Compounder Fund: Etsy Sell Thesis - 04 Sep 2024

Data as of 03 September 2024

We first invested in Etsy (NASDAQ: ETSY) for Compounder Fund’s portfolio in April 2021. Our investment thesis for the company can be found here. In late-June this year, we completely exited Etsy. This article describes our Sell thesis for the company.

When we invested in Etsy, the company ran two e-commerce marketplaces that connected buyers and sellers. The first was the company’s core eponymous marketplace – Etsy – which focuses on being a destination for unique and creative products (from here on, the italicised “Etsy” would refer to the company’s Etsy marketplace, while the non-italicised “Etsy” would refer to the company). The second marketplace was Reverb; acquired by Etsy in 2019, Reverb focused on new, used, and vintage musical instruments. The company’s good, long-term track record of growing its GMS (gross merchandise sales), take rate, and number of active sellers and active buyers, was one of the traits that attracted us to it. Another was the company’s excellent multi-year history of growing its revenue, net income, and free cash flow. We thought Etsy would be able to continue growing these business and financial numbers at a healthy pace. This was because we saw a well-differentiated marketplace in Etsy. Moreover, Etsy had a market opportunity that we estimated to be around US$175 billion back then, which was much higher than its GMS (gross merchandise sales) of US$10.3 billion in 2020.

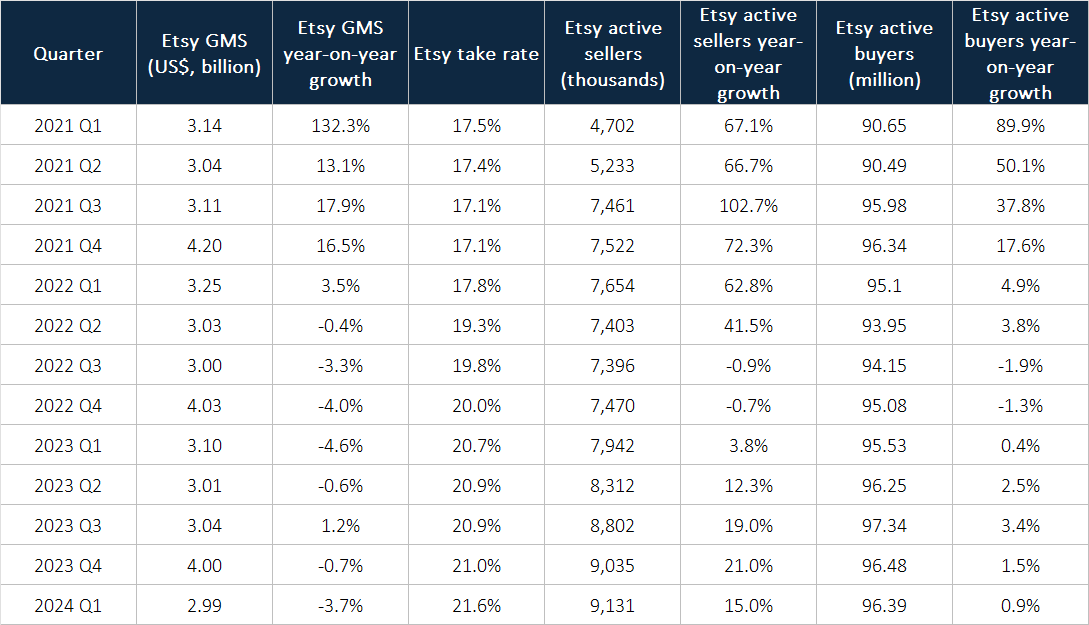

But in the three-plus years of our investment in Etsy, we have observed the growth rate of the company’s business and financial numbers deteriorating significantly. Table 1 shows Etsy’s GMS, take rate, active sellers, and active buyers in each quarter from the first quarter of 2021 to the first quarter of 2024. Despite a growing list of active sellers, the company’s GMS has mostly experienced small year-on-year declines starting from the first quarter of 2022 while the number of active buyers has effectively flat-lined. The take rate – revenue as a percentage of GMS – has shown steady sequential improvement over time, but Etsy’s inability to grow its GMS has taken a toll on its financial numbers.

Table 1; Source: Etsy earnings updates

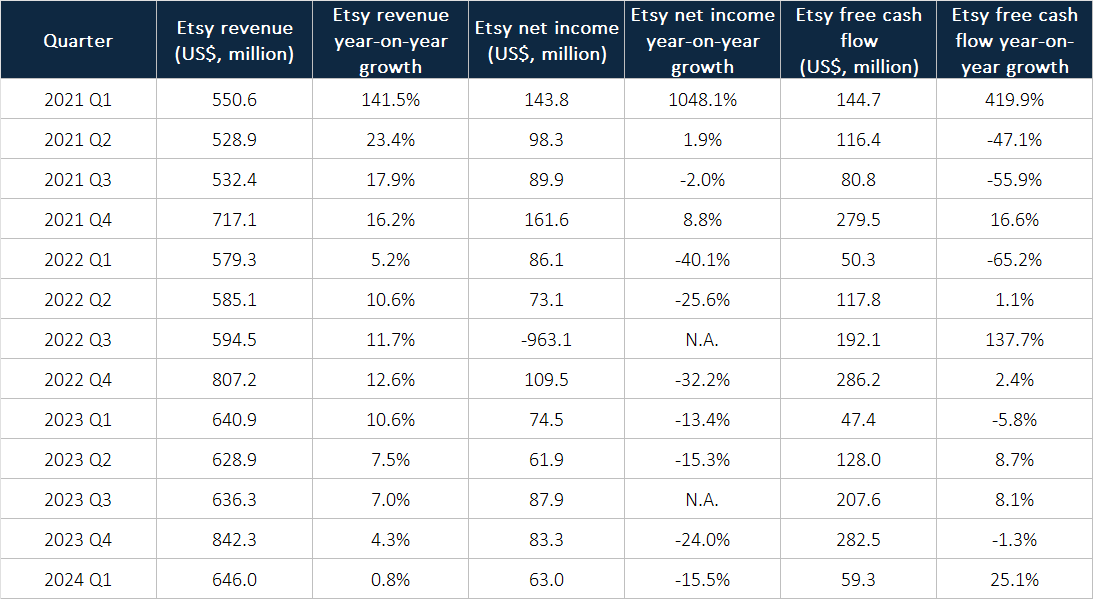

Table 2 shows Etsy’s revenue, net income, and free cash flow in each quarter from the first quarter of 2021 to the first quarter of 2024. The company’s revenue growth rates plummeted in 2023 and in the first quarter of 2024. Moreover, since the first quarter of 2022, Etsy’s net income has largely been declining year-on-year while the growth rates for free cash flow have mostly been lacklustre.

Table 2; Source: Etsy earnings updates

We also think we were mistaken about the characteristics of the Etsy marketplace. An early-June 2024 article from The Information cited data from the equity research firm MoffettNathanson:

“A September 2023 analysis by MoffettNathanson found that nearly 30% of Temu’s top-selling women’s clothing items were also listed for sale on Etsy, and 19 of Temu’s top 25 jewelry items also appeared on Etsy, often listed at much higher prices.”

This is not what a well-differentiated marketplace looks like to us. We were also alarmed by management’s comments in Etsy’s 2024 first-quarter earnings conference call regarding the company’s Chinese competitors (Temu is an online marketplace of Chinese e-commerce company PDD Holdings):

“I think what we’ve been saying all along is that we think that the Chinese competitors are more symptoms than a root cause. I think what we’re observing again and again, both at Etsy and what we read in the commentary from so many others in our space, is that consumers feel really pressured in spite of what we’re seeing about a generally healthy economy. Consumers feel really pressured and so they are seeking value in deep discounts and deep promotions. And so yes, the Chinese competitors are offering that, but Amazon and Walmart are, too.”

The above excerpt suggests that Etsy’s management sees a weak US economy and lower prices from Chinese competitors as the main challenges faced by the company. We think management is not seeing the actual issue, which is the lack of differentiation with the Etsy marketplace.

Compounding the problem are signs we see of poor capital allocation by Etsy’s management. In June 2021 (around two months after our initial investment), Etsy announced the acquisitions of two other e-commerce marketplaces. The first was Depop, a marketplace for second-hand fashion items. The second was Elo7, a Brazil-focused marketplace for unique, handcrafted items. The deals were completed in July 2021 and cost Etsy a total of US$1.7 billion, net of cash acquired (US$1.49 billion for Depop and US$212.1 million for Elo7). In the third quarter of 2022, Etsy incurred an impairment charge of US$1.04 billion for the goodwill associated with Depop (US$897.9 million) and Elo7 (US$147.1 million) when their post-acquisition business results ended up being worse than expected; this impairment was the key reason behind Etsy’s US$963.1 million net loss for the third quarter of 2022 that was shown in Table 2. There was a further impairment of US$68.1 million for Elo7-related assets in the second quarter of 2023. Etsy subsequently sold Elo7 in August 2023 for an undisclosed amount but we estimated that the sale was for a token sum in relation to the scale of Etsy’s business; we compared the net loss of US$2.6 million the company had to recognise for the Elo7 sale with the total Elo7-related impairments of US$215.2 million and its purchase price of US$212.1 million. At the time we exited Etsy, management had not recognised any further impairments for Depop, but suffice to say that the actual quality of Depop’s marketplace is nowhere near management’s view at the start.

We made our initial investment in Etsy at an average price of US$197 per share, but sold at a much lower average price of US$59. The big decline in Etsy’s stock price might lead someone reading this to ask: “Couldn’t you have sold Etsy earlier?” It’s a valid question. Our response will be something we shared in Compounder Fund’s Owner’s Manual:

“And on the topic of selling stocks, we will typically sell a stock in Compounder Fund’s portfolio if we find that the investment thesis is completely broken, or we have made a big mistake in our analysis. But we will be very slow to sell. The slowness is by design – it strengthens our discipline in holding onto the winners in Compounder Fund. Holding onto the winners will be a very important contributor to Compounder Fund’s long run performance.”

To sum up, we now believe we got our initial analysis on Etsy’s growth prospects badly wrong and have thus decided to sell and redeploy the company in other companies that we think have better return potential (in this case, the company was Nu Holdings).

And here’s an important disclaimer: None of the information or analysis presented is intended to form the basis for any offer or recommendation; they are merely our thoughts that we want to share. Of all other companies mentioned in this article, Compounder Fund owns shares in Nu Holdings. Holdings are subject to change at any time.