Compounder Fund: Coupang Investment Thesis - 14 May 2021

Data as of 12 May 2021

Coupang (NYSE: CPNG), which is based in South Korea but listed in the USA, is one of the four companies in Compounder Fund’s portfolio that we invested in for the first time in April 2021. This article describes our investment thesis for the company.

Company description

Founded in 2010, Coupang – whose name comes from a combination of the English word “coupon” and the Korean word for hitting the jackpot, “pang” – is today the largest e-commerce player in South Korea. It effectively operates only in the country and earned total revenue of US$11.97 billion in 2020 (although Coupang generates revenue in the Korean won, it reports its financials in the US dollar).

Coupang carries its own inventory of products for sale to consumers through its app and website. In 2020, 92.3% of Coupang’s total revenue (or US$11.05 billion) came from the sale of this inventory to consumers and it is known as net retail sales. Coupang’s inventory consists of millions of types of products and this is the largest selection available among ecommerce companies in South Korea.

The other 7.7% of Coupang’s total revenue in 2020 (US$922.2 million) is known as net other revenue. It comprises (1) commissions from Coupang’s ecommerce marketplace platform that connects buyers and sellers, (2) fees from the company’s online food delivery service, Coupang Eats, (3) fees for digital advertising services offered by Coupang, and (4) subscription fees from Rocket WOW. Launched in 2019, Rocket WOW is Coupang’s membership program that offers a host of benefits – including unlimited free shipping with no minimum spend, free returns, expedited shipping, exclusive discounts, and more – for a low monthly fee of just 2,900 Korean won, or around US$2.50. Coupang’s ecommerce marketplace also significantly widens the product-selection for consumers. In fact, Coupang’s third-party ecommerce marketplace has the largest selection of products among its peers. Together with Coupang’s own inventory, the company offers “hundreds of millions” of products that are sourced from over 200,000 merchants and suppliers.

Investment thesis

We have laid out our investment framework on Compounder Fund’s website. We will use the framework to describe our investment thesis for Coupang.

1. Revenues that are small in relation to a large and/or growing market, or revenues that are large in a fast-growing market.

Coupang already has a sizeable business. The company pulled in US$13.76 billion of revenue in the 12 months ended 31 March 2021 and it is the largest ecommerce company in its only geographical market of South Korea. But there’s still significant room for the company to grow in the country.

According to research from Euromonitor, as of 2019, South Korea is the 12th largest economy in the world and the fourth largest in Asia. It also has a relatively high GDP per capita of US$31,847 – for perspective, the USA and Singapore both had GDP per capita of around US$65,000 each in 2019. South Korea’s total retail, grocery, consumer foodservice, and travel spend is expected to increase from US$470 billion in 2019 to US$534 billion in 2024, with total ecommerce spend expected to grow by 10% annually from US$128 billion to US$206 billion over the same period. The projection for good ecommerce growth in South Korea looks sensible to us.

The country has the highest smartphone penetration rate in the world with 96% of the population using a smartphone as of 2018. Meanwhile, mobile shopping is already the most popular online commerce channel in South Korea today. So South Koreans are digitally savvy and have high spending power – these two traits can be powerful fuel for ecommerce growth in the country, in our opinion. Another important fuel for high ecommerce growth in South Korea is its high population density – it makes fulfillment for ecommerce companies relatively easy, in our view, if the companies have the right infrastructure. During a March 2021 conversation with TechCrunch, Coupang’s founder and CEO Bom Suk Kim said that South Korea only has around 2,700 square kilometres of inhabitable land that houses the country’s entire population of over 50 million. (For perspective, Singapore’s total land area in 2019 was 725.7 square kilometres, according to data from the Singapore government, and the population was 5.70 million.)

We think Coupang will be able to capture plenty more of South Koreans’ total commerce spending in the future. Since 2013, the company has poured billions of dollars into its technology and fulfillment infrastructure to provide superior customer experiences.The results so far are impressive:

- Coupang can boast of the largest logistics footprint among ecommerce companies in South Korea. At the end of 2020, the company’s fulfillment and logistics centres (more than 100 of them across 30 cities) covered 2.3 million square metres, which is the size of more than 400 football fields. This places 70% of the South Korean population within 11 km of a Coupang logistics facility.

- Coupang has the largest directly-employed delivery fleet in South Korea – 15,000 full-time drivers at the end of 2020 – and the company provides its delivery drivers with proprietary software and custom-designed trucks to improve the efficiency of the delivery process.

- Coupang has machine learning software that anticipates demand and ships products ahead of time to be closer to consumers, hence lowering delivery times. The company also has technology that predicts and assigns the fastest and most efficient path for each order – out of hundreds of millions of combinations of inventory, processing, truck, and route options – within seconds of it being placed.

- Coupang’s ecommerce business is integrated end-to-end, so it is able to implement upstream processes that minimise downstream inefficiencies. For example, Coupang’s packages tend to arrive pre-sorted in truck-ready containers for assigned trucks, thus improving the efficiency of its fleet of delivery drivers.

- Coupang’s clever use of technology, dense logistics network, and large delivery fleet allow the company to provide the following in its Rocket Delivery service: The fastest delivery service in Korea among ecommerce companies; dawn delivery (delivery before 7am if ordered before midnight) and same-day delivery (delivery in the same day if ordered in the morning) for millions of products everyday, even fresh groceries; free, one-day delivery nationwide, 365 days a year for nearly all orders; boxless packaging (more than 75% of Coupang deliveries come without boxes); Zero Packaging, which is Coupang’s recent innovation that eliminates almost all disposable packaging by delivering in eco-bags that are collected for reuse after each delivery; frictionless returns (customers simply tap a button on Coupang’s app and leave the item outside their door for pickup); and importantly, the largest selection of products for consumers to choose from among South Korean ecommerce companies.

We also want to highlight that Coupang had to build its logistics network from scratch because there was no major third-party logistics company in South Korea that offered reliable next-day or same-day delivery services at scale. Because of this, we think that Coupang is one of those rare companies that are creating tailwinds – in this case, the growth of ecommerce in South Korea – rather than merely riding on them. In our opinion, by being the creator of the ecommerce tailwind in South Korea, Coupang’s actual market opportunity in the next few years could be even larger than what Euromonitor has projected (the US$206 billion in ecommerce spending in 2024). This is because Coupang’s future actions may lead to new consumer shopping habits that expands the overall pie.

Although Coupang is currently only active in South Korea, news outlets reported last month that the company is setting its sights on Singapore and possibly Southeast Asia. So international growth for Coupang in parts or all of Southeast Asia, while not easy – there is formidable competition from the likes of Alibaba’s Lazada and Sea Limited’s Shopee, among others – is a possibility.

2. A strong balance sheet with minimal or a reasonable amount of debt

Coupang has a robust balance sheet in our view. The company exited the first quarter of 2021 with US$4.33 billion in cash and equivalents, and much lower debt of US$599.3 million, giving rise to a net-cash position of US$3.73 billion.

For the sake of conservatism, we note that Coupang also has total operating lease liabilities of US$1.20 billion. But this is still dwarfed by the company’s net-cash position.

3. A management team with integrity, capability, and an innovative mindset

On integrity

Earlier, we mentioned that Bom Suk Kim is Coupang’s founder and CEO. This makes the 42 year-old Kim Coupang’s most important leader. We appreciate the fact that Kim has more than a decade of experience leading Coupang (the company was founded in 2010) despite his young age.

We think that Kim’s remuneration structure at Coupang demonstrates integrity. In 2020, he received a base salary of US$886,635, and other miscellaneous compensation of US$195,473. These are modest sums when compared to the scope of Coupang’s business. Kim also received 5.434 million Coupang shares as part of his compensation for the year. At the time the shares were granted (June 2020), the total value of the shares was US$13.26 million. This sum is again relatively modest. But more importantly, they vest over a five-year period starting from 25 June 2020. The multi-year vesting period means that Kim’s remuneration in 2020 is tied to long-term changes in Coupang’s share price, which is in turn tethered to the company’s long-term business performance. We think this structure aligns the interests of Kim and Coupang’s other shareholders.

And speaking of alignment of interests, Kim also has significant skin in the game. Right after Coupang’s IPO in March this year, Kim controlled 174.8 million Coupang shares. Based on Coupang’s 12 May 2021 share price of US$35, his stake is worth US$6.18 billion.

We want to highlight that all of Kim’s Coupang shares are of the Class B variety. Coupang has two share classes: (1) Class B, which are not traded and hold 29 voting rights per share; and (2) Class A, which are publicly traded and hold just 1 vote per share. As a result, Kim currently controls around 77% of Coupang’s voting power despite holding only 10% of the company’s total shares. A manager having virtually complete control over a company can potentially be bad for shareholders. This overwhelming concentration of Coupang’s voting power in the hands of Kim means that we need to be comfortable with him at the company’s helm. We are.

We also want to flag out that Kim’s brother and sister-in-law are both working at Coupang. When a company’s CEO hires his/her family members, we pay attention to how they’re remunerated to determine whether the CEO is acting fairly to the company’s other shareholders. In the case of Coupang, we’re happy to say that the remuneration of Kim’s brother and sister-in-law are trivial when compared to the scope of Coupang’s business. Since 2018, their annual remuneration has ranged from US$279,000 to US$475,000 (for Kim’s brother) and from US$202,000 to US$247,000 (for Kim’s sister-in-law).

On capability and ability to innovate

We rate Bom Suk Kim highly on this front and there are a few things we want to discuss.

The first concerns Kim’s fanatical focus on the customer experience at Coupang. We believe this mindset helps set Coupang apart from its competitors. Because it is something that comes directly from Kim’s worldview, it is unlikely to be replicable, since no two humans are ever identical. In Coupang’s IPO prospectus, Kim wrote a letter to investors. In it are the following passages that we think gives a great window on the fanaticism that Coupang’s founder has on delighting customers:

“Why force customers to choose between amazing service, low prices, and broad selection?

Our mission is to create a world where customers wonder “How did I ever live without Coupang?” We strive to eliminate the conventional tradeoffs in the customer experience.

What does this mean in practice? It’s nighttime, and our friend Suzy, unwinding after another busy day, realizes she needs a pair of headphones, a tutu before her daughter’s ballet practice, and cereal, milk, and fresh strawberries for tomorrow’s breakfast.

Through our single app, Suzy can find all those items and millions more at low prices and have them delivered to her doorstep before 7 AM via Dawn Delivery… for free. She places her order in seconds, and heads off to sleep. When she opens her eyes, it’s like Christmas morning: the order is waiting at her front door. Suzy places the tutu in her daughter’s backpack, prepares breakfast with the family, and enjoys the new headphones on her early-morning commute.

Even from Coupang’s earliest days, we set out to deliver true “wow” experiences every day. We chose to upend conventional wisdom and raise people’s expectations of what is possible. To transform the customer experience, we had to think about e-commerce – indeed commerce – in new ways.

Our first watershed decision was to build an end-to-end logistics network powered by the latest technologies. The lack of existing fulfillment capacity and the limitations of third-party logistics in the market forced us to build our own from scratch. It was an immensely difficult effort that required significant investments of time and capital, but we never wavered in our conviction that it was the right decision for our customers. We can now do what we believe no one else in our market can – guarantee one-day delivery on all Rocket orders – without reducing our selection or charging for delivery.”

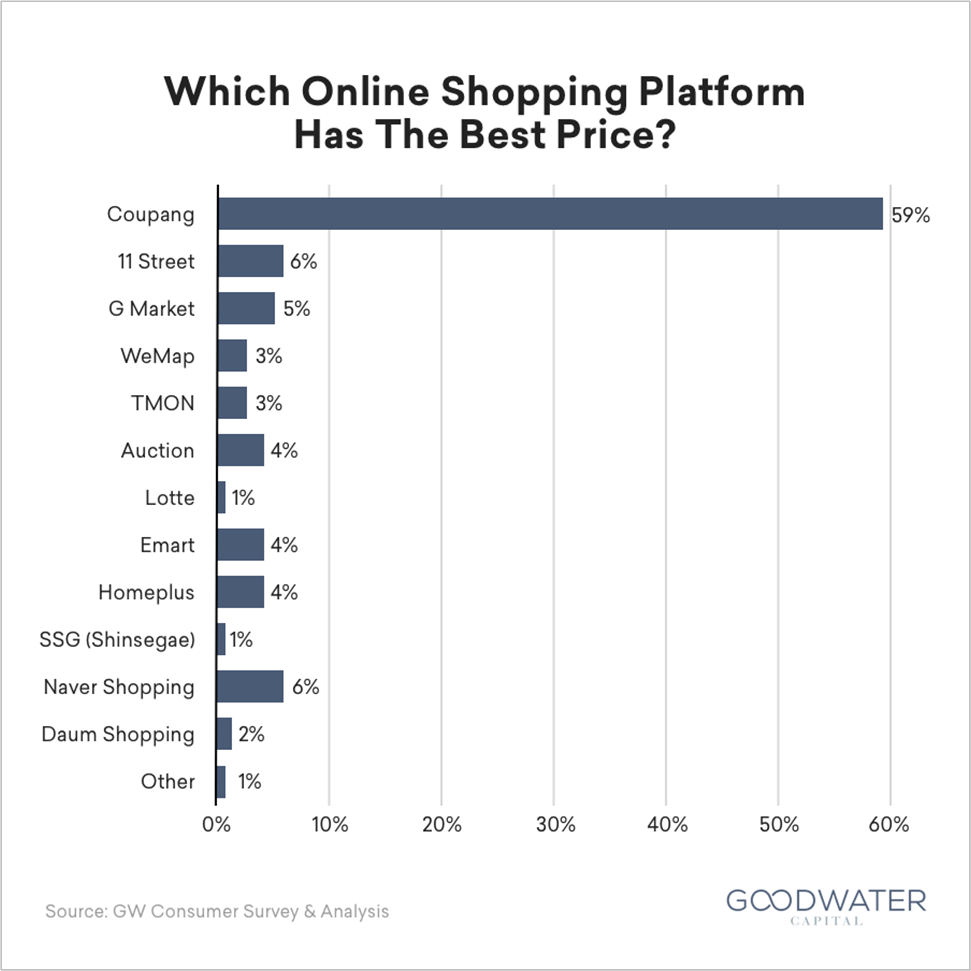

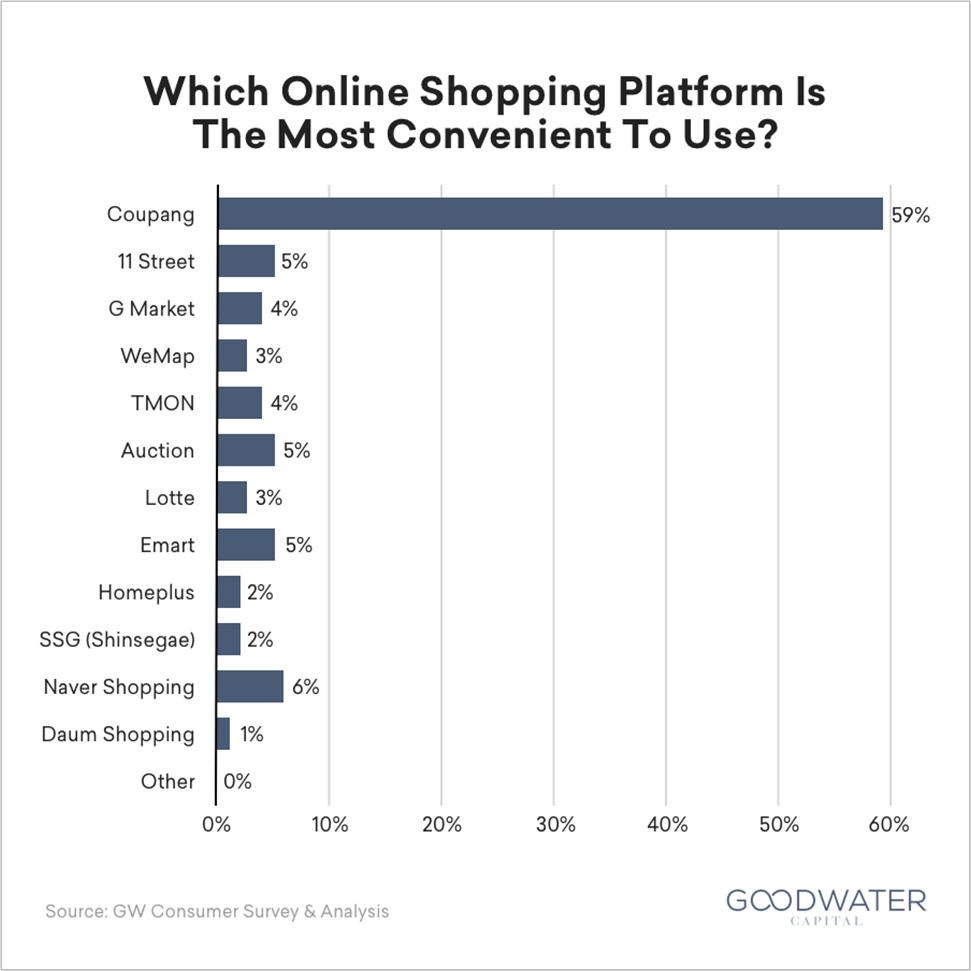

We think that Kim has so far walked his talk. There are two things we can point to. The first is the impressive fulfillment capabilities Coupang currently possesses (such as dawn and same-day delivery, and frictionless returns) that we mentioned earlier. The second is recent consumer surveys from Goodwater Capital showing that consumers in South Korea overwhelmingly prefer Coupang compared to the company’s competitors when it comes to price and convenience; these are illustrated in the two charts below.

Source: Goodwater Capital

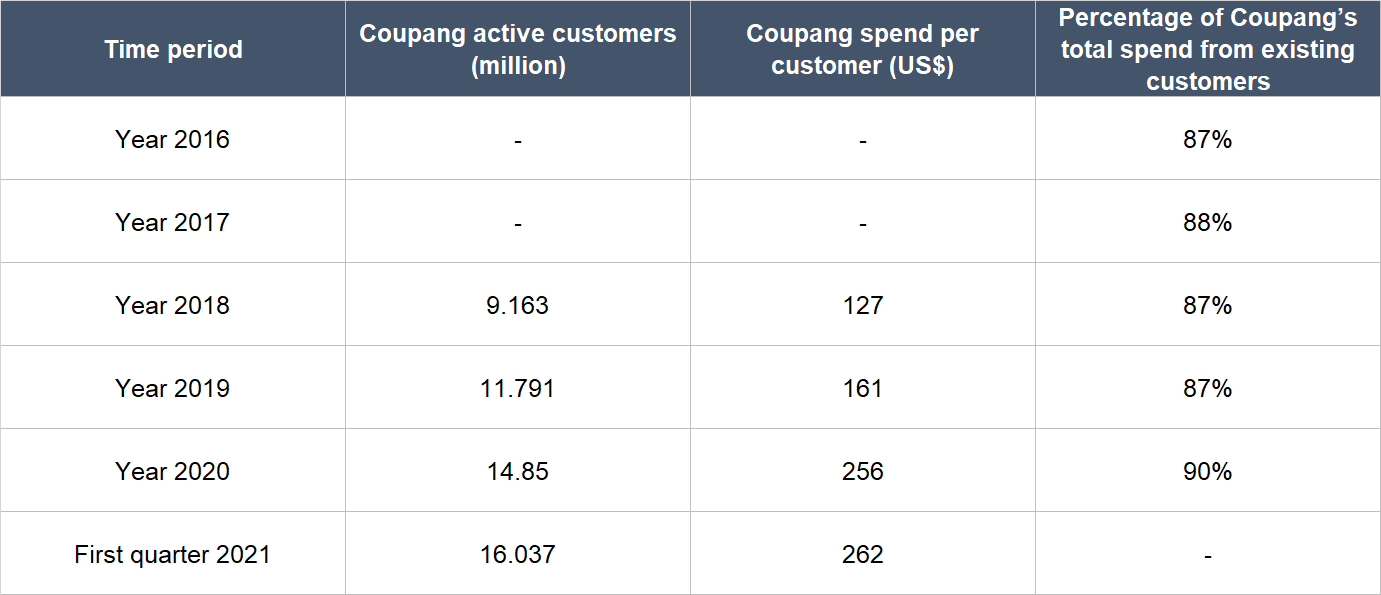

The second thing we want to discuss is Coupang’s excellent track record at growing and retaining its customer base. These can be seen in the table below, which shows (1) the impressive 28% annual growth in Coupang’s active customers from 2018 to the first quarter of 2021, (2) the excellent 38% annual increase in spend per customer over the same period, and (3) the high percentage of Coupang’s total spend in each year from 2016 to 2020 that comes from existing customers.

Source: Coupang IPO prospectus

Coupang has also been excellent at driving higher spend from its customer-cohorts over time and this is the third thing we want to discuss. The chart below shows the growth in spend (indexed to Year 1) for each customer cohort from 2016 to 2019. Each cohort in a given year represents customers who placed their first order with Coupang during the year. For example, the 2016 cohort refers to all Coupang customers who placed their first order with the company at any time during 2016, and impressively, the 2016 cohort’s spend with Coupang had increased by 3.59 times (or 259%) after five years. Another positive thing we want to highlight is that Coupang’s newer cohorts have increased their spend faster than older cohorts. For instance, the 2017 cohort spent 80% more in their second year, whereas the 2018 and 2019 cohorts increased their spend by 98% and 119%, respectively, in their second year.

Source: Coupang IPO prospectus

The fourth thing we want to discuss is Coupang’s history of transforming itself, which we think demonstrates the tenacity and innovative spirit of Kim. Earlier, we mentioned that Coupang was founded in 2010. In the company’s earliest days, it ran a daily-deals business, much like Groupon. But shortly after, Kim pivoted Coupang into a 3rd-party online marketplace model. The new model found quick success. Coupang crossed US$1 billion in sales within three years and found itself preparing for an IPO. But at the very last moment, Kim pulled the plug on the public listing. He reasoned that being a public company would make it hard for Coupang to change course – at that point in time, he had a “nagging feeling” that something wasn’t right with Coupang’s business model. Recounting the episode in a 2019 interview with CNBC, Kim said:

“We had to ask ourselves: ’Was the platform we had built, were the services and experiences that we were providing for our customers, creating a 5% difference or were we creating that kind of world where the customers we love, their jaws would drop? “And the reality was no…

…If we wanted to provide something that really mattered to customers — 100 times better, exponentially better — we had to go through an enormous amount of change. We had to change our entire technology stack, the way we did business, our business model. I think that was the most difficult, but the choice that I’m most proud of.”

So in 2013, Coupang switched to becoming a 1st-party ecommerce company, where it owned its inventory and controlled the entire end-to-end customer experience. In 2014, Coupang launched Rocket Delivery. And over the next few years, Coupang launched Coupang Eats and Rocket WOW, among other services.

The fifth and last thing we want to discuss is what we think is a great corporate culture that Kim has built at Coupang. In Kim’s letter to investors in Coupang’s IPO prospectus, he mentioned the following that touched on the topic:

“We believe it is both our opportunity and responsibility to challenge expectations about important social issues in our community.

In a market where the industry standard is a six-day workweek, we were the first to establish a five-day workweek for our drivers, even as we became the first major service to provide deliveries to customers seven days a week. We also hire our own drivers, Coupang Friends, directly, and provide them with paid time off and full benefits. The vast majority of drivers in the industry receive neither. Additionally, we are planning to grant up to a ₩100 billion, or approximately [US]$90 million, of restricted stock awards to our frontline workers and non-manager employees. We believe we are the first company in Korea to make our frontline employees stockholders.”

We recognise that it’s not all sunshine and rainbows within Coupang. For example, there’s an article written by journalist Max Kim that was published in November 2020 in Rest of World. The piece criticised the way Coupang manages its employees, especially during the outbreak of COVID-19, when the company appeared to have prioritised business-growth over the safety of its employees. Max Kim’s article also featured an interview with a Coupang employee who mocked the company’s delivery systems, saying it’s driven by human labour and not technology. We’re giving Coupang the benefit of the doubt for two reasons. One, it has displayed impressive growth at scale and there’s more on this in the “A proven ability to grow” section of this article. Two, in his letter to investors in Coupang’s IPO prospectus, Kim had laid out concrete ways in which Coupang treats its employees better than the norm. Nevertheless, we’re keeping an eye on Coupang’s corporate culture.

4. Revenue streams that are recurring in nature, either through contracts or customer-behaviour

We think that Coupang has a high level of recurring revenue from customer behaviour. This is based on three pieces of data that we had brought up earlier.

First, the company has millions of active customers and the number has increased by 28% annually from 9.16 million in 2018 to 16.037 million in the first quarter of 2021. Second, Coupang’s customers – as a group – tend to spend significantly more with the company over time, as shown in the data on cohort-spending. Third, spend from existing customers has consistently made up a very high percentage of Coupang’s total customer spend in each year from 2016 to 2020, with the percentage ranging from 87% to 90%.

5. A proven ability to grow

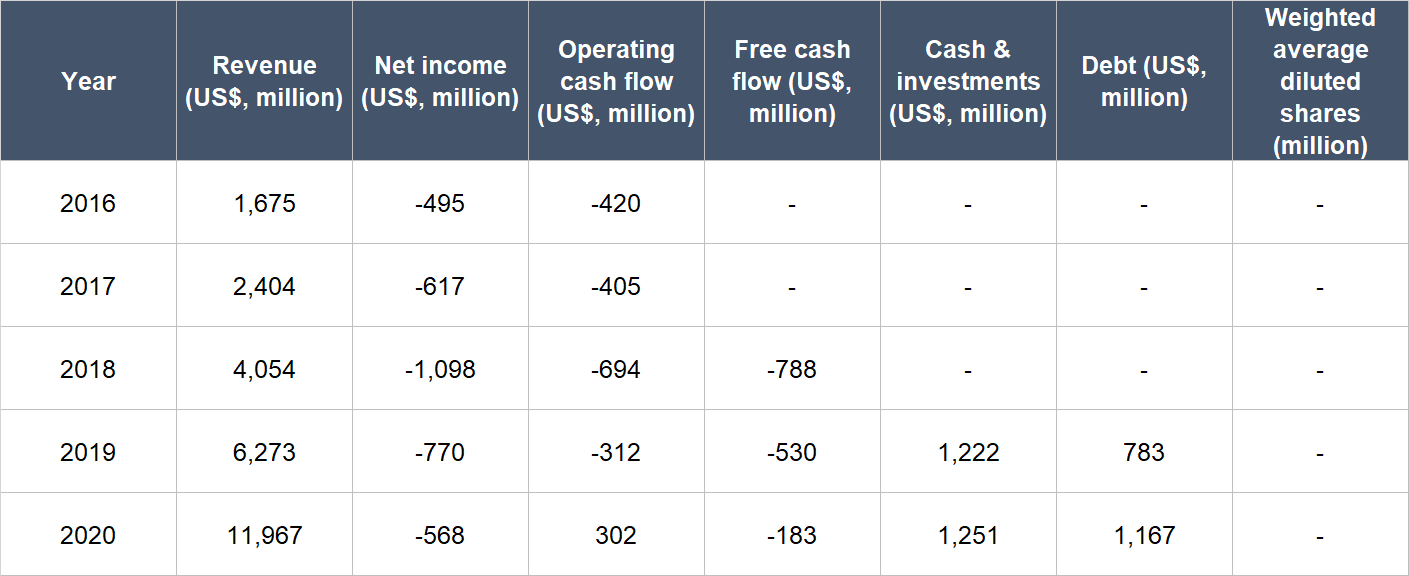

Coupang has a short history as a public-listed company (its IPO was only in March this year) so we don’t have much financial data to study for the company. But we like what we see. The table below shows the key financial figures for Coupang that we can obtain:

Source: Coupang IPO prospectus

A few key things to highlight from Coupang’s historical financials:

- Despite coming off an already sizeable base in 2016, Coupang’s revenue has compounded at an excellent annual rate of 55.3% from then to 2019. Coupang’s revenue growth accelerated to 90.8% in 2020. This was driven partly by the emergence of the COVID-19 pandemic during the year, which led to higher consumer demand for ecommerce in South Korea.

- Coupang has been generating negative net income, but the trend is in the right direction, with the net income margin improving from -29.5% in 2016 to -4.7% in 2020.

- The company reached a significant milestone in 2020 as it produced positive operating cash flow. The operating cash flow margin (operating cash flow as a percentage of revenue) is also trending in the right direction, having climbed from -25.1% in 2016 to 2.5% in 2020.

- Coupang’s free cash flow is also moving in the right direction, having improved from -US$787.9 million in 2018 to -US$183.1 million in 2020. The free cash flow margin (free cash flow as a percentage of revenue) has also improved markedly over the same period, rising from -19.4% to -1.5%. (We only have data for Coupang’s free cash flow since 2018 because we could not obtain prior details on the company’s capital expenditures.)

- The balance sheet was strong for the years we have data on (2019 and 2020), with cash and investments being higher than debt.

- We did not look at Coupang’s share count data because the company’s IPO date was after the end of 2020. We do note that Coupang had around 1.715 billion shares outstanding right after its public listing – we’ll be using this number as the basis for analysing Coupang’s dilution in the future.

Coupang posted impressive year-on-year revenue growth of 74.3% for the first quarter of 2021, as illustrated in the table below. At first glance, Coupang’s net income and free cash flow both look bad. Net income went deeper into the red, with the net income margin also declining from -5.8% to -7.0%. Meanwhile, the free cash flow margin fell significantly from 10.2% to -7.8% because of a plunge in operating cash flow. But we don’t think there’s anything to worry about. During the first quarter of 2021, Coupang recorded a significant increase in stock-based compensation expense because of its IPO. As for cash flow, Coupang only started producing positive operating cash flow in 2020 and even then, the company’s quarterly operating cash flows for the year were lumpy.

Source: Coupang 2021 first quarter earnings update

6. A high likelihood of generating a strong and growing stream of free cash flow in the future

In Coupang’s IPO prospectus, the company wrote that its “long-term goal is to maximize Free Cash Flow while minimizing shareholder dilution.” We like Coupang’s focus on generating free cash flow, and we believe that the company can indeed generate substantial free cash flow in the future.

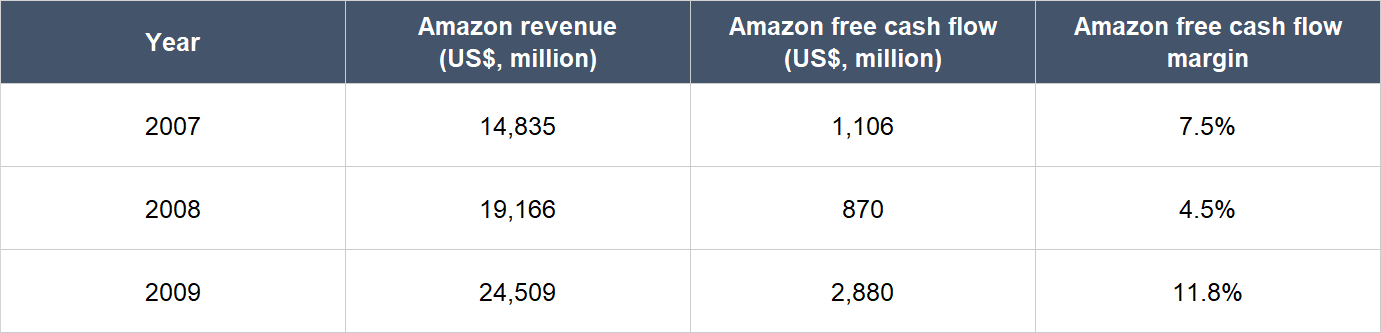

We can look at the US ecommerce juggernaut Amazon as an example. The table below shows the company’s revenues, free cash flows, and free cash flow margins in each year from 2007 to 2009. Back then, Amazon was focused only on first-party (where Amazon owns the inventory) and third-party ecommerce (where Amazon acts as a marketplace connecting merchants and consumers) – Amazon Web Services (or AWS), which is Amazon’s cloud computing arm, was established only in 2006. Amazon was able to generate substantial free cash flow – with decent free cash flow margins – even when its business was predominantly just ecommerce.

Source: Amazon annual reports

We note that Coupang is still unable to generate free cash flow despite having revenue of US$13.76 billion in the 12 months ended 31 March 2021, which is similar to what Amazon had in 2007. But we believe that Coupang should be able to produce substantial free cash flow in the future when its business achieves even larger scale and operating leverage kicks in.

Valuation

We like to keep things simple in the valuation process. Given Coupang’s penchant for free cash flow (which is absolutely correct!), we think the price-to-free cash flow (P/FCF) ratio is a suitable gauge for the company’s value when free cash flow is abundant. When free cash flow is light or negative because Coupang is reinvesting into its business – like the situation right now – the price-to-sales (P/S) ratio will be useful.

Our initial purchases of Coupang shares were completed in early April 2021. Our average purchase price was US$46 per share. At our average price and on the day we completed our purchases, Coupang’s shares had a trailing P/S ratio of around 6.5. This is a high valuation. For perspective, if we assume a 5% free cash flow margin for Coupang right now, the P/S ratio of 6.5 would imply a P/FCF ratio of 130 (6.5 divided by 5%). But we think Coupang is an exceptional company that has years of rapid growth ahead of it. This makes us comfortable with paying up for Coupang’s shares.

For perspective, Coupang carried a P/S ratio of around 4.4 at its 12 May 2021 share price of US$35.

The risks involved

We see a few important risks that could derail our investment in Coupang.

The first is related to geopolitics. For now, Coupang derives effectively all its revenue in South Korea. The country’s neighbour is the hermetic North Korea, which over the past few decades has been displaying an antagonistic stance toward South Korea and its ally, the USA. It does not help too that North Korea has (1) active nuclear weapons programmes, and (2) long been ruled by a dictatorial regime with an iron first and so there are no effective checks and balances in the country that could sensibly prevent any unnecessary aggression toward South Korea. Should there be an armed conflict between North and South Korea in the future, Coupang’s business is likely to be severely impacted.

Key-man risk is the second important concern we have with Coupang. We think that Bom Suk Kim is a talented entrepreneur and business person. If he ever leaves Coupang for any reason, his successor will have giant shoes to fill – and we will be watching the situation closely.

Lastly, there’s valuation risk. We think Coupang’s business is likely to grow at a rapid clip for many years and so it deserves its premium valuation. But if there are any hiccups in Coupang’s business – even if they are temporary – there could be a painful fall in the share price. This is a risk we’re comfortable taking as long-term investors.

Summary and allocation commentary

To sum up Coupang, it has:

- A large and growing ecommerce market in South Korea, whose growth is, we think, partly driven by Coupang’s innovative efforts in developing its own integrated end-to-end fulfillment infrastructure.

- A robust balance sheet that has significantly more cash than debt.

- A leader who has demonstrated integrity and who has an excellent track record of innovation and execution.

- Highly recurring revenues from customer behaviour (Coupang’s customers tend to stick, and spend more, with the company over time).

- A strong history of revenue growth

- A high likelihood of generating substantial free cash flow in the years ahead

As it is with every company, there are risks to note for Coupang. The main ones we’re watching include the tense relationship between North and South Korea; the possibility that Coupang’s growth could be derailed if Bom Suk Kim stops leading the company; and the company’s high valuation.

After considering the pros and cons, we decided to initiate a position of around 0.5% in Coupang in April 2021. We appreciate all the strengths we see in Coupang’s business, but our enthusiasm is tempered by the company’s high valuation and current revenue-concentration in South Korea. On the point about revenue-concentration, we noted earlier that (1) South Korea is a huge economy and (2) Coupang still appears to have significant room to grow in the country’s ecommerce market. But the size of South Korea’s economy is still much smaller than, say, the USA’s. So by currently operating only in South Korea, Coupang may have a relatively lower ceiling on its growth potential compared to other companies in Compounder Fund’s portfolio.

And here’s an important disclaimer: None of the information or analysis presented is intended to form the basis for any offer or recommendation; they are merely our thoughts that we want to share. Of all the other companies mentioned in this article, Compounder Fund also owns shares in Amazon. Holdings are subject to change at any time.