Compounder Fund: MongoDB Investment Thesis - 23 Feb 2021

Data as of 19 February 2021

MongoDB Inc (NASDAQ: MDB), which is based and listed in the USA, is one of the 40 companies in Compounder Fund’s initial portfolio. This article describes our investment thesis for the company.

Company description

MongoDB’s business is simple: The company sells subscriptions to its non-relational database platform. But wait, what’s a non-relational database? What is a database?

A database is simply a platform to store data. Every piece of software requires a database to store, organize, and process data. The database has a direct impact on the software’s performance, scalability, flexibility, and reliability, so its selection is a highly strategic decision for companies.

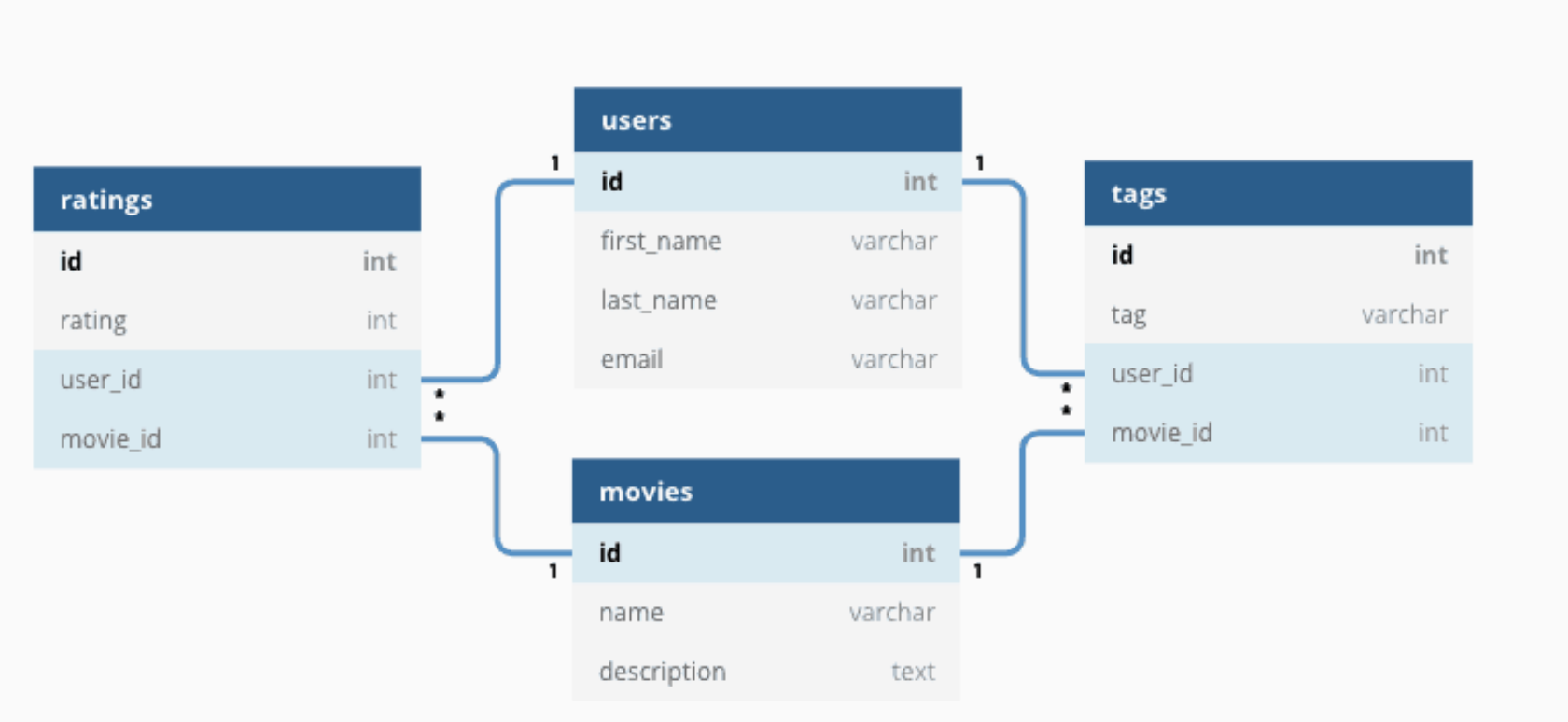

There are many different types of databases to choose from. In the 1970s, relational databases were first developed and they used a programming language known as Structured Query Language (SQL). Relational databases store and organise data points that are related to one another in table form. The picture below is an example of what a relational database looks like.

Source: OmniSci website

Relational databases were useful from the 1980s to the late 1990s. But because they were used to store structured data, they started to lose relevance with the rise of the internet. Relational databases were too rigid for the internet era and were not built to support the volume, velocity, and variety of data that came with the rise of the web. This is where non-relational databases – also known as NoSQL, which stands for either “non SQL” or “not only SQL” – come into play.

NoSQL databases are not constrained to relational databases’ tabular format of data storage. As a result, non-relational databases provide greater flexibility and are adept for working with Big Data, which refers to huge and complex data sets. Big Data can come from a variety of sources – such as mobile devices, wearables, IoT (internet of things) sensors, online payments, website visits, and more – and has three defining characteristics:

- Volume – We’re talking about massive quantities of data; for example, IoT sensors in just one factory floor can produce thousands of data feeds each day

- Velocity – Because Big Data involves huge amounts of data, the data needs to be processed rapidly in order to produce useful insights

- Variety – Big Data can come in many data forms and they are often unstructured, such as audio, video, photos, and more

There are four main types of NoSQL databases, namely, wide-column stores; key-value databases; graph databases; and document databases. Each type of NoSQL database has their uses. MongoDB’s database platform is document-based. A document database is apt for a wide variety of use cases and is often used as a general purpose database. It is also intuitive and easy for software developers to work with.

MongoDB has two main subscription-based products:

- MongoDB Enterprise Advanced, a comprehensive database platform for enterprise customers that can be run in the cloud, on-premise, or in a hybrid (cloud plus on-premise) environment.

- MongoDB Atlas, a multi-cloud-hosted DBaaS (database-as-a-service) platform.

In the first nine months of its fiscal year ending 31 January 2021 (FY2021), MongoDB earned US$419.4 million in total revenue. The two products each contributed around US$185 million (that’s 44% each) to MongoDB’s total revenue for the period. MongoDB also provides consulting and training services that are related to deploying its database platform for customers. These services accounted for 4% of the company’s revenue in the first nine months of FY2021. MongoDB also provides a free-to-use “lite” version of its database platform called Community Server; this free database has been downloaded more than 130 million times since its introduction in 2009.

From a geographical perspective, the Americas is the most important market for MongoDB, accounting for 62% of the company’s total revenue for the first nine months of FY2021. EMEA (Europe, Middle East, and Africa) is the next largest market with a 30% share. The remaining 8% comes from the Asia Pacific region.

Investment thesis

We have laid out our investment framework in Compounder Fund’s website. We will use the framework to describe our investment thesis for MongoDB.

1. Revenues that are small in relation to a large and/or growing market, or revenues that are large in a fast-growing market

Research firm IDC expects the global database market to compound at 12% annually to reach US$106 billion in 2024, up from US$68 billion in 2020. Meanwhile, in a report published in the first half of 2020, Allied Market Research estimated that the NoSQL database market will nearly 10x from US$2.4 billion in 2018 to US$22.1 billion in 2026.

These heady growth projections are just that – projections. But we think they are sensible for a few reasons. First, we shared in our investment thesis for Alteryx that “the quantity of data in the world (generated, captured, and replicated) would compound at an astounding rate of 61% per year, from 33 zettabytes then to 175 zettabytes in 2025,” according to IDC in late-2018. This massive explosion in the quantity of data should be a tailwind for database providers, in our opinion. Second, most of the data generated in the world is unstructured (up to 80%, according to a 2016 IBM article). As discussed earlier, NoSQL databases are more suitable than legacy relational databases for handling unstructured data.

In the meantime, MongoDB’s revenue for the 12 months ended 31 October 2020 is US$521.0 million, a mere fraction of the global database market.

2. A strong balance sheet with minimal or a reasonable amount of debt

MongoDB is still in its high growth phase and is generating negative free cash flow (more on this later). But the company has a decent balance sheet that can support the cashburn.

MongoDB exited October 2020 with US$966.3 million in cash and investments and slightly lower debt of US$947.7 million (all of which are in the form of convertible notes). Having more cash and investments than debt is a positive sign. Moreover, the notes mature in either 2024 or 2026, with the lion’s share of the notes maturing in the latter year , so there’s no short-term need for MongoDB to cough up any cash to repay the convertible notes.

3. A management team with integrity, capability, and an innovative mindset

On integrity

MongoDB was founded in 2007 by Dwight Merriman, Eliot Horowitz, and Kevin Ryan. The trio encountered the difficulties of working with legacy databases at their previous internet advertising company DoubleClick, and this experience led them to set up MongoDB. Today, only Merriman is still with MongoDB and even then, he’s only a director. Horowitz was MongoDB’s Chief Technology Officer (CTO) from 2008 to mid-2020, when he resigned from his post. Meanwhile, Ryan left MongoDB’s board in July 2019.

The most important leader at MongoDB at the moment is the 54 year-old Dev Ittycheria, who joined the company as President and CEO in September 2014, and has been in both roles since. Ittycheria has two key lieutenants, one of whom is Michael Gordon, MongoDB’s Chief Operating Officer and Chief Financial Officer. Gordon ,51, has been in the COO and CFO roles since November 2018 and July 2015, respectively. We appreciate the multi-year tenures that both Ittycheria and Gordon have as MongoDB’s leaders. Mark Porter, MongoDB’s Chief Technology Officer, is Ittycheria’s other key lieutenant. Porter, who’s 54, joined MongoDB only in July 2020 but has many years of experience in senior leadership roles at other technology companies, most notably at Amazon Web Services (where he worked on relational databases) and Oracle. We think the Chief Technology Officer role is important for MongoDB because the company’s product – its database platform – is technology-driven.

In FY2020, Ittycheria and Gordon received total compensation of US$9.36 million and US$5.24 million, respectively. We think these are reasonable sums when compared to the scale of MongoDB’s business. For perspective, the company’s revenue for the year was US$399.8 million. More importantly, the lion’s share of their compensation (91.1% for Ittycheria and 87.4% for Gordon) came from stock awards that we think are well structured: The stock awards comprise restricted stock units (RSUs) that vest over four years. This means that the bulk of Ittycheria and Gordon’s compensation depends on multi-year changes in MongoDB’s share price, which is in turn tethered to the long-term performance of the company’s business. We think this structure aligns the interests of Ittycheria and Gordon with those of MongoDB’s other shareholders.

(We don’t have compensation data for Porter since he joined after the end of FY2020, but we’re confident that his compensation will be well-designed, given what we know about how Ittycheria and Gordon are remunerated.)

And speaking of alignment of interests, Ittycheria owns 995,139 MongoDB shares based on his latest regulatory filings. At MongoDB’s 19 February 2021 share price of US$418, Ittycheria’s shares are worth a sizeable US$416 million. To us, this represents significant skin in the game for MongoDB’s CEO.

On capability and ability to innovate

We think Ittycheria and his team have a good track record at executing and innovating. There are a few things we want to discuss.

First, Ittycheria has an impressive background as a tech entrepreneur and business leader. In 2001, he co-founded BladeLogic, a company that provides tools for datacenter automation. He led BladeLogic as CEO through its IPO in 2007 and until it was acquired by BMC in 2008 for US$800 million.

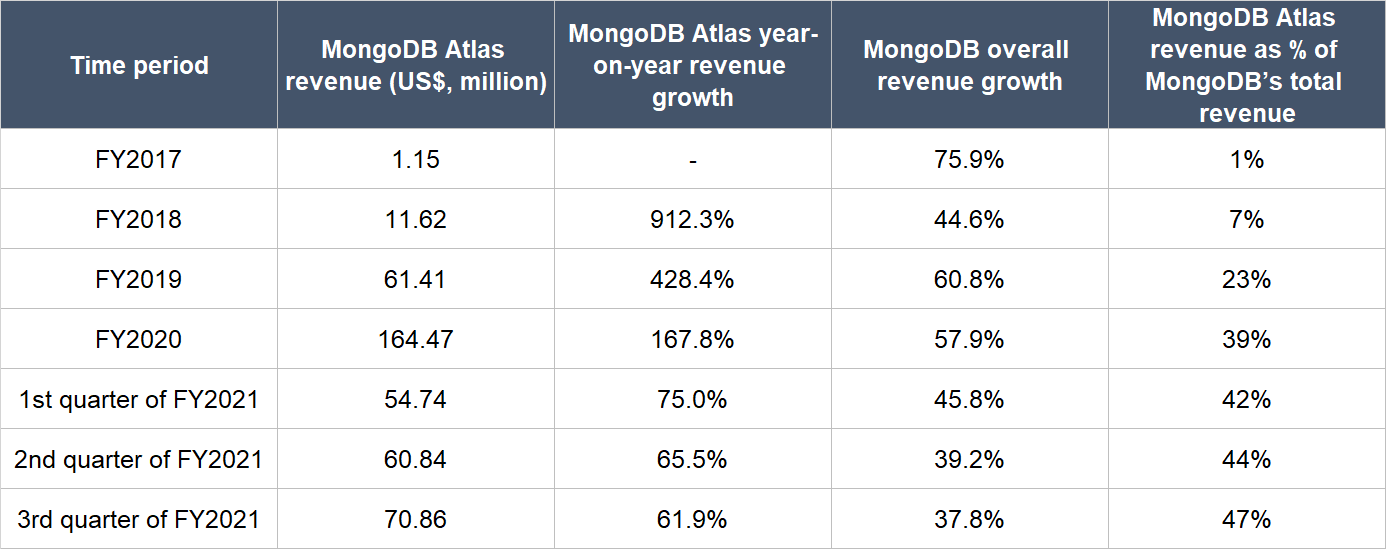

Second, Ittycheria presided over the launch of MongoDB Atlas in June 2016. MongoDB Atlas is available on multiple public cloud computing providers (such as Amazon Web Services, Google Cloud, and Microsoft Azure) and it provides a number of important benefits for users. One, MongoDB Atlas helps users to avoid lock-in by any cloud computing provider. Two, MongoDB Atlas allows the software developers of its users to focus on their own applications and business objectives, rather than managing a database and its related infrastructure, thus improving developer productivity. Three, by removing the need for users to manage a database and its infrastructure, MongoDB Atlas helps users to lower the cost of ownership. Since its launch, MongoDB Atlas’s revenue has been growing rapidly – far faster than MongoDB’s overall revenue growth – and has been growing in importance to the company. These are shown in the table below:

Source: MongoDB annual reports and quarterly earnings updates

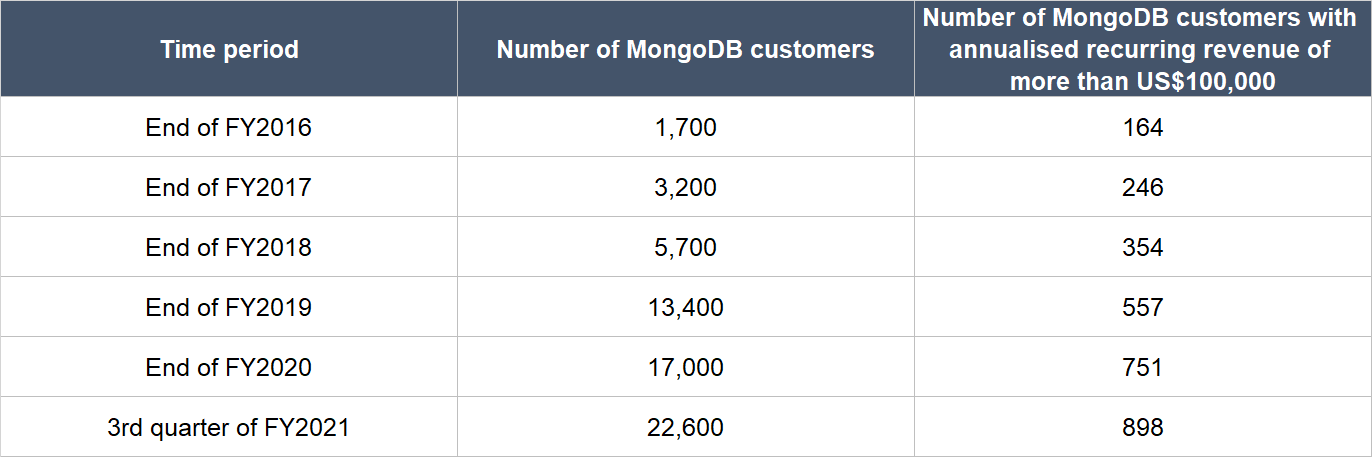

Third, under Ittycheria’s leadership, MongoDB has accumulated a fantastic track record with its land-and-expand strategy. The strategy starts with the company landing a customer with an initial use case, and then expanding the customer’s subscriptions over time. The success can be illustrated through two things: (1) The strong growth over time, shown in the table below, in MongoDB’s customer count and the number of customers with annual recurring revenue (ARR) of US$100,000 or more; and (2) MongoDB’s net ARR expansion rate of over 120% in each quarter for 23 consecutive quarters, or a period of nearly six years, as of the third quarter of FY2021. The net ARR expansion rate essentially measures the change in ARR from all of MongoDB’s customers a year ago compared to today; it includes positive effects from upsells as well as negative effects from customers who leave or reduce their subscriptions. Anything more than 100% indicates that MongoDB’s customers, as a group, are spending more.

Source: MongoDB annual reports and quarterly earnings updates

Fourth, MongoDB’s database platform is very popular with users. We can see this from MongoDB’s high net promoter score (NPS) of 84. The NPS ranges from -100 to +100 and it measures the willingness of customers to recommend a company’s product or service to others and can be a gauge of customer loyalty and satisfaction. MongoDB counts legacy database software providers such as IBM and Oracle as competitors. For perspective, IBM and Oracle have much lower NPS-es of 27 and 25, respectively. We think the high popularity of MongoDB’s database platform stems from the company’s focus on wanting to build truly great products. In the company’s own words, its database product was ”built by developers for developers.” MongoDB was born when its co-founders became frustrated with the shortcomings of legacy database providers. It appears to us that Ittycheria and his team have inherited the same fire to build a better database platform.

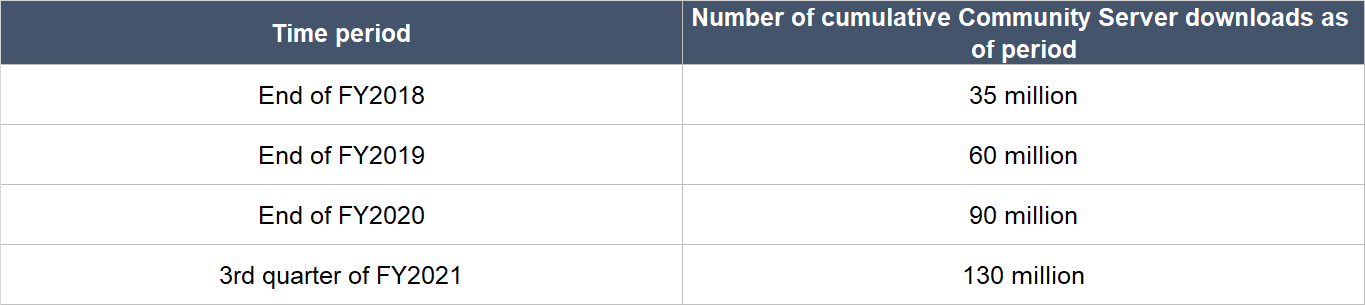

Fifth, Ittycheria and his team have allowed MongoDB’s unique “freemium” model – the company has a Community Server database product that is free to use – to flourish. We mentioned earlier that Community Server currently has more than 130 million downloads since its introduction in 2009. These download numbers did not happen overnight, and are the result of steady growth over the years, as shown in the table below. Community Server allows software developers to evaluate MongoDB’s offering in a frictionless manner and we think it has been a strong contributor to the company’s overall business growth.

Source: MongoDB annual reports and quarterly earnings update

Sixth, Ittycheria appears to have fostered a great workplace culture at MongoDB. Glassdoor is a platform for employees to rate their companies anonymously. Currently, 90% of MongoDB-raters on Glassdoor would recommend a friend to work at the company. Ittycheria also has a 98% approval rating as CEO, far higher than the average Glassdoor CEO rating of 69% in 2019.

4. Revenue streams that are recurring in nature, either through contracts or customer-behaviour

In the first nine months of FY2021, 96% of MongoDB’s total revenue of US$419.4 million were from subscriptions. This is consistent with MongoDB’s history (for FY2016-FY2020), where 90% or more of its revenue would come from subscriptions. The subscriptions to MongoDB Enterprise Advanced are generally for one year terms and are on a per-server basis. Meanwhile, subscriptions to MongoDB Atlas have a mixture of monthly terms (which are based on usage) and annual commitments.

We like subscription businesses, because subscriptions are recurring by nature. But just having a subscription-based business alone does not mean that a company actually has recurring revenue. If the business has a high churn rate (the rate of customers leaving), the company has to constantly fill a leaky bucket. That’s not recurring revenue.

There are good reasons why we think MongoDB does not have to deal with a leaky bucket. As databases are critical to the smooth running and operation of software applications, once a customer uses MongoDB’s database platform, it becomes an important part of the customer’s operations. This means that MongoDB’s customers are likely to continuously renew their contracts and even increase their net spend on MongoDB products as their usage grows. The numbers bear this out. When we were discussing MongoDB’s management earlier, we shared that the company has a multi-year history of (1) rapid growth in its number of customers and (2) producing excellent net ARR expansion rates of more than 120%.

We also want to highlight another trait about MongoDB’s business that strengthens our view on the recurring nature of the company’s revenue: There’s no customer-concentration risk. No single customer accounted for more than 10% of MongoDB’s revenue in FY2020, and this was the case too going back to at least FY2017.

5. A proven ability to grow

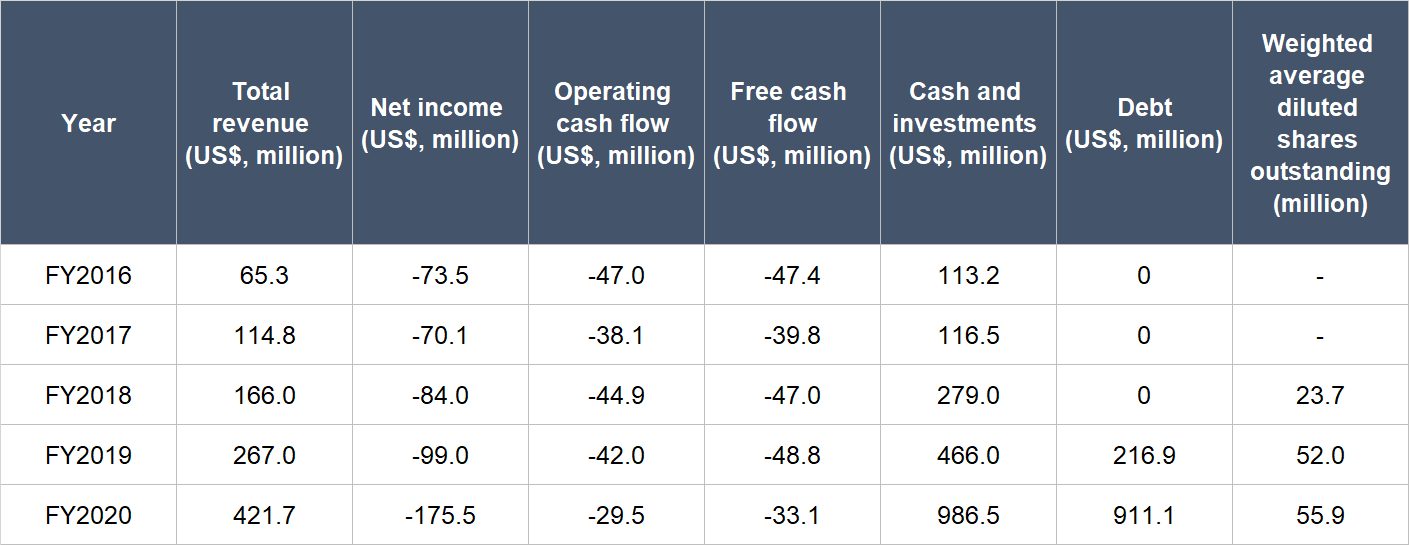

The table below shows MongoDB’s key financials for FY2016 to FY2020. There isn’t much historical financial data to study for MongoDB since the company was listed only in October 2017.

Source: MongoDB IPO prospectus and annual reports

Some important things to highlight from the numbers above:

- MongoDB’s revenue has compounded at an impressive annual rate of 59.4% for FY2016-FY2020. Growth in FY2020 was equally impressive at 57.9%.

- MongoDB is still in its high growth phase so it is not surprising to see that it is not profitable yet. The company’s net loss in fact widened from US$73.5 million in FY2016 to US$175.5 million in FY2020. But our focus is on MongoDB’s cash flows.

- MongoDB’s operating cash flow and free cash flow have both been negative in each year for FY2016-FY2020. But importantly, the numbers are trending in the right direction. There are improvements in MongoDB’s margins for operating cash flow (operating cash flow as a percentage of revenue) and free cash flow (free cash flow as a percentage of revenue). The operating cash flow margin has increased from -71.9% in FY2016 to -7.0% in FY2020. Likewise, the free cash flow margin has stepped up in the same period from -72.7% to -7.8%.

- MongoDB’s balance sheet was strong for the entire time frame under study, with debt being either zero, or comfortably lower than the company’s cash and investments.

- We only started looking at MongoDB’s share count in FY2018 since it was listed in October 2017, which is the second half of the financial year. At first glance, MongoDB’s share count appears to have increased significantly from FY2018 to FY2019 (a 119% jump). But the number we used is the weighted average diluted share count. Right after MongoDB got listed in October 2017, it had a share count of around 49 million. This means that the increase in share count in FY2019 was much milder (in the high single-digit percentage range). Meanwhile, the share count increased by 7.5% in FY2020. These increases are higher than what we would typically like to see, but the good thing is that MongoDB’s revenue growth in FY2019 and FY2020 were much higher than its share count growth. Nonetheless, we will be keeping an eye on future changes in MongoDB’s share count.

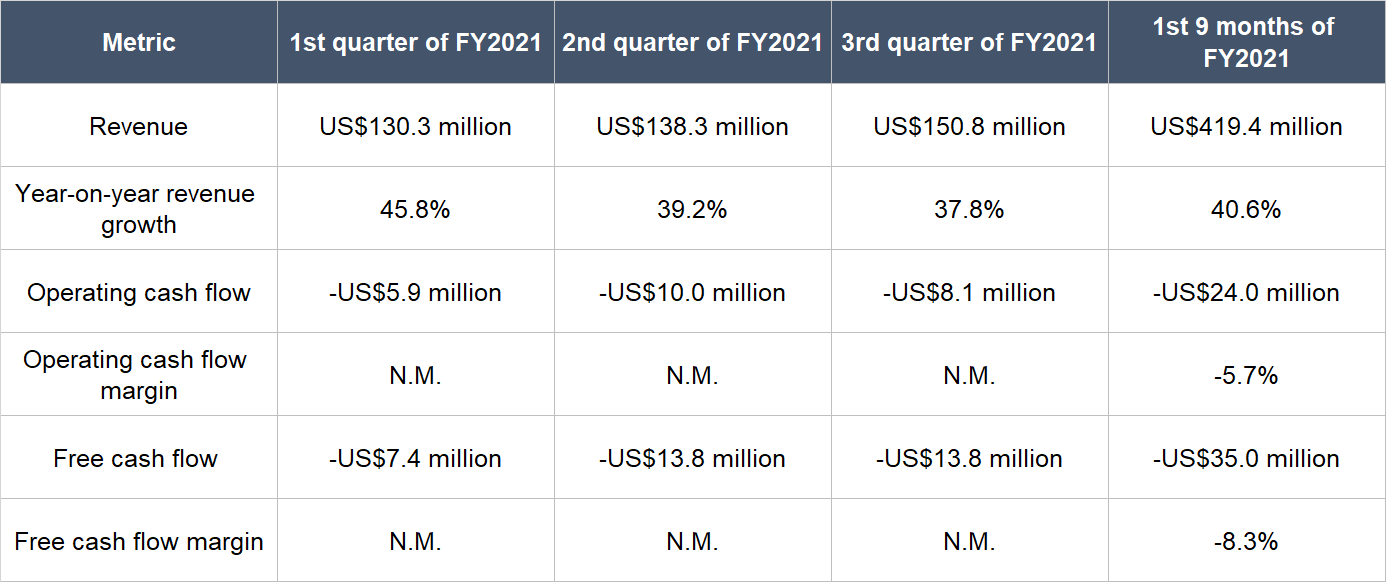

The biggest economic story in 2020 is the emergence of the COVID-19 pandemic. MongoDB did experience some negative impact to its business in the first nine months of FY2021 (referring to the nine months ended 31 October 2020) because of the virus. But the company still managed to produce strong revenue growth while keeping its free cash flow margin stable, albeit negative. The table below shows MongoDB’s revenue, operating cash flow, operating cash flow margin, free cash flow, and free cash flow margin, for the first nine months of FY2021. MongoDB’s weighted average diluted share count increased by 5.2% year-on-year for the period, which is on the high side, but still acceptable given the much higher revenue growth rate of 40.6%.

Source: MongoDB quarterly earnings updates (N.M. = not meaningful)

6. A high likelihood of generating a strong and growing stream of free cash flow in the future

As we mentioned in this article previously, MongoDB has yet to generate positive free cash flow. But we do think the company has a clear path toward generating free cash flow in the future because it has strong unit economics in its business. There are two examples we can point to.

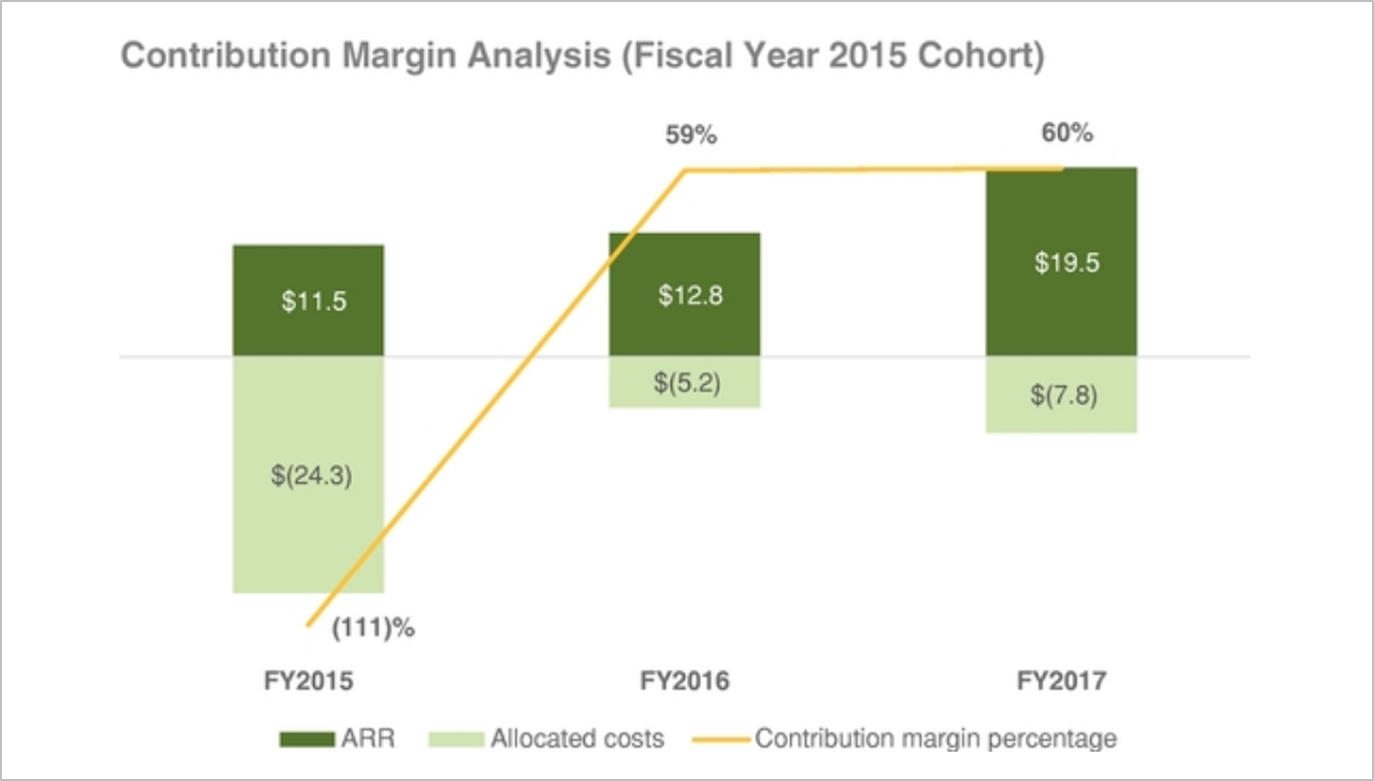

First, the contribution margin of MongoDB’s customers improve over time. The chart below shows the change in the contribution margin for its FY2015 cohort of customers from FY2015 to FY2017. In the first year (FY2015), the contribution margin was low – negative 111% – because the costs to acquire and provide the database subscription service to the cohort of customers was high. But in FY2016 and FY2017, the contribution margin for the FY2015 cohort became strongly positive because of an increase in its ARR and a decrease in costs (because the cost of acquisition becomes much lower).

Source: MongoDB IPO prospectus

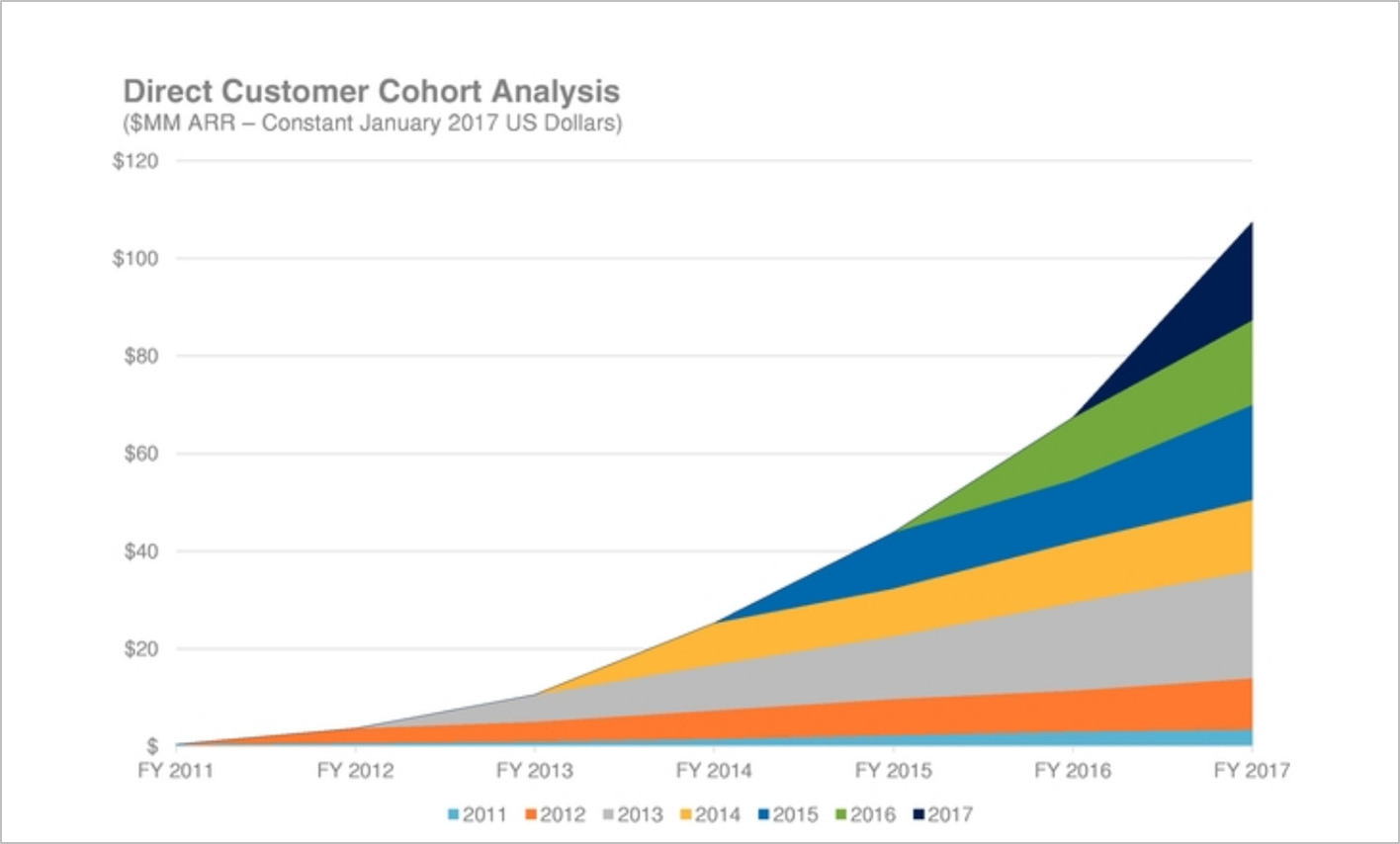

Second, the ARR generated by each cohort of MongoDB’s customers has increased over time. The chart below shows the change in ARR for each annual cohort of customers from FY2011 to FY2017. Each coloured band thickens as the years go by, indicating that each cohort’s ARR increased with time. For example, the FY2013 cohort increased their initial ARR by over four times from US$5.3 million to US$22.1 million in FY2017. We don’t have more recent ARR numbers, but we have good reason to believe that this trend of growth in ARR for each customer-cohort has continued: We mentioned earlier that (1) MongoDB’s net ARR expansion rate had exceeded 120% for 23 consecutive quarters as of the third quarter of FY2021, and (2) MongoDB’s number of customers with more than US$100,000 in ARR has grown significantly over time.

Source: MongoDB IPO prospectus

As MongoDB’s business continues to scale, we believe it will eventually start to produce solid free cash flow. Our belief is also strengthened by the company’s consistently high gross profit margin of around 70% going back to at least FY2016.

Valuation

We completed our purchases of MongoDB shares with Compounder Fund’s initial capital in late July 2020. Our average purchase price was US$211 per MongoDB share. At our average price and on the day we completed our purchases, MongoDB shares had a trailing price-to-sales (P/S) ratio of around 28. We like to keep things simple in the valuation process. In MongoDB’s case, we think the P/S ratio is currently an appropriate metric to gauge the value of the company, since the company does not have any history yet of generating free cash flow.

There’s no need to consult any historical valuation chart to know that the P/S ratio of 28 is high – and that’s a risk. For perspective, if we assume that MongoDB has a 25% free cash flow margin today, then the company would have a price-to-free cash flow ratio of 112 (28 divided by 25%). But we think MongoDB has years of rapid growth ahead of it, given its highly popular database platform and the fact that NoSQL databases have what we think is a strong tailwind going for them (the explosion in the amount of unstructured data generated and the fact that NoSQL databases are better suited to handle unstructured data). This makes us comfortable with paying up for MongoDB’s shares, since we think the company has a good chance of being able to grow into its valuation.

For perspective, MongoDB carried a P/S ratio of around 47 at its 19 February 2021 share price of US$418.

The risks involved

There are four main risks we see with our MongoDB investment.

First is competition. Earlier, we brought up IBM and Oracle as two of MongoDB’s competitors. Other key competitors that MongoDB name-dropped in its latest annual report include Microsoft, Amazon, and Alphabet (parent of Google). All five of the named-competitors are giant technology companies that have significantly stronger financial resources than MongoDB in terms of their revenues and cash on hand. We believe that MongoDB boasts an impressive database platform that software developers love and so far, the company has defended its turf impressively. This can be seen in the company’s excellent net ARR expansion rates and growth in customer numbers that we brought up earlier. But we’re still keeping an eye on changes in the competitive landscape of the database market.

Second, there’s key-man risk. We think Ittycheria has been an important architect of MongoDB’s growth in recent years. Should he leave the company for any reason, we’ll be watching the leadership transition closely.

Third, although we are confident of MongoDB’s ability to produce strong free cash flow in the future, there’s no guarantee that it can do so and the timeline for positive free cash flow may also be long. If MongoDB has an extended period of negative free cash flow, it will have to raise more capital. Although the financial markets have been kind to MongoDB (and many other software companies), this may not be the case in the future. If MongoDB has to raise capital at inopportune times, existing shareholders could be diluted substantially.

Lastly, there’s valuation risk. We think MongoDB’s business is likely to grow at a rapid clip for many years and so it deserves its premium valuation. But if there are any hiccups in MongoDB’s business in the future – even if they are temporary – there could be a painful fall in the share price. This is a risk we’re comfortable taking as long-term investors.

Summary and allocation commentary

Summing up MongoDB, it has:

- A large and growing market opportunity in the form of the global database market

- A robust balance sheet with more cash and investments than debt

- An innovative management team that has (1) built a database platform that is well-loved by the software developer community, and (2) well-aligned incentives

- High levels of recurring revenues because of its subscription model and the fact that the company has a good track record of retaining and upselling customers

- An impressive history of revenue growth

- A high chance of producing a robust stream of free cash flow in the future because of the strong unit economics in its business.

There are risks to note, and they include competition from deep-pocketed companies; key-man risk; the possibility that MongoDB is unable to produce free cash flow; and a high valuation.

After weighing the pros and cons, we decided to initiate a 1% position in MongoDB – a small-sized allocation – with Compounder Fund’s initial capital. We appreciate the strengths we see in MongoDB’s business, but our enthusiasm is tempered by the company’s high valuation and also its current inability to produce positive operating cash flow.

And here’s an important disclaimer: None of the information or analysis presented is intended to form the basis for any offer or recommendation; they are merely our thoughts that we want to share. Of all the other companies mentioned, Compounder Fund also owns shares in Alphabet, Amazon, and Microsoft. Holdings are subject to change at any time.