Compounder Fund: Alphabet Investment Thesis - 18 Jan 2021

Data as of 13 January 2021

Alphabet Inc (NASDAQ: GOOGL), which is based and listed in the USA, is one of the 40 companies in Compounder Fund’s initial portfolio. This article describes our investment thesis for the company.

Company description

Alphabet is the holding company of many businesses, the largest of which is Google. In the first nine months of 2020, Alphabet earned US$125.6 billion in total revenue and Google contributed nearly all of it (US$125.0 billion).

Google should be a familiar name for most of you reading this, but it is much more than its eponymous internet search engine. The core products of Google include Android, Chrome, hardware, Google Cloud, Google Maps, Google Play, YouTube, and of course Google Search. Google is so ubiquitous that it is very likely that all of you reading this use one or more of its products every day – after all, Android, Chrome, Google Maps, Google Play, Search, and Youtube all had over one billion monthly active users each as of end-2019.

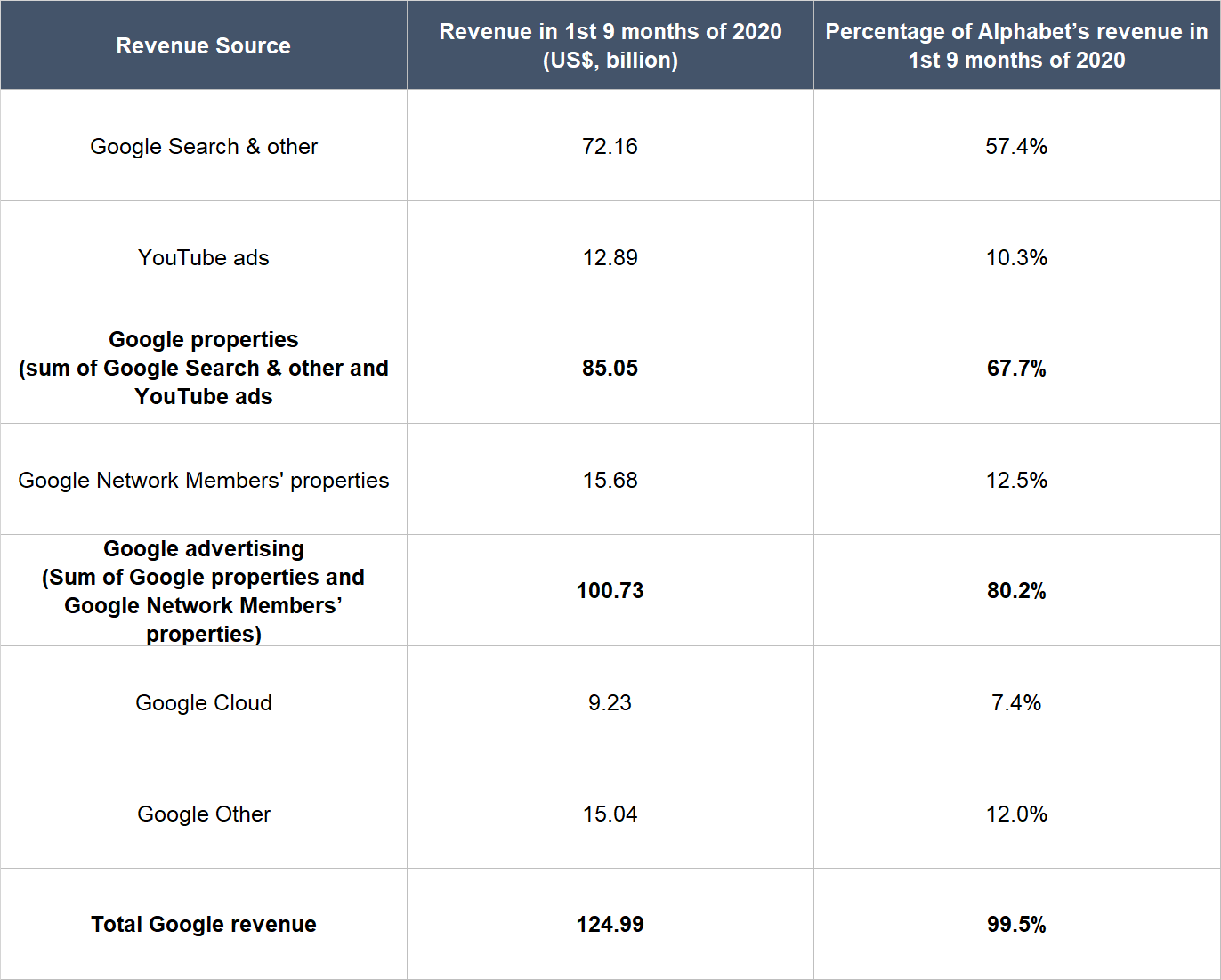

The table below shows a breakdown of Google’s revenue sources in the first nine months of 2020, and what percentage each source is of Alphabet’s overall revenue:

Source: Alphabet 2020 third-quarter earnings update

It’s clear that Google and by extension, Alphabet, relies heavily on advertising as a source of revenue. Google sells digital advertising space on its own properties, such as Gmail, Google Maps, Google Play, Google Search, and Youtube. Meanwhile, Google Network Members’ properties are third-party websites that advertisers can advertise on through Google’s digital advertising services such as AdMob, AdSense, and Google Ad Manager. For instance, if we wanted to, we could list our fund’s website (compounderfund.com) on Google Ad Manager and Google will direct advertisers to our website to advertise. Google will collect a fee from the advertiser and pay us a cut of it.

Google Cloud is where Google provides cloud-computing infrastructure, data analytics, and other services under the Google Cloud Platform banner. Instead of buying their own services, data centres, data storage, and more, companies can ‘rent’ these digitally through Google Cloud Platform by paying regular service fees. Google Cloud also provides the cloud-based Google Workspace productivity software products (such as Google Docs, Google Spreadsheets, and more) and earns revenue through subscriptions.

The Google Other category is where Alphabet lumps the remaining portion of Google’s revenues. Google Other’s revenue consists of: (1) in-app purchases and sales of apps and digital content from Google Play; (2) sales of hardware, including Pixelbooks, Pixel phones, the Google Nest smart-home device, and other products; (3) non-advertising revenue from Youtube, such as subscriptions to a premium-tier; and (4) other products and services.

In all, Google contributed 99.5% of Alphabet’s total revenue in the first nine months of 2020. Alphabet currently has only two business segments: Google, and Other Bets (the company will introduce Google Cloud as a separate segment starting from its 2020 fourth-quarter earnings update). Other Bets is where Alphabet houses all its other businesses, including Access, Calico, CapitalG, GV, Verily, Waymo, and X, among others. In the first nine months of 2020, Other Bets contributed US$461 million in revenue – 0.4% of Alphabet’s top-line – and this came primarily from Access and Verily.

From a geographical perspective, Alphabet is a pretty diversified company. Only 47% of its revenue in the first nine months of 2020 came from the USA. The next biggest region is Europe, Middle East, and Africa with a 30% contribution. The Asia Pacific and Other Americas regions accounted for 18% and 5%, respectively.

Investment thesis

We have laid out our investment framework in Compounder Fund’s website. We will use the framework to describe our investment thesis for Alphabet.

1. Revenues that are small in relation to a large and/or growing market, or revenues that are large in a fast-growing market

In the 12 months ended 30 September 2020, Alphabet earned total revenue of US$171.7 billion, of which advertising accounted for US$138.7 billion (80.8%). These numbers make Alphabet’s business seem massive, which it is. But there’s still plenty of room for Alphabet to run, in our opinion.

Let’s look at the digital advertising market first. According to a December 2020 report by Magna, the global advertising market fell by around 4% in 2020 to US$569 billion. But the global digital advertising market grew by 8% to US$336 billion. It’s worth noting that the global digital advertising space is fast-growing, having doubled from US$88 billion in 2012 to US$181 billion in 2016 according to data from Zenith. These numbers (US$569 billion for global advertising and US$336 billion for digital advertising) are much larger than Alphabet’s advertising revenue. And since Google’s products are ubiquitous, it should be able to continue winning its fair share of the pie. As mentioned earlier, the business has multiple products with more than one billion monthly active users; for another perspective, Google Search had 88% of global market share among internet search engines as of October 2020, according to Satistia.

Cloud computing is also another avenue for growth for Alphabet. According to a forecast from Gartner that was released in November 2019, the public cloud computing market is expected to grow by nearly 16% per year from US$197 billion in 2018 to US$355 billion in 2022. In addition, the productivity software market is expected to grow at 16.5% annually from 2018 to hit US$96 billion by 2025. In terms of market share, Google Cloud Platform is a distant third (with a 6% share in the second quarter of 2020, according to Canalys) behind Amazon’s AWS (31%) and Microsoft’s Azure (20%). So Google Cloud Platform is up against some tough competition. But in the first nine months of 2020, Google Cloud’s revenue still managed to jump by 46.4% from a year ago to US$9.2 billion. This follows Google Cloud’s equally-impressive revenue growth of 48% per year from 2017 (US$4.0 billion) to 2019 (US$8.9 billion). We think that the rising tide of cloud computing will be able to lift some boats, Google Cloud’s included.

The Other Bets segment in Alphabet is also interesting. It gives Alphabet optionality, which is a term that the Motley Fool’s co-founder David Gardner uses to describe the trait certain companies possess of having multiple paths to grow. It’s not easy to find information about all of the businesses in Other Bets, but we believe the major ones are involved in the following areas:

- Access – internet services

- Calico – biotechnology, with a focus on anti-aging research

- CapitalG – a venture capital fund with US$3 billion in assets under management; portfolio companies include tech companies such as Crowdstrike (in cybersecurity), Stripe (in fintech), Airbnb (in hospitality), and Snap (in social media)

- GV – Another venture capital fund with US$5 billion in assets under management; invests in private growth companies “across all stages and sectors, with a focus on enterprise, life sciences, consumer, and frontier technology”

- Verily – a research company focusing on medical devices & medical technology

- Waymo – Develops autonomous vehicle technologies

- X – We think it’s best-described as an innovation lab focusing on moonshot solutions that try to tackle the world’s hardest problems (such as sustainable ocean farming; using robots to better understand plant development and improve crop yields; robots that operate autonomously in everyday life; and beaming the internet from space, among other ambitious projects)

Currently, Other Bets is still incurring losses – its operating income has been negative going back to at least 2013, and for the 12 months ended 30 September 2020, it was a negative US$5.4 billion. Many of the companies within are still in the research and development phase or are only in the early stages of commercialisation. But if any of them do succeed, they could become significant drivers of future growth for Alphabet. In our view, the most promising companies in Other Bets are Waymo and Verily.

2. A strong balance sheet with minimal or a reasonable amount of debt

Alphabet’s balance sheet is as strong as they come. The company exited the third quarter of 2020 with US$132.6 billion in cash and investments, and just US$13.9 billion in debt. For the sake of conservatism, we note that Alphabet also had US$10.2 billion in operating lease liabilities – but this is dwarfed by the amount of cash and investments that the company had on hand.

To add icing on the cake, Alphabet is also a company with a long, stellar history of generating free cash flow, as we’ll show later.

3. A management team with integrity, capability, and an innovative mindset

On integrity

Alphabet was founded in 1998 by Larry Page and Sergey Brin as Google. In 2015, Google reorganised its business to form a new parent company, which is the Alphabet of today. Both of them have been in important leadership roles at Alphabet/Google since the company’s founding. In December 2019, Page and Brin stepped down as the CEO and President of Alphabet, respectively. The president role was removed and stepping in as CEO of Alphabet was Sundar Pichai. Although both Page and Brin remain as directors of Alphabet, we can’t be sure if they are still actively leading the company.

What we do know for a fact is that Alphabet’s co-founders still have huge economic interests in the company while also retaining a massive say on its future. Alphabet has three classes of common stock: A, B, and C. The company’s Class B shares are not publicly listed, hold 10 votes per share, and can be converted at any time into Class A shares on a 1-for-1 basis. The Class A shares, which have the ticker symbol of NASDAQ: GOOGL, hold 1 vote per share. The Class C shares have a ticker symbol of NASDAQ: GOOG, and carry no voting rights.

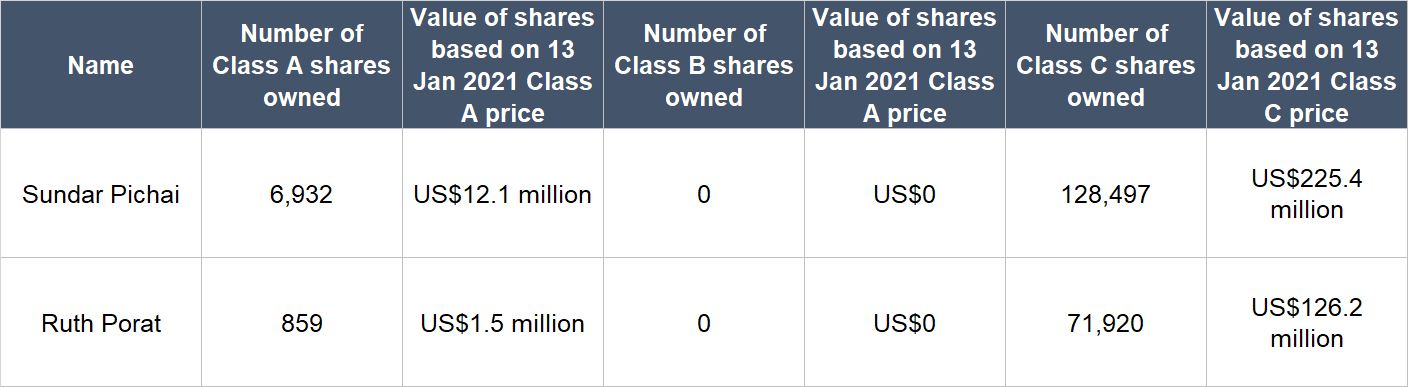

As of 7 April 2020, Page and Brin collectively controlled 39.144 million Alphabet Class B shares (in a 51:49 split) that are worth a staggering US$68.39 billion at the 13 January 2021 price of US$1,747 for each Alphabet Class A share. In addition, based on their latest regulatory filings, Page and Brin together currently own 34,900 Class A shares and 39.267 million Class C shares. At the 13 January 2021 share price for Alphabet’s Class A and Class C stock (US$1,747 and US$1,754, respectively), these shares are worth another huge sum of US$68.95 billion (the Page:Brin ratio is again roughly 51:49). So all together, the combined Alphabet stakes of Page and Brin are worth US$137.35 billion.

And because Page and Brin own a huge chunk of Alphabet’s Class B shares, the two co-founders controlled 51.2% of the company’s voting power, as of 7 April 2020, despite holding only 11.4% of the total share count (this includes all three share classes). Since Page and Brin will effectively call the shots at Alphabet, we need to be comfortable with them holding the company’s voting rights. We are. As mentioned, they have huge economic stakes that are tied to their Alphabet shares, so their interests should be nicely aligned with those of Alphabet’s other shareholders. It helps too that (1) the both of them have collected an annual salary of just US$1 since 2004, the year of the company’s listing, and (2) their bonuses and other forms of compensation from 2004 to 2019 have summed up to only around US100,000.

The key leader at Alphabet now is Sundar Pichai, 47, who first joined Google in April 2004 and steadily rose through the ranks. Before assuming the Alphabet CEO role in December 2019, he became CEO of Google in October 2015. We appreciate both Pichai’s relatively young age, and long tenure at Alphabet/Google. The other key Alphabet leader is CFO Ruth Porat, who joined the company as Google’s CFO in May 2015 before assuming her current role in October of the same year after Google restructured to create Alphabet.

In 2019, Pichai’s total compensation was an astronomical US$280.6 million. But this is a negligible sum when compared to Alphabet’s profit and free cash flow of US$34.3 billion and US$31.0 billion, respectively, in the same year. And importantly, nearly 99% of Pichai’s total compensation came from stock awards that we think are very well-structured.

Pichai’s stock awards have two components to them: Performance stock units (PSUs); and restricted stock units that Alphabet calls GSUs. The PSUs have two tranches – one vests over two years and started from January 2020, while the other vests over three years with the same start date. The actual amount of shares that will be granted for both tranches depends on the total return of Alphabet’s stock over the vesting period. Pichai can receive anything from 0% (if Alphabet’s share price performance is lower than the 75th best-performing stock in the S&P 100 during the vesting period) or 200% (if Alphabet is among the top 25 best-performing stocks in the S&P 100 for the vesting period) of the target amount of shares to be granted for each PSU tranche. The GSUs have two tranches too. The first tranche vests quarterly over one year and began on 25 March 2020 – this was given as an award to Pichai after his promotion to being CEO of Alphabet. The second tranche vests quarterly over three years and also began on 25 March 2020.

Meanwhile, Porat’s total compensation in 2019 was just US$664,052, of which US$650,000 came from her base salary. This is because she was granted stock awards in 2018 that are worth US$46.61 million – Alphabet has a practise of not granting stock awards to its senior leaders every year. Her stock awards in 2018 vest over four years.

So, most of Pichai’s stock awards (around 85%) for 2019 and all of Porat’s stock awards in 2018 depend on multi-year changes in Alphabet’s share price, which in turn is determined by the company’s business performance. To us, this means that Pichai and Porat’s interests are well-aligned with those of Alphabet’s other shareholders.

And speaking of alignment of interests, there’s something else we want to highlight: Pichai and Porat also own substantial stakes in Alphabet as shown in the table below:

Source: Pichai and Porat’s regulatory filings

On capability and ability to innovate

We rate Alphabet’s leaders highly on this front and there are a few things we want to discuss.

First, Alphabet has an outstanding history of developing new products that have gone on to become ubiquitous platforms and huge businesses. Alphabet, in its earliest days, started off as only an internet search engine that was founded by Larry Page and Sergey Brin. Today, Google Search accounts for 88% of the global search engine market, according to Statista, and has kept its market share at a similar level going back to at least January 2010. But there’s more. As mentioned earlier, Alphabet now has a wide range of properties – this includes Android, Chrome, Gmail, Google Drive, Google Maps, Google Play, Google Search, and YouTube – that have over one billion monthly active users each as of end-2019.

The dominance and ubiquity of the Google properties serves to strengthen Alphabet’s business. In 2017, Google said that its search engine handles “trillions of searches… every year” and 15% of the searches it sees each day are completely new. Having to handle a significant number of new searches each day means that having more data to process and learn from can be a strong advantage. Given its dominant market share, Google’s search engine has the richest dataset to learn from so that it can present the most relevant answers to people’s queries. Meanwhile, the huge user base of the other Google properties can further strengthen the core search engine business by providing it with even more data to learn from.

Second, Alphabet has done a phenomenal job with acquisitions. There are two that stand out to us: YouTube and Android. Alphabet acquired YouTube in the fourth quarter of 2006 for US$1.76 billion. The deal had its critics at that time. But in the 12 months ended 30 September 2020, YouTube generated US$17.6 billion in revenue – 10 times what Alphabet paid to acquire the content streaming platform. From 2017 to 2019, Youtube’s revenue also compounded impressively at 36% per year to reach US$15.1 billion. Android, the dominant mobile device operating system of today (Statista estimates Android’s global share of the mobile device operating systems market to be 73% in October 2020), was reportedly acquired by Alphabet quietly for just US$50 million in 2005. It was so quiet that Alphabet’s annual reports for 2005 and 2006 did not even contain a single mention of Android.

Both the Youtube and Android acquisitions were made while Page and Brin were still leading Alphabet actively. But we want to highlight that Pichai likely has his fingerprints all over Youtube and Android’s growth, at least in recent years. He was Google’s Senior Vice President of Android, Chrome, and Apps from March 2013 to October 2014, and as we had already shared, he became CEO of the entire Google business more than five years ago in October 2015. In late 2019, Google announced that it would acquire Fitbit, a wearable devices brand, for US$2.1 billion. The deal was under regulatory scrutiny for over a year, but was finally completed last week. Not all of Alphabet’s acquisitions have turned to gold. For instance, Alphabet bought mobile phone maker Motorola for US$12.5 billion in 2012, and then sold it for just US$3 billion two years later. But we’re not looking for perfection when it comes to Alphabet’s acquisitions. We’re watching the Fitibt deal with interest as it could boost Alphabet’s presence in the wearables market.

Third, we believe Alphabet’s willingness to continue funding the loss-making businesses that are grouped under Other Bets is a good indication of the company’s positive view towards innovation. Alphabet is in a unique position of being able to invest heavily in entirely new products and services without harming its financial health because of its core advertising business’s ability to throw out massive amounts of free cash flow. This makes Alphabet a great platform for innovation and moonshot bets – and we credit management for doing just that. Alphabet’s leadership team included the following passage in the company’s 2019 annual report and it clearly shows how much they value innovation:

“Many companies get comfortable doing what they have always done, making only incremental changes. This incrementalism leads to irrelevance over time, especially in technology, where change tends to be revolutionary, not evolutionary. People thought we were crazy when we acquired YouTube and Android and when we launched Chrome, but those efforts have matured into major platforms for digital video and mobile devices and a safer, popular browser. We continue to look toward the future and continue to invest for the long-term. As we said in the original founders’ letter, we will not shy away from high-risk, high-reward projects that we believe in because they are the key to our long-term success.”

Shortly after he became Alphabet’s CEO, Pichai publicly hinted that he would be imposing more fiscal discipline on the businesses within Other Bets. If he does so without stifling creativity and innovation in the businesses within the segment, that would be like having the best of both worlds.

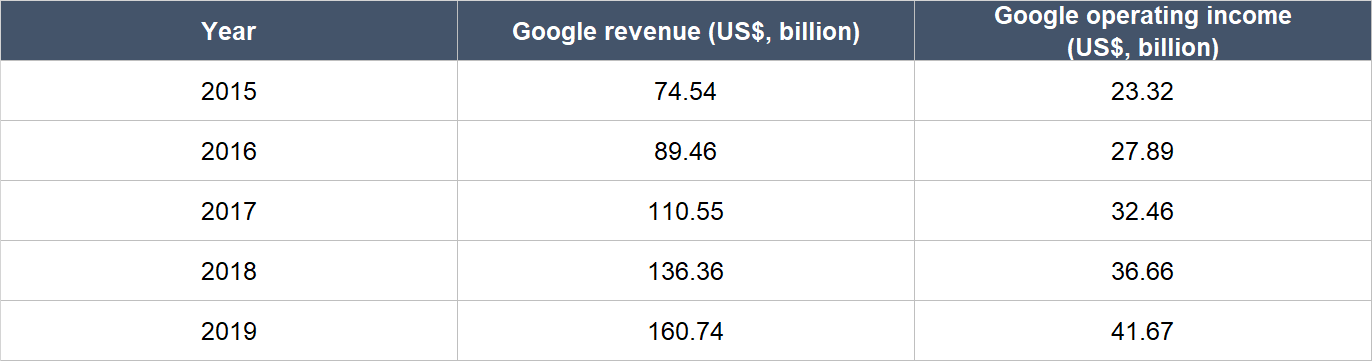

Fourth, Alphabet’s Google business has been growing well ever since Pichai became Google’s CEO, with revenue more than doubling from 2015 to 2019 and operating income nearly doubling over the same period. These are shown in the table below. In addition, with Pichai as Google’s CEO, Google made a transformative hire for Google Cloud in November 2018 by bringing in Thomas Kurian as its leader. Under Kurian, Google Cloud’s sales process has greatly improved. The numbers bear this out. In 2019, Google Cloud’s revenue growth accelerated significantly from 43.9% in 2018 to 52.8%. Then in the second and third quarters of 2020, Google Cloud’s revenue experienced year-on-year revenue growth of 43.2% and 44.8%, respectively; these growth rates are significantly faster than the worldwide cloud infrastructure spending growth of 31.4% in the second quarter and 32.5% in the third quarter, according to data from Canalys.

Source: Alphabet annual reports

Fifth, Google appears to have a wonderful corporate culture, and we credit Alphabet’s leaders for that. Glassdoor is a platform that allows employees to rate their companies anonymously. Currently, 89% of Google-raters on Glassdoor will recommend the company to a friend. Meanwhile, Pichai has a 94% approval rating as CEO, far higher than the average Glassdoor CEO rating of 69% in 2019.

4. Revenue streams that are recurring in nature, either through contracts or customer-behaviour

We think Alphabet has high levels of recurring revenues from two ways: Customer behaviour and contracts.

For customer behaviour, it’s simply the nature of Alphabet’s digital advertising business. Individuals conduct internet searches and visit websites all the time – this means they are constantly being shown advertising. Meanwhile, advertisers also constantly want to connect with consumers through the internet, so there’s no shortage of business for Alphabet. But none of this means that Alphabet’s customers will not reduce their advertising spend over the short run when economic conditions are tough. The current COVID-19 pandemic illustrates this dynamic clearly: Alphabet’s revenue dipped by 1.7% in the second quarter of 2020. This said, our eyes are fixed on the long-term opportunity with Alphabet and we think the company does have strong recurring revenue over the long run.

Customer behaviour driving recurring revenue also comes into play with Alphabet’s non-advertising businesses. In the case of Google Cloud, the cloud computing infrastructure services that it provides are often very important to its customers – this drives repeat purchase behaviour.

On contracts, Alphabet has subscription models, such as those found in Google Workspace and Youtube’s premium tiers.

5. A proven ability to grow

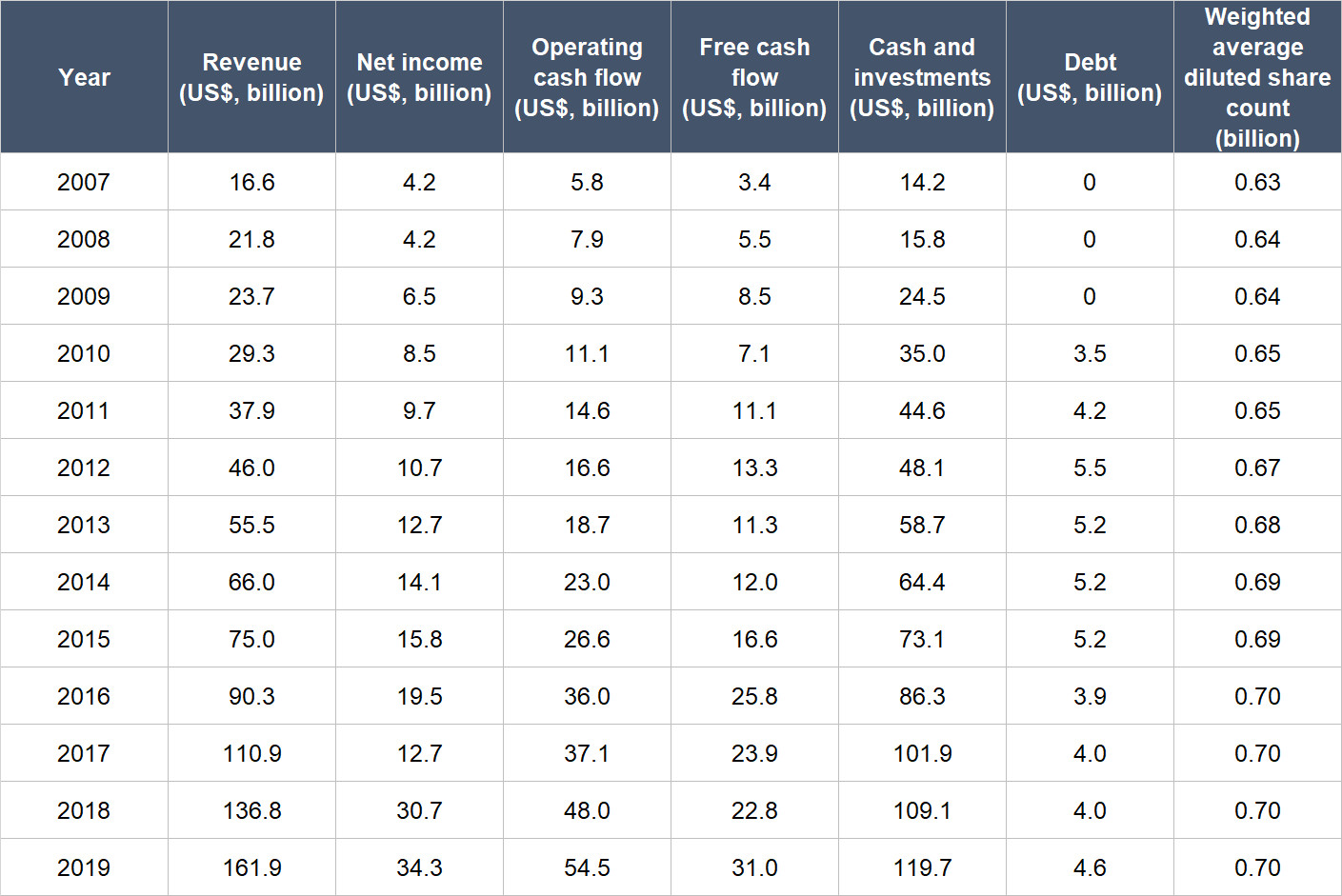

The table below shows Alphabet’s important financials from 2007 to 2019 (we chose 2007 as the starting point to observe how the company fared during the Great Financial Crisis period):

Source: Alphabet annual reports

A few key points about Alphabet’s financials:

- Revenue grew in each year for the whole time period we’re looking at (even during the Great Financial Crisis years of 2008 and 2009) and had compounded at an impressive annual rate of 20.9%. Over the last five years from 2014 to 2019, Alphabet’s revenue had compounded at a similarly strong rate of 19.7% per year.

- The net income growth rate from 2007-2019 and from 2014-2019 were both high at 19.1% and 19.4%, respectively. It’s also impressive to us that Alphabet’s net income grew in nearly every year from 2007 to 2019 – the only exception was in 2017, when there was a big one-time jump in taxes.

- Operating cash flow was consistently positive and grew in each year for the entire time frame we studied. It also increased markedly with growth of 20.6% annually for 2007-2019, and 18.8% for 2014-2019.

- Free cash flow was consistently positive too and had stepped up from 2007 to 2019 at a rapid clip of 20.3% per year. The annual growth in free cash flow from 2014 to 2019 was 20.9% – not shabby at all.

- Alphabet’s balance sheet was rock solid throughout the entire time frame we’re looking at, with debt being either zero, or significantly lower than the amount of cash and investments on hand.

- Dilution has been negligible at Alphabet, with the weighted average diluted share count increasing by a mere 0.8% per year from 2007 to 2019, and by just 0.3% annually from 2014 to 2019.

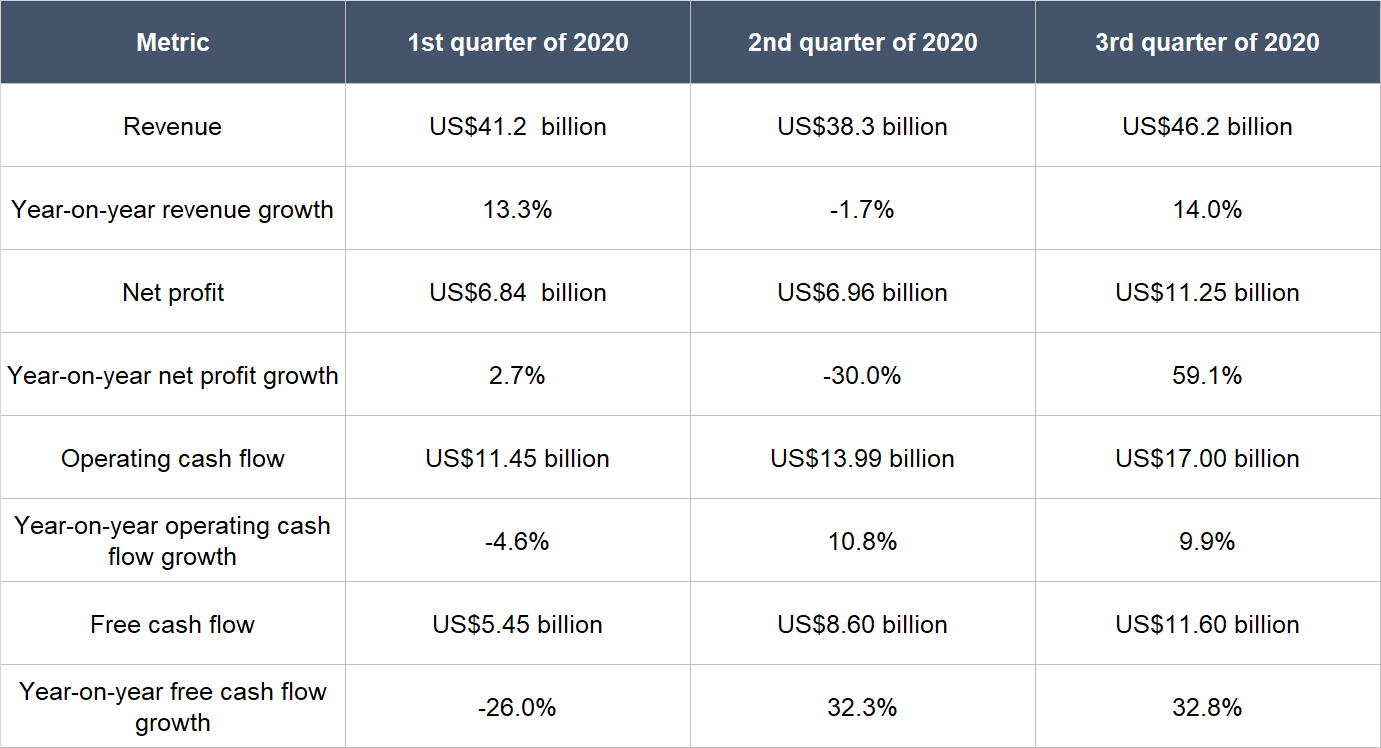

As mentioned earlier, Alphabet’s business had suffered from COVID-19 in 2020. But the picture isn’t all bad. The table below shows the changes in Alphabet’s revenue, net profit, operating cash flow and free cash flow in the first three quarters of 2020. Although Alphabet’s revenue declined year-on-year in the second quarter, growth resumed in the third quarter, and at a pretty healthy rate of 14.0% year-on-year; the swift rebound in the third quarter is a good indication that advertisers are starting to return to Alphabet. There is one more thing worth noting: In the first three quarters of 2020, Alphabet continued its long history of generating solid net income, operating cash flow, and free cash flow.

Source: Alphabet quarterly earnings updates

6. A high likelihood of generating a strong and growing stream of free cash flow in the future

There are two reasons why we think Alphabet excels in this criterion.

First, there’s still significant room to grow for Alphabet. Its digital advertising and cloud computing businesses have total addressable markets that will likely continue to expand in the years ahead. And then there are the companies in Alphabet’s Other Bets segment – while none of them have yet to be successfully commercialised at a high level, the investments that the company has been making in Other Bets may yet pay off in the future. All it takes is just one successful moonshot.

Second, Alphabet has been generating tremendous amounts of free cash flow for years, as we’ve shown earlier. Moreover, its average free cash flow margin (free cash flow as a percentage of revenue) in the past five years from 2014 to 2019 was strong at 21.0%. In 2019, the free cash flow margin was 19.1%. Even with COVID-19 around in the first nine months of 2020, Alphabet’s free cash flow margin was still an excellent 20.4%.

Valuation

We like to keep things simple in the valuation process. In Alphabet’s case, we think the price-to-earnings (P/E) ratio and price-to-free cash flow (P/FCF) ratio are suitable gauges for the company’s value. This is because Alphabet has been adept at producing positive and growing profit as well as free cash flow for a long period of time.

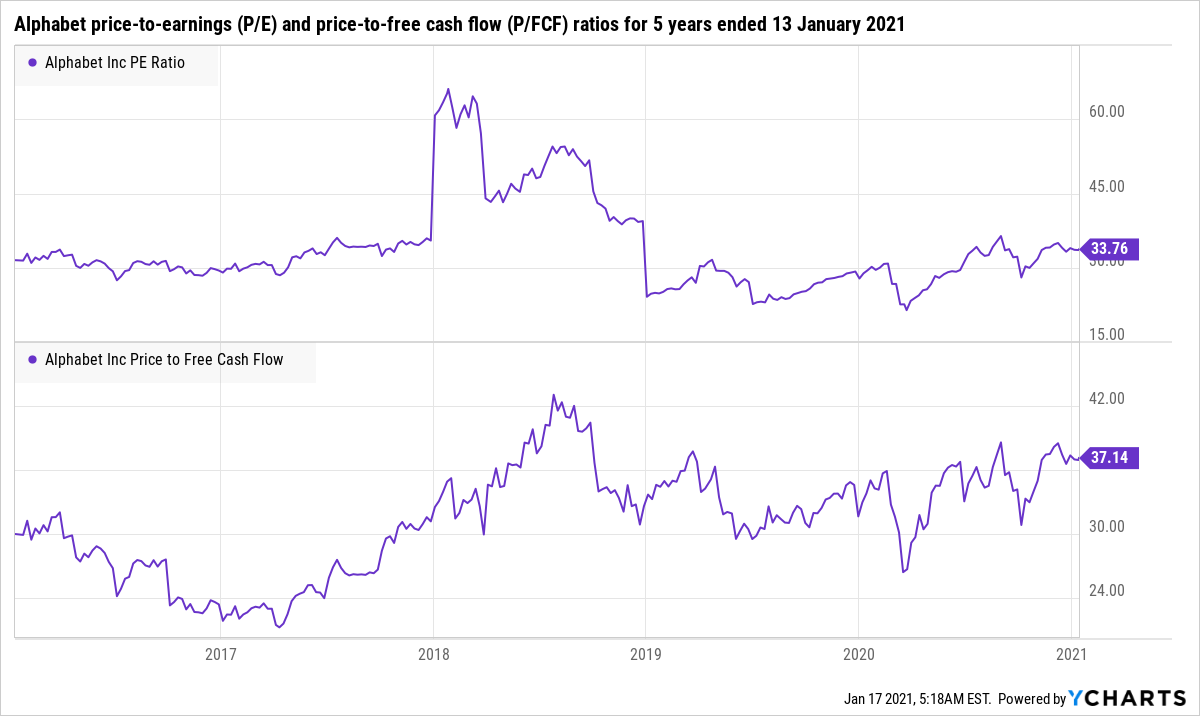

We completed our purchases of Alphabet Class A shares with Compounder Fund’s initial capital in late July 2020. We bought the Class A shares because they carried a slightly lower price than the Class C shares when we made our investments – we have no preference between the two share classes since Alphabet’s voting power is already concentrated in the hands of Larry Page and Sergey Brin, so we went with the share class that had the lower price. Our average purchase price was US$1,508 per Alphabet Class A share. At our average price and on the day we completed our purchases, the company’s shares had trailing P/E and P/FCF ratios that were both around 33. Here’s a chart showing Alphabet’s P/E and P/FCF ratios over the five years ended 13 January 2021:

The P/E and P/FCF ratios that Alphabet had when we made our investments were not high relative to their histories. Moreover, they look reasonable for an innovative company with a long history of impressive growth and a seemingly long runway to expand its business.

For perspective, Alphabet carried P/E and P/FCF ratios of around 34 and 35, respectively, at the 13 January 2021 share price of US$1,747.

The risks involved

There are a few key risks that we see in Alphabet.

First is the threat of heavy-handed regulatory restrictions on the company. Alphabet has been attracting scrutiny from both the public and regulators in recent years. For example, Sundar Pichai had to testify before US lawmakers on behalf of Alphabet in July 2020 on antitrust issues, alongside three other major US tech companies, namely, Amazon, Apple, and Facebook. In another instance, the European Commission fined Google €4.3 billion in July 2018 for infringing European competition law; this was followed by another €1.5 billion fine by the same regulatory body in March 2019, again for antitrust transgressions in Europe. If there’s heavier regulatory pressure on Alphabet, that could harm its digital advertising business.

Second is succession risk. We think Pichai has been an important reason behind Alphabet’s growth in recent years. Should he leave Alphabet, we will be keeping a close eye on the leadership transition. The good thing is that Pichai is still relatively young, so he should still have plenty of gas left in the tank to continue leading the company.

The third risk we note is related to competition. Google is dominant in the global internet search engine market as discussed earlier. Then there’s also the myriad of other properties within Google that each command more than one billion monthly active users. These mean that Google captures plenty of consumer attention and data, and thus is attractive for advertisers. But Google is not the only technology giant in town that is involved with digital advertising. For instance, there’s Facebook, with its social network of over 2.7 billion global monthly active users currently, and also e-commerce juggernaut Amazon’s relatively young but fast-growing digital advertising business that has already gained significant scale. There are younger but rapidly-growing social media upstarts such as TikTok that are commanding significant consumer attention too. But we think there can be room for multiple winners in the digital advertising space going forward and Google is likely to be among them.

Fourthly – and this is related to the first and third risk – there’s a chance that Google’s search engine loses its relevance among consumers over time. This can happen if regulations severely hamper Google’s ability to collect and analyse consumer data, and/or there’s the emergence of a super-app in the Western world – something akin to say Meituan Dianping or Tencent’s WeChat app in the East – that becomes the key portal for consumers to discover information over the internet without having to access Google’s properties.

The last risk we note is related to recessions, for whatever reason. Advertising activity can be sensitive to economic conditions – this means that most of Alphabet’s current business could be negatively affected by an economic downturn. Although Alphabet managed to grow admirably during the 2008-09 Global Financial Crisis, it is a much larger company today and so could find it harder to grow through a future recession. In the current context, the presence of COVID-19 is probably the biggest potential driver for any global economic pain in the near-term (after already causing hurt last year). We’ve seen what COVID-19 has done to Alphabet’s business, with the company reporting a year-on-year revenue decline in the second quarter of 2020.

Summary and allocation commentary

To sum up Alphabet, the company:

- Is operating in the large and expanding digital advertising and cloud computing markets; there’s also the potential for some of its moonshot projects to really take off

- Has a pristine balance sheet with more than a hundred billion dollars in cash and negligible debt

- Has a management team with sensibly-structured compensation plans, and a long history of solid execution and innovation

- Enjoys high levels of recurring revenues from both customer-behaviour and contracts

- Boasts an enviable long-term track record of growth in revenue, net income, and free cash flow

- Has a high possibility of enjoying a strong and growing stream of free cash flow in the future.

There are risks to note and they include the threat of heavy-handed regulation; succession risk; the presence of strong competitors for advertising dollars; the potential for Google’s search engine to lose relevance in the world; and the potential for Alphabet’s business to be harmed in the event of prolonged recessions.

After weighing the pros and cons, we initiated a 2.5% position – a medium-sized allocation – in Alphabet with Compounder Fund’s initial capital.

And here’s an important disclaimer: None of the information or analysis presented is intended to form the basis for any offer or recommendation; they are merely our thoughts that we want to share. Of all the companies mentioned in this article, Compounder Fund also currently owns shares in Amazon, Apple, Facebook, Meituan Dianping, and Tencent. Holdings are subject to change at any time.