raised in the second quarter of fiscal 2020, and more than 2,000 frontline workers at the company’s stores and distribution centres started to receive annual restricted stock units.

- During the second quarter of fiscal 2020, Tractor Supply added over 5,000 net new team members across the company’s stores and distribution centres to meet higher customer-demand. For perspective, the company ended fiscal 2019 with 32,000 full and part-time team members, so 5,000 new individuals is not a trivial addition.

- Tractor Supply rolled out curbside pickup, same-day/next-day delivery, and a new-look website during the second quarter of 2020.

- Two new strategic initiatives were introduced by Lawton in July 2020. First, he wants to build a field activity support team (termed “FAST team”). This initiative is designed to improve the merchandising activities in Tractor Supply’s stores. Team members in the FAST team will focus on merchandising activities so that in-store team members can spend more time on customer service and potentially drive higher comparable store sales. Tractor Supply is looking to hire 1,500 team members to join the FAST team, whose work includes executing merchandising programs during the year and catering to seasonal programs and sales-driving initiatives.

- The second initiative by Lawton is for Tractor Supply to improve its technology and services capabilities in areas such as contactless payments, in-store WiFi, ship-from-store online fulfillment, delivery, and mobile (in July 2020, Tractor Supply launched a new mobile app that’s integrated with Neighbor’s Club). We think this is a critical initiative for the company.

- In the third quarter of 2020, Tractor Supply will begin tests on programmes to improve the usage of space in its stores.

- In the second quarter of 2020, management decided to raise Tractor Supply’s capital spending for the whole of 2020 from a previous range of US$225 million-US$275 million to a new range of US$300 million-US$325 million. The “vast majority” of the increase in capital spending is earmarked for new in-store and technology initiatives. We think the decision to increase capital spending in this current environment when there is an influx of new customers also looks smart to us as the investments can help Tractor Supply retain the new customers (Tractor Supply identified 3.3 million new customers in the second quarter of 2020, up 14% from a year ago).

Tractor Supply has a number of other traits we like that we think are a result of past-management’s actions:

- The company has a network of 12 distribution centres across the US that serve its nearly 1,900 Tractor Supply stores in the country. Around 74% of its merchandise in fiscal 2019 passed through these warehouses that helps to keep operations efficient and costs at a minimum.

- More than 30% of Tractor Supply’s product sales from the last three fiscal years came from brands that are exclusive to the company. We think these products add an extra layer of differentiation to the company’s offering.

- In our view, what makes Tractor Supply stand out among its competitors is its incessant drive to provide “legendary customer service” that results in loyal customers. The company hires in-store team members who live and appreciate what is called the “Out Here” lifestyle and we think this practice creates a shopping environment that naturally resonates with the company’s customers. A 2008 profile of Tractor Supply from Bloomberg stated that the company employs a welder, a rancher, a farmer and an equestrian in each store to advise customers; we don’t know if this holds true today, but Tractor Supply definitely still emphasises hiring people with these skills for its stores. And on the point on loyalty, the Neighbor’s Club loyalty programme has grown its member count from “10+ million” in fiscal 2018 to 15 million in fiscal 2019 and 17 million today.

- Information on competitors is hard to come by, but Tractor Supply believes that it has built up a formidable lead over its peers. In late 2015, the company said it was five times larger than its next four competitors combined.

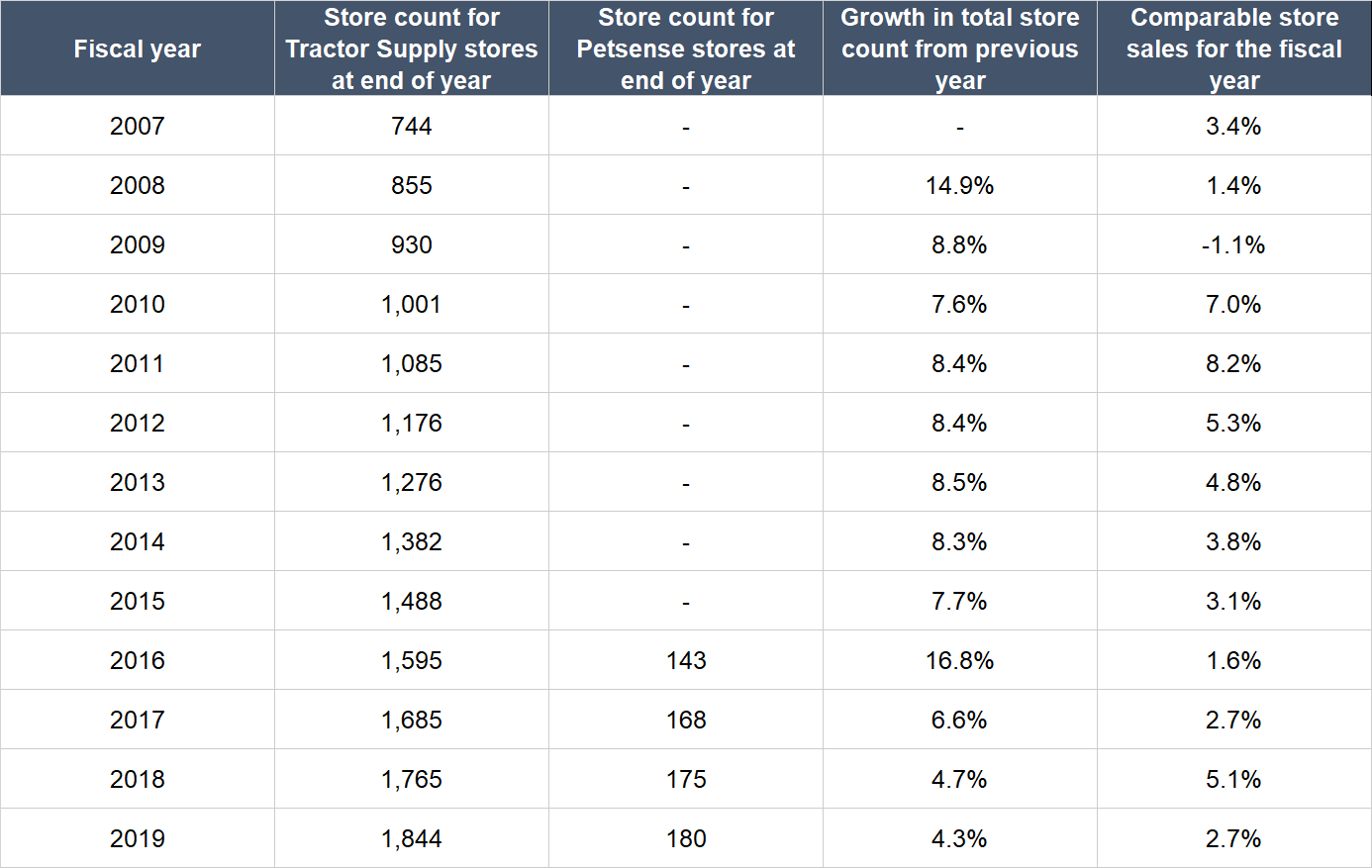

- The table below shows that Tractor Supply has managed to grow its store count significantly over a long period of time (from fiscal 2007 to fiscal 2019) while posting mostly positive comparable store sales growth. In fact, fiscal 2009 was the only year when comparable store sales growth was negative – and even then, the decline was small, and we note that this was also during the 2008-09 Great Financial Crisis.

Source: Tractor Supply annual reports

On integrity

We think Tractor Supply has a well-designed compensation structure that aligns the interests of its leaders and shareholders. Here’s why:

- In fiscal 2019, 68% of the target compensation-mix for the company’s CEO for the year came from long-term incentives, 18% from short-term incentives, and 14% from the base salary.

- The long-term incentives come in the form of stock options, restricted stock units (RSUs), and performance-based stock units (PSUs), that all vest over a three-year period. This means that the incentives are linked to multi-year changes in Tractor Supply’s stock price, which in turn is driven by the company’s long-term business performance.

- The PSUs for the CEO depend on the three-year growth of Tractor Supply’s earnings per share and revenue; if the growth targets aren’t met, the PSUs will not vest.

- The short-term incentives for the CEO depend on the net income growth of Tractor Supply for the year; we would have preferred the metric to be earnings per share, but net income growth is still acceptable.

- The target compensation-mix in fiscal 2019 for Tractor Supply’s other key leaders are: 52% from long-term incentives, 21% from short-term incentives, and 27% from the base salary. We like that more than half of the key leaders’ compensation-mix came from long-term incentives and that the structures for the long-term and short-term incentives are the same as that for the CEO.

- In fiscal 2019, former CEO Gregory Sandfort’s total remuneration was US$8.7 million, which is a reasonable sum when compared to the scope of Tractor Supply’s business (revenue and net profit of US$8.35 billion and US$562.4 million, respectively, in fiscal 2019).

Moreover, Tractor Supply requires its CEO to hold at least six times his/her base salary in the company’s shares. For perspective, new CEO Hal Lawton’s annual base salary is currently US$1.125 million. Other key leaders in the company are also required to hold Tractor Supply shares that are worth one to four times their base salaries, depending on their title. We think this ownership-requirement further aligns the interests of Tractor Supply’s management with that of the company’s shareholders.

4. Revenue streams that are recurring in nature, either through contracts or customer-behaviour

The core of Tractor Supply’s business consists of products that the company calls C.U.E – consumable, usable, and edible. These are everyday items such as livestock feed and bedding, pet food, lubricants, and seasonal products such as heating, pest control and twine.

C.U.E sales provide a level of repeat business for Tractor Supply. Even though the company does not explicitly mention what percentage of its revenue comes from C.U.E products, we believe the percentage should be north of 50%, based on the breakdown of Tractor Supply’s sales by product-category that we provided earlier.

5. A proven ability to grow

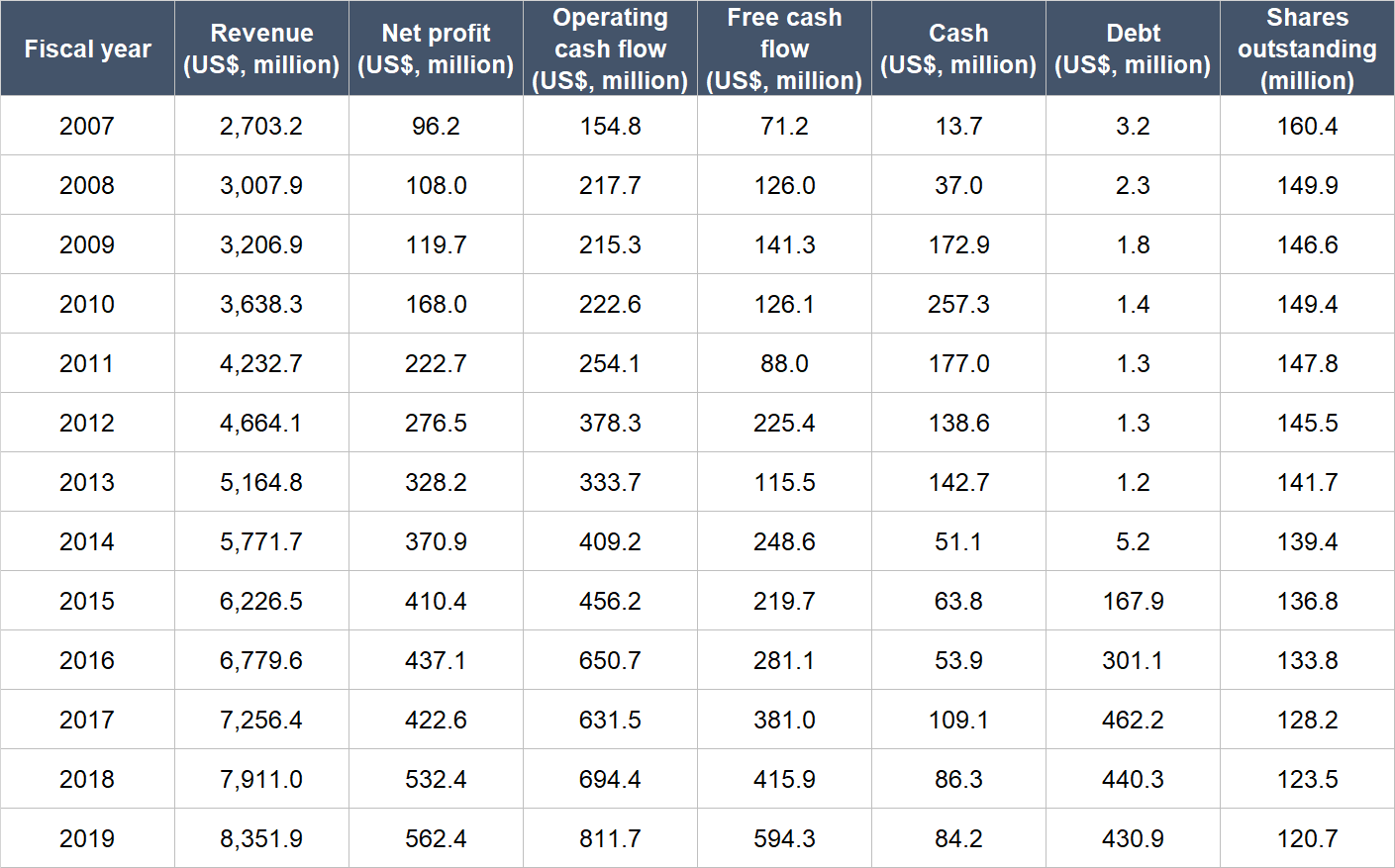

The table below shows the important financial figures for Tractor Supply from fiscal 2007 to fiscal 2019:

Source: Tractor Supply annual reports

A few points about Tractor Supply’s financials:

- Impressively, revenue has grown in every single year from fiscal 2007 to fiscal 2019, even in fiscal 2008 and fiscal 2009 which are the years of the Great Financial Crisis. For the entire time frame we’re studying, Tractor Supply’s revenue has compounded at a respectable rate of 9.9% per year; over the past five years from fiscal 2014 to fiscal 2019, the annual growth rate was similar at 7.7%.

- Net profit grew in nearly each year (fiscal 2017 was the only year with a decline) and had stepped up at a healthy pace of 15.8% annually from fiscal 2007 to fiscal 2019. The nearer-term growth rate (from fiscal 2014 to fiscal 2019) was decent at 8.7%.

- Operating cash flow and free cash flow were both consistently positive with no major declines for the entire time period we’re looking at. From fiscal 2007 to fiscal 2019, there was solid growth in operating cash flow and free cash flow at 14.8% per year and 19.3% per year, respectively. From fiscal 2014 to fiscal 2019, the respective annual growth rates were equally robust at 14.7% and 19.0%.

- Tractor Supply’s balance sheet carried significantly more debt than cash from fiscal 2015 to fiscal 2019. But we note that the company’s free cash flow in each of these years could cover the net-debt position comfortably. Moreover, Tractor Supply has flipped to a net-cash position as of the second quarter of fiscal 2020.

- The company’s share count has fallen at 2.3% per year from fiscal 2007 to fiscal 2019; over the past five years, the share count reduction has accelerated to 2.8% annually. It will be great if the buybacks continue (assuming that the buybacks will happen at reasonable valuations) because it means that existing Tractor Supply shareholders end up holding a larger share of the pie. It’s worth noting that Tractor Supply’s diluted earnings per share grew by 11.9% per year from fiscal 2014 to fiscal 2019 – faster than the net profit growth of 8.7% per year over the same period – because of the share buybacks.

There are many traditional brick-and-mortar retailers in the US that have suffered because of the current COVID-19 pandemic. But Tractor Supply has done really well, as we’ve discussed earlier. The company had enjoyed higher sales in its physical stores and booming growth in its online sales channel. On the e-commerce growth, we want to point out that Tractor Supply has been developing its omnichannel retail efforts over the past few years. You can see this in the slides below from Tractor Supply’s May 2019 Investment Community Day event:

Source: Tractor Supply investor presentation

During Tractor Supply’s fiscal 2020 second-quarter earnings call, management did acknowledge that part of its robust growth in the first half of the year had come from transitory factors such as the COVID-19 pandemic and seasonal good weather. But Tractor Supply’s leaders also saw lasting tailwinds. Here’s CFO Kurt Barton on the topic:

“Now another way to look at this quarter’s comparable-store sales growth is to break down the comp between transitory factors, such as government stimulus checks and COVID-19-related sales as compared to sustainable, more structural tailwinds like trip consolidation, the increase in new customers and re-engaged customers, the rural revitalization trends and the growth in companion animal ownership. While it is difficult to estimate the impact from each of these drivers, we believe that nearly half of the Q2 comparable-store sales growth can be attributed to structural tailwinds, giving us a sustainable opportunity for growth.”

6. A high likelihood of generating a strong and growing stream of free cash flow in the future

There are two reasons why we think Tractor Supply excels in this criterion.

First, the company has been generating positive and growing free cash flow for years. Tractor Supply’s free cash flow margin (free cash flow as a percentage of revenue) is thin, averaging at just 4.9% from fiscal 2014 to fiscal 2019. But as a retailer, the company’s free cash flow margin will necessarily be low. What’s more important is the stability in the free cash flow, and here, Tractor Supply excels.

Second, there’s still plenty of room to grow for Tractor Supply, as we discussed earlier. Moreover, we think Tractor Supply has carved out a strong competitive position in its niche as a rural-lifestyle-products retailer and this makes it tough for competitors (of both the online and offline variety) to snatch business from the company. In turn, it’s likely that the company’s revenue will increase over time, leading to higher free cash flow.

Valuation

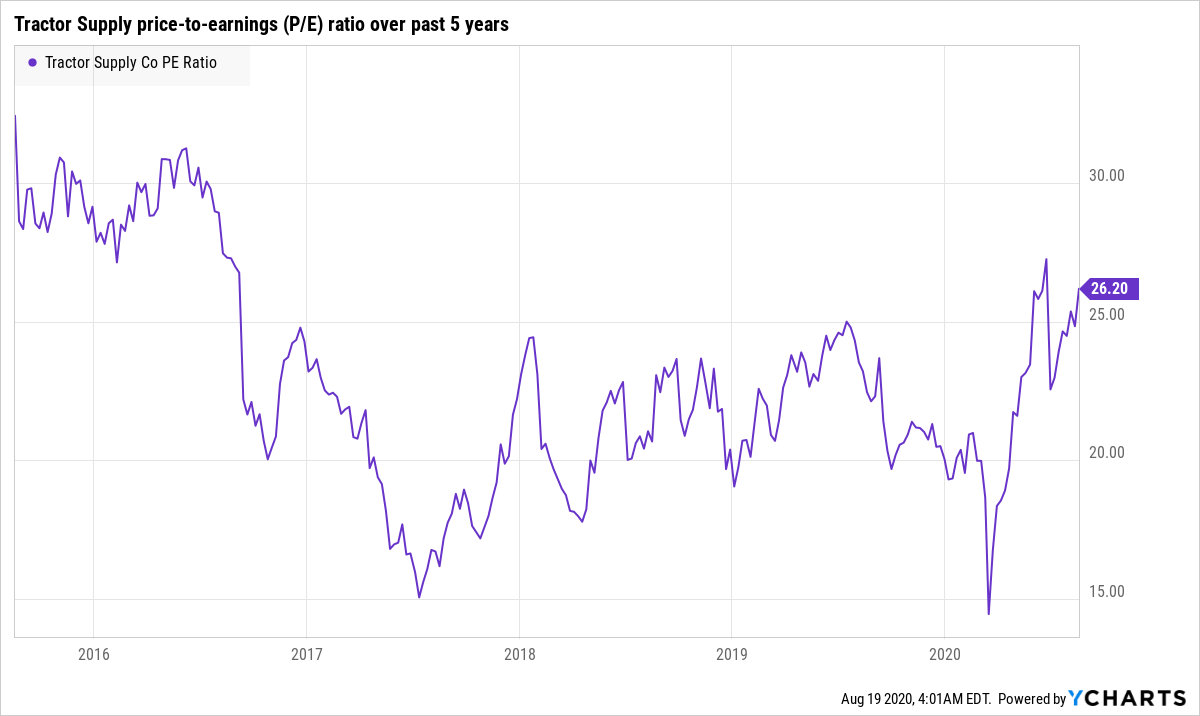

We bought Tractor Supply’s shares for Compounder Fund at an average price of US$144 each. Given the company’s steadily growing profit, we think the price-to-earnings (P/E) ratio is a suitable gauge of its value. With trailing earnings per share of US$5.84, our average purchase price translates to a P/E ratio of 24.6.

The chart above shows Tractor Supply’s P/E ratio over the past five years. You can see that a P/E ratio of 24.6 is not high relative to history. Moreover, it is just a smidge higher than Tractor Supply’s five-year average P/E ratio of 23. In all, we think that a P/E ratio of 24.6 is a good valuation to pay for Tractor Supply, which is a company that has a solid track record of growth, is riding on some strong secular trends, and has a relatively large market opportunity.

The risks involved

There are three big risks we’re keeping an eye on, with all being equally important to us.

The biggest risk that we see in brick-and-mortar retailers is e-commerce. This applies to Tractor Supply too – there is a chance that competition from e-commerce players can harm the company’s business. But to its credit, we think Tractor Supply has done a great job in building a strong competitive edge (through great customer service and a focus on the rural-lifestyle-products niche) and using technology to improve its omnichannel retail operations. Tractor Supply’s triple-digit online sales growth in fiscal 2020’s second quarter is a testament to the company’s omnichannel capabilities.

Current CEO Hal Laton has enjoyed a great start to life at Tractor Supply. He and his team have also implemented initiatives to increase sales and improve customer experiences that we wholeheartedly agree with, such as building support-teams, raising team members’ wages, increasing capital spending on technology, rejigging store lay-outs, and more. We think Lawton’s report-card deserves an “A” so far. But he is still fairly new to Tractor Supply and his ability to execute will be tested in the coming quarters. We’re watching the situation.

We will also be keeping an eye on whether Tractor Supply can actually open the 600 new stores that management has suggested is possible. After all, future stores could cannibalise existing ones. We will be watching for signs of market saturation by tracking Tractor Supply’s comparable store sales growth.

Summary and allocation commentary

Rounding up Tractor Supply, here’s what we see in the company:

- Tractor Supply has the opportunity to increase its store count in the US significantly from its current base of 2,061.

- The company’s balance sheet is currently robust with more cash than debt

- CEO Hal Lawton is new to the job, but he has done excellent work so far. He’s also supported by a team of leaders who have been with Tractor Supply for many years each. Moreover, the company has a well-designed compensation structure that aligns the interests of the management team and shareholders.

- The core of the company’s sales come from consumable, usable, and edible products, thus generating repeat business.

- Tractor Supply has a long history of producing decent growth in revenue, profit, operating cash flow, and free cash flow. The current COVID-19 pandemic has also benefited Tractor Supply’s business, resulting in significantly faster growth compared to the company’s own history.

- We think there’s a high likelihood that Tractor Supply will be able to continue generating strong free cash flow in the future.

The key risks we’re watching include competition from e-commerce, Lawton’s short tenure, and possible market saturation.

Ultimately, we initiated a 2.5% position – a medium-sized allocation – in Tractor Supply with Compounder Fund’s initial capital. We appreciate Tractor Supply’s long history of steady growth and its good valuation. But we’re also mindful that Tractor Supply’s historical growth rates are not the fastest. Moreover, we’re unsure if there truly is significant room for the company to grow its store count, although to be clear, we think the odds are in our favour.

And here’s an important disclaimer: None of the information or analysis presented is intended to form the basis for any offer or recommendation; they are merely our thoughts that we want to share.