Compounder Fund: Apple Investment Thesis - 29 Nov 2020

Data as of 27 November 2020

Apple Inc (NASDAQ: AAPL), which is based and listed in the USA, is one of the 40 companies in Compounder Fund’s initial portfolio. This article describes our investment thesis for the company.

Company description

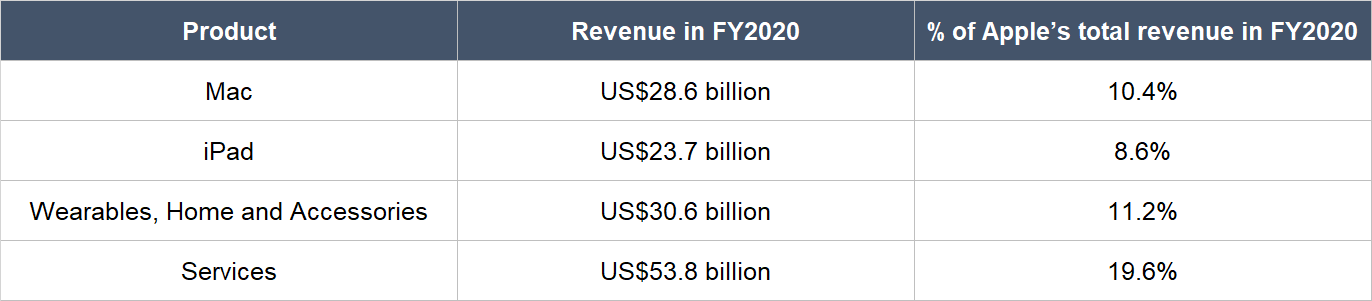

Apple, as most of you likely know, is the company behind the ubiquitous and iconic smartphone device, the iPhone. But there’s so much more to Apple. In the fiscal year ended 26 September 2020 (FY2020), Apple’s non-iPhone business accounted for 49.8% of the company’s total revenue of US$274.5 billion. The non-iPhone business can be split into the following categories:

Source: Apple annual report

The Mac and iPad categories refer to Apple’s line of personal computers and tablet devices, respectively. Meanwhile, the Wearables, Home and Accessories category includes AirPods (Apple’s wireless headphones), Apple TV (Apple’s video streaming device), Apple Watch (Apple’s smartwatch), Beats products (Apple’s line of high performance headphones), HomePod (Apple’s smart speaker), iPod touch (Apple’s portable music player), and more. The Services category includes the following sub-categories:

- Advertising

- AppleCare, which consists of fee-based service and support products

- Cloud Services, which is Apple’s iCloud cloud-storage service

- Digital Content, which consists of the App Store (where users can discover and download apps), Apple Arcade (Apple’s digital games subscription service), Apple Music (Apple’s music streaming service), Apple TV+ (Apple’s video streaming service), and more

- Payment Services, which consists of Apple Pay (Apple’s cashless payments service) and Apple Card (Apple’s co-branded credit card)

From a geographical point of view, Apple is pretty diversified. 45.4% of the company’s revenue in FY2020 came from the Americas while 25.0% was from Europe. The Greater China region and Japan accounted for 14.7% and 7.1% of Apple’s total revenue, respectively. The company sourced the rest of its revenue (7.8%) from other parts of the Asia Pacific region.

Investment thesis

We have laid out our investment framework in Compounder Fund’s website. We will use the framework to describe our investment thesis for Apple.

1. Revenues that are small in relation to a large and/or growing market, or revenues that are large in a fast-growing market

Apple’s revenue in FY2020 is already a massive US$274.5 billion, with iPhones commanding US$137.8 billion, so where can the company find growth? Certainly not in the sale of iPhones, even though the smartphone market is actually much larger than Apple’s iPhone business.

According to Mordor Intelligence, the global smartphone market was US$715 billion in 2019 and is expected to reach US$1,352 billion in 2025. IDC, another market research firm, also paints a similar picture, with its estimation of Apple’s global smartphone market share at 13.6% in the second quarter of 2020. But the problem is that with smartphone penetration already at 50% in 2019 around the world (the USA was at 91%), it’s hard for Apple to grow unit sales for iPhones.

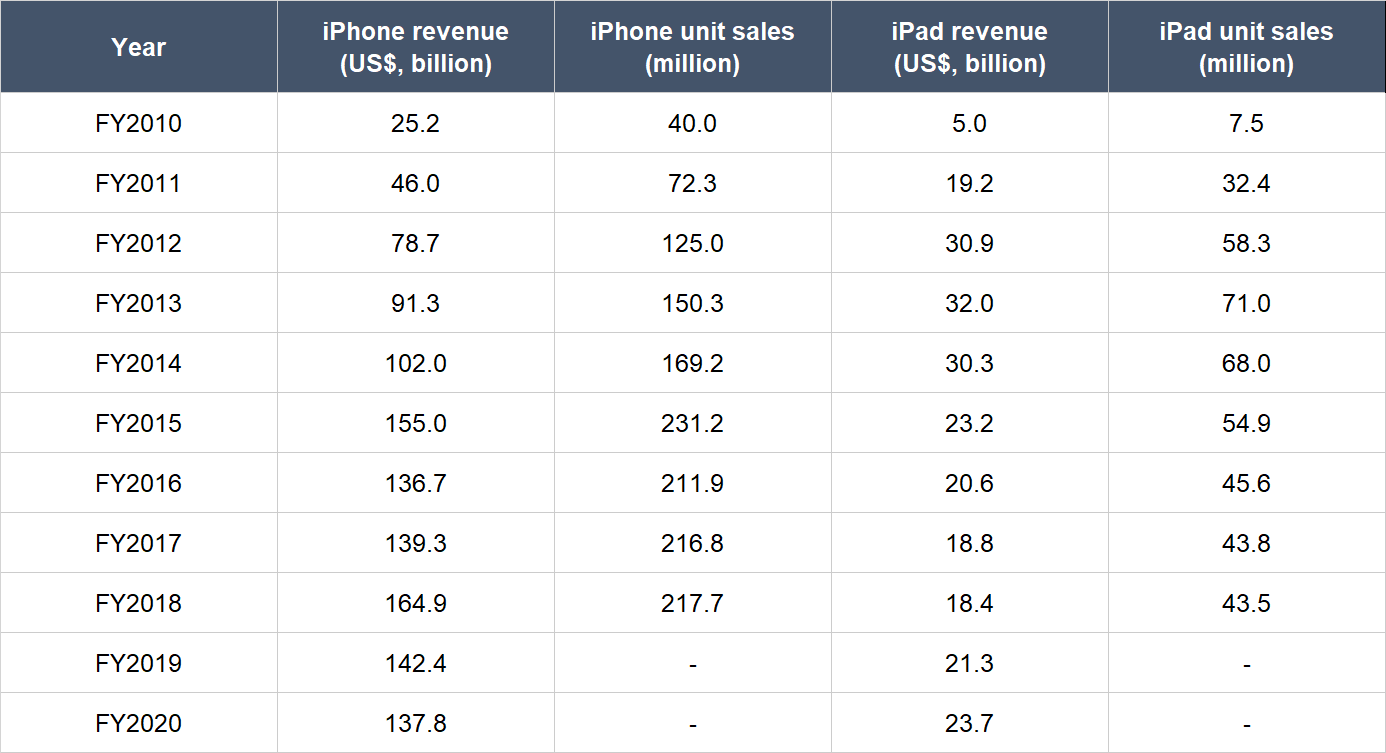

Indeed, the iPhone business has struggled to grow in recent years. The table below shows Apple’s iPhone revenue and unit-sales over the past 10 years from FY2010 to FY2020. There was strong growth in both numbers in the early years of this period. But then Apple’s iPhone revenue and unit-sales stagnated from FY2015 onwards (Apple stopped reporting iPhone unit sales in late 2018).

Source: Apple annual reports

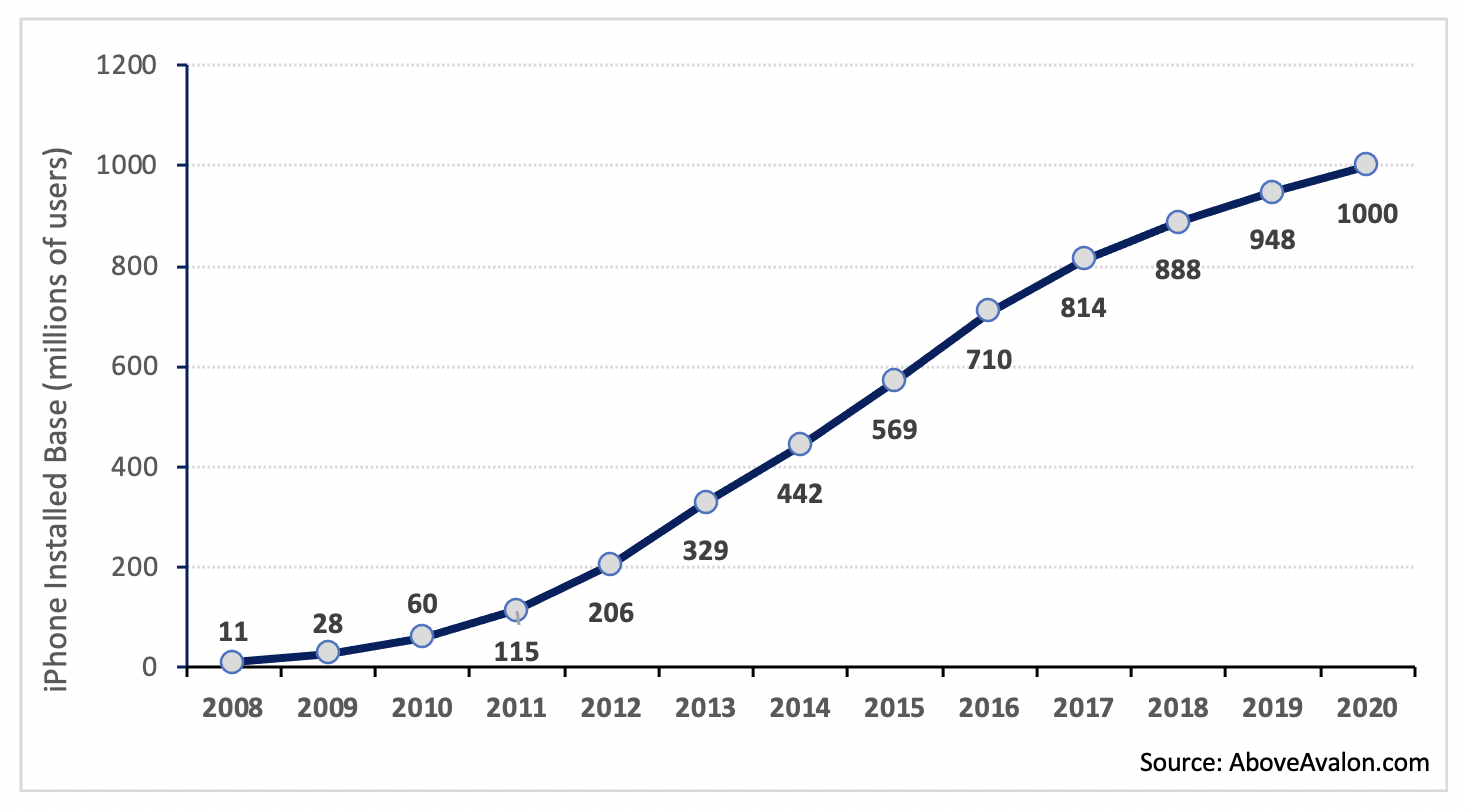

What can drive Apple’s overall growth is the installed base of active Apple devices. Apple only sporadically reveals this number but here’s what we know: The installed base increased from 1.3 billion active devices as of January 2018 to 1.5 billion as of January 2020; the installed base then reached new “all-time highs” in each of the second, third, and fourth quarters of FY2020. According to Above Avalon, a reputable website that analyses all-things-Apple, the installed base of active iPhones is currently 1 billion and has increased significantly over time (see chart below).

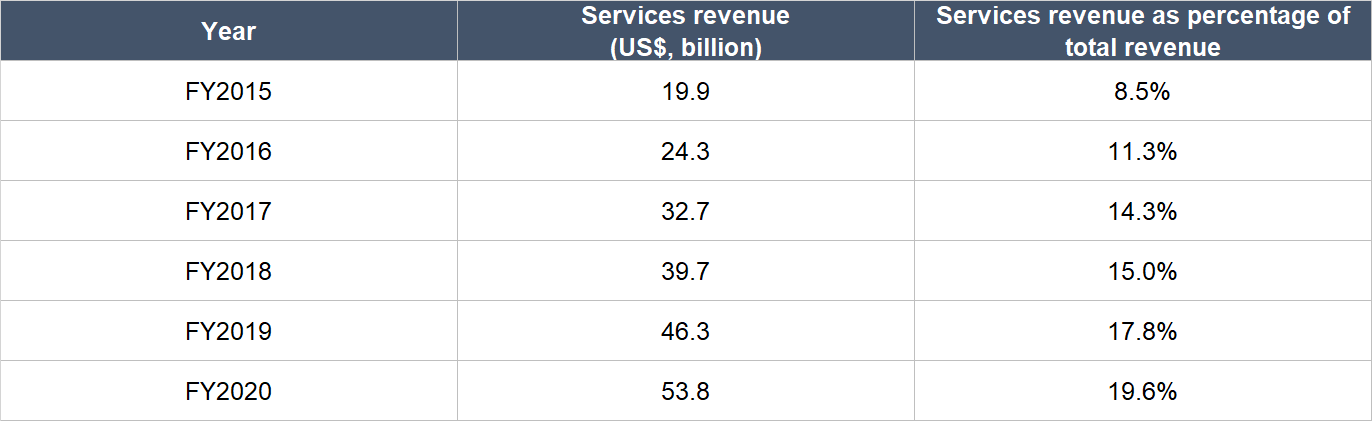

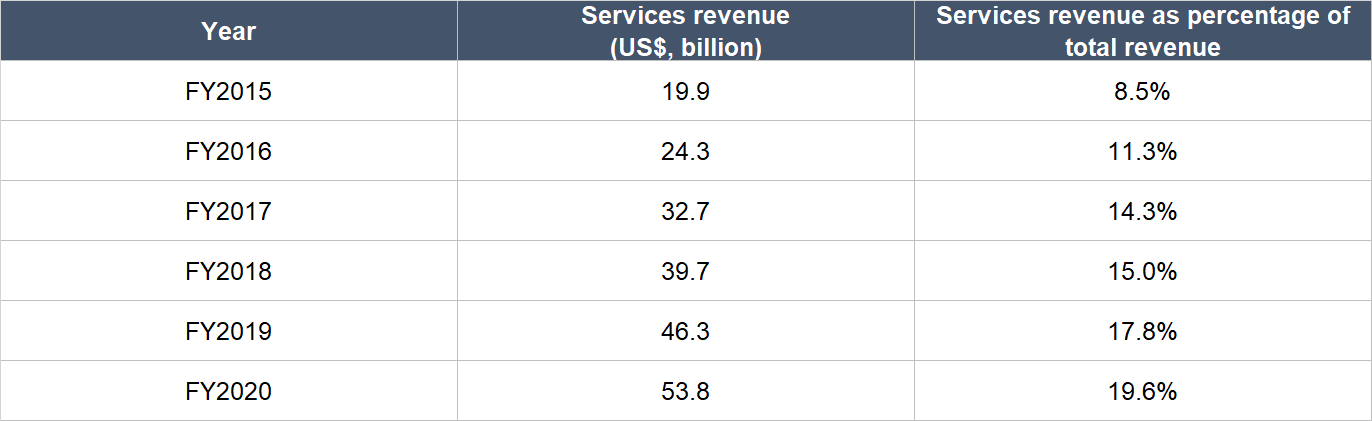

If each device generates only one-time revenue for Apple, the rise in Apple’s installed base of active devices in and of itself cannot provide the company with the room to grow. What it gives is an engaged base of Apple product-users for Apple’s Services business to monetise over time. And how effective Apple has been at driving growth in its Services business! The table below shows the consistently strong growth over the past few years in Apple’s Services revenue and number of paid subscriptions. In FY2020, Apple ended the year with a staggering 585 million paid subscriptions and US$53.8 billion in Services revenue.

Source: Apple annual reports and earnings conference calls

We want to highlight that Apple’s Services business does not depend on just the number of paid subscriptions that are supported by the company. For instance, there’s Apple Pay, which in the fourth quarter of FY2019 (the three months ended late-September 2019) clocked 3 billion transactions, exceeding the number of transactions handled by online payments juggernaut PayPal. Apple Pay’s revenue and number of transactions also “more than doubled year-on-year” during the same quarter. Quartz reported in February this year that Apple Pay accounted for around 5% of global card transactions, according to data from market research firm Bernstein.

At the end of the first quarter of FY2020 (the three months ended late-January 2020), Apple had an installed base of 1.5 billion active devices. Over the course of the year, the company steadily grew its installed base as mentioned earlier. But let’s just take it that Apple had an average installed base of 1.5 billion active devices in FY2020. The company generated US$53.8 billion in Services revenue during the year. This works out to an average Services revenue of just US$36 per device (US$53.8 billion divided by 1.5 billion devices) for the whole year. We think there’s ample room for Apple to grow its average Services revenue per device. For perspective, the cheapest Netflix subscription in the USA is currently US$8.99 per month, which works out to nearly US$108 per year.

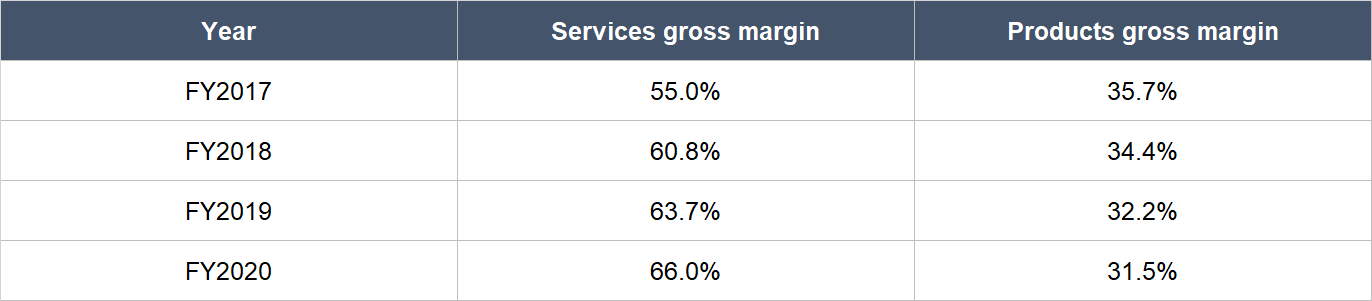

And the great thing about growth in Services revenue for Apple is that the business carries a significantly higher gross margin compared to Apple’s other businesses, and this gross margin has been improving over time. The table below shows the gross margins of Apple’s Services business and that of its products business over the past few years. If revenue from the Services business can continue to take up a larger share of Apple’s overall revenue over time, this could provide a strong boost to Apple’s bottom-line and cash flow.

Source: Apple annual reports

The other prong that could drive Apple’s overall Services revenue is the penetration rate of paid subscriptions. Right now, the number of paid subscriptions (585 million) is less than 40% of the total number of active Apple devices (more than 1.5 billion).

Apple’s iPhone has enduring popularity too, which we think results from the company’s sleek integration of both hardware and software to drive an ever-improving user experience. No one does this better than Apple, in our opinion, and it makes Apple incredibly hard to disrupt. In a 2018 article for his excellent newsletter Stratechery, business-writer extraordinaire Ben Thompson explained why this is so and we agree with him. He says it better than we can, so we’ll let you hear from him directly:

The first time Apple released two different iPhone form factors in the same year was 2013. There the new form factor was the iPhone 5C, but while the industrial design was new, the pricing wasn’t: the 5C slotted into the spot where the discontinued iPhone 5 would traditionally have gone — $100 less than the new flagship iPhone 5S. Analysts and pundits were aghast: how could Apple not produce a truly low-price iPhone? Didn’t they know this guaranteed disruption?

I argued to the contrary in a piece entitled What Clayton Christensen Got Wrong. After recounting the many predictions by the father of disruption that the iPhone would not be a success, I came up with three specific reasons why Apple seemed immune to disruptive gravity:

- First, it was folly to presume that consumers were rational, at least to the extent that rationality could be reduced to easily articulable features balanced against price (or appreciating that round numbers aren’t anything special).

- Second, there are many attributes of a product that can’t be easily measured, but only experienced, and that they loom large when the person using the product is the same as the person buying the product.

- Third, that modular products, by virtue of their prioritization of standardization and interconnectivity, would inevitably fall short on attributes directly connected to the experience of using the device.

The key paragraph is here:

“The attribute most valued by consumers, assuming a product is at least in the general vicinity of a need, is ease-of-use. It’s not the only one — again, doing a job-that-needs-done is most important — but all things being equal, consumers prefer a superior user experience. What is interesting about this attribute is that it is impossible to overshoot.”

The term “overshoot” is right out of disruption theory. Christensen writes in his seminal book, The Innovator’s Dilemma:

“The second element of the failure framework, the observation that technologies can progress faster than market demand…means that in their efforts to provide better products than their competitors and earn higher prices and margins, suppliers often “overshoot” their market: They give customers more than they need or ultimately are willing to pay for. And more importantly, it means that disruptive technologies that may underperform today, relative to what users in the market demand, may be fully performance-competitive in that same market tomorrow.”

This was the basis for insisting that the iPhone must have a low-price model: surely Apple would soon run out of new technology to justify the prices it charged for high-end iPhones, and consumers would start buying much cheaper Android phones instead!…

… Bezos’s letter, though, reveals another advantage of focusing on customers: it makes it impossible to overshoot. When I wrote that piece five years ago, I was thinking of the opportunity provided by a focus on the user experience as if it were an asymptote: one could get ever closer to the ultimate user experience, but never achieve it:

In fact, though, consumer expectations are not static: they are, as Bezos’ memorably states, “divinely discontent”. What is amazing today is table stakes tomorrow, and, perhaps surprisingly, that makes for a tremendous business opportunity: if your company is predicated on delivering the best possible experience for consumers, then your company will never achieve its goal.

What Thompson is saying is that so long as the iPhone is competing based on the user experience, it will never be able to overshoot customer-expectations, and thus will likely not be disrupted by cheaper smartphones. This assumes that the user experience the iPhone provides will continue to be superior compared to other smartphone manufacturers. Apple has no shortage of competitors (there’s Huawei, Samsung, and Xiaomi to name a few) but we don’t see any signs that the iPhone is losing its lead in the user experience area. During Apple’s earnings conference call for the fourth quarter of FY2020, CFO Luca Maestri commented that “in the U.S., the last survey of consumers from 451 Research indicates iPhone customer satisfaction of 98% for iPhone 11, 11 Pro and 11 Pro Max combined.” So, we think that the iPhone will be able to provide a robust platform for the future growth of Apple’s installed base of active devices.

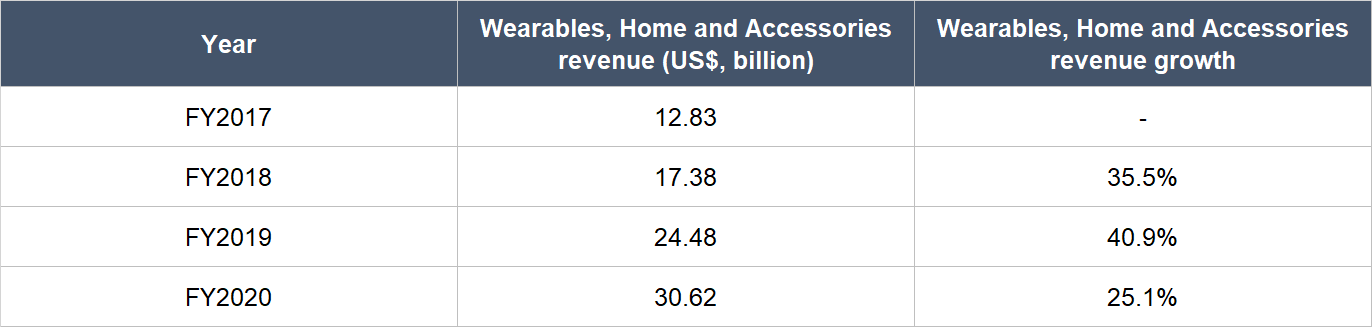

Another important pillar that we think can drive growth in Apple’s installed base will be the products from the Wearables, Home, and Accessories category. This is another area of strong growth for Apple in the past few years, as the table below illustrates.

Source: Apple annual reports

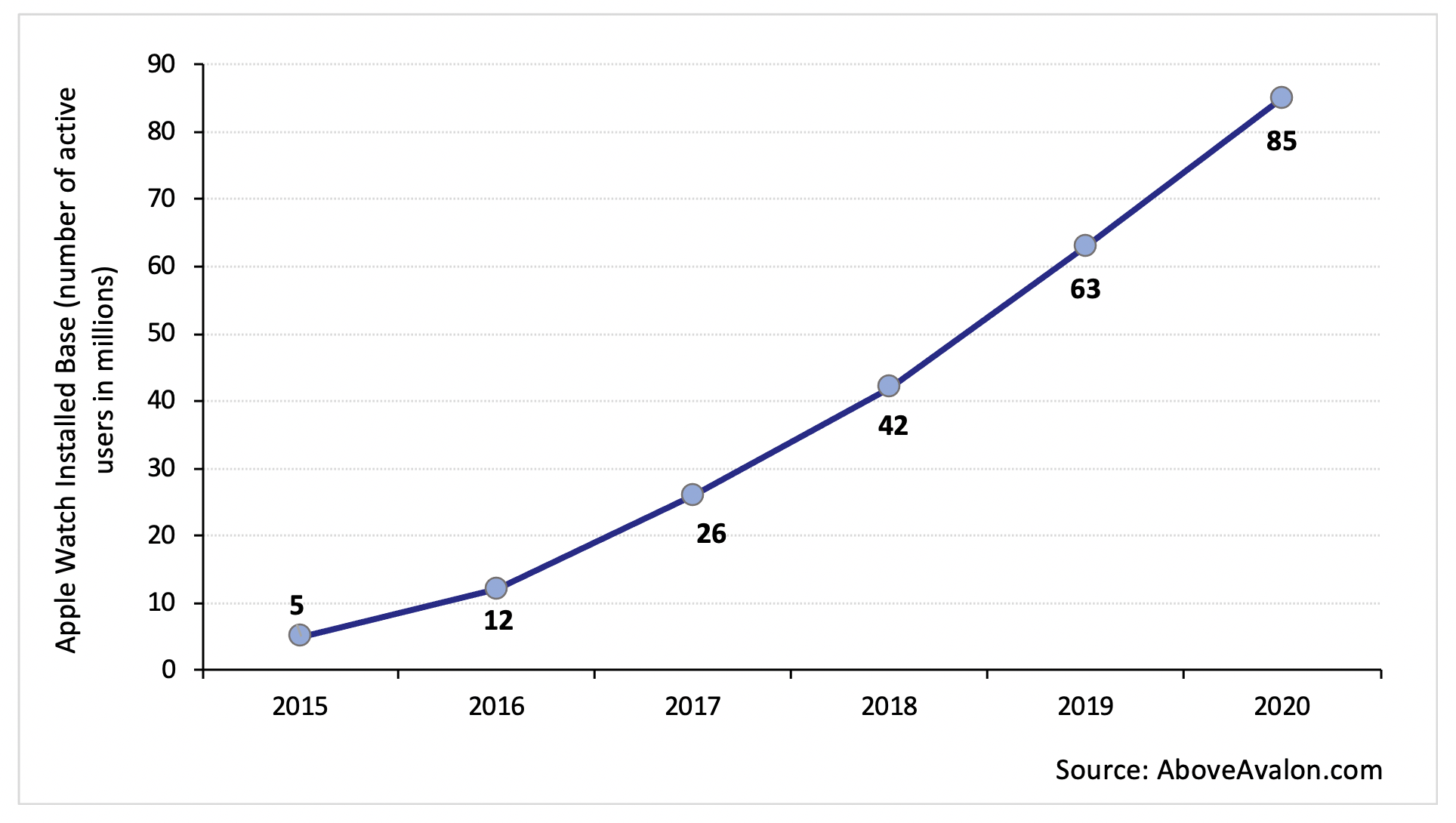

In particular, the Apple Watch’s potential to be an important piece of society’s connected-health ecosystem is intriguing. The Apple Watch contains a whole host of health-monitoring features. And last month, Apple partnered the government of Singapore (we live in Singapore) to launch LumiHealth. It is a first-of-its-kind program that “uses technology and behavioral insights to encourage Singaporeans to keep healthy and complete wellness challenges through their Apple Watch and iPhone,” according to Apple CEO Tim Cook. Above Avalon estimates that there were already 81 million active Apple Watches at the end of June 2020 and that the installed base should cross 100 million soon (if it hasn’t already). The Apple Watch’s installed base has also grown rapidly over time.

The last thing we want to discuss about Apple’s market opportunity is that Apple could also have new products in its pipeline. For instance, there’s no secret that the company has an interest in developing self-driving vehicles. In another instance, there are rumours that Apple could release a smart glasses product, which has apparently been in development for a decade, in 2022. We are not hanging our hats on any of Apple’s new products to be wildly successful. But if they do, we won’t be surprised.

2. A strong balance sheet with minimal or a reasonable amount of debt

Apple currently has a very healthy balance sheet. As of 26 September 2020, Apple’s cash and investments totaled US$191.8 billion (consisting of US$38.0 billion in cash and cash equivalents, and US$153.8 billion in short- and long-term marketable securities). With total debt of US$112.4 billion, Apple has a net cash position of a staggering US$79.4 billion.

During Apple’s earnings conference call for the first quarter of FY2018, management signalled their intent to gradually bring Apple’s net cash position to zero. To be clear, Apple’s management wants the company’s cash and debt to balance to zero in the future. Back then, Apple’s net cash position was US$163 billion.

To bring Apple’s net cash position to zero would mean Apple will weaken its balance sheet by spending serious cash on reinvesting into its business, acquisitions, paying a dividend, and/or buying back shares. We have no issues with any of these activities if they’re done sensibly and as we’ll discuss in detail later, we think Apple has steady hands at the helm in the form of CEO Tim Cook.

Moreover, as we’ll also show later, Apple has displayed a prodigious ability to generate cash flow from its business. In our opinion, this lowers the financial risks Apple has to face when its net cash position becomes zero in the future.

3. A management team with integrity, capability, and an innovative mindset

On integrity

Apple is led by CEO Tim Cook, who took over in August 2011 from the company’s legendary co-founder Steve Jobs . Prior to becoming CEO, Cook was Apple’s chief operating officer (COO), a post he was given in October 2005.

We think Cook’s compensation structure exhibits integrity. For FY2019, Cook’s compensation consisted of two components. First, there’s a total of US$11.6 million in salary (US$3.0 million), non-equity bonuses (US$7.67 million), and other items (US$0.88 million). The second component is the most important and it consisted of the vesting of 560,000 Apple shares. At the time of vesting (24 August 2019), these shares were worth around US$113.5 million. That’s a princely sum, but it’s basically a rounding error when compared to the scope of Apple’s business – in FY2019, Apple’s net income and free cash flow were US$55.3 billion and US$58.9 billion, respectively.

Back in FY2019, Cook last received an equity award when he was promoted to CEO in August 2011. The 560,000 Apple shares he received in FY2019 was part of the 2011 equity award. Of the 560,000 shares, 280,000 depended on Apple’s total shareholder return over a three year period from 25 August 2016 to 24 August 2019. The 280,000 shares in question would vest only if Apple’s total shareholder return for the three years was in the top-third among companies in the S&P 500 index. If Apple’s total shareholder return for the period was in the bottom-third, none of the 280,000 shares would vest. Meanwhile, the remaining 280,000 Apple shares (those that did not depend on Apple’s total shareholder return) vested according to the amount of time that has passed since 2011. So it’s clear that the lion’s share of Cook’s compensation in FY2019 depended on multi-year changes in Apple’s stock price, which in turn, was driven by the company’s business performance. We think this structure exhibits integrity – it is well-designed and strongly aligns the interests of Cook with Apple’s other shareholders.

We also want to discuss a fact about Cook’s aforementioned compensation structure that we think highlights his strong moral fibre. In 2013, Cook requested for a significant change to the structure of his 2011 equity award. Originally, the 2011 equity award vested only according to time. Cook wanted to introduce tiered-vesting that is based on Apple’s total shareholder return over a multi-year period. The change created significant downside risk for Cook that was not present in the original structure of the 2011 equity award.

Recently in late September 2020, Cook was given an equity award of nearly 668,000 Apple shares that are worth US$77.5 million at Apple’s share price of US$116 as of 27 November 2020. This is the first equity award granted to Cook since his 2011 award that we discussed above. Half of the ~668,000 shares would vest over a multi-year period (one-third on April 2023, another third on April 2024, and the last third on April 2025), and the other half would vest according to Apple’s total shareholder return over a three year period from the first day of FY2021 to the last day of FY2023. This is again, a very well-designed compensation scheme, in our opinion.

The other key leaders in Apple also saw the majority of their compensation in FY2019 come from equity awards. The awards have two components: (1) Apple shares that vest over four-and-a-half years; and (2) Apple shares that vest according to the company’s total shareholder return over a three-year period from the beginning of FY2019 to the end of FY2021. We like this. Most of Apple’s other key leaders, besides Cook, also have multi-year tenures of more than five years at the company, and we appreciate the experience they have.

And one last thing on the alignment of interest between Apple’s leaders and shareholders: As of 2 January 2020, Cook controlled 3.39 million Apple shares that are worth more than US$390 million at the 27 November 2020 share price of US$116.

On capability and ability to innovate

The late Steve Jobs was a true visionary. Under his leadership, Apple introduced the iPhone in June 2007, a device which has profoundly shaped the global digital economy. We don’t think Tim Cook’s in the same league as Jobs in terms of daring and ingenuity. But we still rate Cook highly on execution and innovation. There are a number of things we want to discuss.

First, as mentioned earlier, Cook was Apple’s COO for around six years before he became CEO. As COO, Cook was instrumental in (1) managing Apple’s complex supply chain and manufacturing activities and (2) fine-tuning them into world-class systems. In Cook’s current role as CEO, he continues to keep a close watch on Apple’s manufacturing activities and supply chain. It has been over nine years since Cook has been CEO of Apple. In this time, Apple has rarely, if ever, encountered manufacturing problems that have caused significant disruptions to its business. And crucially, the iPhone’s features have improved considerably over time, so the complexities involved with manufacturing iPhones must have grown too – this makes Apple’s lack of any major manufacturing issues even more impressive.

Second, we showed earlier that Apple has seen strong growth in its Services business in the past few years. Apple’s move towards services such as digital payments, the App Store, on-demand TV streaming, iCloud, and more, are a testament to our view that innovation is still happening at the company under Cook’s watch. The table below shows the increase in Apple’s Services revenue as a percentage of total revenue since FY2015:

Source: Apple annual reports

Third, Apple’s Wearables, Home, and Accessories category has also produced admirable results in the past few years as we discussed earlier. We also mentioned that the Apple Watch, which was first released in April 2015, a few years after Cook became CEO, has seen its installed base grow to an impressive 81 million as of June 2020. We credit Cook for the development and growth of the Apple Watch product. And speaking of product-growth, we think the iPhone and the iPad are worth mentioning too. These two products were first launched by Apple in June 2007 and January 2010, respectively. So even though Cook’s likely not the one who dreamed up the first versions of these products, he still has been involved with them as Apple’s CEO for more than nine years now. Both products saw explosive revenue growth in their earlier years. And although their growth has slowed in recent times, they still generate significant revenues for Apple. The table below shows Apple’s revenues from the iPhone and iPad since FY2010. We think Cook deserves significant credit for the longevity of both products.

Source: Apple annual reports

Fifth, since Cook’s appointment as CEO, Apple has continued to churn out gobs of free cash flow, as we’ll show later. And just as importantly, we think Cook has done a tremendous job in allocating the torrent of cash that Apple’s business generates. From the end of FY2012 to the end of FY2020, Apple’s share count declined considerably by a total of 33.8% because of share buybacks. Given the sharp increase in Apple’s share price over the same period, we think the buybacks that have taken place under Cook’s stewardship have proven to be a masterstroke.

4. Revenue streams that are recurring in nature, either through contracts or customer-behaviour

Existing iPhone users may not be buying a new iPhone every year. But we have good reason to believe that iPhone users tend to purchase new iPhones when they change their mobile devices and this creates a form of recurring revenue for Apple through repeat customer purchases:

- User-surveys often indicate extremely high customer satisfaction with the iPhone. Earlier in this article, we shared Apple CFO Luca Maestri’s comment in the FY2020 fourth-quarter earnings conference call that “in the U.S., the last survey of consumers from 451 Research indicates iPhone customer satisfaction of 98% for iPhone 11, 11 Pro and 11 Pro Max combined.” Similar language has appeared in Apple’s earnings conference calls over the past few years.

- Also earlier in this article, we referenced data from Above Avalon showing that Apple’s installed base of active iPhones has increased significantly over time.

Beyond iPhones, Apple’s Services business is likely to be mostly recurring in nature too. For example, revenue from subscriptions to services such as iCloud and Apple Music tend to recur as customers automatically renew their contracts. Apple also takes a cut from transactions made via Apple Pay and payments is a type of activity that users make all the time.

5. A proven ability to grow

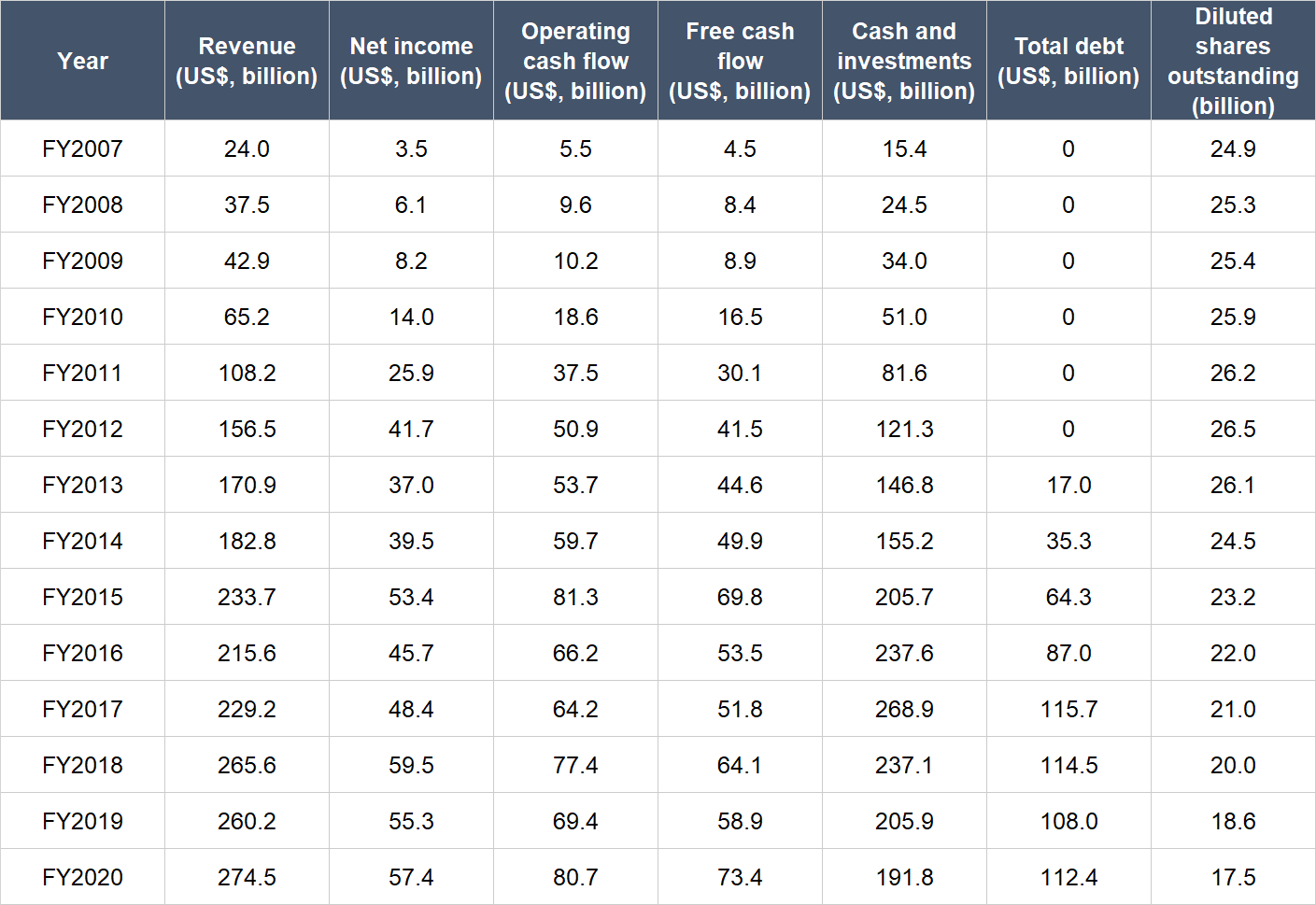

The table below shows the important financials for Apple going back to FY2007, the year of the iPhone’s first launch:

Source: Apple annual reports

There are a few important things to unpack from the table above:

- Apple’s revenue has compounded at an impressive rate of 20.6% per year from FY2007 to FY2020. But annual growth over the past five years from FY2015 to FY2020 has grounded to a halt at just 3.3%.

- In a similar manner to revenue, net income has compounded impressively at 24.0% from FY2007 to FY2020, but increased at an anaemic pace of just 1.5% per year from FY2015 to FY2020.

- The growth-dynamics of Apple’s operating cash flow and free cash flow are similar to its revenue and net income. For the entire timeframe we’re looking at (FY2007 to FY2020), Apple’s operating cash flow and free cash flow grew by 23.0% and 24.0% per year, respectively. For 2015 to FY2020, Apple’s operating cash flow actually shrank by 0.1% annually while free cash flow inched up by just 1.0% per year.

- Apple is a machine when it comes to generating cash. The company’s free cash flow margin (free cash flow as a percentage of revenue) averaged at an impressive 24.7% from FY2007 to FY2020. In FY2020, the free cash flow margin was 26.7%.

- Apple’s balance sheet has been rock-solid throughout the entire timeframe under study, with the amount of debt being either zero or considerably lower than the amount of cash and investments. As mentioned earlier, Apple intends to bring its net cash position to zero over time (as a reminder, we’re not worried about this) and this intention can be clearly seen in the narrowing net cash position of the company from US$153.2 billion in FY2017 to US$79.4 billion in FY2020.

- Apple has not diluted shareholders at all. In fact, the company’s diluted share count has declined by 5.0% per year from FY2012 (the first full year with Tim Cook as CEO) to FY2020. This decrease in the share count has helped Apple’s net income and free cash flow per share to grow at faster rates than the actual numbers. For perspective, Apple’s net income grew by 1.5% per year from FY2015 to FY2020, but increased by 7.3% annually on a per share basis. Similarly, Apple’s annual free cash flow growth over the same period was merely 1.0%, but free cash flow per share climbed by 6.8% per year. Apple has been aggressively returning capital to shareholders (in the form of share buybacks and dividends) and we’ll discuss this shortly.

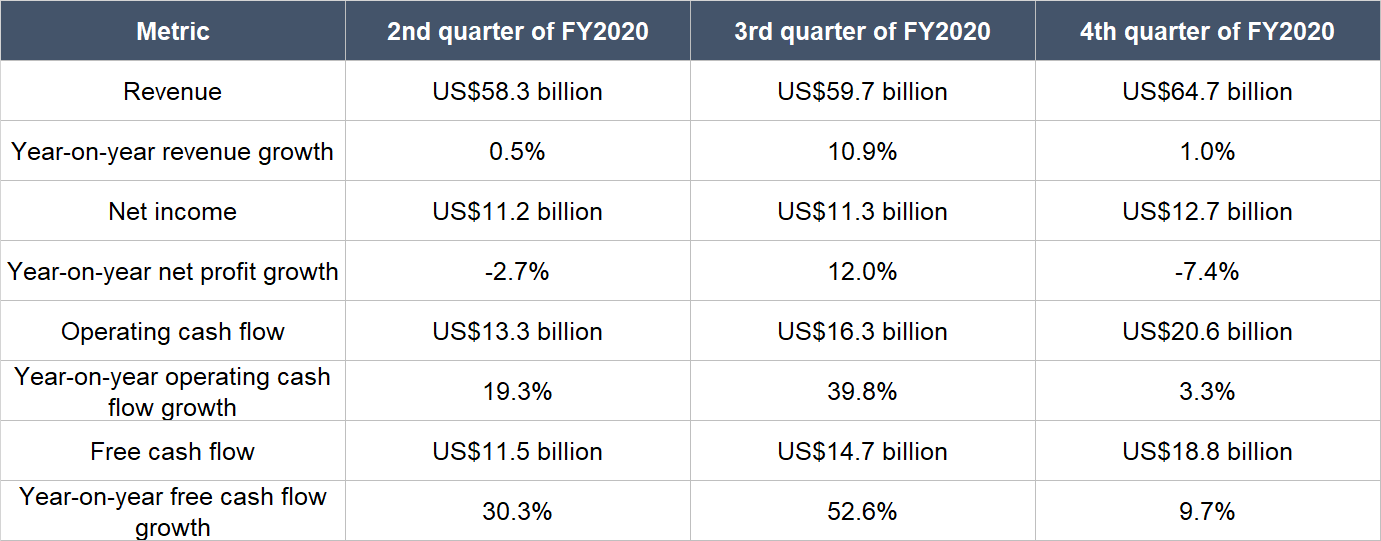

During the last three quarters of FY2020, Apple was contending with COVID-19. But the company still managed to produce revenue and cash flow growth in all three quarters. This is shown in the table below:

Source: Apple quarterly financials

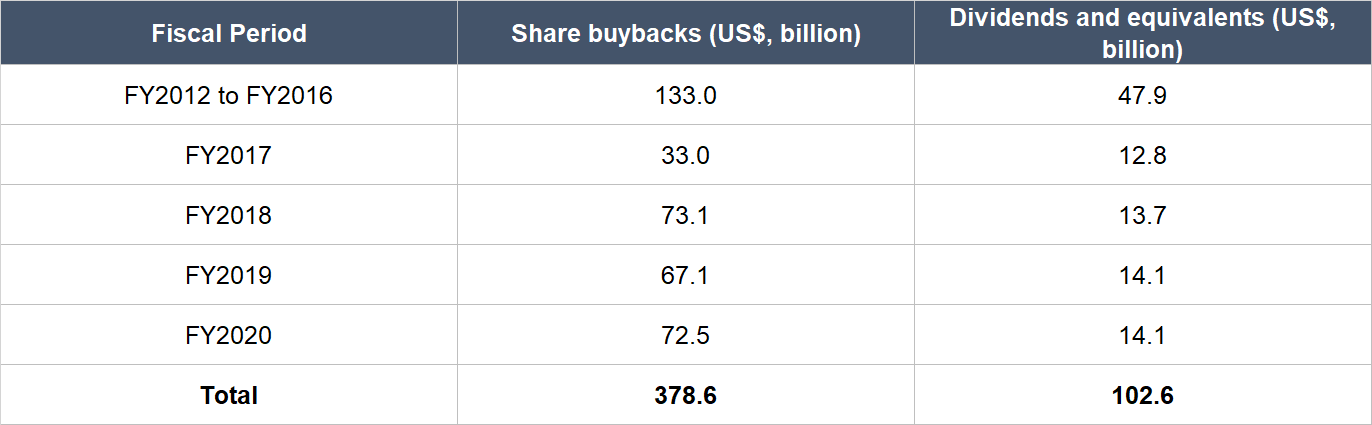

As promised, the table below illustrates the tremendous amount of capital Apple has returned to investors in the form of share buybacks and dividends since FY2012. Apple still has ample ammunition to continue doing so, given its robust balance sheet and prodigious ability to generate free cash flow. And remember, the company has the intention to bring its net cash position to zero over time, so it’s likely that Apple will continue to return capital to shareholders via buybacks and dividends.

Source: Apple filing

6. A high likelihood of generating a strong and growing stream of free cash flow in the future

Earlier in this article, we showed clearly that Apple generates a lot of cash from its business. There’s no reason for us to believe that Apple’s free cash flow margin will shrink in the future. In fact, if Apple’s revenue-mix continues to shift towards the higher-margin Services business over time (as we think it would), the company’s overall free cash flow margin is likely to improve.

We also believe that Apple can produce annual revenue growth in the high-single digit percentage range over the next few years. In our opinion, this growth will be driven by Apple’s services and wearables businesses. And there could also be icing on the cake if Apple introduces any new product categories that turn out to be big hits with consumers and/or enterprises. So if Apple can indeed grow its revenue while widening its free cash flow margin, the company will be producing more cash flow in the years ahead compared to today.

Valuation

We like to keep things simple in the valuation process. In Apple’s case, we think the price-to-earnings (P/E) and price-to-free cash flow (P/FCF) ratios are appropriate metrics to gauge the value of the company. This is because Apple has been extremely adept at producing both for many years.

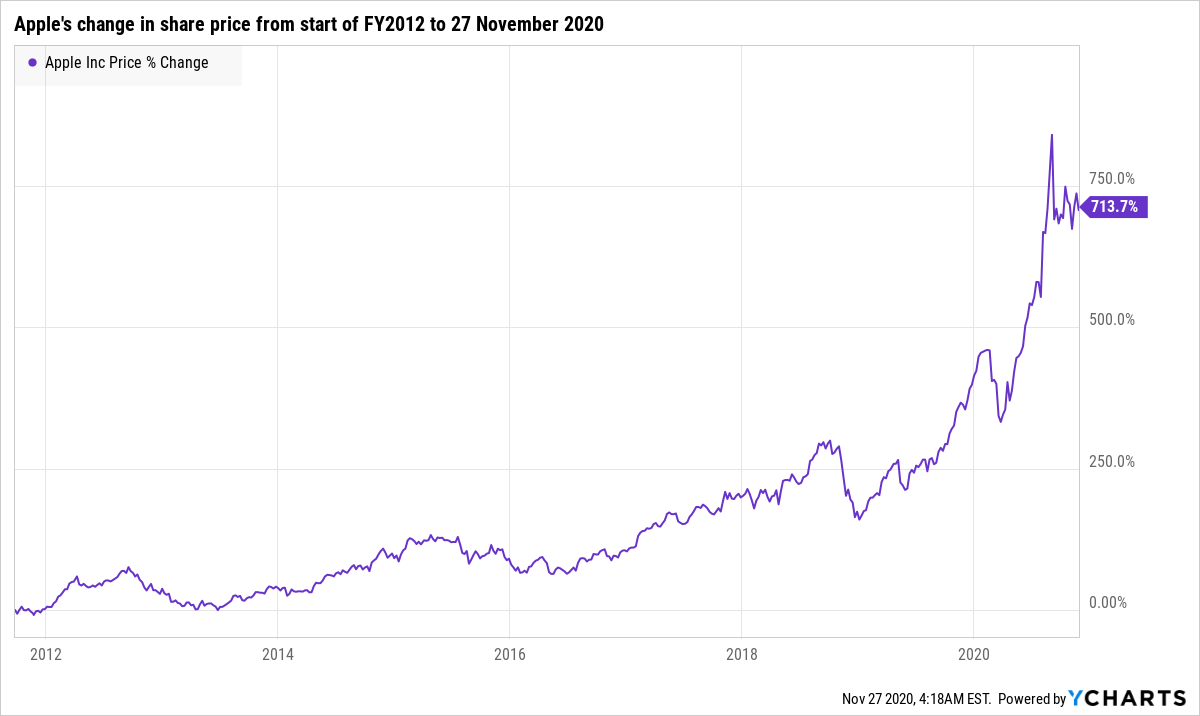

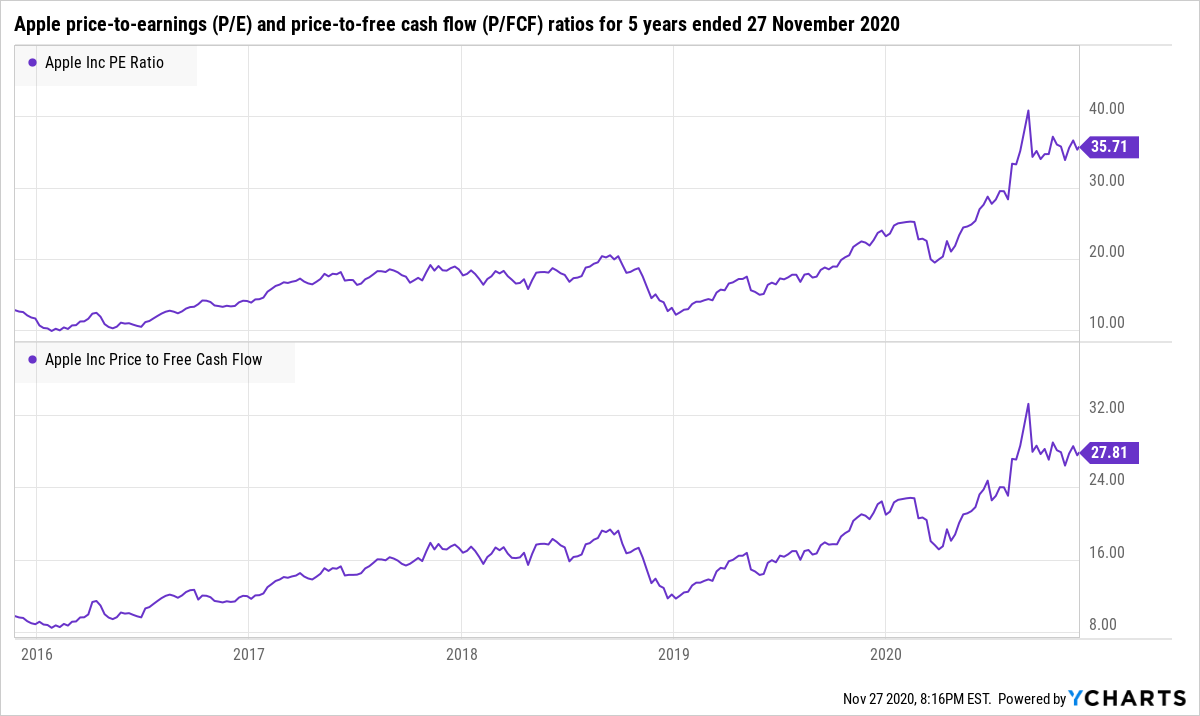

We completed our purchases of Apple shares with Compounder Fund’s initial capital in early August 2020. Our average purchase price was US$100 per Apple share. At our average price and on the day we completed our purchases, the company’s shares had trailing P/E and P/FCF ratios of around 30 and 25, respectively. These ratios are high relative to their histories. Here’s a chart showing Apple’s P/E and P/FCF ratios over the five years ended 27 November 2020:

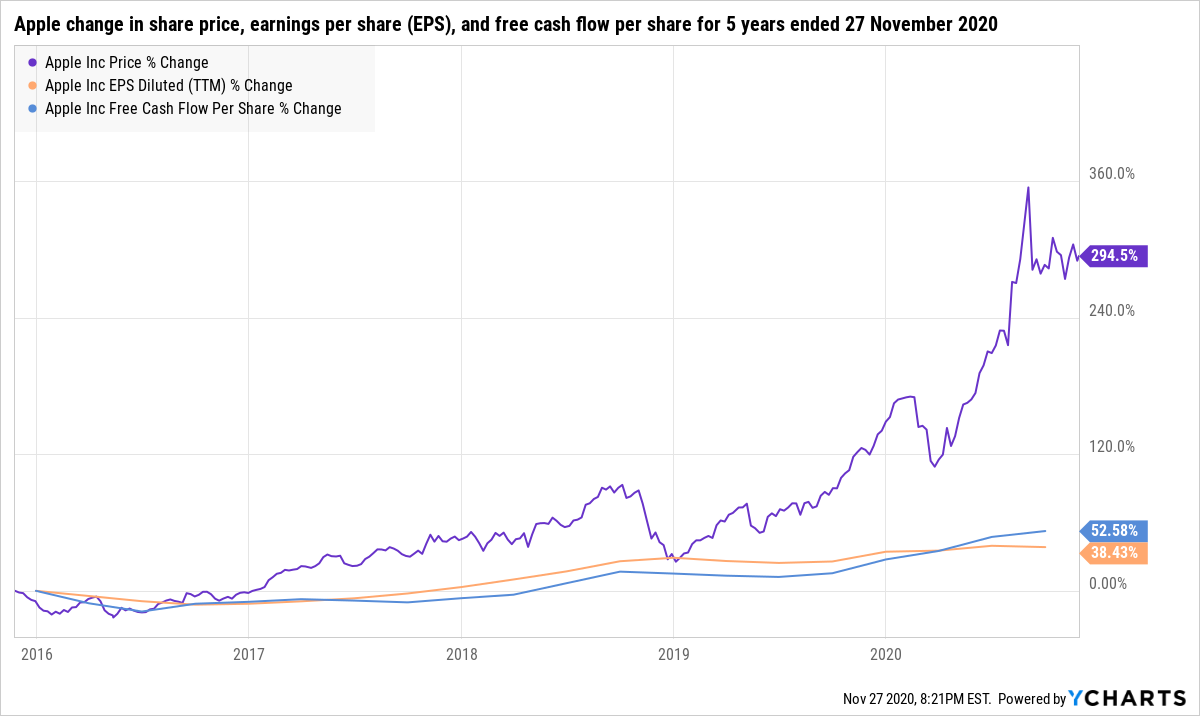

Moreover, Apple’s share price has risen much faster than its earnings and free cash flow in the past five years as the chart below illustrates:

But we think Apple deserves the higher valuation ratios it carries today. This is because of the ongoing shift in Apple’s revenue mix toward services, which improves the stability of the company’s business. In addition, we think Apple’s earnings and free cash flow per share should be able to grow annually, at the very least, in the mid-teens percentage range over the next few years. Apple’s valuation ratios look very reasonable to us when seen in the context of the company’s potential growth. The key drivers for the growth in Apple’s earnings and free cash flow per share will be (1) the high-single digit annual revenue growth that we believe Apple can produce over the same timeframe, and (2) the continued reduction in the company’s share count through large-scale share buybacks.

For perspective, Apple carried P/E and P/FCF ratios of 35 and 28, respectively, at the 27 November 2020 share price of US$116.

The risks involved

There are a few risks with Apple that we’re watching. In no particular order…

Concentration risk: Apple still relies heavily on iPhone sales (half of the company’s revenue in FY2020 came from the iPhone), even though we note that the company will be more focused on growing its Services revenue in the future. We believe that Apple has a sticky customer base – built from the company’s intense focus on the user experience – that can fend off competition. But the smartphone market is highly competitive and there’s a chance that other smartphone makers could eventually come up with products that beat the iPhone in terms of the user experience.

“Elephant” risk: As Apple grows larger, delivering more growth becomes a bigger challenge. We think the company’s up for it. But we also note that at over US$274 billion in annual revenue today, Apple needs to earn an extra US$13.7 billion in sales next year just to grow its top-line by 5%. From there, the revenue growth hurdle will keep rising.

Valuation risk: We believe that Apple’s current valuation is very reasonable. But the company’s P/E and P/FCF ratios have also been around 10 or below in the past few years. A compression in Apple’s valuation ratios could happen in the future, especially if growth in Apple’s Services business stalls.

Key-man risk: Tim Cook has been leading Apple for more than nine years now. We think he’s a solid leader and we would like to see him continue as CEO in the years ahead. If he leaves, we’ll be watching the leadership transition. The good thing is that at only 59 years old now, Cook is still relatively young, so he likely still has plenty of gas left in the tank to continue leading Apple. Another smaller key-man risk we’re watching relates to Jonathan Ive, the previous leader of Apple’s design team. Ive left Apple sometime in 2019, after leading the team responsible for designing Apple’s products since 1996, to set up his own industrial design company, LoveFrom. Apple’s apparently a customer of LoveFrom. In our study of Apple’s history, we see Ive as a central character. We think the aesthetics of Apple’s products are a key reason why they’re so well-loved by consumers, so Ive has been instrumental in building the company’s tremendous brand power. We think Cook has so far navigated the departure of Ive well, but we’re keeping an eye on the situation.

Regulatory risk: In the USA, Apple is under scrutiny from the public and lawmakers. For example, Tim Cook had to testify before US lawmakers in July this year on antitrust issues, alongside three other major US tech companies (Alphabet, Amazon, and Facebook). Then in August, Epic Games, the developer of the popular computer game “Fortnite”, sued Apple because of concerns Epic Games has over the pricing policies of Apple’s App Store. The lawsuit is ongoing. Earlier this month, Apple voluntarily cut its App Store commission rate to 15% for software developers that earn less than US$1 million in annual revenue from the platform; previously, Apple took a 30% commission from the total price of paid-apps and in-app purchases from the App Store. Interestingly, only 0.2% of the 1.8 million apps in the App Store generated more than US$1 million in revenue in 2019, and the 0.2% of apps in question accounted for 92% of Apple’s total App Store revenue, according to data from research firm Sensor Tower. So Apple’s latest move to lower its App Store commission rate could be seen as the company trying to prevent itself from having to face formal accusations from regulators that it is abusing the power of the App Store. But if regulators do decide to step in and lower the App Store’s overall take-rate for all apps, it could severely dent the growth of Apple’s Services business.

Geopolitical risk: China is an important market for Apple, accounting for nearly 15% of total revenue in FY2020. But the governments of the USA and China aren’t exactly on the best of terms at the moment. With Apple being a prominent American company, it could face a backlash from the Chinese government if tensions between the two global superpowers do not ease up. Apple could also be harmed by any decisions the US government makes in relation to China. For example, in August this year, the US government wanted to ban the use of the WeChat app in iPhones. WeChat is a superapp from the Chinese technology giant Tencent that has 1.2 billion users (mostly in China) as of 30 September 2020. The ban order is currently on hold, but if it is eventually upheld, demand for iPhones in China could fall substantially. Here’s an excerpt on the matter from an August 2020 South China Morning Post article:

“When it comes down to it, though, it seems few will struggle to choose between iPhones and WeChat. In a Weibo poll asking people whether they would switch to a new smartphone or uninstall WeChat if the app disappears from iOS, more than 1.2 million out of 1.3 million people who voted indicated that they would get a new phone.”

Summary and allocation commentary

To sum up Apple, it has:

- Room for growth – despite its already massive revenue base – because of the potential for its installed base of active devices to increase over time which, in turn, can drive higher adoption of the company’s Services business

- A rock-solid balance sheet with significantly more cash and investments than debt

- Tim Cook, a highly capable, innovative CEO, who also has a strong moral fibre

- Recurring revenue streams that come from repeat-customer purchases of the iPhone (even though there may be a long time gap between each purchase) and repeat-use of the various services in Apple’s portfolio

- A proven track record of long-term growth; even though Apple’s growth in more recent years has ground to a halt, we believe it can pick up again because of strength in the Services business

- A high chance of being able to produce strong free cash flow in the future; Apple has a prodigious history in generating free cash flow and a high possibility of enjoying increasing free cash flow margins over time as its Services business grows in prominence

There are risks with Apple that we see. These risks include revenue-concentration from a single product line; difficulty in growing because of how large its business already is; valuation ratios that are high in relation to history; key-man risk; and threats to the company’s business from (1) regulatory actions from US government and (2) any actions by the governments of the USA and China that arise from their quarrels.

After weighing the pros and cons, we initiated a 2.5% position – a medium-sized allocation – in Apple with Compounder Fund’s initial capital. We think Apple is in the middle of an interesting transformation, where the prominence of the Services business would increase over time from its current level of around 20% of Apple’s overall revenue. We’re also highly impressed with the company’s ability to generate free cash flow and with Tim Cook (even though we acknowledge that he’s not in the same league as Steve Jobs when it comes to visionary innovation). But our enthusiasm is tempered by the sheer size of Apple’s current business – the larger the business, the harder it is to grow.

And here’s an important disclaimer: None of the information or analysis presented is intended to form the basis for any offer or recommendation; they are merely our thoughts that we want to share. Of all the companies mentioned in this article, Compounder Fund also currently owns shares in Alphabet, Amazon, Facebook, Netflix and PayPal. Holdings are subject to change at any time.