Compounder Fund: Portfolio Update (October 2024) - 09 Oct 2024

Jeremy and I intend to share frequent but non-scheduled updates on how Compounder Fund’s portfolio looks like. The last time we shared an update on this was for the fund’s portfolio as of 19 August 2024. In the update, I shared that we had trimmed the fund’s holdings in Costco, Intuitive Surgical, and Starbucks to add to Amazon and Meta Platforms. I also mentioned that some of the cash from the trimming was also used to establish a new position in Cassava Sciences; our thesis can be found here. Since then, there have been no changes to the list of Compounder Fund’s holdings. We’ve also made only tiny tweaks to the portfolio since, with the most notable changes being a trimming of the fund’s MongoDB position, and additions to Alphabet, Amazon, and Visa.

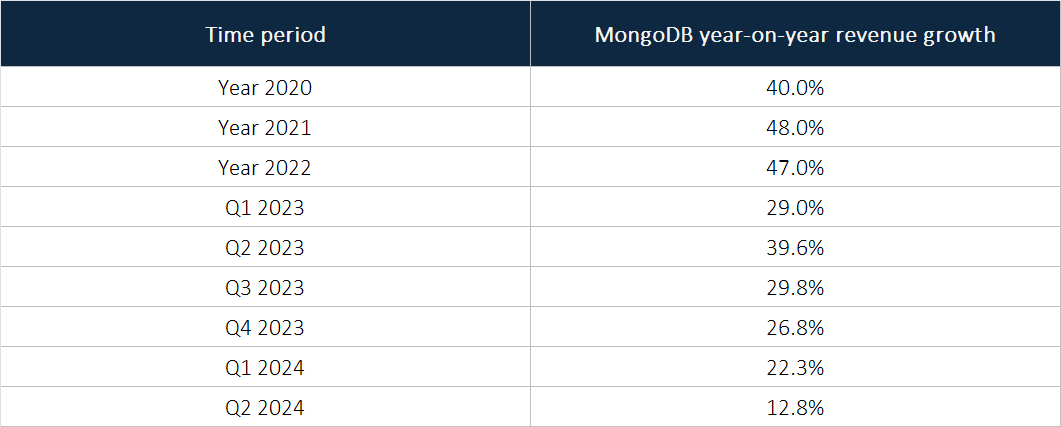

MongoDB, which provides subscriptions to its document-based, non-relational database platform, has seen its revenue growth decelerate significantly in the past few quarters, as Table 1 illustrates. Moreover, management’s latest guidance for the company’s revenue growth in 2024 is just 14.3%. We think there’s a good chance MongoDB’s revenue growth can reaccelerate in the future for two reasons:

- In the first half of 2024, MongoDB experienced lower than expected growth in consumption of Atlas, its multi-cloud hosted database-as-a-service platform, which management believed was because of a weak macroeconomic environment. During the company’s 2024 first-quarter earnings call, management commented (emphases are mine):

“We’re a database or a data platform and the usage of our platform is directly or very tightly correlated to the performance of the end customer’s business. If they’re selling 100 widgets a week and all of a sudden, now they’re selling 80 widgets a week that will mean that they’re using the database less intensely. So when we see broad-based slowdown across different customer cohorts, of different sizes across different industries and across different geos, that strikes us as pretty much a macro issue. And so that’s why based on — and we have close to 50,000 customers. So we have a pretty good feel for what’s happening right now, and that’s why we feel that there’s definitely a macro element to it.”

If the macro environment improves for MongoDB, that could lead to an uptick in its future growth rates.

- Although there is currently significant spending related to artificial intelligence (AI), most of it is at the infrastructure layer, with companies still largely experimenting with AI applications. MongoDB’s database is predominantly exposed to the application layer, so a prerequisite for the company to benefit from an AI-tailwind is if AI applications become more widespread, which would drive growth in inferencing workloads. If AI applications do grow, we think MongoDB has a good chance of riding on this tailwind. AI workloads tend to involve a wide variety of data types and this is where MongoDB’s document-based database excels. Management shared during the 2024 second-quarter earnings call (emphasis are mine):

“More than any other type of modern workload, AI-driven workloads require the underlying database to be capable of processing queries against rich and complex data structures quickly and efficiently. Our flexible document model is uniquely positioned to help customers build sophisticated AI applications because it is designed to handle different data types, your source data, vector data, metadata and generated data right alongside your live operational data, outdating the need for multiple database systems and complex back-end architectures.”

But we still decided to lighten Compounder Fund’s position in MongoDB because of the aforementioned relatively poor revenue-growth rates in recent quarters, and the company’s high valuation. At the end of September 2024, MongoDB carried price-to-sales (P/S) and price-to-free cash flow (P/FCF) ratios of 11 and 133, respectively.

Table 1; Source: MongoDB quarterly earnings updates

With its stock price down by 9% in the third quarter of 2024, we thought internet search giant Alphabet was a good candidate to add to. Market participants have concerns over the long-term health of Alphabet’s core business, Google Search; they worry that users could ditch Google Search in droves for AI chatbots such as ChatGPT and Perplexity when finding information online. This is a risk we’re watching but we find that Alphabet also has its strengths:

- The company’s balance sheet is a fortress, with US$110.9 billion in cash and short-term investments, and just US$25.7 billion in total debt and operating lease liabilities, as of 30 June 2024. Moreover, it’s still producing prodigious amounts of cash; Alphabet’s free cash flow in the trailing 12 months was US$60.5 billion, while the average free cash flow for 2021, 2022, and 2023, was US$62.1 billion. Alphabet’s strong balance sheet and robust free cash flows provide it with the financial resources to experiment and adapt.

- We think that Alphabet has a really strong team in AI, with luminary leaders such as Jeffrey Dean and Demis Hassabis. It was research from Alphabet, in the form of the famous 2017 paper Attention Is All You Need, that provided the intellectual foundation for the popular AI products of today, such as ChatGPT from OpenAI. Alphabet’s latest foundation model, Gemini 1.5, which was released in February this year, has a context window of up to 1 million tokens. This was (and still is today) the largest context window among foundation AI models; the context window measures the number of tokens a model can process at once. We think Alphabet has the intellectual resources to compete well in AI.

- Alphabet has six products with more than two billion monthly users each; this is a massive distribution advantage that the company has for any AI features it has developed.

- A Google Search product that is integrated with AI could look materially different from what it is today. The good thing is that Alphabet has navigated major technology shifts in the past, such as the shift towards mobile devices. The early results of Alphabet’s experiments with integrating AI into Google Search are also promising; here are some of management’s recent comments (emphases are mine):

“[From the 2024 first-quarter earnings conference call] A number of technical breakthroughs are enhancing machine speed and efficiency, including the new family of Gemini models and a new generation of TPUs [tensor processing units]. For example, since introducing SGE [ Search Generative Experience] about a year ago, machine costs associated with SGE responses have decreased 80% from when first introduced in Labs driven by hardware, engineering, and technical breakthroughs.

[From the 2024 second-quarter earnings conference call] With AI, we are delivering better responses on more types of search queries and introducing new ways to search. We are pleased to see the positive trends from our testing continue as we roll out AI Overviews, including increases in Search usage and increased user satisfaction with the results. People who are looking for help with complex topics are engaging more and keep coming back for AI Overviews. And we see even higher engagement from younger users aged 18 to 24 when they use Search with AI Overviews.”

At the end of September 2024, Alphabet carried price-to-earnings (P/E) and P/FCF ratios of 24 and 34, respectively. We think these valuations are undemanding for a company that (1) currently still has a commanding share of around 90% of the online search market, and (2) has its strengths when dealing with the threat its core business is facing from competing AI technologies.

Coming to Amazon, we last increased Compounder Fund’s position in the company just two months ago in August. We shared our reasons for doing so – which also apply for the most recent addition – in the aforementioned update published on 20 August 2024:

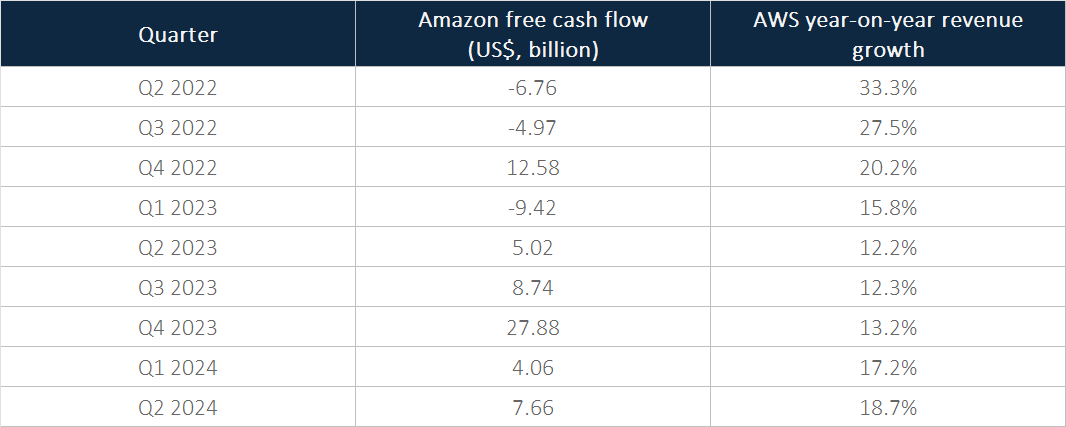

“In the case of Amazon, the e-commerce and cloud computing juggernaut, its free cash flow has surged in recent quarters while the year-on-year revenue rates at AWS, its cloud-computing arm, has accelerated, as shown in [Table 2].

[Table 2]; Source: Amazon quarterly earnings updatesAt the time of our addition, Amazon was trading at a P/FCF ratio of 36 [Amazon ended September 2024 with a P/FCF ratio of 41]. We see continued healthy revenue growth at the company in the coming years, driven by the massive tailwinds present in the e-commerce and cloud computing markets, and a clear path toward higher FCF margins. On margins, management has commented in the past few earnings conference calls that there’s room to continue growing Amazon’s operating margins in the e-commerce business, which would flow through to its overall free cash flow margin. On the tailwinds, e-commerce was still just 15.9% of total retail sales in the USA in the first quarter of 2024 while around 90% of global IT (information technology) spending today is still for on-premise technologies. The latter suggests significant room for further migration of IT spending towards the cloud. Moreover, if and when AI applications become ubiquitous, Amazon’s CEO Andy Jassy thinks that these applications will be built on the cloud from the start. AWS is likely to be a major beneficiary of these trends in our view. In the first quarter of 2024, AWS saw more absolute-dollar sequential growth in revenue than any other cloud provider and during the second-quarter earnings conference call, Jassy revealed that AWS is innovating in AI at a rapid pace:

“During the past 18 months, AWS has launched more than twice as many machine learning and generative AI features into general availability than all the other major cloud providers combined.””

As for Visa, which operates a global payments network, it ended September with P/E and P/FCF ratios of 29-30. These valuations are nowhere near their five-year highs of over 50 each and they look fair for a company we think can continue to compound free cash flow at a high-teens to low-20s annual percentage rate over the next five to 10 years. For perspective, Visa’s management thinks there’s a US$200 trillion market opportunity in new flows, which is multiples of the total volume of US$15.5 trillion that the company processed in the 12 months ended 30 June 2024; new flows are where Visa facilitates commercial and global money movement.

Visa’s attractive valuations are partly the result of a dip in the company’s stock price that happened in late-September after it was sued by the US’s Justice Department for anticompetitive business practices in the US debit-card market. We have no special insight on how the lawsuit will eventually play out (and it’s worth noting that the legal battle is likely to take many years to resolve), but we can recognise Visa’s strong competitive position today. The company currently has the largest payments network in the world (in terms of transaction volume) with a market share of around 39%. We believe this gives Visa a dominant network effect that is incredibly hard to break, so the trajectory of its future long-term business growth continues to look healthy to us regardless of the outcome of the lawsuit, barring the highly unlikely result of Visa’s network being significantly neutered.

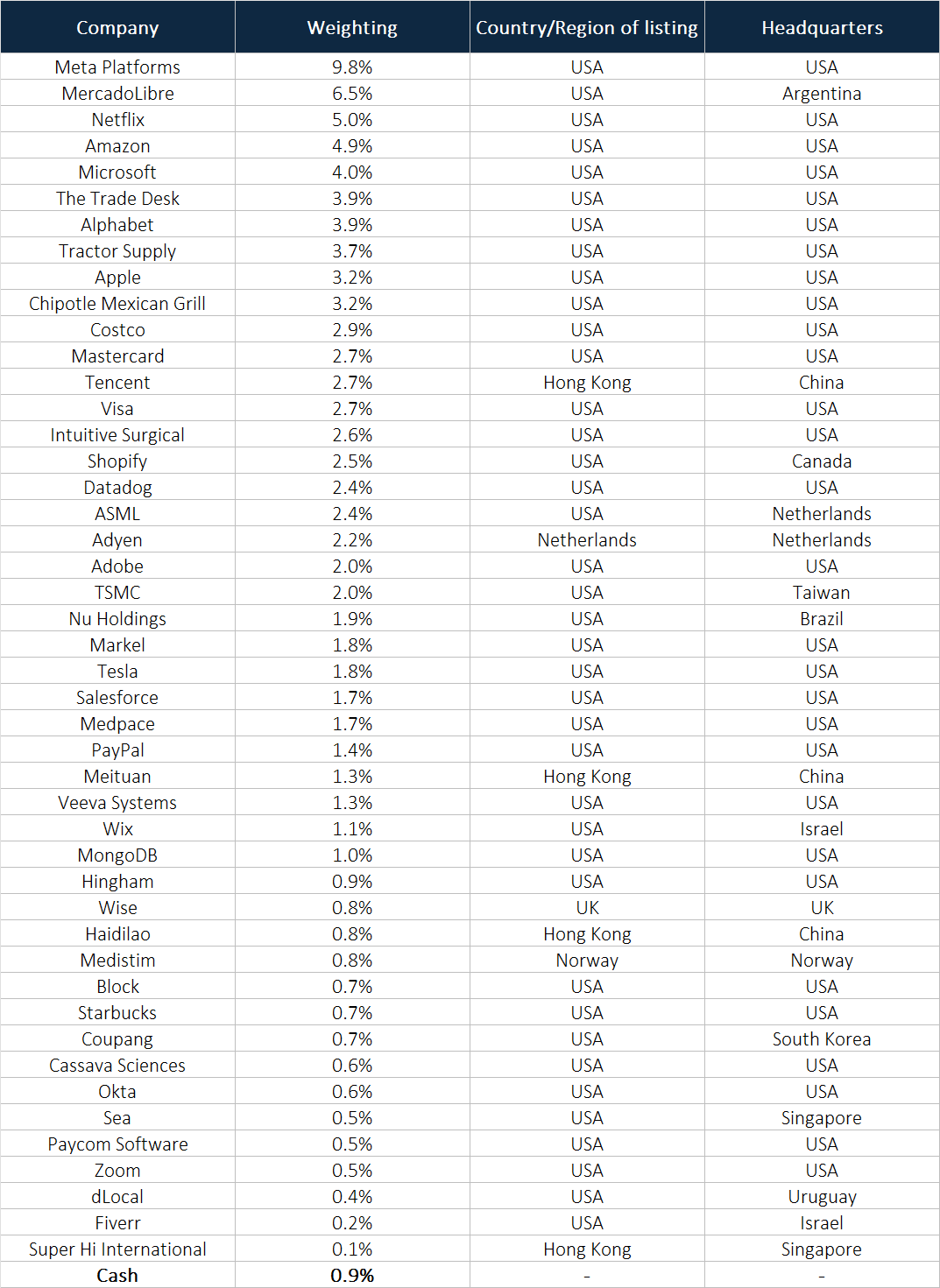

Here’s how Compounder Fund’s portfolio looks like as of 7 October 2024:

Table 3

And here’s an important disclaimer: None of the information or analysis presented is intended to form the basis for any offer or recommendation; they are merely our thoughts that we want to share. Holdings are subject to change at any time.