Compounder Fund: Okta Investment Thesis - 06 Sep 2020

Data as of 5 September 2020

Okta (NASDAQ: OKTA) is one of the 40 companies in Compounder Fund’s initial portfolio. This article describes our investment thesis for the company..

Company description

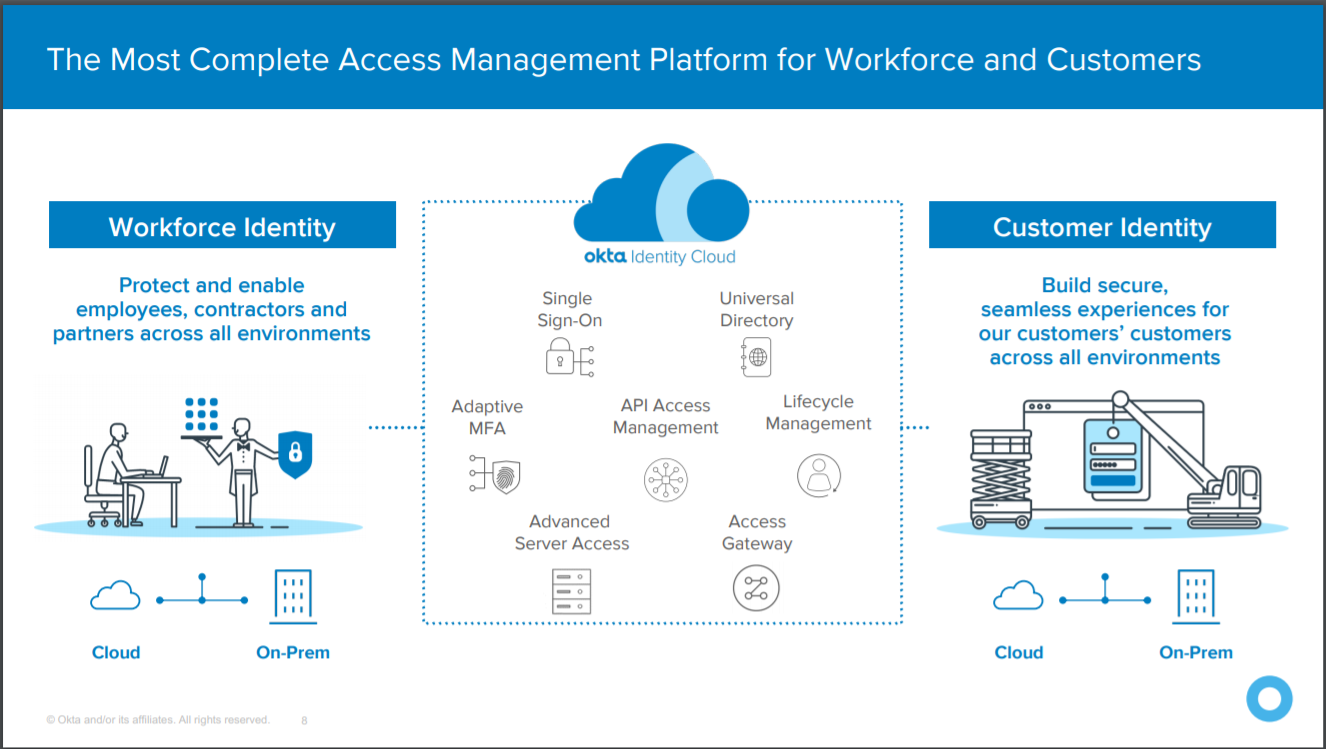

Okta’s vision is to enable any organisation to use any technology. To fulfill its vision, Okta provides the Okta Identity Cloud software platform where all its products live. Okta’s cloud-based software products help other companies manage and secure access to applications for their employees, contractors, partners, and customers.

The internal use-cases, where Okta’s solutions are used by organisations to manage and secure software-access among their employees, contractors, and partners, are referred to as workforce identity by Okta. An example of a workforce identity customer is 20th Century Fox. The external-facing use cases are known as customer identity, and it is where Okta’s solutions are used by its customers to manage and secure the identities and service/product access of their customers. Adobe is one of the many customers of Okta’s customer identity platform.

Source: Okta August 2020 investor presentation

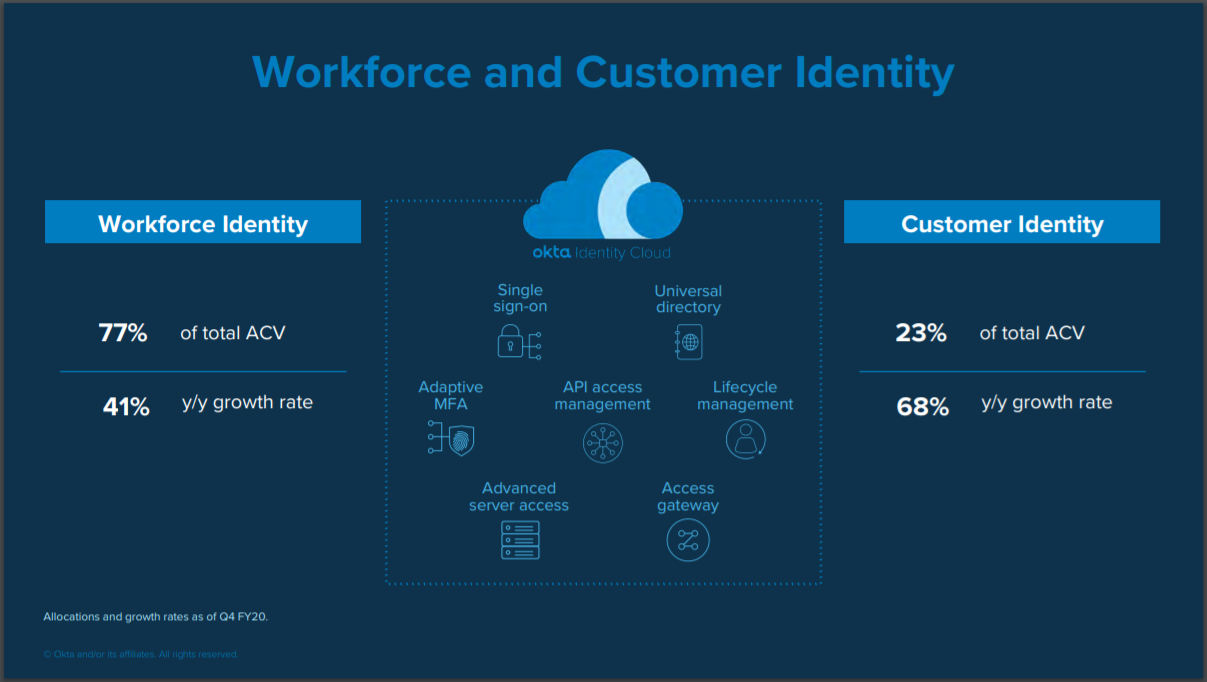

There’s a rough 80:20 split in Okta’s revenue between the workforce identity and customer identity solutions.

Source: Okta April 2020 investor presentation

At the end of FY2020 (fiscal year ended 31 January 2020), Okta had more than 7,950 customers. These customers come from nearly every industry and range from small organisations with less than 100 employees to the largest companies in the world.

For a geographical perspective, Okta sourced 84% of its revenue in FY2020 from the US.

Investment thesis

We have laid out our investment framework in Compounder Fund’s website and will use the framework to describe our investment thesis for Okta.

1. Revenues that are small in relation to a large and/or growing market, or revenues that are large in a fast-growing market

Okta estimates that its market opportunity for workforce identity is U$30 billion today. This is up from US$18 billion around three years ago. The company arrived at its current workforce identity market size of US$30 billion in this way: “50,000 US businesses with more than 250 employees (per 2019 US.Bureau of Labor Statistics) multiplied by 12-month ARR [annual recurring revenue] assuming adoption of all our current products, which implies a market of [US]$15 billion domestically, then multiplied by two to account for international opportunity.”

For customer identity, Okta estimates the addressable market to be US$25 billion. Here’s Okta’s description of the method behind its estimate: “Based on 4.4 billion combined Facebook users and service employees worldwide multiplied by internal application usage and pricing assumptions.” We are taking Okta’s estimate of its customer identity market with a pinch of salt. But we’re still confident that the opportunity is huge, given the growth and size of the entire SaaS (software-as-a-service) market. For perspective, a July 2020 forecast from market research firm Gartner sees global SaaS spending growing by more than 11% annually from US$$102 billion in 2019 to US$141 billion in 2022.

In the 12 months ended 31 July 2020, Okta’s revenue was just US$703.7 million, which barely scratches the surface of its total estimated market opportunity of US$55 billion. We also think it’s likely that Okta’s market is poised for growth. Based on Okta’s studies, the average number of apps that companies are using has increased by 52% from 58 in 2015 to 88 in 2019. In April 2020, Okta’s co-founder and CEO, Todd McKinnon, was interviewed by Ben Thompson for the latter’s excellent tech newsletter, Stratechery. During the interview, McKinnon revealed that large companies (those with over 5,000 employees) typically use thousands of apps. And because of COVID-19 and the resulting work-from-home movement, Okta also mentioned earlier this year that it saw a substantial increase between February and March in the number of apps deployed by companies.

The high and growing level of app-usage among companies means it can be a massive pain for an organisation to manage software-access for its employees, contractors, partners, and customers. This pain-point is what Okta Identity Cloud is trying to address. By using Okta’s software, an organisation does not need to build custom identity management software – software developers from the organisation can thus become more productive. The organisation would also be able to scale more efficiently.

And speaking of COVID-19, Okta’s management believes that the pandemic has accelerated the trends that were already in the company’s favour. We agree. Here’s what management said in Okta’s recent earnings conference calls (for the first and second quarters of FY2021):

“[First quarter of FY2021]

The megatrends of increased adoption of Cloud and hybrid IT, digital transformation and Zero Trust security have been driving our business for the past several years and will continue to drive our business well into the future. In fact, once we emerge from the crisis stage of the pandemic, we expect to see an acceleration of these trends. These trends resonate now more than ever, and our leadership position going into this crisis will be further enhanced as we expand our presence and product offerings.”“[Second quarter of FY2021]

We believe that the world will not return to the pre-COVID work environment. In fact, the three mega-trends that have been driving our business for the past several years, the adoption of cloud and hybrid IT, digital transformation and zero-trust security, are being accelerated by the COVID environment as organizations are rapidly evolving their digital strategy to survive the pandemic while their remote work environments continue to grow. During this crisis, our customers are using Okta’s platform more than ever.”

2. A strong balance sheet with minimal or a reasonable amount of debt

As of 31 July 2020, Okta held US$2.51 billion in cash and short-term investments. This is significantly higher than the company’s total debt of US$1.73 billion (all of which are convertible notes that are due in 2023, 2025, or 2026), and means the company has a robust balance sheet.

For the sake of conservatism, we also note that Okta had US$189.2 million in operating lease liabilities. But the company’s cash and short-term investments still comfortably outweigh the sum of its debt and operating lease liabilities (US$1.92 billion)

3. A management team with integrity, capability, and an innovative mindset

On integrity

Todd McKinnon cofounded Okta in 2009 with Frederic Kerrest. McKinnon, who’s 48 years old, has served as Okta’s CEO since the company’s founding. He has a strong pedigree in leading software companies, having been with salesforce.com from 2003 to 2009, and serving as its Head of Engineering prior to founding Okta. salesforce.com is one of the pioneering software-as-a-service companies, and is also one of the companies in Compounder Fund’s initial portfolio. Kerrest, 43, is Okta’s COO (chief operating officer) and has been in the role since the year of the company’s founding. Kerrest is also a salesforce.com alumni; he joined in 2002 and stayed till 2007, serving as a senior executive. In our view, the young ages of McKinnon and Kerrest, as well as their long tenures with Okta, are positives.

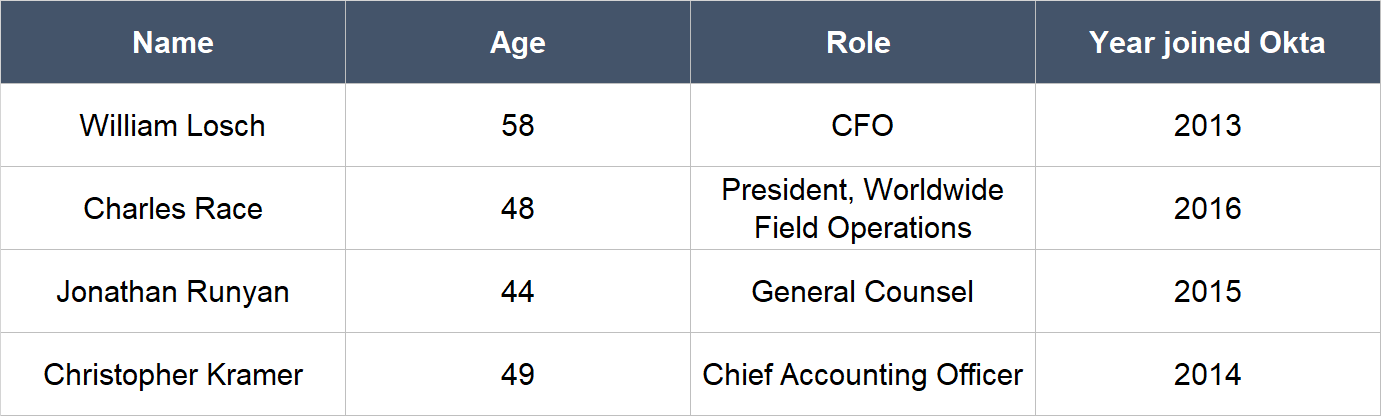

The other important leaders in Okta include:

Source: Okta website and proxy statement

(We note that Race is planning to retire early in FY2022, and Okta is in the process of searching for its next go-to market leader. The departure of Race is well-telegraphed and Okta has a lot of time for succession planning, so we’re not concerned with this particular leadership turnover.)

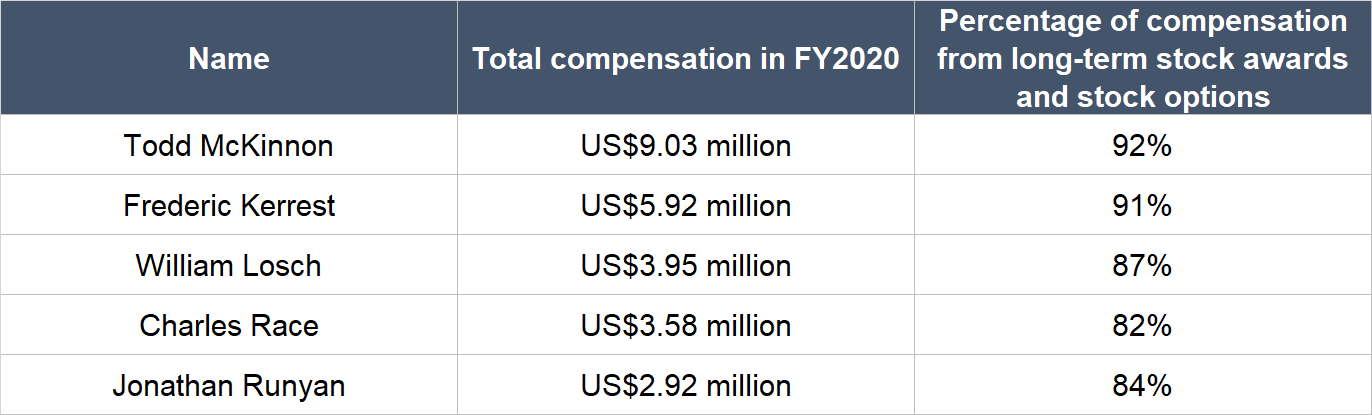

In FY2020, Okta’s senior leaders each received total compensation that ranged from US$2.9 million to US$9.0 million. These are reasonable sums compared to the scale of Okta’s business. Furthermore, 84% to 92% of their total compensation was in the form of stock awards and stock options that vest over four years. This means that the compensation of Okta’s senior leaders are tied to the long run performance of the company’s stock price, which is in turn driven by the company’s business performance. So we think that Compounder Fund’s interests as a shareholder of Okta are well-aligned with the company’s management.

Source: Okta FY2020 proxy statement

Moreover, both McKinnon and Kerrest own significant stakes in Okta. As of 1 April 2020, McKinnon and Kerrest controlled 7.80 million and 3.42 million shares of the company, respectively. These shares have a collective value of US$2.36 billion at Okta’s share price of US$203 as of 5 September 2020. The high stakes that Okta’s two key leaders have lend further weight to our view that management’s interests are aligned with the company’s other shareholders.

We want to highlight that the shares held by McKinnon and Kerrest are mostly of the Class B variety. Okta has two share classes: (1) Class B, which are not traded and hold 10 voting rights per share; and (2) Class A, which are publicly traded and hold just 1 vote per share. McKinnon and Kerrest only controlled 8.9% of Okta’s total shares as of 1 April 2020, but they collectively held 49.9% of the company’s voting power. In fact, all of Okta’s senior leaders and directors together controlled 52.6% of Okta’s voting rights as of 1 April 2020. The concentration of Okta’s voting power in the hands of management (in particular McKinnon and Kerrest) means that we need to be comfortable with the company’s current leadership. We are.

On capability

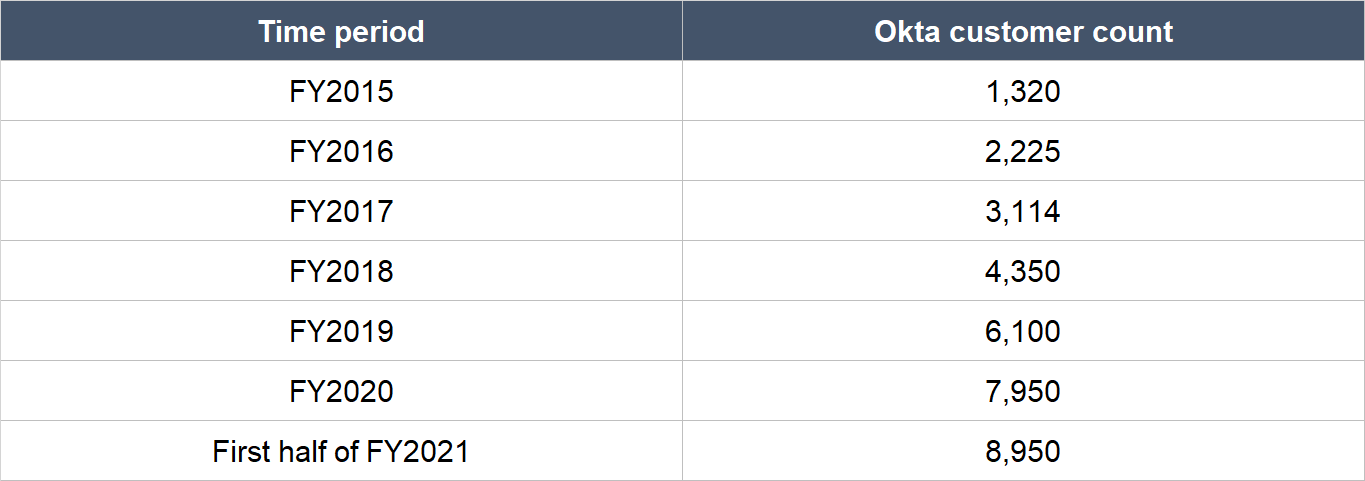

From FY2015 to the first half of FY2020, Okta has seen its number of customers increase seven-fold (42% per year) from 1,320 to 8,950. So the first thing we note is that Okta’s management has a terrific track record of growing its customer count.

Source: Okta FY2021 second-quarter earnings update, FY2020 annual report, and IPO prospectus

To win customers, Okta currently offers over 6,500 integrations with IT (information technology) infrastructure providers, and cloud, mobile, and web apps. This is up from over 5,000 integrations as of 31 January 2017. The companies that are part of Okta’s integration network include services from tech giants such as Microsoft, Alphabet, Amazon.com, salesforce.com (all four companies are also in Compounder Fund’s initial portfolio) and more. Impressively, software providers are increasingly being told by their customers that they have to be integrated with Okta before the software can be accepted.

In our view, the integration also creates a potentially powerful network effect where more integration on Okta’s network leads to more customers, and more customers leads to even more integration. During the aforementioned Stratechery interview, McKinnon shared about the competitive edge that Okta enjoys because of its efforts in integrating thousands of apps:

“[Question]: The average enterprise — maybe it’s hard to say because it varies so widely — how many SaaS services does a typical enterprise subscribe to?

[Todd McKinnon] TM: Especially for any company with over 5,000 employees, it’s thousands of apps. Apps that they’ve purchased commercially, the big ones you’ve heard of, the ones that are in niche industries or verticals you haven’t heard of, and then the ones built themselves, it’s thousands.

[Question]: And then Okta has to build an integration with all of those

[Todd McKinnon] TM: Yeah. One of the big things we did very early on was we got really good at a metadata-driven integration infrastructure, which allowed us to have this burgeoning catalog of pre-packaged integrations, which was really unique in the industry because it is a hundreds or for a big company, it’s thousands of applications.

[Question] And it ends up being a bit of a moat, right? It’s a traditional moat where you dig it up with hard work where you actually went in and you built all of these thousands of integrations, and anyone that wants to come along, if they have a choice of either recreating all the work you did or, we should just use Okta and it’s already sort of all taken care of.

[Todd McKinnon] TM: Yeah, and it’s one of the things people misunderstand on a couple of different levels. The first level is they just get the number wrong. “I think there’s ten, right?” Or I’ve heard of ten big applications, so I think if I connected the ten, that would be enough, which is just off by multiple orders of magnitude.

And then the second thing they get wrong is they think that, especially back in the day it was like, “Oh, there it’s going to be standards that do this.” It’s going to be SAML as a standard. There’s this standard called Open ID. And what we’ve found is that the standards were very thin, meaning they didn’t cover enough of the surface area of what the customers needed, so it might do simple login but it didn’t do directory replication, or not enough of the applications adhere to the standard. So there’s a lot more heterogeneity than people thought of so that moat was a lot wider, a lot faster than people expected.

[Question] Is it fair to say that it’s your goal or maybe it has happened that people thought there would be a standard like SAML that would take care of all of this, but it’s going to end up being that Okta as the standard?

[Todd McKinnon] TM: That is the goal and I think it’s evolving to where there are de facto standards. A big shift is that we have big companies that tell software vendors that if you want to sell to us, you have to integrate to Okta and they have to go to our platform, build the integration, have it be certified. So that’s not a technical standard per se, but it’s a de facto standard of an application that can be sold to a large enterprise.”

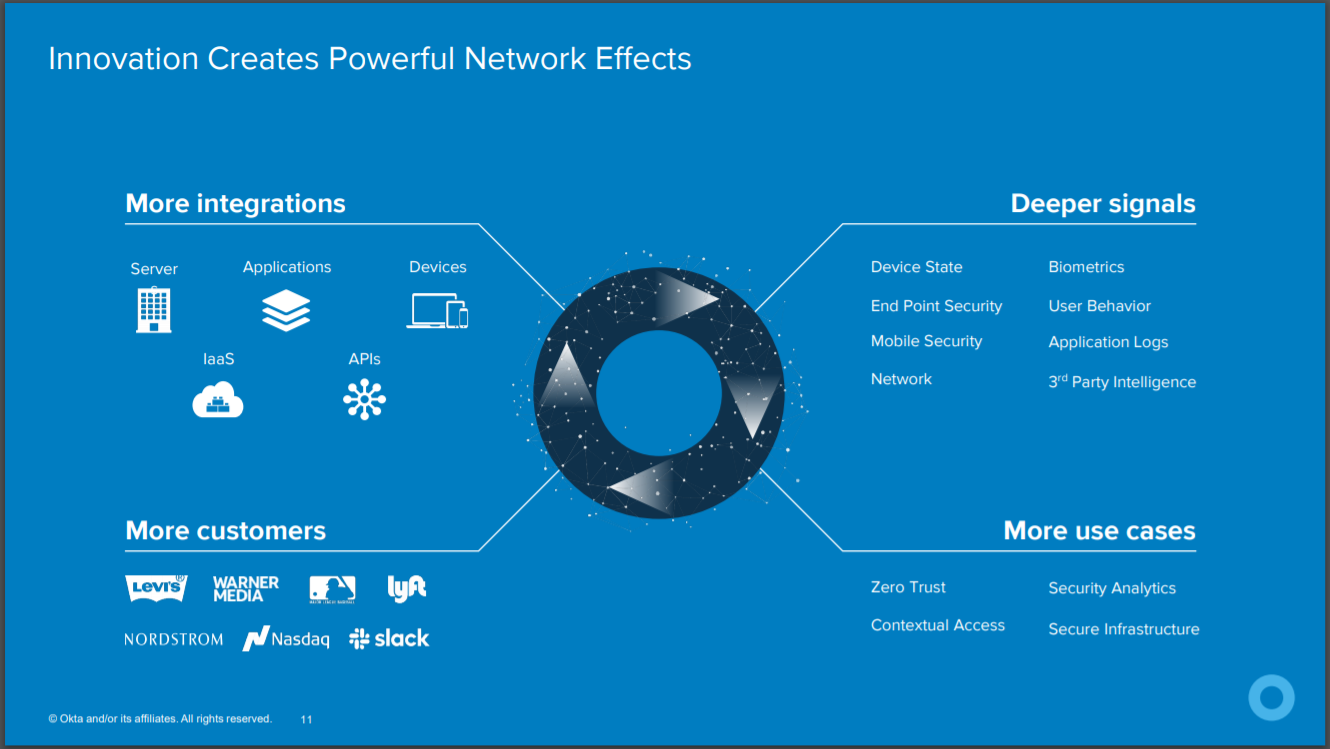

There’s more to Okta’s network effect. That’s because the more integrations and customers there are within Okta, the more signals there are that Okta can learn from and the more use cases Okta can build that benefit its customers. This virtuous cycle is shown in the graphic below:

Source: Okta August 2020 investor presentation

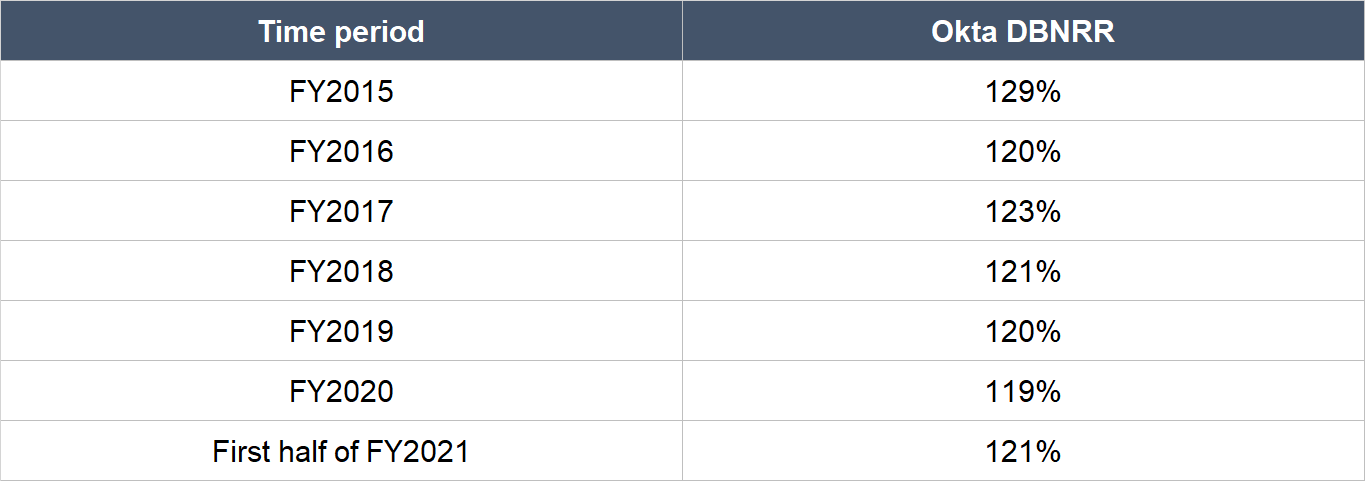

We also credit Okta’s management with the success that the company has found with its land-and-expand strategy. The strategy starts with the company landing a customer with an initial use case, and then expanding its relationship with the customer through more users and/or more use cases. The success can be illustrated through Okta’s strong dollar-based net retention rates (DBNRRs). The metric is a very important gauge for the health of a SaaS company’s business. It measures the change in revenue from all of Okta’s customers a year ago compared to today; it includes positive effects from upsells as well as negative effects from customers who leave or downgrade. Anything more than 100% indicates that the company’s customers, as a group, are spending more – Okta’s DBNRRs have been in the high-teens to high-twenties range over the past few years. There has been a noticeable but slight downward trend in Okta’s DBNRR, but the figure of 121% for the first half of FY2021 is still impressive.

Source: Okta FY2021 second-quarter earnings update, FY2020 annual report, and IPO prospectus

The way that Okta has stepped up to the plate in the current COVID-19 pandemic has given us even more confidence in management’s abilities. Here are a few instances:

- In the first quarter of FY2021, Okta helped Fedex to deploy Okta Identity Cloud within 36 hours (that’s just three days!) to enable more than 85,000 of Fedex’s remote and essential employees to connect to critical applications.

- When COVID-19 started flaring up in the USA, the state of Illinois needed a way to securely manage its digital infrastructure and the digital identities of state employees, state agencies, contractors, and citizens. Illinois chose Okta to provide this important service.

- Prior to the first quarter of FY2021, the US-based wireless provider T-Mobile had already been a customer of Okta for sometime. When T-Mobile recently completed its merger with peer-company Sprint, T-Mobile relied on Okta to manage the digital identities of an additional 30,000 employees.

- In the past few months, Okta successfully handled an incredible level of usage from its customers. Here’s management’s comment on the matter in Okta’s FY2021 second-quarter earnings conference call: “From March through July, there was a one-day record of over 145 million logins, and the number of unique app logins increased by almost 70% to nearly 16 billion. Total MFA [multi-factor authentication] usage increased nearly three times over the same period last year.”

- In early-July 2020, Okta announced “a major milestone in cloud reliability and uptime, offering 99.99% uptime to all customers in every region of the world at no additional cost.”

- Okta ended FY2020 with a headcount of over 2,200. In the first half of FY2021, with COVID-19 as a backdrop, the company has impressively increased its headcount by around 300 in its customer-facing and innovation teams. Instead of retreating at a time of widespread economic distress, Okta went on the offensive.

We also want to point out the presence of Ben Horowitz on Okta’s board of directors. Horowitz is a co-founder and partner in a venture capital firm we admire and that was partly named after him, Andreessen Horowitz (the firm, popularly known as a16z, is an early investor in Okta). Horowitz has served as a director of Okta since February 2010 and we think having him on Okta’s board allows the company’s management to tap on a valuable source of knowledge.

On innovation

Okta is a pioneer in its field. It was one of the first companies that realised that a really important business could be built on the premise of a cloud-based software that secures and manages an individual’s digital identity for cloud-based applications. To us, that is fantastic proof of the innovative ability of Okta’s management. Stratechery’s interview of Todd McKinnon provided a great window on the thinking of him and his team in the early days of Okta’s founding:

“[Question] When Okta first came on the scene, it was Single Sign-on, so you could sign on in one place and then you’d be logged into other places, now it’s an Identity Cloud. Is that an actual shift in the product or strategy or is that just a shift in a marketing term?

[Todd McKinnon] TM: It’s interesting. When we started the company, you could see that cloud was going to be the future. We started 11 years ago, so in 2009, Amazon Web Services was out, Google Apps for Domains was out. So you could kind of see that infrastructure was going to go to the cloud, you could see that collaboration apps were going to go to the cloud. I was working at Salesforce at the time, so it was really clear that the apps stack was going to be in the cloud and we got really excited about what could be possible or what new types of platforms could be built to enable all this.

When we started, it’s funny, we called the first product, which was going to be a cloud single sign-on, we called it Wedge One. So not only was it the wedge, but it was like the first, first wedge. Now it turns out that in order to build cloud single sign on you had to build a lot of pretty advanced stuff behind the scenes to make that simple and seamless, you had to build a directory, you had to build a federation server, you had to build multi-factor authentication, and after we were into it for two or three or four years, we realized that there’s a whole identity system here so it’s much more than a wedge. In fact, it really can be a big part in doing all that enablement we set out to do.

[Question] That’s very interesting, so are you still on Wedge One? Did you ever make it to Wedge Two?

[Todd McKinnon] TM: (laughs) The Wedge keeps getting fatter. The Identity Cloud is pretty broad these days. It’s directory service, it’s reporting analytics, it’s multi-factor authentication, it does API Access Management. It’s very flexible, very extensible, so really the Identity Cloud now is an Identity Platform, it’s striving to really address any kind of identity use cases a customer has, both on the customer side, customer identity, and on the workforce side.

What’s interesting about it is that at the same time over the last eleven years, identity has gone from being something that’s really important maybe for Windows networks or around your Oracle applications to there are so different applications connected from so many types of devices and so many networks that identity is really critical, and we’re in this world now where ten years ago people were telling me “Hey, I’m not sure if it’s possible to build an independent identity company” to now it’s like everyone says, “Oh, it’s such an obvious category that the biggest technology companies in the world want to own it.” So it has been quite a shift.”

We also want to surface a comment that McKinnon made in Okta’s FY2021 second-quarter earnings conference call that we think brilliantly highlights the forward-thinking nature of the company’s leadership team:

“While we’re hyper-focused on executing in today’s environment, I thought it would be helpful to share some of my thoughts around the long-term vision for Okta. So if you look out a little further on the time horizon, as cloud adoption continues to proliferate, five-plus years from now, we see a world where there are just a few first-class clouds that really matter inside a company. These clouds might be for collaboration, CRM, infrastructure, and ERP, for example. Our long-term vision is for identity to be one of these first-class clouds.

We believe identity is key because it facilitates choice and flexibility while enhancing security and reducing risk in all other technologies. In our long-term vision, we see Okta establishing itself as a standard for digital identity. In order to achieve this, we will continue to grow aggressively by adding more users, more customers, particularly large enterprise customers, expanding internationally, adding more strategic partners, and increasing the use cases that come from building out our platform and accelerating the network effects that I mentioned earlier. I hope that gives you a little better understanding of how we’re thinking about building Okta into the next iconic cloud company.”

4. Revenue streams that are recurring in nature, either through contracts or customer-behaviour

Okta runs its business on a SaaS model and generates most of its revenue through multi-year subscriptions, which are recurring in nature. In FY2020, 94% of Okta’s total revenue of US$586.1 million came from subscriptions. The company’s average subscription term was 2.6 years as of 31 January 2020 and interestingly, Okta’s contracts are non-cancelable. The remaining 6% of Okta’s revenue in FY2020 was from professional services, where the company earns fees from helping its customers implement and optimise the use of its products.

It’s important to us too that there’s no customer concentration in Okta’s business. No single customer accounted for more than 10% of the company’s revenue in each year from FY2018 to FY2020. We also want to highlight that Okta has a diversified customer base by industry and that most of its customers are large enterprises. To us, these traits are further positive signs on the resilience of Okta’s revenue streams.

5. A proven ability to grow

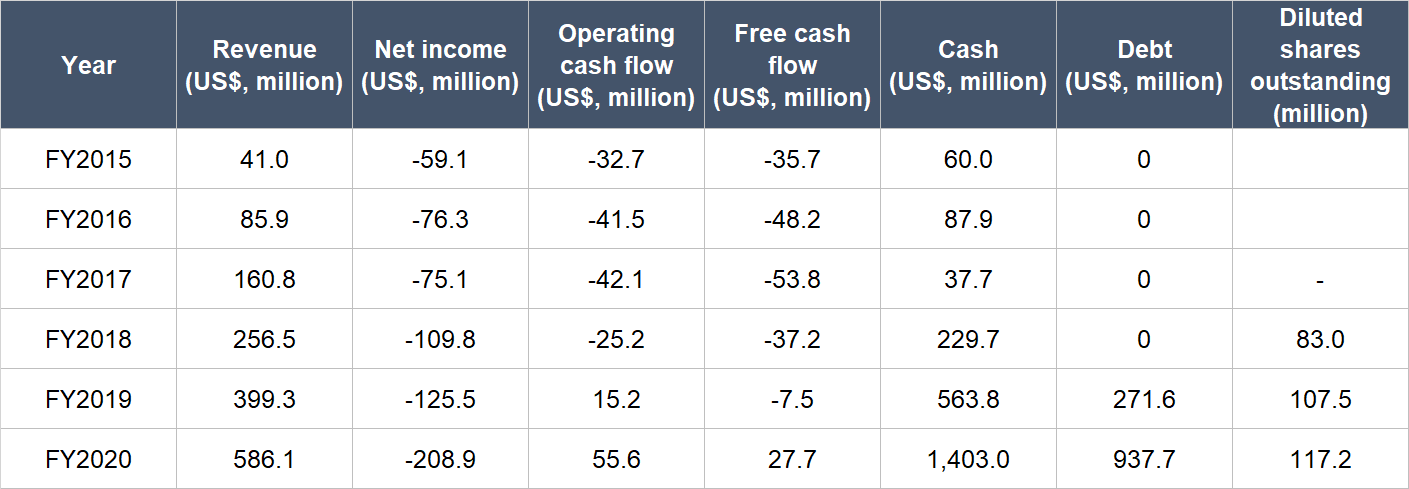

There isn’t much historical financial data to study for Okta, since the company was only listed in April 2017. But we do like what we see:

Source: Okta IPO prospectus and annual reports

A few key points to note about Okta’s financials:

- Okta has compounded its revenue at an impressive annual rate of 70.2% from FY2015 to FY2020. The rate of growth has slowed in recent years, but was still really strong at 46.7% in FY2020.

- Okta is still making losses, but the good thing is that it started to generate positive operating cash flow in FY2019 and positive free cash flow in FY2020..

- The company’s balance sheet remained robust throughout the timeframe under study, with significantly more cash and investments than debt.

- At first glance, Okta’s diluted share count appeared to increase sharply by 29.5% from FY2018 to FY2019. (We only started counting from FY2018 since Okta was listed in April 2017, which is in the first quarter of FY2018.) But the number we’re using is the weighted average diluted share count. Right after Okta got listed, it had a share count of around 91 million. Moreover, Okta’s weighted average diluted share count showed an acceptable growth rate (acceptable in the context of the company’s rapid revenue growth) of 9% in FY2020.

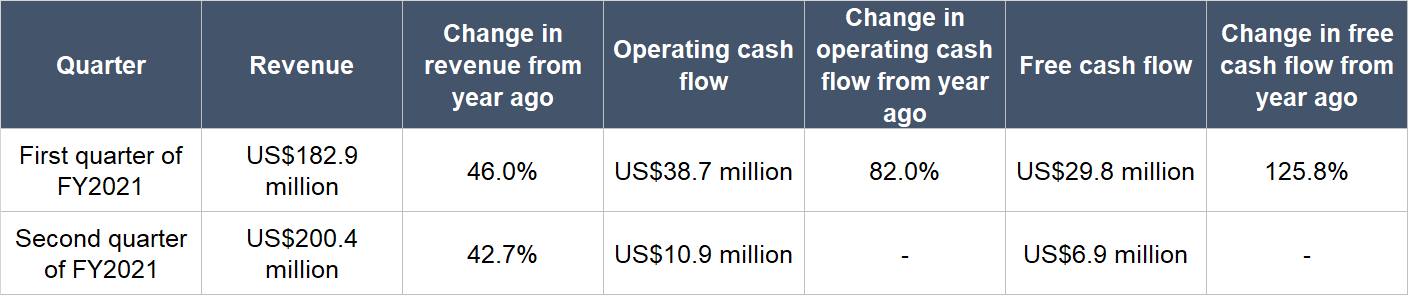

At a time when the US economy is suffering because of COVID-19 (US GDP fell by 9.1% year-on-year in the second quarter of 2020), Okta has managed to continue posting strong revenue growth in the first half of FY2021. In addition, the company is starting to even more heavily flex its cash-flow-muscle. These are all shown in the table below.

Source: Okta earnings updates (operating cash flow and free cash flow for Okta in FY2020’s second-quarter were both negative)

6. A high likelihood of generating a strong and growing stream of free cash flow in the future

Okta has already started to generate positive operating cash flow and free cash flow. We think it’s likely that Okta’s free cash flow will increase at a rapid clip in the future for two reasons.

First, it looks likely to us that Okta will be producing impressive top-line growth in the years ahead. As we discussed earlier, COVID-19 has not dented Okta’s growth and may even be a positive catalyst for its business. But even when the pandemic blows over, we think Okta is set to capitalise on strong secular tailwinds with the growing adoption of cloud services making it necessary for companies to become more efficient at managing the digital identities of their employees, contractors, partners, and customers.

Second, we think Okta can enjoy a higher free cash flow margin in the future as its business scales. Right now, Okta has a poor trailing free cash flow margin (free cash flow as a percentage of revenue) of just 7.9%. But we think there’s ]plenty of room for improvement given the typically asset-light nature of a software business. And for perspective, Veeva Systems, a SaaS company serving the life sciences industry and another of Compounder Fund’s holdings in the initial portfolio, has an average free cash flow margin of 29% in its last five completed fiscal years.

Valuation

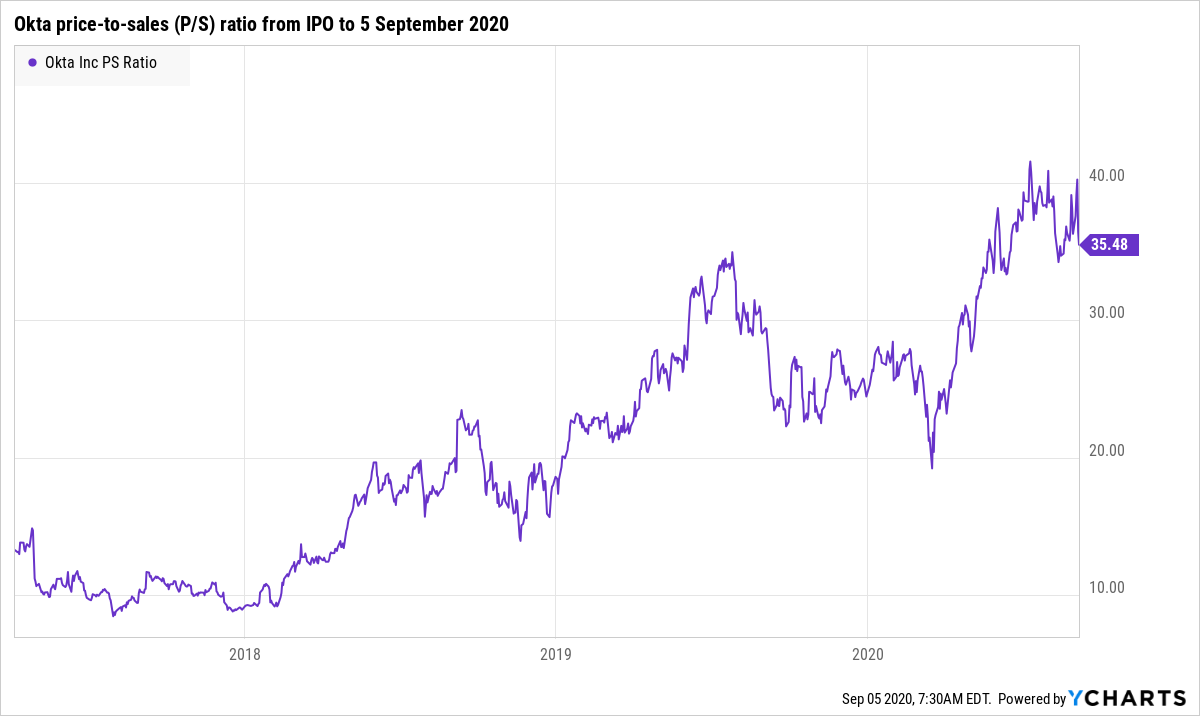

We completed our purchases of Okta shares with Compounder Fund’s initial capital in late July 2020. Our average purchase price was US$210 per Okta share. At our average price and on the day we completed our purchases, Okta shares had a trailing price-to-sales (P/S) ratio of around 40. We like to keep things simple in the valuation process. In Okta’s case, we think the P/S ratio is an appropriate metric to value the company, since the company has yet to produce much free cash flow.

The P/S ratio of 40 is pretty darn high. For perspective, if we assume that Okta has a 25% free cash flow margin today, then the company would have a price-to-free cash flow ratio of 160 based on the current P/S ratio (40 divided by 25%). Moreover, the P/S ratio of 40 is high when compared to history. The chart below shows Okta’s P/S ratio from its listing to 5 September 2020:

But there are strong positives in Okta’s favour. The company has: (1) Revenue that is low compared to a large and possibly fast-growing market; (2) a software product that is mission-critical for users; (3) a large and rapidly expanding customer base; and (4) sticky customers who have been willing to significantly increase their spending with the company over time. We believe that with these traits, there’s a high chance that Okta will continue posting excellent revenue growth – and in turn, excellent free cash flow growth – in time to come.

Indeed, Okta has a target to grow its revenue by 30% to 35% annually from now till FY2024, and to have a free cash flow margin of between 20% and 25% at the end of that period. These goals were communicated by management in April 2020 during Okta’s Investor Day event. For perspective, Okta projected revenue growth of 37% for the whole of FY2021 in the fiscal year’s second-quarter earnings update; this is up from a revenue-growth outlook of between 31% and 33% given in the first quarter.

For perspective, Okta carried a P/S ratio of 36.1 at the 5 September 2020 share price of US$203.

The risks involved

There are five key risks we’re watching with Okta.

The first is Okta’s short history in the stock market, given that its IPO was just three years ago in April 2017. But we are willing to back Okta because we think its business holds promise for fast-growth for a long period of time (the company’s identity-as-a-service business is very important for the digital transformation that so many companies are currently undergoing).

Competition is another risk we’re keeping an eye on. In its FY2018 and FY2019 annual reports, Okta named technology heavyweights such as Alphabet, Amazon, IBM, Microsoft, and Oracle as competitors. In its FY2020 annual report, Okta singled out Microsoft as its “principal competitor.” All of them have significantly stronger financial might compared to Okta. But we’re comforted by Okta’s admirable defense of its turf – the proof is in Okta’s strong DBNRRs and impressive growth in customer-numbers over the years. Moreover, in late 2019, market researchers Gartner and Forrester also separately named Okta as a leader in its field.

Okta’s high valuation is the third risk. The high valuation adds pressure on the company to continue executing well; any missteps could result in a painful fall in its stock price. This is a risk we’re comfortable taking.

Hacking is also a risk we’re watching. Logging into applications is often a time-sensitive and mission-critical part of an employee’s work. Okta’s growth and reputation could be severely diminished if the company’s service is disrupted, leading to customers being locked out of the software they require to run their businesses for an extended period of time.

COVID-19 is the fifth risk. The pandemic has resulted in severe disruptions to economic activity in many parts of the world, the USA included. We think that the mission-critical nature of Okta’s service means that its business is less likely to be harmed significantly by any coronavirus-driven recession. Okta’s recent earnings updates have shown this to be the case. In the company’s FY2021 second-quarter earnings conference call, CFO William Losch said that Okta has “not experienced any degradation in gross renewal rates during the pandemic and continue to experience strength with customer upsells, particularly with… enterprise customers.” But there may still be headwinds in the future.

Ultimately, we will consider parting ways with Okta if we see any or all of the following signs from the company: (1) The DBNRR comes in at less than 100% for an extended period of time; (2) it fails to increase its number of customers; and (3) it’s unable to convert revenue into free cash flow at a healthy clip in the future.

Summary and allocation commentary

In summary, Okta has:

- A valuable cloud-based identity-as-a-service software platform that is often mission-critical for customers;

- high levels of recurring revenue;

- outstanding revenue growth rates;

- positive operating cash flow and free cash flow, with the potential for much higher free cash flow margins in the future;

- a large, mostly untapped addressable market that could potentially grow in the years ahead;

- an impressive track record of winning customers and increasing their spending; and

- capable leaders who are in the same boat as the company’s other shareholders

Okta does have a rich valuation, so we’re taking on valuation risk. There are also other risks to note, such as Okta’s short listing history, competitors with heavy financial muscle, hacking, and potential headwinds because of COVID-19.

After weighing the pros and cons, we initiated a 2.0% position – a medium-sized allocation – in Okta with Compounder Fund’s initial portfolio. We think Okta scores well in terms of having a sizeable market opportunity and a high probability of being able to grow into its market. But our enthusiasm for the company is also tempered by its high valuation.

And here’s an important disclaimer: None of the information or analysis presented is intended to form the basis for any offer or recommendation; they are merely our thoughts that we want to share.