Compounder Fund: Portfolio Update (July 2021) - 12 Jul 2021

Jeremy and I intend to share frequent but non-scheduled updates on how Compounder Fund’s portfolio looks like. The last time we shared an update on this was for Compounder Fund’s portfolio in mid-April 2021.

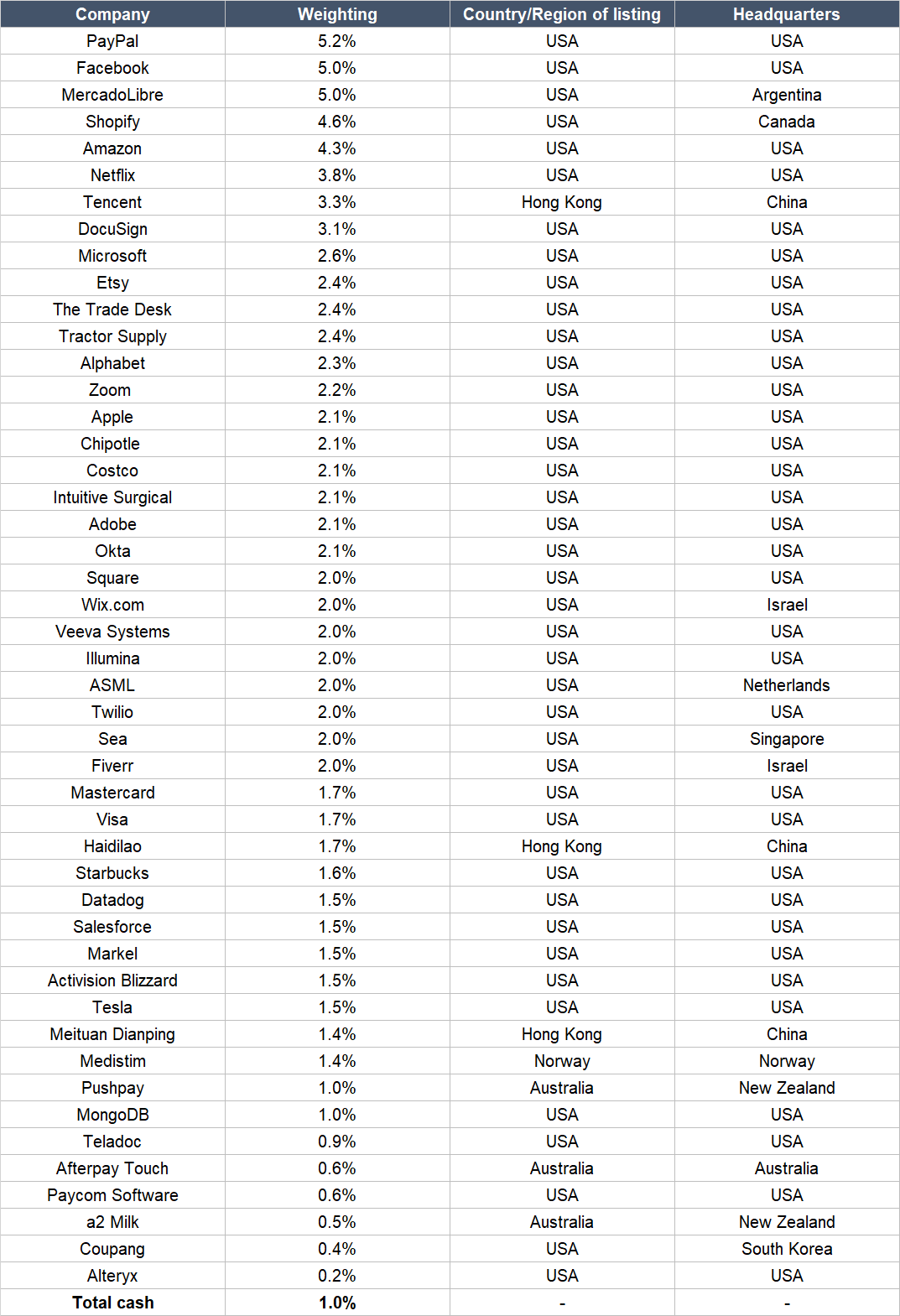

In it, I shared all 47 holdings in the fund’s portfolio. As of the date of this update, the portfolio contains the same 47 holdings, and there are no new stocks added.

As you know, Compounder Fund is able to accept new subscriptions once every quarter with a dealing date that falls on the first business day of each calendar quarter. In the middle of June 2021, Jeremy and I successfully closed Compounder Fund’s fourth subscription window since its initial offering period (which ended on 13 July 2020).

This new capital was deployed quickly in the days after the last subscription window’s dealing date of 1 July 2021. Jeremy and I invested the new capital across 30 of Compounder Fund’s existing holdings. They are (in alphabetical order): Activision Blizzard, Adobe, Alphabet, Amazon, Apple, ASML, Chipotle Mexican Grill, Costco, Datadog, DocuSign, Etsy, Facebook, Fiverr, Illumina, Intuitive Surgical, Mastercard, MercadoLibre, Netflix, Okta, PayPal, Sea, Shopify, Starbucks, Tencent, Tesla, Twilio, Veeva Systems, Visa, Wix, and Zoom.

As of this letter’s publication, we have released our investment theses on all 47 companies that are currently in Compounder Fund’s portfolio and they can be found here. In the future, if and when we add new companies to the portfolio or completely exit any of the 47 companies, we will be publishing our theses for these actions.

In Compounder Fund’s Owner’s Manual, we mentioned that “if Compounder Fund receives new capital from investors, our preference when deploying the capital is to add to our winners and/or invest in new ideas.” Not all of the 30 existing holdings in Compounder Fund’s portfolio that we added capital to have seen their stock prices rise strongly after we initially invested in them. But all of them have executed brilliantly in recent times and produced wonderful results (the only exceptions were Mastercard and Visa, where revenue growth in their last reported quarters were low and negative, respectively). They are winners, according to our definition. Here’s how Compounder Fund’s portfolio looks like as of 10 July 2021:

Our biggest addition was to Shopify. In our investment thesis for Shopify, we had an in-depth discussion on our admiration for the company’s CEO and co-founder, Tobi Lütke. As part of our discussion, we shared a number of passages from Lütke’s powerhouse of an investors’ letter that he wrote for the company’s 2015 IPO prospectus. We want to bring up one passage that we also mentioned in our investment thesis (emphasis is ours):

“Over the years we’ve also helped foster a large ecosystem that has grown up around Shopify. App developers, design agencies, and theme designers have built businesses of their own by creating value for merchants on the Shopify platform. Instead of stifling this enthusiastic pool of talent and carving out the profits for ourselves, we’ve made a point of supporting our partners and aligning their interests with our own. In order to build long-term value, we decided to forgo short-term revenue opportunities and nurture the people who were putting their trust in Shopify. As a result, today there are thousands of partners that have built businesses around Shopify by creating custom apps, custom themes, or any number of other services for Shopify merchants.”

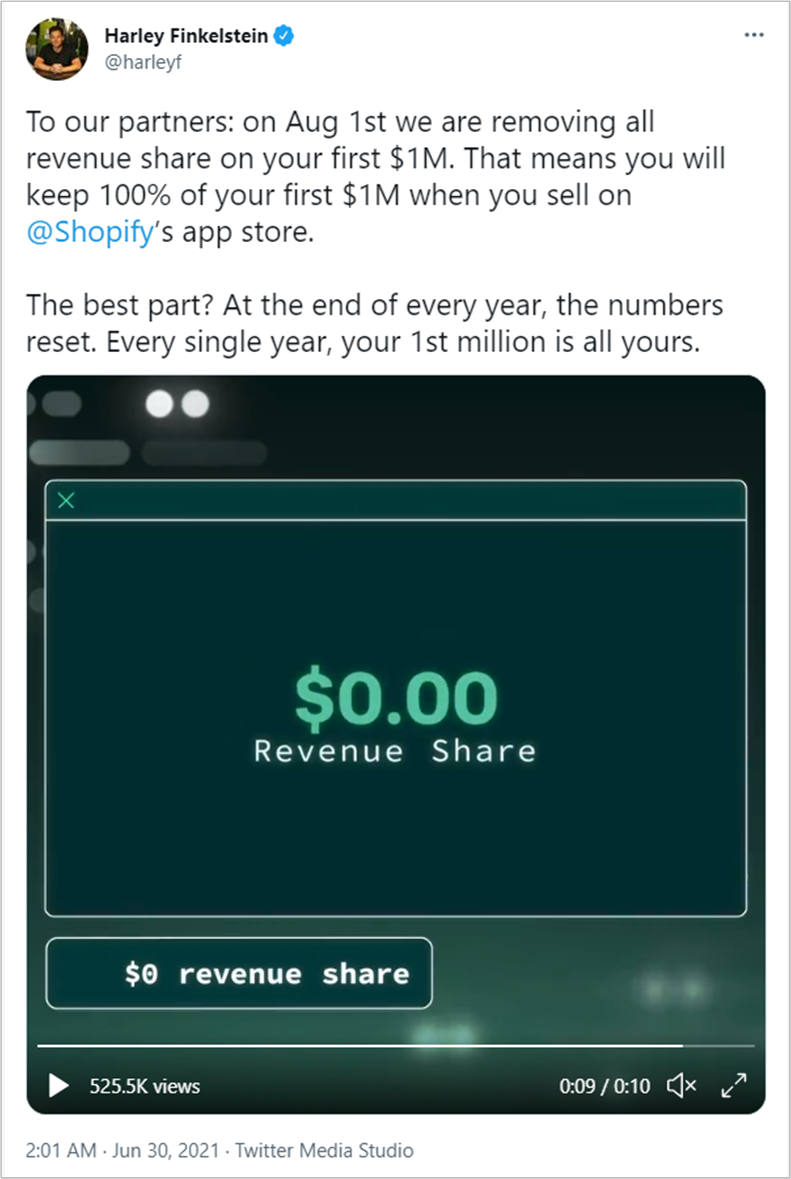

Jeremy and I believe that Lütke’s deep belief in patiently building value, even at the expense of Shopify’s short-term gains, was a massive reason for the company’s past growth. We also think that Lütke’s belief will continue to drive the company’s future growth. In late-June this year, Shopify’s president Harley Finkelstein made the tweet below that significantly reinforced our confidence in Lütke’s willingness to continue patiently building value at Shopify.

The “partners” that Finkelstein referred to are the app developers who develop and sell apps on the Shopify App Store to merchants who use Shopify’s platform. These apps help Shopify’s merchants improve their business operations and grow their businesses. By completely removing revenue-share for the first US$1 million that app developers make on the Shopify App Store, Shopify will be foregoing some revenue over the short-term. But we believe that the long-term value that would be created for Shopify would be huge multiples of whatever short-term revenue-hit the company is going to suffer. Shopify’s move makes it even more attractive for app developers to build for Shopify’s platform compared to the past. This, in turn, is likely to result in even better tools for Shopify’s merchants to grow their businesses, and thus benefit Shopify in the long run. Shopify’s latest move is another wonderful example of a company with a leader who has a unique way of looking at the world. This unique worldview is important to us. In Compounder Fund’s 2020 fourth-quarter investors’ letter, I wrote:

“There’s an interesting angle to our analytical edge that I want to discuss. Jeremy and I are constantly seeking out management teams that have a unique way of looking at the world – this is part of how we assess a management team’s ability to innovate. Having a unique worldview is important to us because it means that a company’s management team is likely to hold an analytical edge over competitors. And crucially, we think this edge is resistant to erosion by market forces.”

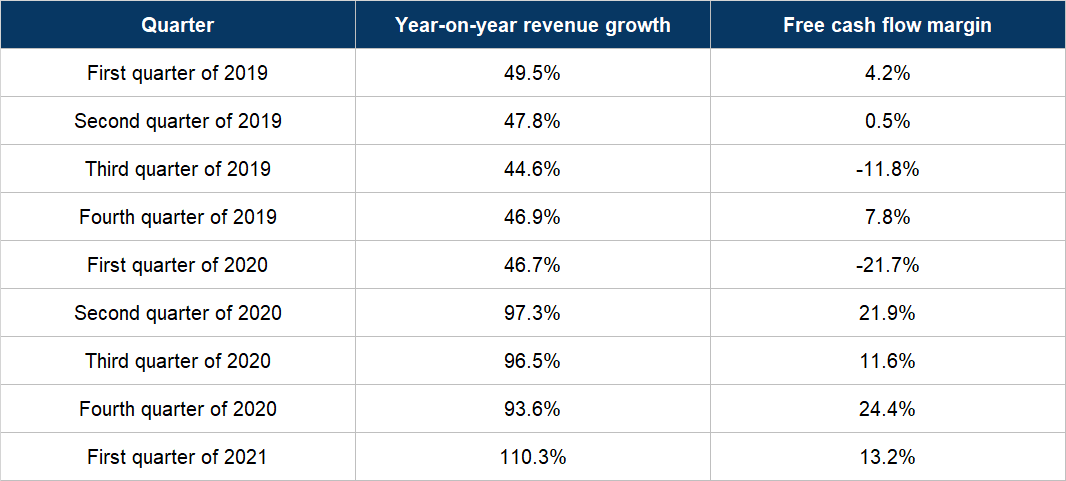

We were also comfortable to add to Shopify because (1) its recent revenue growth rates continue to astound us, and (2) its cash flow picture is improving. The table below shows Shopify’s quarterly revenue growth and free cash flow margin (free cash flow as a percentage of revenue) going back to the first quarter of 2019.

Source: Shopify earnings updates

In December 2020, Lütke was interviewed by Sriram Krishnan for the latter’s The Observer Effect website. We came across the excellent interview recently and it gave us even deeper insights into the way Lütke has built and currently runs Shopify. There was one answer Lütke gave during the interview, shown below, that was particularly striking to us:

“[Laughs] So, going back a little bit further there—you know what, I should talk about books. One thing that is interesting is how people have accused Shopify of being a book club thinly veiled as a public company.

We tend to read a lot and talk about a lot of books. We read Nassim Taleb’s books and one person on my team began talking about Antifragile and gave an outline. He said, “I think Nassim is putting a word to the thing that you keep talking about…”

Now, I come from an engineering perspective. One of my biggest beefs with engineers, in general, is that they love determinism. I think there’s very little determinism in engineering left that’s of value. An individual computer is deterministic; once you introduce even just a network connection into the mix, everything becomes unpredictable and you have to write code that’s resilient to the unknown. Most interesting things come from non-deterministic behaviors. People have a love for the predictable, but there is value in being able to build systems that can absorb whatever is being thrown at them and still have good outcomes.

So, I love Antifragile, and I make everyone read it. It finally put a name to an important concept that we practiced. Before this, I would just log in and shut down various servers to teach the team what’s now called chaos engineering.

But we’ve done this for a long, long time. We’ve designed Shopify very well because resilience and uptime are so important for building trust. These lessons were there in the building of our architecture. And then I had to take over as CEO.

When that happened, I made two decisions: one, I’m going to try to learn as much about business as possible. But, if business is very different from software architecture, I’m going to be no good no matter what I do. And so, I ran an experiment to treat engineering principles, software architecture, complex system design, and company building as the same thing. Effectively, we looked for the business equivalent of just turning off servers to see if the system has resiliency. For instance, we used to ask people to use their mouse on their non-dominant hand for a day. We introduced these little nudges to ensure that people didn’t become complacent.”

Jeremy and I first came across the concept of antifragility – referring to something that strengthens when exposed to non-lethal stress – from Nassim Nicholas Taleb’s book, Antifragile, which was referenced by Lütke. Antifragility is an important concept for Compounder Fund. Jeremy and I run the fund with the idea that bad things will happen from time to time – to economies, industries, and companies – but we just don’t know how and when. As such, we are keen to own shares in antifragile companies, the ones which can thrive during chaos. This is why the strength of a company’s balance sheet is an important investment criteria for us – having a strong balance sheet increases the chance that a company can survive or even thrive in rough seas. But a company’s antifragility goes beyond its financial numbers. It can also be found in how the company is run. We were delighted to realise that antifragility is a trait that has been built into Shopify for – to borrow Lütke’s words – “a long, long time.” This is another reason why we added to our Shopify position.

We’re sharing all this information with the public and with the fund’s investors for two reasons. First, we believe deeply in investor education and want Compounder Fund’s return and actions to be a source for people to learn about investing. Second, we believe that this transparency will help investors of Compounder Fund develop comfort with our investing process over time, which is great; in turn, this will also free us from the time-consuming activity of dealing with questions on how we invest, and thus give us more to invest better for our investors.

And here’s an important disclaimer: None of the information or analysis presented is intended to form the basis for any offer or recommendation; they are merely our thoughts that we want to share. Holdings are subject to change at any time.