Compounder Fund: DocuSign Sell Thesis - 04 Sep 2024

Data as of 03 September 2024

We first invested in DocuSign (NASDAQ: DOCU) for Compounder Fund’s portfolio in July 2020. Our investment thesis for the company can be found here. In late-June this year, we completely exited DocuSign. This article describes our Sell thesis for the company.

When we first invested in DocuSign, it was providing cloud-based software – accessed via subscriptions – for users to manage agreements. Its core product was – and still is – eSignature, which enables users to sign a document securely using almost any device from virtually anywhere in the world. eSignature saved companies time and money when they executed their agreements, and this led to strong growth in DocuSign’s spend from existing customers (represented by the dollar-based net retention rate, or DBNRR), revenue, free cash flow, and customer count over time. We showed the growth of these metrics in our thesis on the company. In our thesis, we also described DocuSign Agreement Cloud:

“…DocuSign Agreement Cloud, which is a suite of software services – again all delivered over the cloud – that automates and connects the entire agreement process. Among other features, DocuSign Agreement Cloud includes:

- Automatic generation of an agreement from data in other systems;

- Support of negotiation-workflow;

- Collection of payment after signatures;

- Use of artificial intelligence (AI) to analyse agreement-documents for risks and opportunities; and

- Hundreds of integrations with other systems, so that the agreement process can be seamlessly combined with other business processes and data…

…Speaking of DocuSign Agreement Cloud, it was released in March 2019… it includes multiple software services. DocuSign sees DocuSign Agreement Cloud as a new category of cloud software that connects existing cloud services in the realms of marketing, sales, human resources, enterprise resource planning, and more, into agreement processes. We see two huge positives that come with the introduction of multi-product sales. Firstly, it will likely lead to each DocuSign customer using more of the company’s products. This means that DocuSign could be plugged into an increasing number of its customers’ business processes, resulting in stickier customers. Secondly, DocuSign thinks that covering a wider scope of the entire agreement process could roughly double its market opportunity from the current size of US$25 billion to around US$50 billion.”

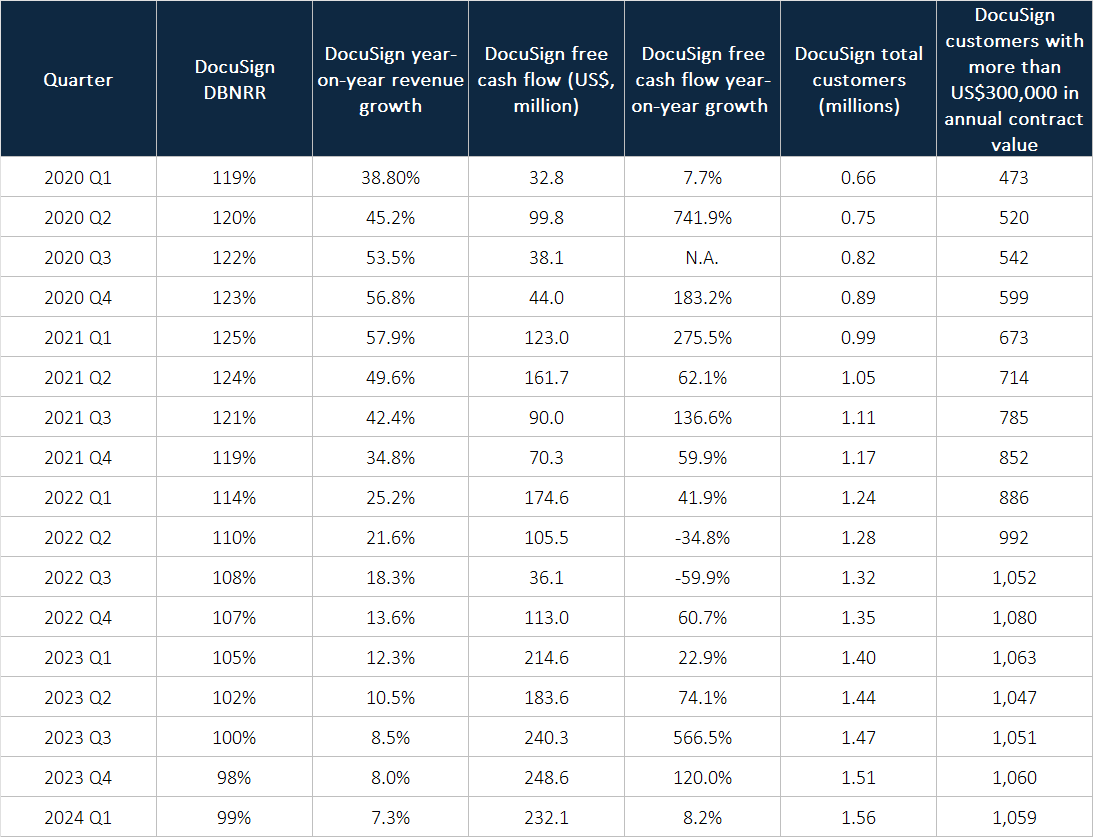

DocuSign Agreement Cloud was a relatively new service when we first invested, and we were optimistic about its ability to drive the company’s future business growth. But unfortunately, it appears to have failed to catch on and the last earnings conference call in which management voluntarily discussed it was for the first quarter of 2022. This was fine for a while. During the first two years or so of our investment in DocuSign, the company’s business was developing along a similar trajectory as what we expected. It was posting healthy DBNRRs of 110% or more, and had good growth in its revenue, free cash flow, and customer count (in both total customers and high-spending customers). But DocuSign’s business-growth started unravelling in the fourth quarter of 2022. Its year-on-year revenue growth-rate fell to the low-teens range and proceeded to decline in each subsequent quarter to just 7.3% in the first quarter of 2024. Along the way, its DBNRR also shrank to 99% – meaning existing customers were spending less compared to a year ago – while the number of its high-spending customers stagnated. A saving grace was DocuSign’s generally excellent free cash flow (FCF) growth, but we will come back to this soon. Table 1 below shows DocuSign’s DBNRR, year-on-year revenue growth, year-on-year free cash flow growth, total customers, and high-spending customers (those with more than US$300,000 in annual contract value) in each quarter going back to the first quarter of 2020:

Table 1; Source: DocuSign filings

Allan Thygessen assumed the chief executive role at DocuSign in October 2022 and spoke of his desire to run a company with double-digit revenue growth rates during his first earnings conference call as CEO (which was for the third quarter of 2022). But as we discussed earlier, the company’s year-on-year revenue growth rate had instead declined steadily to a pedestrian 7.3% in 2024’s first quarter. Moreover, in DocuSign’s earnings update for the first quarter of 2024, the guidance given for the company’s revenue growth for the year was just 6%. To boost growth, Thygessen announced a new product strategy for the company, a platform named Intelligent Agreement Management (IAM) this April. It is a one-stop platform for users to create, manage, and learn from their agreements. This reminded us of DocuSign Agreement Cloud, the platform launched in March 2019 that subsequently struggled (the company’s lacklustre DBNRRs and failure to grow high-spending customers since the third quarter of 2022 are tell-tale signs), as it was also billed as a solution for “how organisations prepare, sign, act on and manage their agreements.” DocuSign’s new attempt to sell a holistic agreement-management platform, in the form of IAM, may succeed where the Agreement Cloud failed. But we’ve yet to observe any signs that can give us confidence on this.

Coming to DocuSign’s FCF, the company’s trailing FCF margin at the time of our sale was already at 32%. We did not see much room for further improvement in the margin. This meant the company’s future FCF growth rates would likely mirror its revenue growth. And its future revenue growth, as we have been explaining in this Sell thesis for DocuSign, did not look promising to us.

DocuSign’s stock price reflected the company’s struggle to grow its business in the latter half of our ownership (we were invested in the company for nearly four years, from July 2020 to June 2024). It fell from our average purchase price of US$199 at our initial investment to our average sale price of US$53. The big decline in DocuSign’s stock price might lead someone reading this to ask: “Couldn’t you have sold DocuSign earlier?” It’s a valid question. Our response will be something we shared in Compounder Fund’s Owner’s Manual:

“And on the topic of selling stocks, we will typically sell a stock in Compounder Fund’s portfolio if we find that the investment thesis is completely broken, or we have made a big mistake in our analysis. But we will be very slow to sell. The slowness is by design – it strengthens our discipline in holding onto the winners in Compounder Fund. Holding onto the winners will be a very important contributor to Compounder Fund’s long run performance.”

To sum up, we now believe we were wrong in our initial analysis on DocuSign’s growth prospects and thus decided to sell and redeploy the company in other companies that we think have better return potential (in this case, the company was Nu Holdings).

And here’s an important disclaimer: None of the information or analysis presented is intended to form the basis for any offer or recommendation; they are merely our thoughts that we want to share. Of all other companies mentioned in this article, Compounder Fund owns shares in Nu Holdings. Holdings are subject to change at any time.