Compounder Fund: Tesla Sell Thesis - 18 Mar 2026

Data as of 17 March 2026

We first invested in Tesla (NASDAQ: TSLA) for Compounder Fund’s portfolio in January 2021. Our investment thesis for the company can be found here. In early-January 2026, we completely exited Tesla. This article describes our Sell thesis for the company.

When we invested in Tesla, the lion’s share of its revenue came from its automotive business segment, where it designs, manufactures, and sells electric vehicles. We were impressed with the rapid growth in Tesla’s vehicle deliveries (a nearly seven-fold increase from around 76,000 vehicles in 2016 to almost 500,000 in 2020) and thought that the company had an extremely strong brand that would likely endure. We thought a core part of the brand’s strength came from the fanaticism Tesla’s CEO and major shareholder, Elon Musk, has with delivering a fantastic overall user experience with Tesla’s vehicles. An important part of our thesis also lay in Tesla’s optionality (see note below), two prongs of which are the development and sale of autonomy software on a subscription basis, and the establishment of an autonomous ride-hailing fleet.

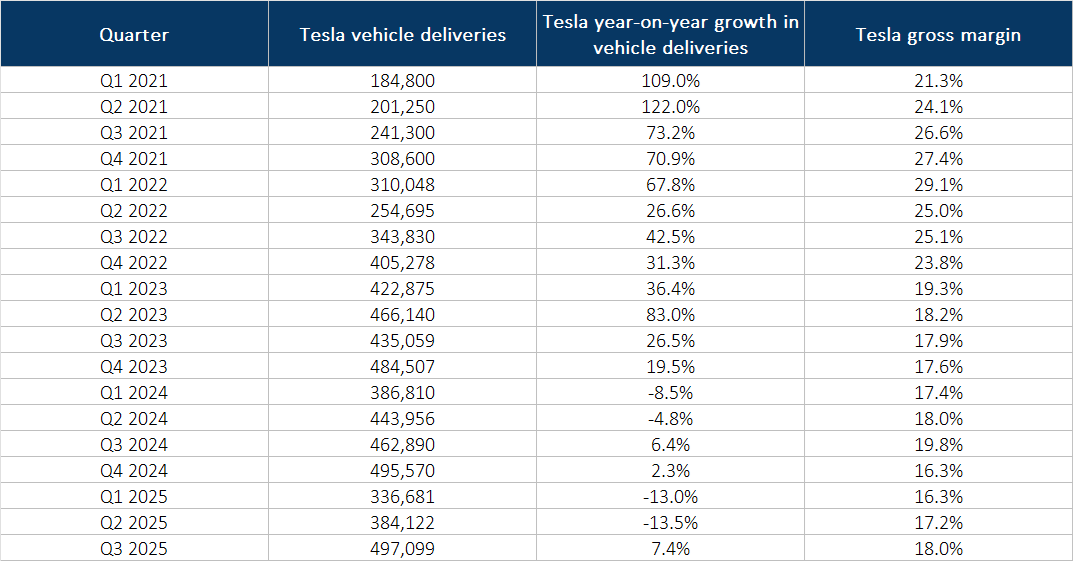

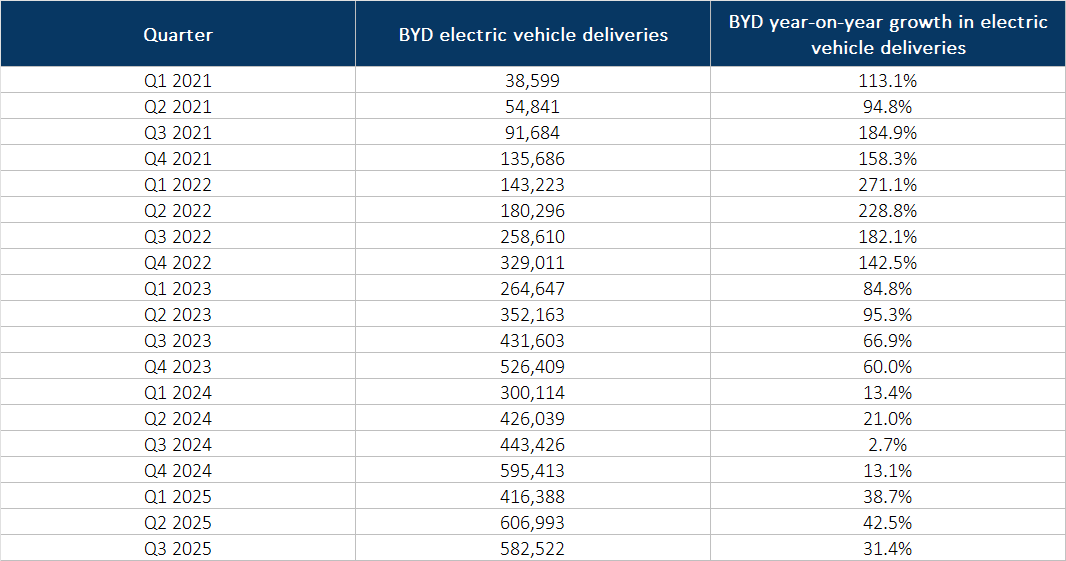

For a few years after our investment, Tesla continued delivering outstanding growth in vehicle deliveries and improvements in its gross margin, as shown in Table 1 below. But the table also shows that Tesla’s vehicle deliveries and gross margin started floundering in 2024 and this continued into 2025. The decline in Tesla’s deliveries in some of the recent quarters was jarring when compared with the growth in global deliveries that some of China’s electric vehicle manufacturers were posting; the example of BYD, China’s and the world’s largest electric vehicle company, is shown in Table 2 below.

Table 1; Source: Tesla quarterly delivery and earnings updates

Table 2; Source: BYD quarterly delivery updates

But even as Tesla’s core electric vehicles business was weakening in 2025, its stock price rose 103% from the bottom in early-April 2025 to US$450 at the end of the year, driving its price-to-earnings (P/E) and price-to-sales (P/S) ratios to 269 and 17, respectively.

We do note that since our initial investment, Tesla had made promising strides with its autonomy software and autonomous ride-hailing fleet under Musk’s leadership. The company had even started building autonomous humanoid robots. Here’s Tesla’s progress on these three fronts at the time we sold the company’s shares:

- Tesla had launched Version 14 of its FSD (Full Self Driving) autonomy software package, and around 12% of the total Tesla fleet had bought it

- Robotaxi, Tesla’s autonomous ride-hailing service, was launched in the second quarter of 2025 in Austin, Texas, as a pilot program and had expanded to at least one other market (cities in the San Francisco Bay Area).

- Optimus, Tesla’s autonomous humanoid robot, was being manufactured on a small scale, but the company already had the second version of the robot and management was looking forward to unveiling Version 3 in the first quarter of 2026.

Meanwhile, Tesla was also enjoying great progress in designing its own AI (artificial intelligence) chip. It had the A14 chip in production, and was looking to produce the next generation A15 chip. Musk was effusive about the A15 chip’s capabilities during Tesla’s 2025 third-quarter earnings conference call:

“By some metrics, the AI5 chip will be 40x better than the AI4 chip, not 40%, 40x because we have a detailed understanding of the entire software and hardware stack. So we’re designing the hardware to address all of the pain points in software…

…With the AI5, we deleted the legacy GPU or the traditional GPU, which is — it’s in AI4. But AI5 does not have — we just deleted the legacy GPU because it basically is a GPU. So we also deleted the image signal processor. And there’s like a long list actually of deletions that are very important. As a result of these deletions, we can actually fit AI5 in a half reticle and with good margin for the traces from the memory to the Tesla Trip accelerators, the ARM CPU cores and the PCI-X sort of the PCI blocks. So this is a beautiful chip. I’ve hoarded so much life energy into this chip personally. And I’m confident this will be — this is going to be a winner next level…

…The challenge that they have is that they’ve got to satisfy a large range — a lot of requirements from a lot of customers, but Tesla only has to satisfy requirements from one customer, that’s Tesla. That makes the design job radically easier and means we can delete a lot of complexity from the chip. Like I can’t emphasize how important this is. So like when you look at the various logic blocks in the chip, as you increase the number of logic blocks, you also increase the interconnections between the logic blocks. So you can think of it like there’s highways, like how many highways do you need to connect the various parts of the chip. And especially if you’re not sure how much data is going to go between each logic block on the chip, then you kind of end up having giant highways going all over the place. It’s a very — like it becomes an almost impossibly difficult design problem. And NVIDIA has done an amazing job of dealing with almost an impossibly difficult set of requirements. But in our case, we’re going for radical simplicity…

…I think AI5 will be the best performance per watt, maybe by a factor of 2 or 3 and the best performance per dollar for AI, maybe by a factor of 10.”

Robotaxi and Optimus are two particular projects in Tesla that have the potential for explosive growth. Tesla’s management has publicly commented that Robotaxi is able to scale significantly faster than Alphabet’s competing Waymo service once it exits the testing phase. This is because Tesla’s autonomy software has an end-to-end neural network architecture whereas some elements of hardcoding are present in Waymo’s version. If Robotaxi scales successfully, it could be a massive business. In our Tesla thesis, we shared that Uber’s 2019 IPO prospectus had pegged the personal mobility market opportunity to be US$5.7 trillion across 175 countries. Meanwhile, Musk thinks that Optimus is likely to be Tesla’s biggest ever product. He thinks each robot is up to five times as productive as a person, and has said that it “has the potential to be north of [US]$10 trillion in revenue” and “is the infinite money glitch.”. But monetisation at scale for Robotaxi and Optimus were still far off when we sold Compounder Fund’s Tesla shares. Both projects were still early in their testing phases; Robotaxi was only present in a few geographies in the US, and Optimus robots were merely walking around in Tesla’s factories and not engaged in economically productive work. It’s also worth noting that scaling the manufacturing of Optimus is fraught with difficulties and comes with uncertain timing. Here’re Musk’s recent comments on the topic:

[From Tesla’s 2024 fourth-quarter earnings conference call]

“There’s a lot of uncertainty on the exact timing because it’s not like a train arriving at the station for Optimus. We are designing the train and the station and in real time while also building the tracks. And sort of like, why didn’t the train arrive exactly at 12:05? And like we’re literally designing the train and the tracks and the station in real-time while like how can we predict this thing with absolute precision? It’s impossible…

…This is an entirely new supply chain, it’s entirely new technology. There’s nothing off the shelf to use. We tried desperately with Optimus to use any existing motors, any actuators, sensors. Nothing worked for a humanoid robot at any price. We had to design everything from physics-first principles to work for humanoid robot and with the most sophisticated hand that has ever been made before by far. Optimus will be also able to play the piano and be able to thread a needle. I mean this is the level of precision no one has been able to achieve.”

[From Tesla’s 2025 first-quarter earnings conference call]

“Almost everything in Optimus is new. There’s not like an existing supply chain for the motors, gearboxes, electronics, actuators, really anything in the Optimus apart from the AI for Tesla, the Tesla AI computer, which is the same as the one in the car. So when you have a new complex manufactured product, it will move as fast as the slowest and the least lucky component in the entire thing. And as a first order approximation, there’s like 10,000 unique things. So that’s why anyone who tells you they can predict with precision, the production ramp of the truly new product is — doesn’t know what they’re talking about. It is literally impossible.”

[From Tesla’s 2025 third-quarter earnings conference call]

“Trying to make 1 million Optimus robots per year, that manufacturing challenge is immense, considering that the supply chain doesn’t exist. So with cars, you’ve got an existing supply chain. With computers, you’ve got an existing supply chain. With a humanoid robot, there is no supply chain. So in order to manufacture that, Tesla actually has to be very vertically integrated and manufacture very deep into the supply chain, manufacture the parts internally because there just is no supply chain.”

[From Tesla’s 2025 fourth-quarter earnings conference call, after we had sold Tesla]

“There’s really nothing from the existing supply chain that exists in Optimus. Everything is designed from physics first principles. So that means the normal S-curve of manufacturing ramp will be longer for Optimus than it is for products that have at least some portion of an existing supply chain. Like when everything is new, the production rate will be proportionate to the least lucky, least confident part of the entire supply chain. And if there’s 10,000 things that need to go right, it’s — it only takes one to be slow to lag that. But — so it will be sort of a stretched out S-curve.”

We still think Tesla has a strong brand. But the data shared in Table 1 makes us less confident about Tesla’s brand-strength compared to when we first invested in the company. We may even have been wrong with our view that the brand would remain strong because of Musk’s fanaticism with the user experience, given the comparison between Tesla’s delivery-numbers and those of BYD. But in any case, given the aforementioned poor performance in Tesla’s vehicle deliveries and gross margin, we thought the rise in the company’s stock price from April 2025 to December 2025, along with its high valuation, meant its risk-to-reward ratio was not in our favour.

We made our initial investment in Tesla at an average split-adjusted price of US$245 per share and sold at an average price of US$445. Part of the capital from the sale of Compounder Fund’s Tesla shares was redeployed to some existing companies in the portfolio (in this case, the companies were Amazon, MercadoLibre, Shinhan Financial Group, and Tencent).

Note: Optionality, a term coined by The Motley Fool’s co-founder, David Gardner, describes the trait a company has of being able to evolve and find entirely new ways to grow.

And here’s an important disclaimer: None of the information or analysis presented is intended to form the basis for any offer or recommendation; they are merely our thoughts that we want to share. Of all other companies mentioned in this article, Compounder Fund owns shares in Amazon, MercadoLibre, Shinhan Financial Group, and Tencent. Holdings are subject to change at any time.