Compounder Fund: Facebook Investment Thesis - 17 Sep 2020

Data as of 14 September 2020

Facebook Inc (NASDAQ: FB) is one of the 40 companies in Compounder Fund’s initial portfolio. This article describes our investment thesis for the company.

Company description

Co-founded by Mark Zuckerberg in 2004, Facebook has in the space of just 16 years become one of the largest companies in the world with a market capitalisation of US$758 billion.

Most of you reading this will likely know about Facebook’s eponymous free-to-use social media platform, so we won’t describe its features in detail (future references to the social media platform in this article will be given in italics). In short, Facebook allows users to connect with friends and/or family, post pictures and videos, and view content from their connections or other users they follow, through mobile devices and/or computers.

There’s more to Facebook. Here are the company’s four other key products:

- Instagram: Facebook acquired Instagram in 2012 for US$1 billion in cash and shares. Instagram is an app for people to share photos and videos with their followers or the public.

- Messenger: A messaging app for users to connect with friends, family, groups, and businesses across platforms and devices.

- WhatsApp: A mobile messaging platform for users to message anyone on the app using their registered phone number. Facebook bought Whatsapp in 2014, paying US$4.6 billion in cash and 178 million shares (worth around US$13.8 billion then).

- Oculus: Oculus is Facebook’s hardware, software, and developer ecosystem for virtual reality products. It was acquired by Facebook in the same year as the Whatsapp purchase for around US$400 million in cash and 23 million shares (worth around US$1.6 billion then).

In 2019, Facebook pulled in US$70.7 billion in revenue and nearly all of it (some US$69.7 billion) came from the company selling advertising placements on its products to marketers. Advertisers purchase ads from Facebook that can appear in multiple places including Facebook, Instagram, Messenger, as well as third-party applications and websites.

Facebook is a geographically diverse business. In 2019, the US and Canada collectively accounted for 45.6% of the company’s total revenue. Europe (23.8%) and Asia Pacific (21.8%) are the next two largest regions for Facebook. Other countries in the world made up the remaining 8.9% of revenue.

Investment thesis

We have laid out our investment framework in Compounder Fund’s website. We will use the framework to describe our investment thesis for Facebook.

1. Revenues that are small in relation to a large and/or growing market, or revenues that are large in a fast-growing market

Facebook is the world’s largest social media company. As of 30 June 2020, there were 1.785 billion daily active users on Facebook. The total number of unique persons on the company’s family of apps – termed “Family Daily Active People” – was 2.47 billion. There are also more than 9 million active advertisers across its services. These are staggering numbers. For perspective, the global population is currently 7.8 billion. We don’t expect Facebook to be able to grow its user-base at a rapid clip going forward. But we think there’s still an opportunity for Facebook to expand its user base and create more value for advertisers to market on the company’s family of apps. As ubiquitous as the internet is for those of us living in Singapore, plenty of people in other countries have yet to experience the web. Worldwide, there are only 4.6 billion internet users today, according to Statista.

In the 12 months ended 30 June 2020, Facebook’s revenue was US$75.2 billion. Again, this is a massive number, but it’s still relatively small when compared to the size of the overall advertising market. According to Magna, the global advertising market is expected to decline by 7% in 2020 but still come in at US$540 billion. Within the global advertising market is digital advertising, which is expected to be US$302 billion this year, effectively flat from 2019. It’s worth noting that the global digital advertising space is fast-growing, having doubled from US$88 billion in 2012 to US$181 billion in 2016 according to data from Zenith (growth is slow this year because of COVID-19).

We believe digital advertising is more effective than advertising done over other media platforms. In the case of Facebook, the company holds a wealth of information about its avid users. Using Facebook ads, advertisers are able to narrow down their target audience by demographics, location, interests, and behaviour. This provides a better experience and return on investment for advertisers compared to many other forms of advertising.

We also think Facebook is one of those rare companies that are creating tailwinds (the boom in digital advertising) rather than merely riding them. In fact, Facebook has democratised access to advertising for even the smallest businesses. CEO Mark Zuckerberg recently commented in a statement for US lawmakers:

“Facebook gives small businesses and individual entrepreneurs access to sophisticated tools that previously only the largest players had. Now any business can use our services to establish an online presence, reach potential customers and grow.”

Although Facebook has long depended on advertising for effectively all its revenue (and still does so today), we wouldn’t be surprised if the company grows new wings in the future. For instance, the company is active in exploring payments-related businesses. In mid-2019 Facebook announced its plans to launch its own cryptocurrency called Libra, although we do note that the initiative has since faced significant regulatory resistance. Then in late 2019, Facebook launched a payments service – Facebook Pay – that works across its family of apps (Facebook, Messenger, Instagram, and WhatsApp). In June this year, Facebook used Facebook Pay’s infrastructure to roll out payments services for WhatsApp in Brazil. It is the first time WhatsApp has launched payments and although Brazil’s central bank suspended the feature just a week after it was introduced (Facebook is currently working with Brazilian regulators to resolve the problems), it will still be interesting to watch Facebook’s developments in the payments space given the wide reach of its family of apps.

Sticking with WhatsApp, the app’s huge network – it commands 2 billion users (based on data from February 2020), up from 1 billion just four years ago – also gives Facebook optionality for other types of services to be layered on. Motley Fool co-founder David Gardner describes optionality as a company having multiple paths to grow. WhatsApp launched a version of its messaging app that is targeted for businesses – WhatsApp Business – in early 2018. WhatsApp Business allows businesses to easily communicate with customers. Today, there are over 50 million users of WhatsApp Business and the user base is “growing quickly,” according to Zuckerberg in a recent Facebook earnings conference call. And speaking of business-users, it’s worth noting too that Facebook launched Facebook Shops in May this year. Facebook Shops is a digital storefront that businesses can set up for free in minutes, and it works across both Facebook and Instagram. In all, there are more than 180 million businesses that use Facebook’s plethora of tools each month.

Then there’s also the Metaverse as a potential opportunity for Facebook. In an excellent recent blog post of his, Matthew Ball, a venture capitalist and media-business analyst, describes the Metaverse as having the following qualities:

“The Metaverse, we think, will…

1. Be persistent – which is to say, it never “resets” or “pauses” or “ends”, it just continues indefinitely

2. Be synchronous and live – even though pre-scheduled and self-contained events will happen, just as they do in “real life”, the Metaverse will be a living experience that exists consistently for everyone and in real time

3. Have no real cap to concurrent participations with an individual sense of “presence” – everyone can be a part of the Metaverse and participate in a specific event/place/activity together, at the same time and with individual agency

4. Be a fully functioning economy – individuals and businesses will be able to create, own, invest, sell, and be rewarded for an incredibly wide range of “work” that produces “value” that is recognized by others

5. Be an experience that spans both the digital and physical worlds, private and public networks/experiences, and open and closed platforms

6. Offer unprecedented interoperability of data, digital items/assets, content, and so on across each of these experiences – your “Counter-Strike” gun skin, for example, could also be used to decorate a gun in Fortnite, or be gifted to a friend on/through Facebook. Similarly, a car designed for Rocket League (or even for Porsche’s website) could be brought over to work in Roblox. Today, the digital world basically acts as though it were a mall where though every store used its own currency, required proprietary ID cards, had proprietary units of measurement for things like shoes or calories, and different dress codes, etc.

7. Be populated by “content” and “experiences” created and operated by an incredibly wide range of contributors, some of whom are independent individuals, while others might be informally organized groups or commercially-focused enterprises”

Put simply, the Metaverse is something like a pervasive digital world that is interlinked with the real world. And the economic opportunities may be immense. In the same blog post we referenced just above, Ball wrote:

“Even if the Metaverse falls short of the fantastical visions captured by science fiction authors, it is likely to produce trillions in value as a new computing platform or content medium. But in its full vision, the Metaverse becomes the gateway to most digital experiences, a key component of all physical ones, and the next great labor platform.”

Facebook may be able to play a role in building the Metaverse and we’re watching the company’s developments in this area with keen interest. Here’s Ball on Facebook’s Metaverse angle from the same blog post again (note the reference to Oculus):

“Although Facebook CEO Mark Zuckerberg has not explicitly declared his intent to develop and own the Metaverse, his obsession with it seems fairly clear. And this is smart. More than any other company, Facebook has the most to lose from the Metaverse as it will build an even larger and more capable social graph and represent both a new computing platform and a new engagement platform. At the same time, the Metaverse also allows Facebook to extend its reach up and down the stack. Despite several efforts to build a smartphone OS and deploy consumer hardware, Facebook remains the one FAAMG company stuck purely at the app/service layer. Through the Metaverse, Facebook could become the next Android or iOS/iPhone (hence Oculus), not to mention a virtual goods version of Amazon [Compounder Fund also owns Amazon shares].

Facebook’s Metaverse advantages are immense. It has more users, daily usage and user-generated content created each day than any other platform on earth, as well as the second largest share of digital ad spend, billions in cash, thousands of world-class engineers, and conviction from a founder with majority voting rights. Its Metaverse-oriented assets are also growing rapidly and now include patents for semiconductor and brain-to-machine computing interfaces. At the same time, Facebook has a very troubled track record as a platform for where third-party developers/companies can build sustainable businesses, as a ringleader in a consortium (e.g. Libra), and in managing user data/trust.”

2. A strong balance sheet with minimal or a reasonable amount of debt

Facebook ticks this box easily. In fact, we will say that Facebook’s balance sheet is like a fortress. As of 30 June 2020, Facebook had US$58.2 billion in cash and marketable securities while carrying zero debt. The company does have operating lease liabilities, but they were merely US$10.5 billion.

It also helps that Facebook has been consistently generating strong free cash flow over the years (more on this later).

3. A management team with integrity, capability, and an innovative mindset

On integrity

As we mentioned earlier, Facebook’s CEO is Mark Zuckerberg, who is currently only 35 years old. He has been running the company since its birth in 2004.

We appreciate founder-led companies (although to be clear, we do not exclusively invest in founder-led companies). Founders are often guided by a sense of purpose and drive to see their brainchild succeed. A March 2016 article by business consultancy Bain & Company cited a study by three business professors – Lee Joon Mahn, Kim Jongsoo, and Bae Joonhyung – that was published earlier in the year and mentioned that “companies where the founder is still CEO are more innovative, generate 31% more patents, create patents that are more valuable, and are more likely to make bold investments to renew and adapt the business.”

Facebook is founder-led, and we also appreciate the fact that despite Zuckerberg’s young age, he already has 16 years of leadership-tenure at the company. (The other co-founders of Facebook are Dustin Moskowitz, Chris Hughes, and Eduardo Saverin.)

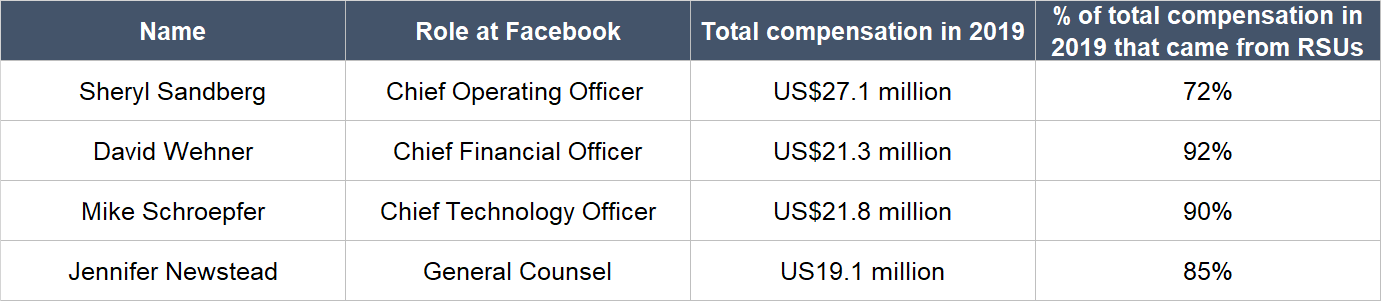

We also think that Facebook’s compensation structure shows that (1) Zuckerberg is a leader with integrity and (2) the interests of the company’s management team and shareholders are well aligned. On the first point, there are three things we want to highlight:

- Zuckerberg has been drawing a US$1 salary since 2013. During a Q&A session on Facebook in 2015, Zuckerberg said: “I’ve made enough money. At this point, I’m just focused on making sure I do the most possible good with what I have. The main way I can help is through Facebook — giving people the power to share and connecting the world. I’m also focusing on my education and health philanthropy work outside of Facebook as well. Too many people die unnecessarily and don’t get the opportunities they deserve. There are lots of things in the world that need to get fixed and I’m just lucky to have the chance to work on fixing some of them.”

- Zuckerberg does not get any bonus or stock awards too, because Facebook’s board believes that he is already appropriately incentivized due to his large stake in Facebook. As of 31 May 2020, Zuckerberg has economic ownership of 367.87 million Facebook shares. These shares are worth a staggering US$97.9 billion at the share price of US$266 on 14 September 2020.

- Zuckerberg’s total compensation in 2019 was US$23.4 million if personal security expenses are included. This is a princely sum, but it’s a rounding error when compared to Facebook’s profit of US$18.49 billion in the same year.

On the second point, Facebook’s other key leaders all saw the lion’s share of their total compensation in 2019 come from restricted stock units (RSUs) that vest over four years – this is shown in the table below. We like seeing compensation plans that are tied to the long-term performance of a company’s share price, since it is the company’s business performance which drives the share price over the long run.

Source: Facebook 2019 Proxy Statement

We want to highlight that 99% of the shares held by Zuckerberg are of the Class B variety. Facebook has two share classes: (1) Class B, which are not traded and hold 10 voting rights per share; and (2) Class A, which are publicly traded and hold just 1 vote per share. Zuckerberg only controlled 12.9% of Facebook’s total shares as of 31 May 2020, but he held 53.1% of the company’s voting power. A manager having virtually complete control over the company can potentially be bad for shareholders. This concentration of Facebook’s voting power in the hands of Zuckerberg means that we need to be comfortable with him at the company’s helm. We are.

Although Zuckerberg’s philanthropic actions are not directly-related to investing, we think they do shine a positive light on the character of Facebook’s most prominent co-founder. Zuckerberg and his wife, Priscilla Chan, set up the Chan Zuckerberg Initiative (CZI) in 2015 after the birth of their daughter. At the same time, Chan and Zuckerberg also pledged to give 99% of their Facebook shares during their lives to advance CZI’s mission “to build a more inclusive, just, and healthy future for everyone.”

On capability and ability to innovate

We rate Facebook’s leadership team highly in terms of capability and innovation and there are a few things we want to discuss (in no particular order).

First, as already mentioned, Facebook is one of those rare companies that are creating tailwinds (the boom in digital advertising) rather than merely riding them. The company is democratising access to advertising services – for as low as a few dollars, advertisers are able to reach their target audiences on Facebook’s platforms. We think this opens up a whole new demand for advertising that previously did not exist. A strong supporting datapoint: Facebook has a significantly more diversified customer base than traditional media. For example, in the second quarter of 2020, the top 100 advertisers on Facebook’s platforms represented just 16% of its total advertising revenue; in comparison, the top 200 advertisers made up almost 80% of all broadcast network TV advertising, according to a Leading National Advertisers report from 2015. We think this difference in customer-concentration can only appear if Facebook is able to serve the long-tail of advertising-demand that can’t afford the typically high costs of advertising on traditional media.

Second, there’s Facebook’s impressive shift from desktop advertising to mobile advertising. In the third quarter of 2012, only 12.0% of Facebook’s quarterly revenue of US$1.26 billion came from mobile advertising. By the second quarter of 2017, mobile advertising made up 85.5% of Facebook’s total quarterly revenue of US$9.32 billion. We have reason to believe that mobile advertising accounts for the sheer majority of Facebook’s revenue today, since “substantially all” of Facebook’s daily and monthly active users access the social media platform on mobile devices. In a mobile dominated world (when it comes to the internet, users spent nearly double the time on mobile than on desktops in 2018, according to data from Mary Meeker’s Internet Trends 2019 report), getting the right mobile strategy is crucial.

Third is the substantial increases over the years in Facebook’s user base (Faecbook’s daily active user count) and average revenue per user across all the company’s geographies. These are illustrated in the tables below:

Source: Facebook earnings presentations

Fourth, Zuckerberg appears to have built a great corporate culture at Facebook. The company was ranked Number 1 on Glassdoor’s annual list of “Best Places to Work” three times out of the last 10 years (in 2011, 2013, and 2018). In 2019 and 2020, Facebook was ranked 7th and 23rd, respectively. Glassdoor is a platform that allows employees to rate their companies anonymously. Currently, 90% of Facebook-raters on Glassdoor will recommend the company to a friend. Meanwhile, Zuckerberg has a 94% approval rating as CEO, far higher than the average Glassdoor CEO rating of 69%. We’re aware that in June this year, there was employee-unhappiness at Facebook over Zuckerberg’s stance back then on inflammatory remarks on race issues made by US President Donald Trump on the company’s platforms (Zuckerberg opted not to do anything about them, but appears to have reversed course in recent weeks). But we think the evidence still points toward a fantastic workplace environment and culture at Facebook, in aggregate.

Fifth, Facebook has in recent years been plagued with regulatory concerns and public pressure regarding the appearance of harmful content on its platforms. To counter these, Facebook has spent billions in technology, pioneering the use of artificial intelligence to scan its platforms to remove hateful content at scale. In Facebook’s 2020 second-quarter earnings update, Zuckerberg gave more context:

“Our AI systems already proactively identify about 90% of hate speech we remove before anyone reports it – no other internet service does anything remotely as sophisticated as this – and we are committed to continuing to improve. We’re having an independent audit done of our Community Standards Enforcement Report, which is our transparency report on how effectively we’re removing harmful content. We’re also opening ourselves up to an audit from the Media Rating Council to look at our content monetization policies and brand safety controls, and we’re going to work with the Global Alliance for Responsible Media to provide greater transparency into our measurement of hate speech numbers.”

Sixth, there’s Facebook’s initiatives outside of digital advertising – such as the metaverse, business communications and payments services, and digital shops – that we talked about when we discussed the company’s market opportunity earlier. Not all of these will work, but at least the company is trying.

Seventh, although there has been plenty of controversy surrounding Zuckerberg and Facebook in recent years as we had pointed out earlier, we think that he is genuinely trying to build a company that has a purpose beyond profit. In Facebook’s IPO prospectus, Zuckerberg included a shareholders’ letter (see page 80 of the document) that is a tour-de-force on the topic. Here’s just one excerpt on the point:

“As I said above, Facebook was not originally founded to be a company. We’ve always cared primarily about our social mission, the services we’re building and the people who use them. This is a different approach for a public company to take, so I want to explain why I think it works.

I started off by writing the first version of Facebook myself because it was something I wanted to exist. Since then, most of the ideas and code that have gone into Facebook have come from the great people we’ve attracted to our team.

Most great people care primarily about building and being a part of great things, but they also want to make money. Through the process of building a team — and also building a developer community, advertising market and investor base — I’ve developed a deep appreciation for how building a strong company with a strong economic engine and strong growth can be the best way to align many people to solve important problems.

Simply put: we don’t build services to make money; we make money to build better services.”

We reserve the right to be wrong, but we believe in Zuckerberg’s letter.

Eighth, we think Facebook’s management has made some astute capital allocation decisions. In April 2012, shortly before Facebook had its IPO in May, the company inked a deal to acquire photo-sharing app Instagram for what was then worth US$1 billion in cash and Facebook shares. Fast forward to today, and Instagram has become an increasingly important part of its overall business. Although Facebook still does not reveal Instagram’s official financials, Bloomberg reported earlier this year that Instagram generated US$20 billion in revenue in 2019. When the acquisition was first revealed, it was shocking to some that Facebook had acquired Instagram for US$1 billion. At that time, Instagram had only 13 employees, and it had raised private funding at a US$500 million valuation just days before Facebook came into the picture. But given the size of Instagram’s business today, we think the investment has already provided huge – and growing – returns for Facebook.

Ninth, we’re impressed by the commitment of Mark Zuckerberg to invest heavily but responsibly in Facebook’s growth and to keep up with hiring despite the current economic uncertainty because of the COVID-19 pandemic. We think this is a great mentality to have and will be to the long-term benefit of Facebook. For perspective on Facebook’s hiring, in the second quarter of 2020, the company added 4,200 net new employees – its highest ever number of net additions – to end the quarter with a total headcount of 52,500. Here’s the relevant comment Zuckerberg gave in Facebook’s 2020 first-quarter earnings conference call:

“I’ve always believed that in times of economic downturn the right thing to do is keep investing in building the future. I believe this for a few reasons. First, when the world changes quickly, people have new needs and that means there are more new things to build. Second, since many big companies will pull back on investments, there are a lot of things that wouldn’t otherwise get built that we can help deliver. And third, I believe there is a sense of responsibility and duty to invest in the economic recovery and to provide stability for your community and stakeholders if you have the ability to do so. We’re in a fortunate position to be able to do this. Along with our strong financial position and the important social value our services provide, we’re planning to hire at least 10,000 more people in product and engineering roles this year so we can continue building and making progress.

That said, with advertisers spending less and our business performance below previous expectations, we do plan to moderate some areas of our expense growth, especially in business functions. We accept that our profit margins will decrease this year as we continue investing, and Dave will share more on our financial outlook in a few minutes. But this economic pullback has certainly reinforced for me the importance of maintaining high margins. Our financial position has allowed us to continue investing in building products and making investments like our partnership with Jio even when the underlying economic conditions are challenging.”

4. Revenue streams that are recurring in nature, either through contracts or customer-behaviour

We think Facebook’s revenue streams are highly recurring in nature through customer-behaviour for a few reasons.

First, Facebook’s advertising services appear to be robust or even antifragile to us. Antifragility is a term introduced by Nassim Taleb, a former options trader and the author of numerous books including Black Swan and Antifragile. Taleb classifies things into three groups:

- The fragile, which breaks when exposed to stress (like a piece of glass, which shatters when dropped)

- The robust, which remain unchanged when stressed (like a football, which does not get affected much when kicked or dropped)

- The antifragile, which strengthens when exposed to stress (like our human body, which becomes stronger when we exercise)

Here’s business-writer extraordinaire Ben Thompson explaining the potentially-antifragile nature of Facebook’s advertising services in an article discussing the company’s 2020 first-quarter results from his excellent newsletter Stratechery:

“That first bit gets at the other thing the Wall Street Journal article got wrong: it is not simply that direct response stayed strong while brand advertising declined, but rather that Facebook actually received more direct response advertising because brand advertising declined…

Notice, though, what happens in a situation like the coronavirus crisis, where a segment of advertisers competing for limited inventory stop buying ads: the mobile gaming company doesn’t reduce their budget — to do so would be to kill the company! — but in fact ends up getting more efficient spend. Suddenly the clearing price for the auction to show those app install ads is $0.75 per app install; now the mobile gaming company is getting 26,667 app installs for its $20,000 spend, which results in an expected profit of $6,667.

This does, obviously, entail downside for Facebook — that extra ~$6,000 in profit is out of Facebook’s pocket — but at the same time the loss is capped because not only is the mobile gaming company not reducing its spend, it is in fact incentivized to increase its spend given the reduced competition and thus increased profitability for its ads. And, of course, as that opportunity is seized on by more and more companies, Facebook’s profits, which in the end are gated by the amount of inventory it has, not only return to normal but arguably have more upside, given that usage of the platform is increasing.”

(Direct response advertising refers to advertising that is meant to drive an immediate customer response. Meanwhile, brand advertising is known as delayed response advertising and is intended to build up brand image and the value of a company’s product.)

Here’s another datapoint supporting our view on the robustness of Facebook’s services: In the second quarter of 2020, during the height of the COVID-19 lockdown in the US, Facebook’s total revenue grew 10.7% from a year ago to US$18.69 billion; in contrast, US GDP fell by 9.1% in the same quarter and Alphabet’s revenue was effectively flat. Alphabet, which is also in Compounder Fund’s initial portfolio, is the parent company of internet search giant Google and also depends on digital advertising as its main source of revenue.

Second, Facebook has a very diverse customer base, so there’s no customer concentration. We mentioned earlier that the company has 9 million advertising customers, and that the top 100 advertisers only accounted for 16% of total revenue in the second quarter of 2020.

Third, Facebook has a long history of growing its daily-active-user count, and to us, this is a sign that users are actively engaging with Facebook. This is important because a high level of user-engagement gives advertisers more reasons to use Facebook’s apps as an advertising platform, which in turn strengthens the recurrence of Facebook’s revenue.

5. A proven ability to grow

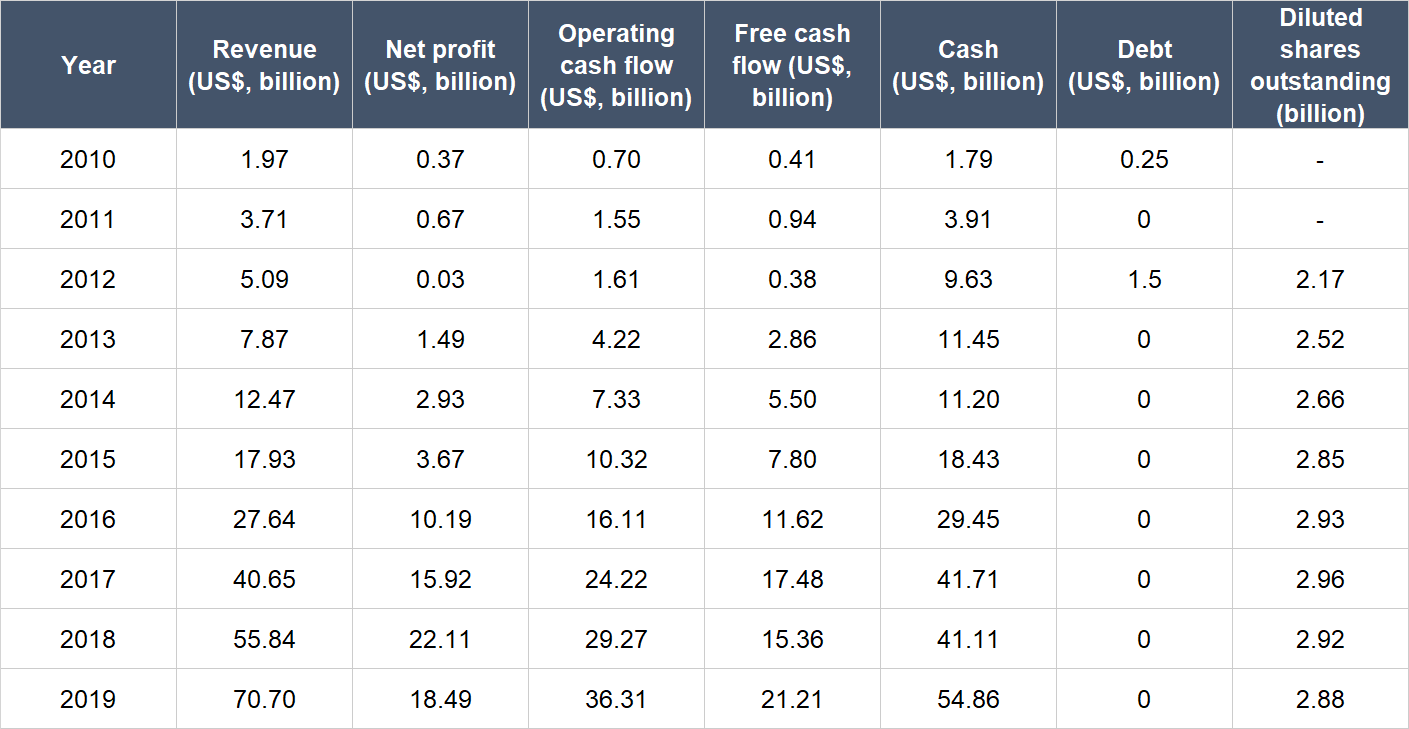

The table below shows Facebook’s important financial figures from 2010 to 2019:

Source: Facebook annual reports

A few key points about Facebook’s financials:

- Revenue has compounded impressively at 48.8% per year from 2010 to 2019. Over the past five years (2014 to 2019), annual growth was still excellent at 41.5%. In 2019, the growth rate decelerated, but was still strong at 26.7%.

- For the entire time period under study, profit had been consistently positive and had compounded at 54.3% per year. From 2014 to 2019, the growth rate was still high at 44.6%. In the first half of 2019, Facebook recorded a US$5 billion fine from the Federal Trade Commission (FTC). This is a one-off expense. Excluding this, net profit for the whole of 2019 would have been around US$23 billion. Moreover, Facebook’s 2019 profit was also impacted by a higher effective tax rate of 25.5% compared to 12.8% in 2018. For perspective, Facebook’s effective tax rate in the first half of 2020 is 16%, so the 25.5% tax rate in 2019 is anomalously high. We also note that Facebook had a huge decline in profit in 2012 but it’s nothing to worry about: There was a significant one-time increase in stock-based compensation (an expense) because of Facebook’s IPO during the year.

- Both Facebook’s operating cash flow and free cash flow were consistently positive and exhibited strong growth. Operating cash flow grew by 55.1% per year from 2010 to 2019, 37.7% per year from 2014 to 2019, and 24.0% in 2019. Facebook’s free cash flow also had similar annual growth rates for the selfsame time periods: 55.2% from 2010 to 2019; 31.0% from 2014 to 2019; and 38.1% in 2019.

- The balance sheet was rock-solid throughout with debt either being much lower than cash or at zero.

- Facebook has not been diluting shareholders in any noticeable way, since the share count has only increased slightly by 3.2% per year from 2012, the year of Facebook’s listing. Moreover, Facebook’s share count actually fell in both 2018 and 2019.

The first half of 2020 saw Facebook continue to grow its business, as illustrated in the table below. (Note that the operating cash flow and free cash flow figures for the second quarter of 2020 seen below are adjusted for the FTC fine of US$5 billion that was paid in April 2020.) The growth rates are significantly slower than what Facebook has achieved in the past, but we think they’re still healthy when considering the global economic uncertainties caused by COVID-19.

Source: Facebook quarterly earnings updates

6. A high likelihood of generating a strong and growing stream of free cash flow in the future

We believe Facebook scores well in this criterion for two key reasons.

First, it’s likely that Facebook will be able to grow its business at a strong pace for years into the future. As already mentioned, Facebook’s core market of digital advertising still has legs to run, and the company has other potential avenues for growth, such as in payments, e-commerce and the Metaverse.

Second, Facebook has done very well in producing free cash flow from its business for a long time. Its average free cash flow margin (free cash flow as a percentage of revenue) was 38.4% from 2014 to 2019, and the figure came in at 35.9% in the first half of 2020 after adjusting for the aforementioned US$5 billion FTC fine.

Valuation

We completed our purchases of Facebook shares with Compounder Fund’s initial capital in late July 2020. Our average purchase price was US$238 per Facebook share. At our average price and on the day we completed our purchases, both the trailing price-to-earnings (P/E) and price-to-free cash flow (P/FCF) ratios of Facebook were around 30, after adjusting for the US$5 billion FTC fine. We like to keep things simple in the valuation process. In Facebook’s case, we think the P/E and P/FCF ratios are appropriate metrics to value the company, since the company has a long history of producing solid and growing streams of profit and free cash flow.

To us, Facebook is a company with a large and growing market opportunity as well as a high probability of being able to enjoy strong growth in the years ahead (we think Facebook’s earnings and free cash flow will likely grow at double-digit annual rates). With these traits, a P/E and P/FCF ratio of 30 each is very reasonable, in our view. History is also on our side. The chart below shows Facebook’s P/E and P/FCF ratios in the five years ended 14 September 2020 and you can see that 30 is not high compared to where the two valuation metrics have been in the past.

(The numbers in the chart above are not adjusted for the FTC fine.)

For perspective, Facebook carried P/E and P/FCF ratios of around 33 and 32, respectively, at the 14 September 2020 share price of US$266.

The risks involved

We see four main threats to our investment thesis for Facebook.

The first is regulatory risk. Facebook has faced growing scrutiny among regulators over the years. As mentioned earlier, Facebook recorded a US$5 billion penalty from the FTC in 2019. This was because of privacy issues. In addition to the penalty, Facebook was required to enhance its privacy compliance and oversight measures. There is also the risk that regulators may slap more fines on Facebook or more importantly, force Facebook to change its business operations. In July this year, Mark Zuckerberg had to testify before US lawmakers on antitrust issues, and Facebook is still currently under investigation by antitrust regulators.

From our standpoint, Facebook’s ability to offer targeted ads sets it apart from other advertising platforms, and in fact, benefits many small businesses. If Facebook is forced to change its advertising services, then the value it brings to advertisers may be materially impacted. There is also the risk that regulators may force Facebook to break up its business (such as by spinning off Instagram). We are keeping a keen eye on regulatory changes that concern Facebook. Here’re important comments on the topic of regulation that Zuckerberg shared during Facebook’s 2020 second-quarter earnings conference call:

“Our advertising is one of the most effective tools that small businesses have to find customers, to grow their businesses, and to create jobs… It’s true that making it more difficult to target ads would affect the revenue of companies like Facebook. But the much bigger cost of such a move would be to reduce the effectiveness of the ads and opportunities for small businesses to grow. This would reduce opportunities for small businesses so much that it would probably be felt at a macro-economic level. Is that really what policymakers want in the middle of a pandemic and recession? The right path, I believe, is regulation that keeps people’s data safe while allowing the benefits of this kind of personalized and relevant advertising.”

The second is key man risk. We see Zuckerberg as the key person (and to a lesser extent, COO Sheryl Sandberg) who has overseen Facebook’s success. He is only 35 years old and likely has many years ahead of him to continue leading the company. But if he leaves the CEO role for whatever reason, his successor will have big boots to fill and we will be watching the leadership transition.

The third is competition. User engagement is the most important component of Facebook’s business. High user engagement on Facebook’s platforms make them attractive to advertisers. So far, Facebook’s active user base has grown each year, but competition for users’ attention is extremely high. Social media apps such as TikTok and Snapchat are increasingly popular among the younger generation. Facebook’s family of apps still dominate the social media space, but we’re watching for negative impacts to Facebook’s business from its rivals.

The fourth is negative publicity. Facebook is under intense public scrutiny because of it being such a dominant and visible company. Negative publicity is therefore an important risk to its business, in our view. In fact, earlier this year, many large companies joined the #StopHateForProfit campaign and stopped advertising on Facebook’s platforms for some time due to what they believe was inappropriate handling of hate speech and misinformation by Facebook. Although boycotts such as these do have a negative impact on Facebook’s revenue, they have so far not been pronounced because of Facebook’s highly diversified advertiser base. But continued negative publicity could lead to even larger future boycotts, so we are keeping a close eye on the situation.

Summary and allocation commentary

Facebook fits our investment framework to a tee. To summarise Facebook:

- It operates in a fast-growing market.

- It has a rock-solid balance sheet, providing it with the financial base to pursue growth.

- Its management team has demonstrated integrity, capability in growing the business (such as by making astute capital allocation decisions), and the ability to innovate.

- It has a highly recurrent revenue stream from its digital advertising business

- It has an excellent long-term track record of growing its revenue, profit, and free cash flow

- It is already generating strong free cash flow, and is likely to be able to generate a growing stream of free cash flow in the years ahead.

As it is with every other company, there are risks to note for Facebook. The main ones we’re watching include regulatory risks, key man risk, the threat of competition, and potential negative publicity.

After weighing the pros and cons, we initiated a 4% position – a large-sized allocation – in Facebook with Compounder Fund’s initial capital. We think Facebook offers the awesome combination of having a large market opportunity and a high probability of being able to grow at a strong pace for the long run. Moreover, Facebook’s valuation seems reasonable to us. As such, we are happy to have Facebook be one of the larger positions in Compounder Fund’s initial portfolio.

And here’s an important disclaimer: None of the information or analysis presented is intended to form the basis for any offer or recommendation; they are merely our thoughts that we want to share.