Compounder Fund: Pushpay Investment Thesis - 22 Nov 2020

Data as of 17 November 2020

Pushpay Holdings (ASX: PPH) is one of the 40 companies in Compounder Fund’s initial portfolio. This article describes our investment thesis for the company.

Company description

Pushpay is headquartered in New Zealand and its shares are listed there as well as in Australia. The company provides a succinct description of what its business does in its latest annual report for its financial year ended 31 March 2020 (FY2020), so we won’t reinvent the wheel:

“Pushpay provides a donor management system, including donor tools, finance tools and a custom community app, to the faith sector, non-profit organisations and education providers located predominantly in the United States (US) and other jurisdictions. Our leading solutions simplify engagement, payments and administration, enabling our Customers to increase participation and build stronger relationships with their communities.

Church Community Builder is a subsidiary of Pushpay Holdings Limited and provides a Software as a Service (SaaS) church management system in the US and other jurisdictions. Church Community Builder provides a platform that churches use to connect and communicate with their community members, record member service history, track online giving and perform a range of administrative functions. Combined, Pushpay and Church Community Builder deliver a best-in-class, fully integrated ChMS, custom community app and giving solution for customers in the US faith sector.”

In essence, Pushpay provides a set of software tools that enable churches to manage donations from church members and better engage with these members. From the business-description above, it’s not a surprise to note that more than 98% of Pushpay’s revenue in FY2020 and the first half of FY2021 was sourced from the USA, even though the company is based in New Zealand.

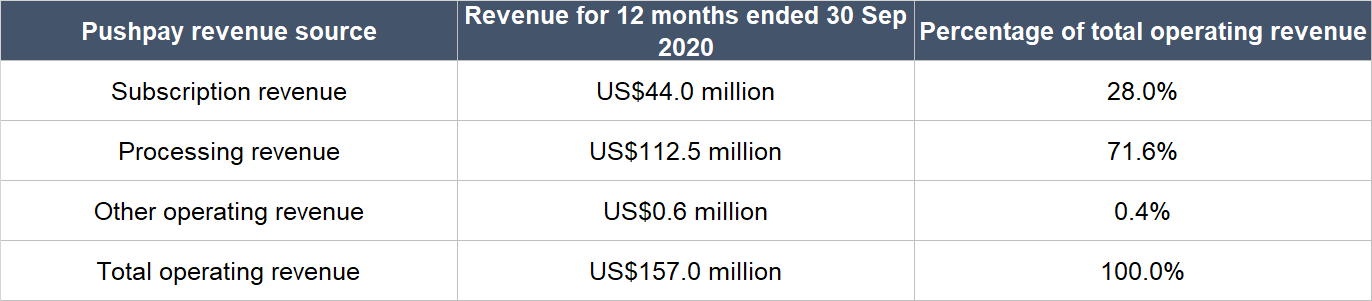

Pushpay charges customers that use its app a monthly or annual subscription fee that depends on the size of the customer (the average weekly attendance at the church). In addition, Pushpay charges its customers a processing fee for payment transactions (the donations from churchgoers) made through its app and this fee is usually a percentage of the payment volume. Lastly, Pushpay also earns a small amount of revenue by providing data integration, training, and other implementation services. The table below shows a breakdown of Pushpay’s operating revenue from these three sources for the 12 months ended 30 September 2020:

Source: Pushpay annual report and half-yearly earnings update

Pushpay processed US$6.0 billion in payments through its app in the 12 months ended 30 September 2020. Based on its processing revenue for the same period, we can see that Pushpay’s take-rate for processing donations from church members is around 1.8% for this timeframe.

Investment thesis

We have laid out our investment framework in Compounder Fund’s website and will use the framework to describe our investment thesis for Pushpay.

1. Revenues that are small in relation to a large and/or growing market, or revenues that are large in a fast-growing market

Pushpay is tackling a niche market in the form of the US faith sector, and to a lesser extent non-profit organisations. Although it’s a niche, Pushpay’s total addressable market is large compared to the current size of its business. The company estimates that its total addressable market stands at more than US$1 billion, based on its long-term target of winning over 50% of the medium and large church segments in the USA. Pushpay views churches with 0-199 average weekly attendees as small, 200-1,099 attendees as medium, and 1,100 or more attendees as large.

For perspective, Pushpay earned US$159.1 million in revenue in the twelve months ended 30 September 2020, which is clearly much lower than its touted market opportunity. We think Pushpay’s view on its market opportunity is sensible for a few reasons.

First, there are many more churches that can become Pushpay customers. Pushpay had 10,896 customers as of 30 September 2020, of which around 6,220 are medium to large churches. According to the Christianity Today website and a 2017 study done by Simon Brauer, there were more than 240,000 churches in the USA in 2012. A study from Lifeway Research published in 2019 showed that around 11% of Protestant churches have 250 or more weekly attendees. So, we estimate that there are probably somewhere between 20,000 to 36,000 churches in the USA that belong to Pushpay’s definition of medium to large.

Second, there’s plenty more payment volume in churches that Pushpay can process. As we mentioned earlier, Pushpay’s trailing-12-months payment volume is US$6.0 billion. According to Charity Navigator, citing data from the Giving USA 2018 report, US$127 billion was donated to religious organisations in the USA in 2016. We think it’s reasonable to assume that church-giving makes up a significant majority of the US$127 billion. This is because 63% of all Americans currently identify as Christians, while up to 26% of Americans have no particular religion, based on data from the Pew Research Centre – in other words, an overwhelming majority of religious people in the USA identify with the Christianity faith.

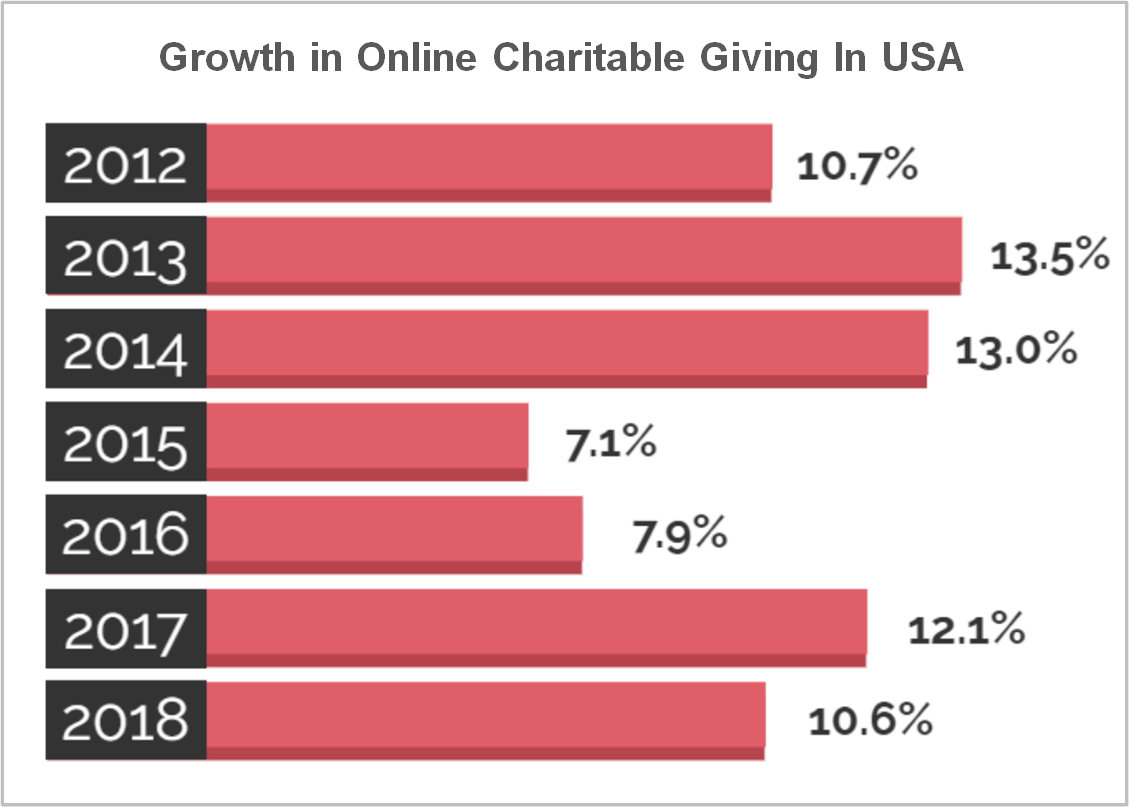

Third, prior to COVID-19, there was already a multi-year trend of high single-digit to low-teens growth in online charitable donations. This is illustrated in the chart below. The emergence of the COVID-19 pandemic has accelerated online giving and we don’t think this trend will stop. Online giving is just so much more efficient and convenient for churches and their members, and Pushpay has been a key benefactor. Pushpay’s total payment processing volume of US$3.2 billion in the six months ended 30 September 2020 is 14% higher compared to the six months ended 31 March 2020 – this is significant because December is a seasonally high period for church donations. Pushpay also shared commentary recently on the acceleration it’s seeing in online giving:

“[From FY2020 annual report]

While a number of organisations have temporarily closed their physical premises in response to COVID-19, Pushpay has seen a clear shift to digital whereby Customers are utilising its mobile first technology solutions to communicate with their congregations…… In terms of digital giving trends, Pushpay’s processing volume over the month of March was higher than the Company expected prior to COVID-19. Pushpay expects the increase in digital giving as a proportion of total giving resulting from COVID-19, to outweigh any potential fall in total giving to the US faith sector.

[From FY2021 first-half earnings update]

While a number of organisations have temporarily closed their physical premises in response to COVID-19, Pushpay has seen a clear shift to digital whereby Customers are utilising its mobile-first technology solutions to communicate with their congregations…… In terms of digital giving trends, Pushpay’s processing volume over the six months ended 30 September 2020 was higher than the Company expected prior to COVID-19. Pushpay expects the increase in digital giving as a proportion of total giving resulting from COVID-19, to outweigh any potential fall in total giving to the US faith sector.”

During an August 2020 interview with the Sydney Morning Herald, Pushpay’s CEO Bruce Gordon shared more insights on churches’ recent digital transformation:

“Sermons are recorded mid-week now and streamed throughout the course of the entire week. We have churches running services seven times on a Sunday and our largest churches some of them are reaching upwards of 300,000 attendees over the course of a week through the digital streaming through the mobile app…

…We have essentially embedded opportunities to express your generosity and build out what we call a donor management system, which identifies where individual church participants are relative to their giving journey…

…Suddenly in mid-March our phones rang off the hook for a number of weeks in the US as the churches said ‘by golly I’ve closed my doors I need a digital strategy, I need the ability to reach my congregation through mobile,’ so it’s been a high growth period for us…

…Our top 25 churches have experienced an average of a 15 per cent increase in giving in June versus the previous June, it’s huge.”

Source: Nonprofitsource.com

There’s also an important point we want to bring up about Pushpay and its market opportunity. We think there’s a good chance that Pushpay can achieve significant market penetration (the 50% or more market share that it’s aiming for), because it is focusing on a niche area.

2. A strong balance sheet with minimal or a reasonable amount of debt

Pushpay ended September 2020 with US$23.1 million in cash and cash equivalents but US$47.6 million in total borrowings, which gives rise to a net debt position (total debt less cash and cash equivalents) of US$24.5 million. On the surface, this does not look like a strong balance sheet. But looking under the hood, a different picture emerges.

The company’s high debt is due to borrowings taken to fund the US$87.5 million acquisition of the aforementioned Church Community Builder. Prior to the deal, which was completed on 1 December 2019, Pushpay had a pristine balance sheet that had no debt. Pushpay funded the acquisition of Church Community Builder through a combination of cash on hand and US$62.5 million in debt. As a result, Pushpay ended FY2020 with a net-debt position of US$49.7 million.

Pushpay started to generate positive free cash flow in FY2020. In the first half of FY2021 (the six months ended 30 September 2020), Pushpay produced US$26.7 million in free cash flow. This allowed Pushpay to bring its net-debt position down from US$49.7 million as of 30 March 2020 to US$24.5 million as of 30 September 2020. We’re confident that Pushpay has a high level of recurring revenue (more on this later) and that it can generate strong and growing free cash flow in the future (more on this later too). So we are comfortable with Pushpay’s current net-debt position and we don’t think it is a problem at all.

3. A management team with integrity, capability, and an innovative mindset

There are some important recent management shuffles at Pushpay and sales of shares by the company’s insiders that we want to discuss.

Pushpay is currently led by Bruce Gordon, who became the company’s chairman in February 2014 and then took on the CEO role in June 2019. The company was co-founded by Chris Heaslip and Elliot Crowther in 2011. Heaslip was already CEO at the time of Pushpay’s listing in New Zealand’s stock market in August 2014 (the Australia listing happened in October 2016). In May 2019, he resigned as Pushpay’s CEO before stepping away completely from the company by resigning as a director in March 2020. Meanwhile, Crowther, who was an executive director of Pushpay since July 2011, had left the company in June 2018 on the same day that he sold all of his 9% stake.

Elsewhere, Christopher and Peter Huljich (who are father and son) announced in early-November this year that they will be stepping down as directors of Pushpay on 31 December 2020. This came just a few months after the Huljich family’s decision in July 2020 to sell a quarter of their Pushpay stake to end with 43.2 million shares. The Huljich family are early investors in Pushpay, having first invested in the company in December 2013. They have also been directors of the company since before its New Zealand IPO.

Then on 26 August 2020, Gordon announced that he had agreed to sell around half of his Pushpay stake; as of 31 March 2020, he held 2.768 million Pushpay shares. The sale of shares alone does not concern us. After all, Gordon’s remaining stake (some 1.384 million shares) are worth around A$9.74 million at the 17 November 2020 share price of A$7.04. This works out to around US$7.1 million and it is still much higher than Gordon’s total compensation for FY2020 (more on this later). But the problem is, Gordon has also signalled his intention to be stepping down as CEO once a suitable replacement is found.

Wrapping it up, we’re faced with the following situation at Pushpay: (1) The company can no longer count on its founders’ involvement; (2) the Huljich family, an important early investor, sold a big chunk of shares and is no longer interested in having any say on the future direction of the company; and (3) Bruce Gordon recently sold half of his Pushpay stake and he wants to step down as CEO soon. All these will mean that Pushpay has lost and will lose important, experienced personnel. Moreover, the bunched timing of their departures (would-be departure in the case of Gordon) and sale of shares is disquieting. This instability at the top of Pushpay is a risk we’re watching, but we don’t see it as a dealbreaker.

On integrity

For FY2020, Bruce Gordon received US$354,000 in total compensation. This is a very reasonable sum when compared to the scope of Pushpay’s business – the company’s revenue and free cash flow in FY2020 were US$129.8 million and US$23.1 million, respectively. Moreover, Gordon’s compensation included restricted stock units (RSUs) that vest over three years, and a short-term incentive that is based on operating revenue, subscription fees added, and EBITDAF (earnings before interest, tax, depreciation, amortisation and FOREX changes) targets. We appreciate the multi-year vesting period of the RSUs. Although we will prefer long-term incentives over short-term ones, the metrics that guide Gordon’s short-term incentive are still aligned with the interests of Pushpay’s shareholders, in our view.

Source: Pushpay annual reports

We’re also heartened by the fact that over the past few years, the total compensation for Gordon’s predecessor, Chris Heaslip, was reasonable and grew at a slower pace than the company’s revenue. These are shown in the table above.

On capability and ability to innovate

We already know that Pushpay is on the lookout for Bruce Gordon’s successor as CEO, and Gordon himself has so far been in the hot seat for just 17 months. So it may appear that discussing Pushpay’s history of growth and innovation would not be that meaningful. But we think there’s still value in doing so. This is because Pushpay’s Chief Financial Officer, Shane Sampson, has been in the role for five years (since October 2015); meanwhile, Steve Basden, who has the title of Chief Growth Officer, joined the company at least four years ago. Put another way, the fingerprints of Sampson and Basden can likely be found on the good work Pushpay has accomplished in recent years.

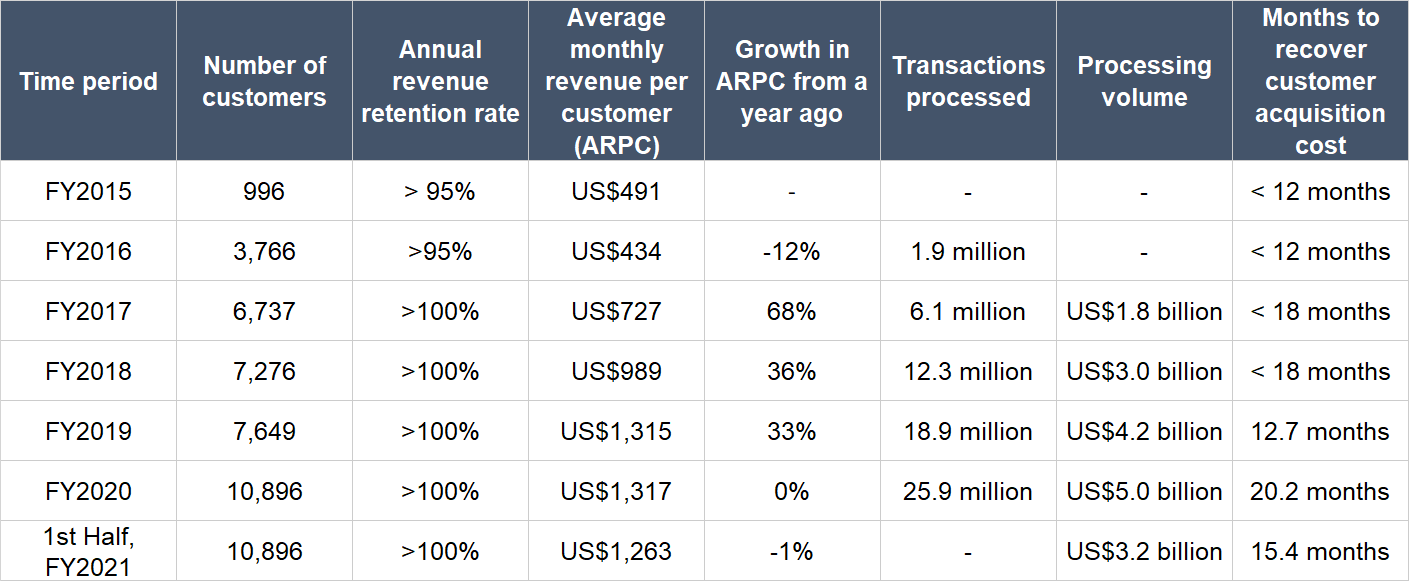

There are a number of things we want to highlight here. First, Pushpay’s management team has excelled at the following important things since FY2015: (1) Growing the number of customers: (2) retaining customers; (3) driving higher revenue per customer; (4) growing the number of transactions and payment volume; and (5) maintaining sensible unit economics by recouping customer acquisition costs in significantly less than two years. Here’s a table showing all of these:

Source: Pushpay annual reports and half-yearly earnings update

We want to share some further comments on the numbers for FY2020 and the first half of FY2021. Pushpay’s aforementioned December 2019 acquisition of Church Community Builder had noticeable impacts on the company’s customer-count and average revenue per customer (ARPC). In FY2020, Pushpay’s customer-count increased by 3,247 and this growth can be split into organic growth (+531) and Church Community Builder (+2,716). Meanwhile, growth in Pushpay’s ARPC was affected because Church Community Builder has a lower ARPC when compared to Pushpay’s customer base prior to the acquisition. If Church Community Builder is excluded, Pushpay’s ARPC for FY2020 would be US$1,614, up 23% from FY2019, and the ARPC for the first half of FY2021 would have increased from a year ago too.

Speaking of Church Community Builder, it looks like an astute acquisition, and this is the second thing we want to highlight. We think the deal has two strong positives: There is high potential for cross-selling and for Pushpay to enhance its platform with Church Community Builder’s software products. Indeed, shortly after the acquisition, Pushpay started integrating its giving and engagement solution with Church Community Builder’s church management system. In September this year, this combined product suite was branded as ChurchStaq. It’s still early days for the combined product suite but the signs are promising. Pushpay shared the following comments in its FY2021 first-half earnings update:

“Subsequent to the acquisition of the Church Community Builder business, Pushpay has seen an increased number of Customers utilising the combined Pushpay and Church Community Builder platforms to meet their giving and engagement needs, providing a strong indication that the market values a fully integrated solution. Over the six months ended 30 September 2020, sales of the combined product offering, ChurchStaq™, outperformed internal expectations, which reinforces the hypothesis that the majority of customers prefer an integrated end-to-end solution.”

Third, Pushpay has a strong track record of innovation, the latest of which is the introduction of ChurchStaq. The table below shows the key moments in the timeline of Pushpay’s history of product innovation from its founding in 2011 to April 2020. Here are some of the new product features Pushpay added in the six months ended 30 September 2020:

- Integrated sign-in provides financial administrators with a streamlined log-in experience to transition between Pushpay’s giving and engagement platform and Church Community Builder’s church management system

- Transaction History provides users with their transaction history, giving details, essential giving information, and the latest church content and announcements in an integrated manner; this helps reduce the administrative burden on churches

- Worship Planning enables church leaders to access and update service plans on their mobile phones, including the ability to add songs and other items to the service.

Source: Pushpay annual report

Fourth, Pushpay’s ability to generate free cash flow has improved remarkably in the past few years. The chart below, which shows Pushpay’s EBITDAF margin (EBITDAF as a percentage of revenue) since the second half of FY2018, provides an apt illustration. There will be more discussion on Pushpay’s free cash flow later.

Source: Pushpay half-yearly earnings update

Fifth, Pushpay appears to have a positive corporate culture, which we think will lead to happier and more productive employees. Glassdoor is a platform that allows employees to rate their companies anonymously. Currently, 71% of Pushpay-raters on Glassdoor will recommend the company to a friend. Meanwhile Bruce Gordon has a 97% approval rating, far higher than the average Glassdoor CEO rating of 69% in 2019.

4. Revenue streams that are recurring in nature, either through contracts or customer-behaviour

As we mentioned earlier, Pushpay derives its revenue from subscriptions and payment-processing fees. We view both these sources as highly recurring in nature.

For subscription revenue, this is a monthly or annual fee that Pushpay’s customers have to pay as long as they need Pushpay’s software. We believe that as church communities start to rely on digital engagement, Pushpay’s platform will become an increasingly mission-critical component of churches’ day-to-day operations. As for processing revenue, we think that the church donations made through Pushpay’s app recurs simply due to repeat user behaviour.

Lending weight to our view on the recurring nature of Pushpay’s revenue are two things that we shared earlier: (1) the strong growth in the company’s customer count over the years, and (2) the company’s annual revenue retention rate of more than 100% in the past few years. The following is an example of how the annual revenue retention rate is calculated. The retention rate for FY2020 is defined as the amount of revenue at the end of FY2020, divided by the amount of revenue from the end of FY2019, for customers who joined Pushpay prior to the end of FY2019. An annual revenue retention rate of more than 100% indicates that all customers who joined Pushpay’s platform before the end of FY2019 generated more revenue for Pushpay in FY2020 in aggregate, even after including lost revenue from customers who leave Pushpay.

5. A proven ability to grow

Pushpay has demonstrated a solid track record of growth. The table below highlights the key financial numbers for the company from FY2015 to FY2020 (we chose FY2015 as the starting point because Pushpay’s prior revenues were not meaningful):

Source: Pushpay annual reports

There are a few things to unpack from Pushpay’s historical financials:

- Revenue has grown in each year and has compounded impressively at an annual rate of 89.4% from FY2016 to FY2020. Growth has slowed in recent years, but was still strong at 40.1% in FY2019 and 31.9% in FY2020.

- Pushpay first went public in 2014 when it was still unprofitable and burning cash. But the company has since turned the picture around. Pushpay generated a profit in FY2019 and FY2020 with decent margins of 19% and 12%, respectively. It also produced positive operating and free cash flow in FY2020, with a respectable free cash flow margin of 17.8%.

- The balance sheet was pristine with zero debt from FY2015 to FY2019. As mentioned earlier, Pushpay’s debt spiked in FY2020 after it took up loans to acquire Church Community Builder. And as we had also discussed, we’re not concerned with Pushpay’s debt because of the company’s cash flow characteristics.

- Pushpay’s diluted share count has increased by 8.5% per year from FY2015 to FY2020. This is higher than what we typically like to see. But we think it’s fine since revenue growth was much stronger over the same period, and dilution has been minimal in the past three years.

In the first half of FY2021, Pushpay continued to produce excellent results. Revenue was up 51.1% from a year ago to US$86.5 million, with Church Community Builder contributing to less than half of the growth. In these six months, subscription revenue and processing revenue jumped by 57% and 50% respectively. What’s really impressive is the growth in Pushpay’s profit and free cash flow. Profit doubled to US$13.4 million while free cash flow tripled to US$26.7 million, driven by a tripling too in operating cash flow to US$27.0 million. Pushpay ended the first half of FY2021 with an excellent free cash flow margin of 30.8%.

6. A high likelihood of generating a strong and growing stream of free cash flow in the future

We think Pushpay excels in this criterion. This is because Pushpay is already generating positive free cash flow and has a free cash flow margin which improved from an already respectable 17.8% in FY2020 to 30.8% in the first half of FY2021.

More importantly, there is a high likelihood, in our view, that Pushpay’s revenue can continue to grow at a high double-digit rate in the years ahead, driven by the digital transformation of churches. And because Pushpay has healthy unit economics, any revenue growth can be translated into commensurate or even higher free cash flow growth, since the company is likely to maintain or even improve its free cash flow margin over time.

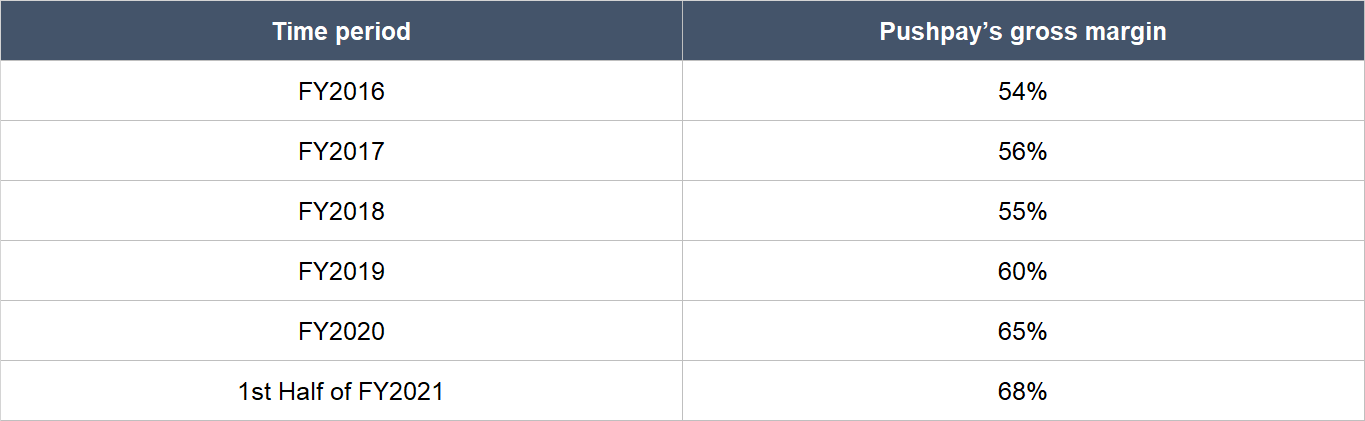

On Pushpay’s unit economics, we can point to two things. First, Pushpay is able to recover its customer acquisition costs (CAC) in a decent amount of time; earlier, we shared that Pushpay’s months to recover CAC has never exceeded 20.2 months since FY2015. Second, Pushpay boasted a solid gross margin of 68% in the first half of FY2021, and the gross margin has improved over time.

Source: Pushpay annual reports and half-yearly earnings updates

Valuation

We like to keep things simple in the valuation process. In Pushpay’s case, we think the price-to-free cash flow (P/FCF) ratio is an appropriate metric to gauge the value of the company. This is because Pushpay has started to produce positive free cash flow and its free cash flow margin in FY2020 is already a respectable 17.8%.

We completed our purchases of Pushpay shares with Compounder Fund’s initial capital in late July 2020. Our average purchase price was A$7.41 per Pushpay share (we bought Pushpay’s Australia-listed shares for Compounder Fund because they are easier to access through the fund’s broker). At our average price and on the day we completed our purchases, the company’s shares had a trailing P/FCF ratio of around 66 based on its financials for FY2020. This ratio looks high optically. But to us, it’s a fair price to pay for a company that we think can comfortably compound its revenue by north of 25% annually over the long run.

For perspective, Pushpay carried a P/FCF ratio of around 35 at the 17 November 2020 stock price of A$7.04. The eagle-eyed among you may realise that Pushpay’s P/FCF ratio had declined significantly from late-July 2020 to 17 November 2020. This happened because of Pushpay’s strong revenue growth and the big jump in the company’s free cash flow margin from 17.8% in FY2020 to 30.8% in the first half of FY2021.

The risks involved

We see four key risks with Pushpay.

Earlier, we discussed the recent flurry of leadership changes at the company. This is an important risk because instability at the helm of Pushpay could derail its growth. We’re watching how the situation unfolds. We’re currently comforted by the quality of Pushpay’s product portfolio and the presence of Shane Sampson as CFO and Steve Basen as Chief Growth Officer.

Another risk we’re watching concerns Pushpay’s execution. Our investment thesis is built on our belief that in the years ahead, Pushpay can continue to win more medium to large churches as customers and increase the volume of donation-payments processed on its platform. Over the past few years, Pushpay has excelled on both fronts. But Pushpay appears to have run into a speed bump recently with customer-acquisition – the company’s number of medium to large customers fell from 6,418 at the end of FY2020 to 6,220 at the end of the first half of FY2021. One data point does not make a trend so we’re not worried. But we’re keeping an eye on things here.

There is also the risk of a shrinking total addressable market. Pushpay’s penetration rate is still low, so we’re confident that there’s ample room for the company to grow. But data from the Pew Research Centre shows that Christianity is on the decline in the USA. The number of Americans who identify with the Christianity faith has fallen from 74% in 2009 to 63% today. If this trend accelerates, Pushpay may face an uphill struggle to grow.

Lastly, the risk of competition is something we are looking at too. There are many companies, such as Tithely, that offer churches an alternative to Pushpay to digitally manage donations and their congregations. Pushpay has so far held its own admirably, given its strong track record of growth. But there’s no guarantee that Pushpay can continue winning.

Summary and allocation commentary

To summarise, Pushpay:

- Has an addressable market of more than US$1 billion that is significantly higher than the company’s current revenue

- Has a high chance of achieving deep penetration in its market

- is in a net debt position that looks highly manageable, given our belief that the company has attractive free cash flow characteristics

- has an innovative leadership team that is reasonably compensated

- has a business model that generates recurring revenue streams through subscriptions and repeat use from customers (referring to the processing of payments)

- has an excellent multi-year track record of revenue growth

- has started generating positive free cash flow with an impressive free cash flow margin, and the company is likely to continue doing so

There are risks. The important ones to note include recent leadership changes; a recent decline in the number of customers for Pushpay’s core customer segment of medium to large churches; the possibility of a shrinking market opportunity given the decline in Christianity in the USA; and lastly, the presence of fierce competition in Pushpay’s business.

After weighing the pros and cons, we thought a 2.5% position in Pushpay for Compounder Fund – a medium-sized allocation – is appropriate. We appreciate all the positives that we see in Pushpay. But when we first invested in the company, its co-founders had recently stepped away. And although Pushpay’s market opportunity is much larger than the current scale of its business, US$1 billion is not exactly a massive addressable market. So we did not think it made sense to have Pushpay to be a large position in the portfolio.

And here’s an important disclaimer: None of the information or analysis presented is intended to form the basis for any offer or recommendation; they are merely our thoughts that we want to share. Of all the companies mentioned in this article, Compounder Fund also currently owns shares in Amazon.com. Holdings are subject to change at any time.