Compounder Fund: Portfolio Update (October 2022) - 12 Oct 2022

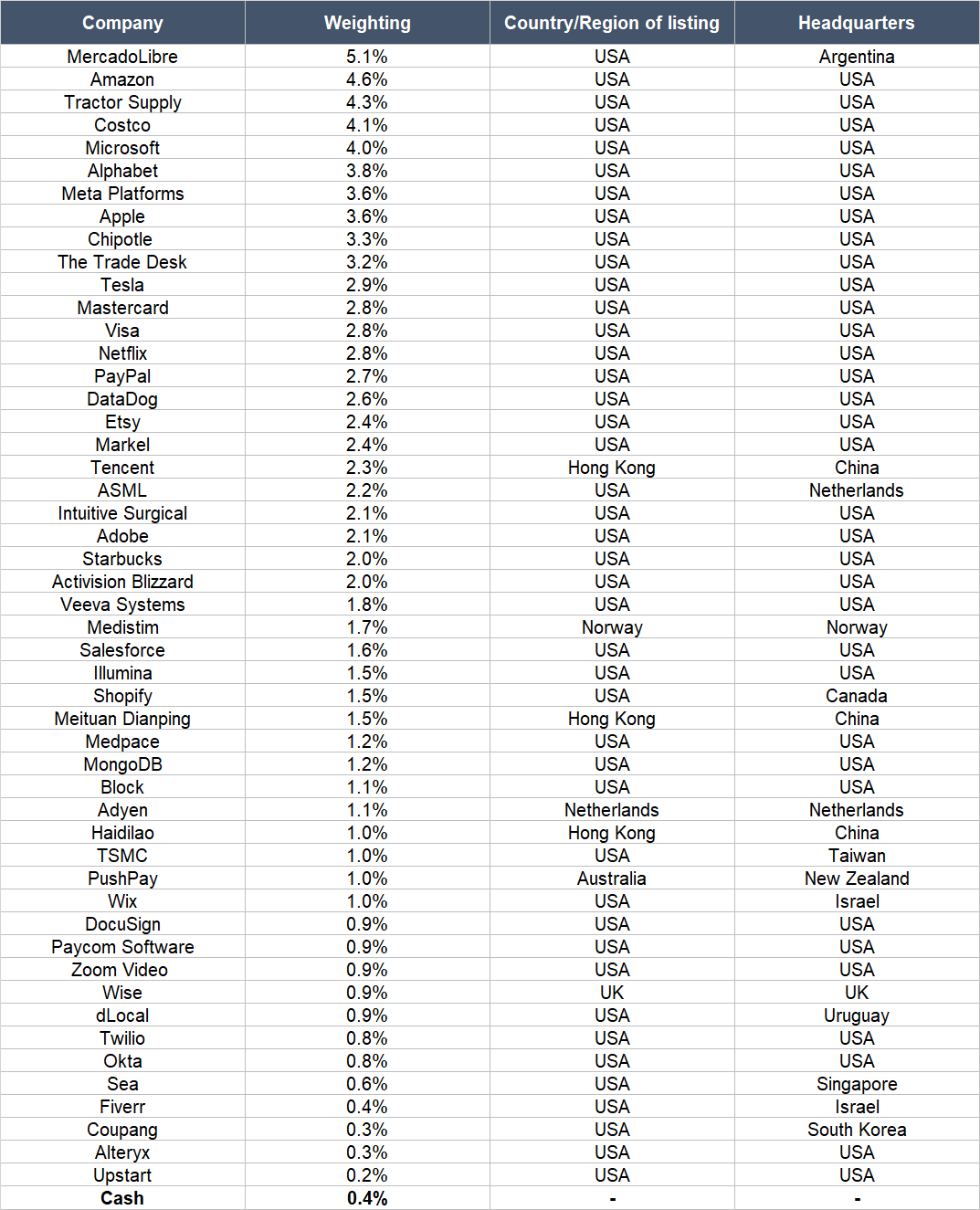

Jeremy and I intend to share frequent but non-scheduled updates on how Compounder Fund’s portfolio looks like. On 31 August 2022, I published an update on Compounder Fund’s portfolio on the fund’s website. In the update, I mentioned a few things: (a) all 50 holdings in the fund’s portfolio; (b) our full sale of Teladoc shares from the fund; (c) the partial sale of the fund’s stakes in Tencent and Sea; and (d) an investment in a new company, namely, Medpace. As of the date of this update, the portfolio contains the same 50 holdings although some involuntary removals could happen in the near future.

First, there’s the acquisition of Activision Blizzard by Microsoft that I discussed in previous updates (see here and here). In September, Activision’s CEO, Bobby Kotick, gave an update on the deal. A number of countries have already approved the transaction and the regulatory process is proceeding as the management teams of both Activision and Microsoft have expected. There’s no change in the time-line for the acquisition and it is still expected to close before 30 June 2023. As previously discussed, Jeremy and I intend for the fund to hold onto its Activision shares and receive the cash from Microsoft if and once the acquisition is completed (but our intention could change depending on developments at both companies and the stock market in general).

Next, there’s the privatisation of Pushpay that I first mentioned in a previous update. Last month, there was speculation in the media that the privatisation may fall through; Pushpay acknowledged the existence of the media speculation in an official announcement but gave no update on the progress of its discussions with the potential buyers. Then earlier this week, there was new speculation that Pushpay had received a revised non-binding buyout offer from one of its existing shareholders. The shareholder, BGH Capital, was among the third parties that first broached the acquisition of Pushpay in late-May. This time, Pushpay acknowledged that it had indeed received an “indicative non-binding proposal” but no price, nor timing for any potential transaction, was mentioned. Our stance with Pushpay remains the same as what I previously communicated:

“Jeremy and I think Pushpay’s long-term growth prospects are healthy and we intend for Compounder Fund to hold onto its Pushpay shares for now (our intention is, again, subject to change depending on developments at the company and stock market in general). We’ll make new decisions as and when Pushpay releases information about the offers.”

Compounder Fund is able to accept new subscriptions once every quarter with a dealing date that falls on the first business day of each calendar quarter. In the middle of September 2022, Jeremy and I successfully closed Compounder Fund’s eighth subscription window since its initial offering period (which ended on 13 July 2020). This new capital was deployed quickly in the days after the last subscription window’s dealing date of 3 October 2022. Jeremy and I invested the new capital in four existing Compounder Fund holdings. They are (in alphabetical order): Adobe, Alphabet, Mastercard, and Visa.

In Compounder Fund’s Owner’s Manual, we mentioned that “if Compounder Fund receives new capital from investors, our preference when deploying the capital is to add to our winners and/or invest in new ideas.” Not all of the four existing holdings in the portfolio that we added capital to have seen their stock prices rise strongly after we initially invested in them. But all of them have executed well since our investments and they’ve produced solid business results. They are winners, according to our definition. Here’s how Compounder Fund’s portfolio looks like as of 9 October 2022:

Table 1

*0.3% of the Block position comes from Block shares that are listed in Australia, but for all intents and purposes, we see the Australia-listed Block shares as being identical to the US-listed variety

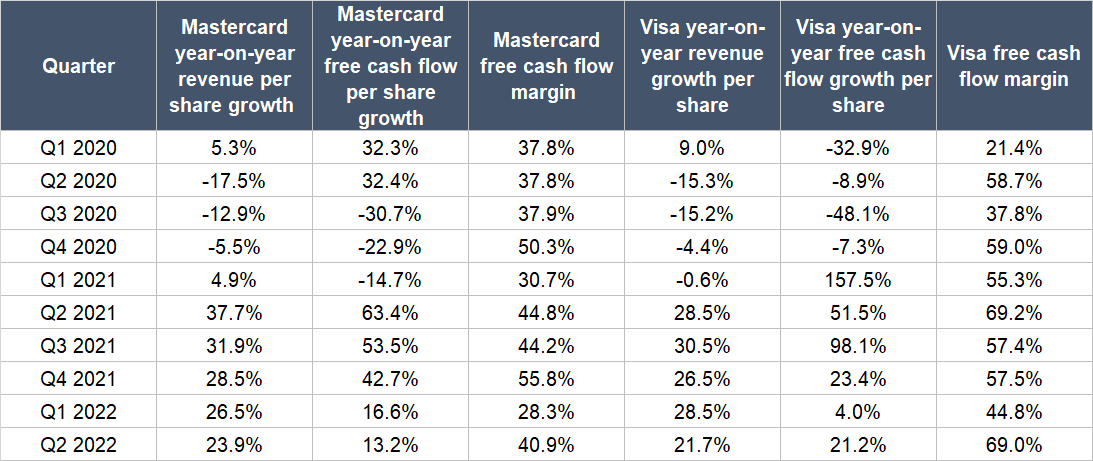

Our biggest additions in early-October 2022 were in Mastercard and Visa (we invested similar amounts in both companies). The two payment networks have demonstrated strong and consistent business growth since 2021 (both companies were affected in 2020 because of COVID-19), as Table 2 below illustrates. In “The risks involved” sections of our investment theses for both companies (see here and here), we highlighted the intense competition they face as one of the key risks we’re watching. But since our initial investments in Mastercard and Visa in mid-July 2020, both companies have been fortifying their positions as key players in the digital payments ecosystem. Some examples:

- In the year-to-date alone, Mastercard has inked more than 20 crypto-card deals, where consumers who hold cryptocurrencies are able to spend with fiat currencies with Mastercard-powered cards. Similarly, Visa’s management mentioned in a June 2022 investor conference that the company was working with around 70 organisations in the crypto ecosystem that are in various stages of issuing crypto-cards to allow consumers to spend their cryptocurrencies in the form of fiat money. In our view, these developments lower the risk that Mastercard and Visa’s payment networks would be disrupted in the future if cryptocurrencies become more widely adopted by consumers.

- Fintechs (financial technology companies) have also been partnering with Mastercard and Visa for their own digital payment services. For example, Mastercard struck up more than 250 payments-related partnerships with fintechs in 2021. In another instance, Apple’s buy-now-pay-later (BNPL) service, Apple Pay Later, which was announced this June, is powered by Mastercard. Over at Visa, fintechs issuing Visa cards grew by 30% in the fiscal year ended 30 September 2021 while payment volumes from fintechs nearly doubled. Visa also reported more than 100 fintech partnerships in Europe alone, as of July this year. Fintechs have the potential to build their own payment rails and thus disrupt Mastercard and Visa. But the burgeoning of partnerships that Mastercard and Visa have with fintechs lowers this risk, in our opinion.

Table 2

Source: Company filings

There are two other key factors that influenced our decision to add to Mastercard and Visa:

- Both companies have experienced robust growth in their businesses over the past decade (see our investment theses for more details), when inflation was mostly low in the USA and other parts of the world. One of the big risks confronting the global economy today is inflation remaining high for a prolonged period of time. If this risk does manifest, both Mastercard and Visa could stand to benefit. During Visa’s 2022 first-quarter earnings conference call, management said that inflation has historically been a net-positive for the company.

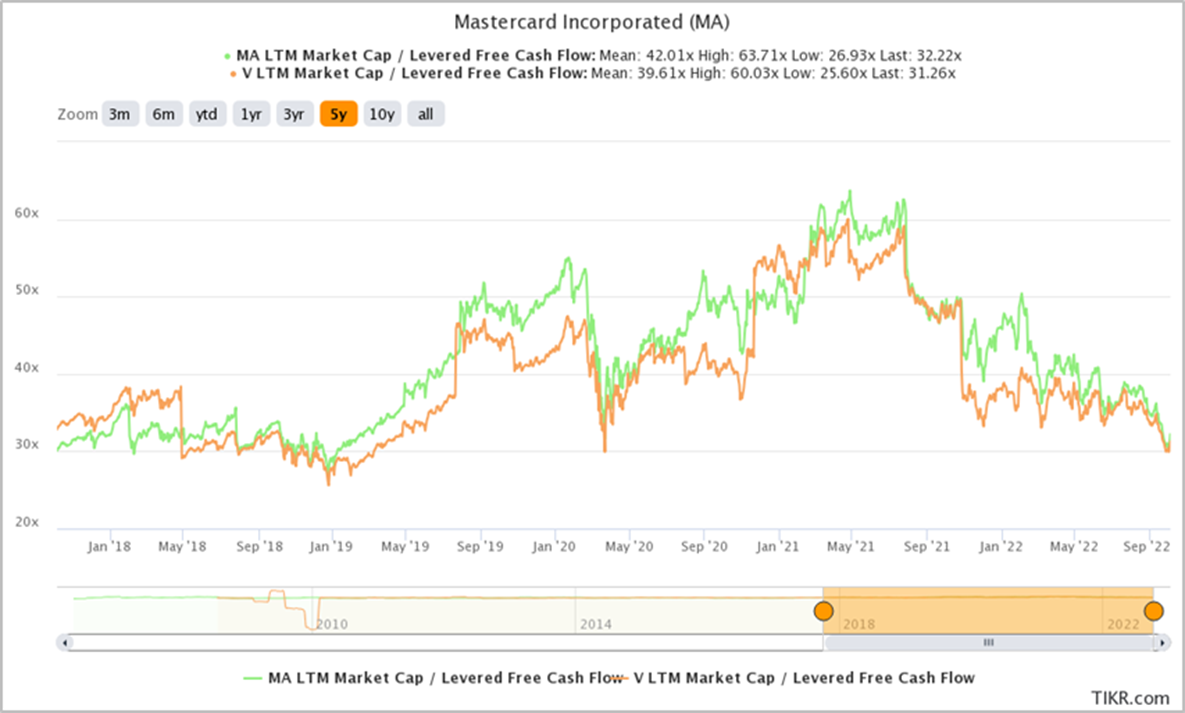

- The two payment networks have price-to-free cash flow (P/FCF) ratios that are near five-year lows, as illustrated in Figure 1. As of 30 September 2022, Mastercard and Visa have P/FCF ratios of 31 and 24, respectively.

Figure 1 (Green is for Mastercard; Orange is for Visa)

Source: Tikr

We’re sharing all this information with the public and with the fund’s investors for two reasons. First, we believe deeply in investor education and want Compounder Fund’s return and actions to be a source for people to learn about investing. Second, we believe that this transparency will help investors of Compounder Fund develop comfort with our investing process over time, which is great; in turn, this will also free us from the time-consuming activity of dealing with questions on how we invest, and thus give us more to invest better for our investors.

And here’s an important disclaimer: None of the information or analysis presented is intended to form the basis for any offer or recommendation; they are merely our thoughts that we want to share. Holdings are subject to change at any time.