Compounder Fund: Mastercard Investment Thesis - 03 Dec 2020

Data as of 1 December 2020

Mastercard (NYSE: MA), which is based and listed in the USA, is one of the 40 companies in Compounder Fund’s initial portfolio. This article describes our investment thesis for the company.

Company description

Mastercard should be a familiar company to many of you who are reading this. Chances are, you have a Mastercard credit card in your wallet. But what’s interesting is that Mastercard is not in the business of issuing credit cards – it’s also not in the business of providing credit to us as consumers.

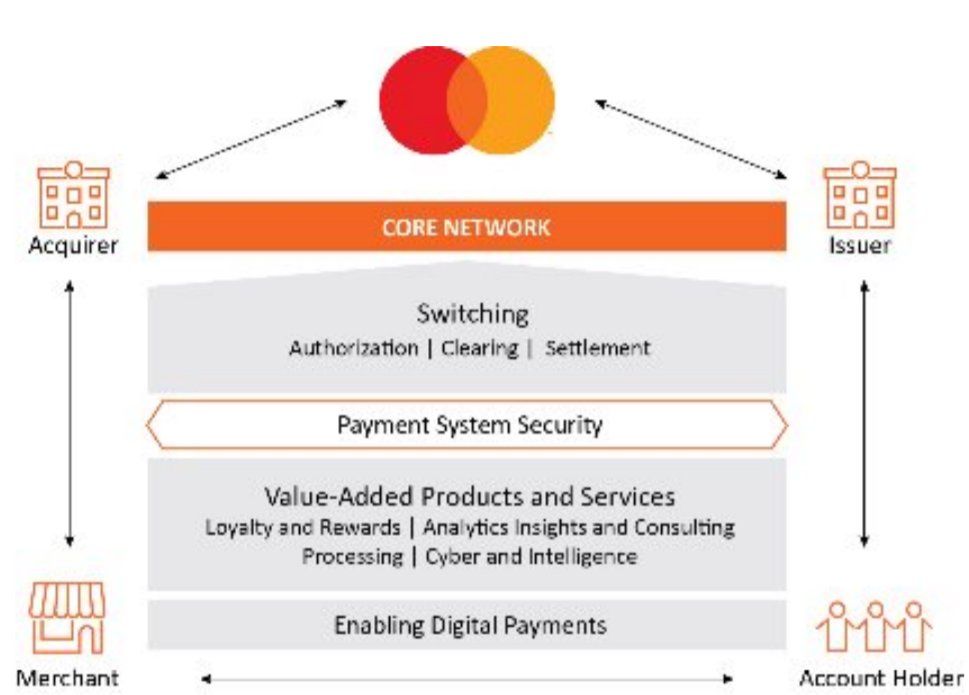

What Mastercard does is to provide the network on which payment transactions can happen. Here’s a graphical representation of Mastercard’s business:

Source: Mastercard 2019 annual report

Let’s imagine you have a Mastercard credit card and you’re buying an item in a supermarket. The transaction will involve five parties: Mastercard; the cardholder (you); the merchant (the supermarket); an issuer (your bank that issued you the credit card); and an acquirer (the supermarket’s bank). The transaction process will then take place in six steps:

- Paying with your Mastercard credit card: You (cardholder) purchase your item from the supermarket (the merchant) with your credit card

- Payment authentication: The supermarket’s point-of-sale system captures your account information and sends it to the supermarket’s bank (the acquirer) in a secure manner.

- Submission of transaction: The supermarket’s bank gets Mastercard to request an authorisation from your bank (the issuer).

- Authorisation request: Mastercard sends information of your transaction to your bank for authorisation.

- Authorisation response: Your bank authorises your transaction and pings the go-ahead to the supermarket.

- Payment to merchant: Your bank sends the payment for your transaction to the supermarket’s bank, which then deposits the money into the supermarket’s bank account.

Mastercard’s revenue comes from the fees it earns when it connects acquirers and issuers. In the first nine months of 2020, Mastercard earned US$11.81 billion in net revenue, which can be grouped into five segments:

- Domestic assessments (US$4.91 billion): Fees charged to issuers and acquirers, based on dollar volume of activity, when the issuer and the merchant are in the same country.

- Cross-border volume fees (US$2.65 billion): Charged to issuers and acquirers, based on dollar volume activity, when the issuer and merchant are in different countries.

- Transaction processing (US$6.35 billion): Revenue that is earned for processing domestic and cross-border transactions and it is based on the number of transactions that take place.

- Other services (US$3.29 billion): Includes services such as data analytics; consulting; fraud prevention, detection, and response; loyalty and rewards solutions; and more.

- Rebates and incentives (-US$6.01 billion): These are payments that Mastercard pays to its customers. Revenues from domestic assessments, cross-border volume fees, transaction processing, and other services collectively make up Mastercard’s gross revenue. We arrive at Mastercard’s net revenue when we subtract rebates and incentives from gross revenue.

With the ability to handle transactions in more than 150 currencies in over 210 countries, it should not surprise you to find that Mastercard has a strong international presence. In the first nine months of 2020, the North American region accounted for just 35% of the company’s total net revenue of US$11.81 billion while international markets collectively accounted for the rest.

Investment thesis

We have laid out our investment framework in Compounder Fund’s website. We will use the framework to describe our investment thesis for Mastercard.

1. Revenues that are small in relation to a large and/or growing market, or revenues that are large in a fast-growing market

On the surface, Mastercard’s business already looks huge. As of 30 September 2020, Mastercard had 2.69 billion cards in issue (under the Mastercard and Maestro brands). The company processed 89.1 billion switched transactions in the 12 months ended 30 September 2020, with a gross dollar volume of US$6.32 trillion; these transactions helped to bring in US$15.60 billion in net revenue for the same period.

But the total market opportunity for Mastercard is immense. According to a November 2019 investor presentation by the company, the size of the payments market is US$235 trillion. From this perspective, Mastercard has barely scratched the surface.

Source: Mastercard November 2019 investor presentation

Prior to the current COVID-19 pandemic, around 80% of transactions in the world were still settled with cash. The pandemic has hurt Mastercard’s business, especially in the cross-border volume fees segment (revenue from the segment fell by 36% year-on-year in the first nine months of 2020) because of decline in travel across the world. But the pandemic’s potential long run impact to Mastercard is positive – it could accelerate the acceptance of digital payment methods over traditional cash. Here are comments on the topic that were shared by Mastercard’s management during the company’s 2020 third-quarter earnings conference call:

“We’re positioning ourselves for the future by driving this accelerated shift toward electronic payments. According to our research, almost seven in 10 people globally say the shift will likely be permanent. We believe that as the economies reopen, people will shop in stores again. But e-commerce will remain elevated from pre-pandemic levels as behaviors have changed and payment preferences have shifted. Our research also shows that about 60% of consumers plan to use less cash even after the pandemic subsides. As a result, merchants are becoming more digital and consumers and businesses are adapting how they interact at the point of sale, both in-person and online.”

Mastercard currently has no domestic operations in China. But this could change in the near future. Last year, Mastercard formed a JV with NetsUnion Clearing Corporation last year to conduct business in China. In February this year, the JV received in-principle approval from China’s central bank to operate in the country. NetsUnion Clearing Corporation’s stakeholders include China’s central bank, the People’s Bank of China. Even without China, we think Mastercard already has ample room for growth. If the China opportunity manifests – and this is far from certain – it would be icing on the cake.

2. A strong balance sheet with minimal or a reasonable amount of debt

As of 30 September 2020, Mastercard has US$10.81 billion in cash and investments on its balance sheet, against US$12.57 billion in debt. This gives rise to a net debt position of US$1.76 billion.

We generally prefer a balance sheet that has more cash than debt. But we’re not troubled at all in the case of Mastercard. This is because the company has an excellent track record in generating free cash flow as we’ll show later. For a preview, the average annual free cash flow generated by Mastercard in 2017, 2018, and 2019 was US$5.03 billion, which compares well with the amount of net-debt the company has.

3. A management team with integrity, capability, and an innovative mindset

There’s a recent management change at Mastercard that we want to comment on. Ajay Banga, 60, has been Mastercard’s CEO since July 2010. We appreciate his long tenure and leadership of the company. And as we’ll show later, Banga has presided over a long period of outstanding growth at Mastercard.

But in February this year, the company announced that Banga will leave the CEO post on 1 January 2021 and assume the Executive Chairman role. Succeeding Banga will be Mastercard’s then-Chief Product Officer, Michael Miebach. Given the timeline involved, this leadership transition seems well-planned and the promotion from within is a positive sign on Mastercard’s culture, in our view. Miebach, who’s relatively young at 52 this year, joined Mastercard in June 2010. Banga has high-praise for Miebach, commenting in the announcement:

“As the company moves into this next phase of growth, we have a deep leadership bench–with Michael at the helm–to take us to the next level. He has a proven track record of building products and running businesses globally.

Over his career, Michael has held leadership positions in Europe, the Middle East and Africa and in the U.S. across payments, data, banking services and technology. During the course of Michael’s 10 years at Mastercard, he has been a key architect of our multi-rail strategy–including leading the acquisition of Vocalink and the pending transaction with Nets–to address a broader set of payment flows. He’s also a visionary who kickstarted much of the work behind our financial inclusion journey.

I am excited to continue working closely with Michael and supporting Mastercard’s success when I become Executive Chairman.”

Miebach looks like a safe pair of hands to us and we note that Banga will still continue to have a say on Mastercard’s future given his upcoming role as Executive Chairman.

On integrity

In 2019, Ajay Banga’s total compensation was a princely sum of US$23.2 million. But it is reasonable when compared with the scale of Mastercard’s business – the company’s profit and free cash flow in the same year were US$8.11 billion and US$5.54 billion, respectively. More importantly, to us, his compensation structure aligns his interests well with those of Mastercard’s shareholders. Here are the important points:

- In 2019, 69.2% of Banga’s total compensation was from performance stock units (PSUs) and stock options that vest over multi-year periods of three years and four years, respectively.

- The PSUs are based on (1) Mastercard’s revenue and earnings per share growth over a three-year period, and (2) changes in Mastercard’s stock price, after adjusting for dividends, over the same timeframe. We emphasised the term “per share” because Mastercard shareholders can only benefit from the company’s growth if there is per-share growth.

- The value of the PSUs and stock options are nearly the same.

- The lion’s share of Banga’s total compensation in 2019 came from components that effectively depend on multi-year changes in both Mastercard’s share price and business performance.

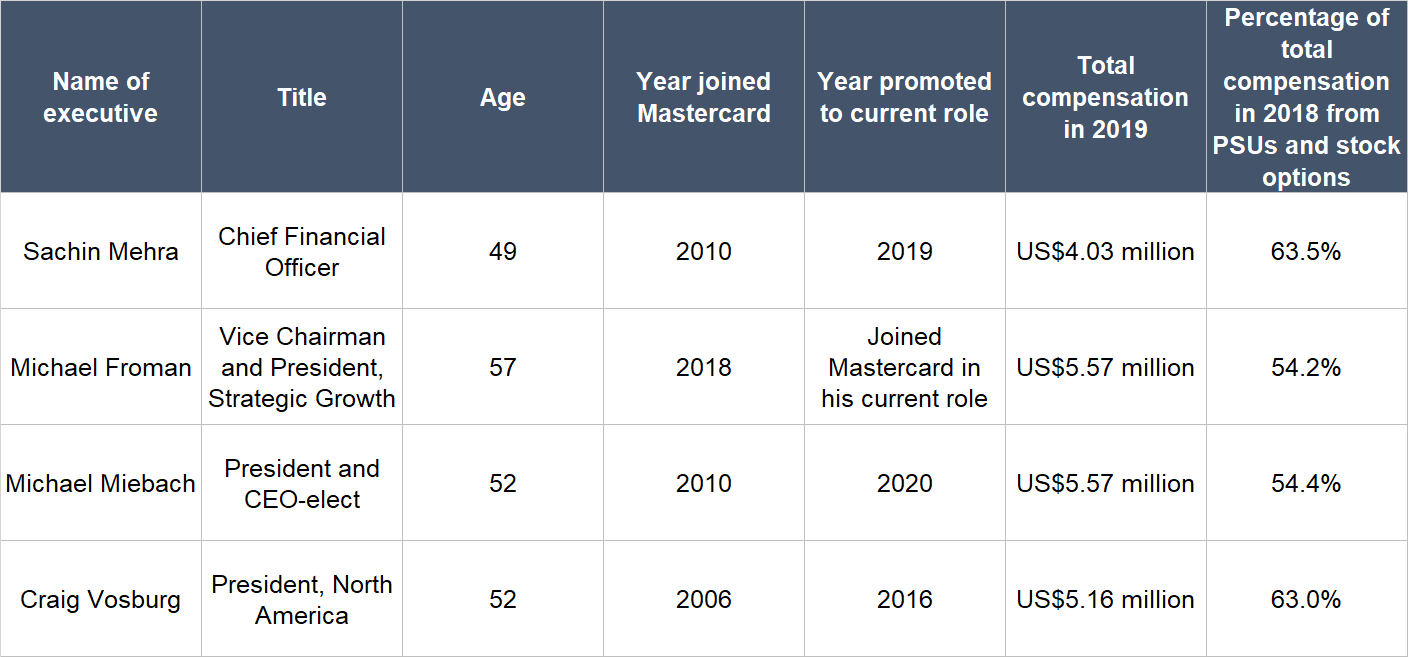

In 2019, the majority of the total compensation of Mastercard’s other key leaders, including Michael Miebach, also came from PSUs and stock options that have the same characteristics as Banga’s (see table below). Moreover, Mastercard’s other key leaders were mostly promoted to their current roles after spending years with the company. The fact that Mastercard regularly promotes from within is another positive sign for us on the company’s culture.

Source: Mastercard 2019 proxy filing

And speaking of alignment of interests, there’s something else we want to highlight: Mastercard has stock ownership guidelines for its key leaders. For 2019, Banga and Miebach were required to own Mastercard shares that are worth at least six and four times their respective base salaries of US$1.25 million and US$625,000 (stock options and any unvested shares do not count). As of 20 April 2020, Banga controlled 1.88 million Mastercard shares which have a value of more than US$637 million at the company’s 1 December 2020 share price of US$339. Meanwhile, Miebach’s stake of 86,176 Mastercard shares is worth north of US$29 million.

On capability and innovation

Mastercard is a digital payment services provider. Some of the key business metrics that showcase the health of its network are: (1) Gross dollar volume, or GDV, of payments that flow through the network; (2) cross-border volume growth; (3) the number of processed transactions; and (4) the number of the company’s cards that are in circulation. The table below shows how the four metrics have grown in each year since 2007. We picked 2007 as the start so that we can understand how Mastercard’s business fared during the 2008-09 Great Financial Crisis.

![]()

Source: Mastercard annual reports and earnings updates

2009 was a relatively rough year for Mastercard, but growth in the company’s key business metrics picked up again quickly. Meanwhile, 2020 has so far been a tough year for the company because of COVID-19. But it turns out that Mastercard’s management has a great overall long-term track record in growing its key business metrics. As mentioned earlier, out-going CEO Ajay Banga had been leading the company since 2010, so the increases in the business metrics from 2007 to 2019 happened mostly under his watch. Prior to being CEO-elect, Miebach was Mastercard’s Chief Product Officer, a role he was promoted to in January 2016. So, Mastercard’s business-growth in the past few years likely also bears Miebach’s fingerprints.

As another positive sign on Mastercard’s culture (we talked about the promotion from within earlier), the company has strong Glassdoor reviews. Glassdoor is a website that allows a company’s employees to rate it anonymously. Currently, 85% of Mastercard-raters on Glassdoor will recommend the company to a friend. Meanwhile, Banga has a 98% approval rating, far higher than the average Glassdoor CEO rating of 69% in 2019.

Coming to innovation, Mastercard’s management has, for many years, been improving the payments-related solutions that it provides to consumers and organisations. This is aptly illustrated by the graphic below, which shows the changes in Mastercard’s business from 2012 to 2018:

Source: Mastercard November 2019 investor presentation

Here are some interesting recent developments by Mastercard:

- Launched Mastercard Track in 2019; Mastercard Track is a B2B (business-to-business) payment ecosystem which helps to automate payments between suppliers and buyers.

- Drove blockchain initiatives in 2019, in the areas of cross-border B2B payments and improving provenance-knowledge in companies’ supply chains.

- Implemented AI-powered solutions to prevent fraudulent transactions and improve fraud detection.

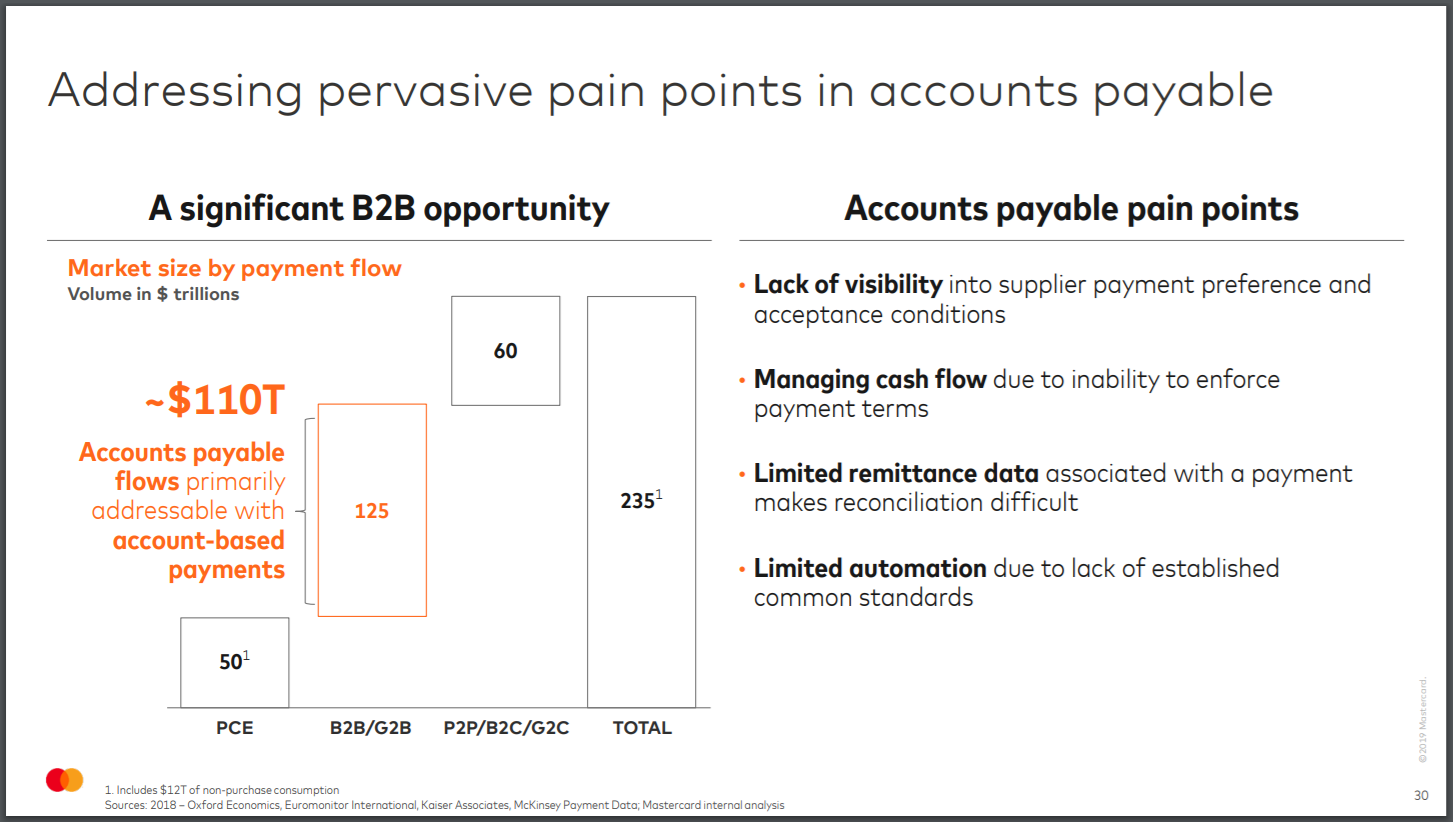

In particular, the B2B opportunity is huge and worth tackling, because companies do encounter many pain-points that are related to payment issues. This is shown in the graphic below.

Source: Mastercard November 2019 investor presentation

4. Revenue streams that are recurring in nature, either through contracts or customer-behaviour

We think that Mastercard is a great example of a company with recurring revenue from customer-behaviour. Each time people make a purchase and pay with a Mastercard credit card, the company takes a small cut of the payment.

We showed earlier that the company handled trillions in dollars worth of payments in 2019, and processed billions in transactions. These numbers, together with the fact that no individual customer accounted for more than 10% of Mastercard’s revenues in 2019, 2018, and 2017, lend further weight to our view that the company’s revenue streams are largely recurring in nature.

Yes, COVID-19 has hurt Mastercard’s business by reducing spending opportunities, especially those related to travel. But when COVID-19 stops becoming a serious global health threat, spending activity should recover, providing the fuel for Mastercard’s growth.

5. A proven ability to grow

The table below shows Mastercard’s important financials from 2007 to 2019:

Source: Mastercard annual reports

A few key points about Mastercard’s financials:

- Net revenue compounded decently at 12.6% per year from 2007 to 2019; over the last five years from 2014 to 2019, the company’s annual topline growth was similar at 12.3%.

- The company also managed to produce net revenue growth in 2008 (22.7%) and 2009 (2.1%); those were the years when the global economy was rocked by the Great Financial Crisis.

- Net profit surged by 18.2% per year from 2007 to 2019. Mastercard’s annual net profit growth from 2014 to 2019 was similarly healthy at 17.5%. Net profit was negative in 2008 because of large legal settlement expenses of US$2.5 billion incurred during the year, but it is not a cause for any concern to us.

- Operating cash flow was consistently positive and grew in most years for the entire time frame we studied. It also increased markedly with growth of 21.8% per year. The growth rate from 2014 to 2019 was still impressive at 19.2% annually.

- Free cash flow, net of acquisitions, was consistently positive too and had stepped up from 2007 to 2019 at a rapid clip of 20.1% per year. The annual growth in free cash flow from 2014 to 2019 was 16.8% – not too shabby. It’s worth noting that Mastercard’s capital expenditure of US$2.6 billion in 2019 is significantly higher compared to the past primarily because of large acquisitions totalling US$1.4 billion. Without the acquisitions, Mastercard’s free cash flow in 2019 would be much higher at US$7.0 billion.

- The net-cash position on Mastercard’s balance sheet was positive from 2007 to 2018 and had dipped into negative territory only in 2019. We mentioned earlier that we’re not troubled by Mastercard currently having more debt than cash, since the company has been adept at producing free cash flow and the amount of net-debt is manageable.

- Mastercard’s diluted share count declined by 24% in total from 2007 to 2019, and also fell in nearly every year over the same period. This is positive for the company’s shareholders, since it boosts the company’s per-share earnings and free cash flow. For perspective, Mastercard’s free cash flow per share compounded at 20.0% per year from 2014 to 2019, which is higher than the annual growth rate of 16.8% over the same period for just free cash flow. Mastercard’s share price has also increased by a stunning 3,120% in total, after adjusting for dividends, from the start of 2007 to the end of 2019. This means that the share buybacks conducted by Mastercard’s management to reduce the share count over the years have been excellent uses of capital.

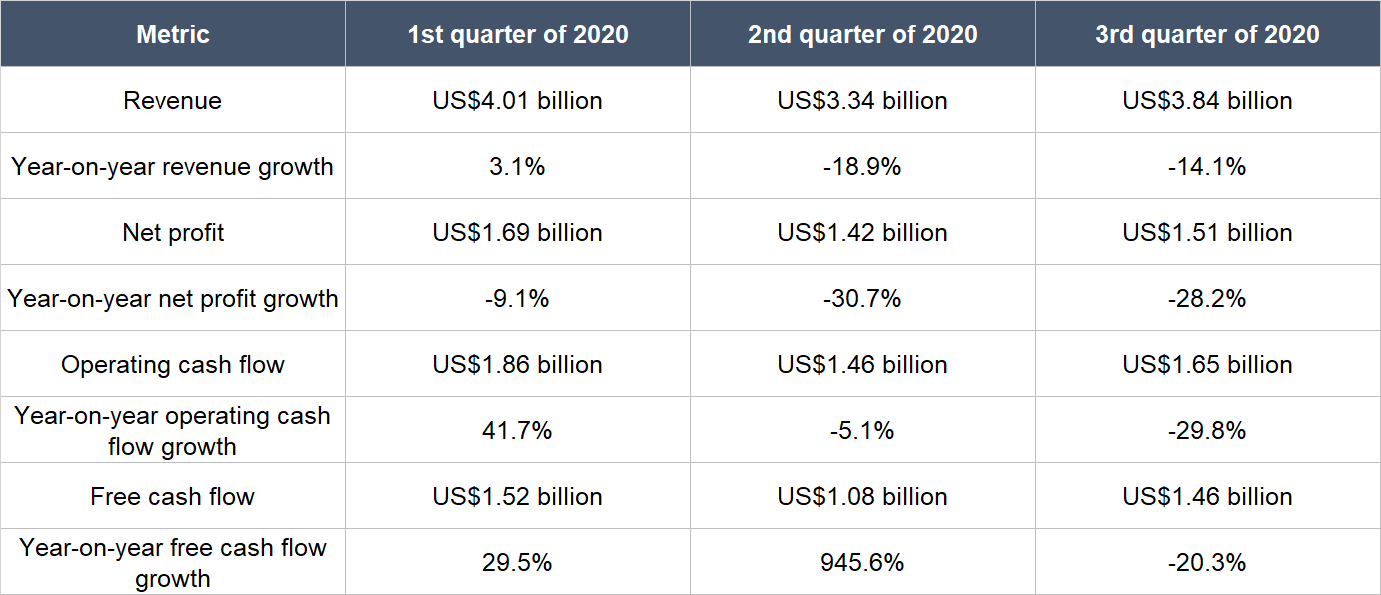

Mastercard has been contending with COVID-19 for much of 2020. The pandemic, as discussed earlier, has hurt the company’s business. This can be seen in the table below, which shows the changes in Mastercard’s revenue, net profit, operating cash flow and free cash flow in the first three quarters of 2020. But we’re looking at the long run here with Mastercard and we think COVID-19 is merely a short-term hiccup for the company.

Source: Mastercard quarterly earnings updates

6. A high likelihood of generating a strong and growing stream of free cash flow in the future

There are two reasons why we think Mastercard excels in this criterion.

First, the company has a long track record of producing strong free cash flow from its business. Moreover, its average free cash flow margin (free cash flow as a percentage of revenue) in the past five years from 2014 to 2019 was strong at 33.5%. In 2019, the free cash flow margin was 32.9%. Even with COVID-19 around in the first nine months of 2020, Mastercard’s free cash flow margin was still an excellent 36.2%.

Two, there’s still tremendous room to grow for Mastercard in the entire payments space. The company has a strong network (the number of currencies it can handle; the number of countries it operates in; the sheer payment and transaction volumes it is processing; the billions in its self-branded credit cards that are circulating) as well as a capable and innovative management team that has integrity. These traits should lead to higher revenue for Mastercard over time. If the free cash flow margin stays fat – and we don’t see any reason why it shouldn’t – that will mean even more free cash flow for Mastercard in the future.

Valuation

We like to keep things simple in the valuation process. In Mastercard’s case, we think the price-to-earnings (P/E) ratio and price-to-free cash flow (P/FCF) ratio are suitable gauges for the company’s value. This is because the company has been adept at producing positive and growing profit as well as free cash flow for a long period of time.

We completed our purchases of Mastercard shares with Compounder Fund’s initial capital in early August 2020. Our average purchase price was US$309 per Mastercard share. At our average price and on the day we completed our purchases, the company’s shares had trailing P/E and P/FCF ratios of around 43 and 45, respectively. These ratios are high relative to their histories. Here’s a chart showing Mastercard’s P/E and P/FCF ratios over the five years ended 1 December 2020:

(Note: The chart above is from Ycharts and the P/FCF ratio excludes the impact of acquisitions.)

But we’re happy to pay up, since Mastercard excels under our investment framework for Compounder Fund. We also want to point out two things. First, Mastercard’s current earnings and free cash flow per share numbers are somewhat depressed because of COVID-19. Second, Mastercard does not just have a large market opportunity – the chance that it can win in its market is also very high, in our view. Put another way, Mastercard scores well in both the magnitude of growth and the probability of growth. For companies like this, we’re more than willing to accept a premium valuation. But the current high P/E and P/FCF ratios mean that an investment in Mastercard carries valuation risk. This is something we are comfortable with.

For perspective, Mastercard carried P/E and P/FCF ratios of around 51 and 53, respectively, at the 1 December 2020 share price of US$339.

The risks involved

There are a few key risks that we see in Mastercard.

First is the aforementioned leadership transition that will happen soon, where Ajay Banga will be handing over the baton to Michael Miebach. We have confidence in Miebach, but we will be keeping an eye on his performance as CEO.

Competition is the second risk we’re watching. We mentioned in our investment thesis for PayPal (a digital payments services provider) that the payments space is highly competitive. There are larger payment networks such as that operated by Mastercard’s competitor and fellow Compounder Fund holding, Visa (the company processed US$8.8 trillion in payments in the 12 months ended 30 September 2020). In our PayPal thesis, we also said:

“Then there are technology companies with fintech arms that focus on payments, such as China’s Tencent and Alibaba. In November 2019, Bloomberg reported that Tencent and Alibaba plan to open up their payment services (WeChat Pay and Alipay, respectively) to foreigners who visit China. Let’s not forget that there’s blockchain technology (the backbone of cryptocurrencies) jostling for room too. There’s no guarantee that PayPal will continue being victorious. But the payments market is so huge that we think there will be multiple winners – and our bet is that PayPal will be among them.”

Just like PayPal, there are no guarantees that Mastercard will continue winning. But we do think the odds are in Mastercard’s favour.

The third risk we have our eyes on is regulations. Payments is a highly regulated market, and Mastercard could fall prey to heavy-handed regulation. Lawmakers could impose hefty fines or tough limits on Mastercard’s business activities. In general, we expect Mastercard to be able to manage any new legal/regulatory cases if and when they come. But we’re paying attention to any changes in the regulatory landscape that could impair the health of Mastercard’s business permanently or for a prolonged period of time.

Fourth is the company’s high valuation. We’re comfortable paying up for Mastercard, but if there are any hiccups in the company’s growth – even if they are temporary in nature – there could be painful falls in the share price. This is a risk we’re comfortable taking as long-term investors.

Lastly, there is the risk of recessions. Mastercard did grow its net revenue in 2009, but the growth rate was low. The current COVID-19 pandemic, and the ensuing global economic contraction, has also hurt the company’s business. We don’t know when a future global recession will happen again. But when it does, payment activity on Mastercard’s network could be lowered.

Summary and allocation commentary

To wrap up, Mastercard excels under our investment framework:

- The payments market is worth a staggering US$235 trillion and Mastercard has barely scratched the surface.

- The company currently has more debt than cash, but the net-debt level is manageable and the company has a long history of producing strong free cash flow.

- Mastercard’s management team has proved itself to be innovative and capable, but that’s not all – the company’s leaders also have sensible compensation structures that align their interests with shareholders.

- Mastercard’s revenue streams are highly likely to be recurring in nature (each time we make a payment with a Mastercard service or product, the company gets a cut of the transaction).

- The company has a long history of growing its net revenue, profit, and free cash flow, while keeping its balance sheet strong and reducing its share count.

- There is a high likelihood that Mastercard will continue to be a free cash flow machine.

The company does have a high valuation – both in absolute terms and in relation to history. But we have no qualms with accepting a premium valuation for a high-quality business. The other risks to our Mastercard investment includes the leadership transition that’s happening soon; the tough competitive landscape; the potential for regulatory changes to harm the company’s business; and recessions.

After weighing the pros and cons, we initiated a 2.5% position – a medium-sized allocation – in Mastercard with Compounder Fund’s initial capital. We appreciate all the positives that we see in Mastercard. But our enthusiasm is slightly tempered by the fact that Mastercard’s revenue increased at only a mid-teens annual rate for the past 10-plus years, and so the company is unlikely to exhibit hypergrowth in the future. We prefer to have faster-growing companies to be larger positions in the portfolio.

And here’s an important disclaimer: None of the information or analysis presented is intended to form the basis for any offer or recommendation; they are merely our thoughts that we want to share. Of all the companies mentioned in this article, Compounder Fund also currently owns shares in PayPal, Tencent, and Visa. Holdings are subject to change at any time.