Compounder Fund: Meituan Sell Thesis - 18 Mar 2026

Data as of 17 March 2026

We first invested in Meituan (SEHK: 3690) for Compounder Fund’s portfolio in July 2020. Our investment thesis for the company can be found here. In early-January 2026, we completely exited Meituan. This article describes our Sell thesis for the company.

When we invested in Meituan, we thought of the company as a ‘super app’ for food delivery and a host of other lifestyle services in China. It was the clear leader in on-demand food delivery with a dominant market share. We were impressed with the company’s multi-year history of growing its important business metrics, such as GTV (gross transaction volume), transacting users, and transacting merchants. The growth in Meituan’s business metrics drove outstanding improvements in its financials. Revenue compounded at a rapid pace of 122% per year from 2015 to 2019, and was still up an impressive 49.5% in 2019. The company also produced positive net profit and free cash flow in 2019 after a few years of losses and negative free cash flow. Meituan’s business suffered significantly during the early phases of COVID-19, but we adopted a long-term view on its prospects.

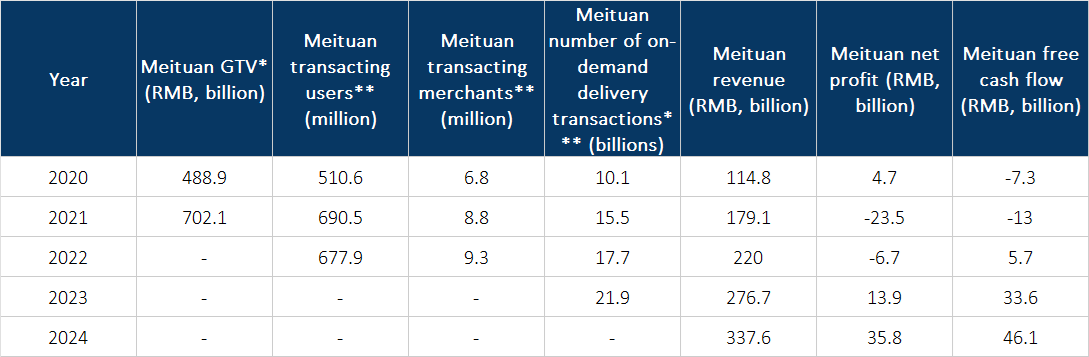

After our investment, Meituan continued delivering strong growth in GTV, transacting users, transacting merchants, revenue, net profit, and free cash flow up to 2024. These are shown in Table 1 below, which also shows Meituan’s number of on-demand delivery transactions. What makes the figures in Table 1 even more impressive is that the Chinese government started to crack down on China’s technology sector in 2021 and only appeared to have softened its stance in 2024.

Table 1; Source: Meituan quarterly earnings updates and annual reports

*Meituan stopped reporting GTV numbers in 2022

**Meituan stopped reporting transacting users and transacting merchants in 2023

***Meituan stopped reporting the number of on-demand delivery transactions in 2024; the number for 2020 is for food delivery only

But the competitive landscape for Meituan shifted dramatically in early-2025. That was when JD.com and Alibaba amped up the competitive heat in the on-demand food delivery market through heavy subsidies (the initial subsidies for the duo were RMB 10 billion each; see note below for more). Our primary concern is on the long-term economics of Meituan’s core on-demand delivery business. The management of JD.com has repeatedly commented that they see food delivery as a service to capture customers into the company’s broader e-commerce ecosystem:

[From JD.com’s 2025 first-quarter earnings conference call]

“It’s important to note that at JD, we do not see food delivery as a stand-alone business. It’s deeply rooted and well-integrated into JD’s robust retail infrastructure and ecosystem, a pivotal differentiator. In a very brief time, JD Food Delivery has made remarkable headway in the aspects of order volume, onboarded merchants and riders. In particular, as we speak, JD Food Delivery order volume today is reaching close to 20 million orders, another important milestone that we expect to surpass very soon. This demonstrates our incentive strategies and strong execution at the right time. On-demand retail with food delivery included will generate powerful synergies with our core retail and other businesses such as JD Health and drive overall growth and efficiency gain across the entire JD ecosystem in the years to come.”

[From JD.com’s 2025 second-quarter earnings conference call]

“I want to reiterate that we do not view our food delivery as a stand-alone business as it’s deeply integrated with JD’s broader ecosystem. We aim to further unlock synergies not only between JD Food Delivery and JD Retail, but also with JD Logistics and other businesses across our ecosystem. This is where our strategic focus lies. Going forward, we will stay focused on our strategic priorities and invest with high efficiency at appropriate pace, amidst the evolving dynamics in the food delivery market.”

[From JD.com’s 2025 third-quarter earnings conference call]

“Ultimately, JD food delivery should be a self-sustaining business. Moreover, food delivery is deeply integrated into JD overall ecosystem. We believe there is significant potential for synergies in user momentum, supply and fulfillment within our ecosystem. The way of our business working together is not simply adding 1 and cutting another. JD user acquisition costs — in the long term JD-user acquisition cost will decrease. And at the group level, we are committed to driving sustainable growth while maintaining profitable and cash flow sufficient.”

[From JD.com’s 2025 fourth-quarter earnings conference call (after we had sold Meituan)]

“What is even more encouraging is the quality of user growth. User shopping frequency surged by over 40% year-on-year for the full year with broad-based gains across all user groups, including new and existing users as well as Plus members. In addition to user acquisition, JD Food Delivery also played an important role in this frequency lift. We view the expansion of user base and engagement as a long-term strategic driver for our business and expect it will further amplify in 2026 and beyond…

…We are also seeing a strategic shift where advertisers are reallocating budgets towards platforms like JD as we are regarded as the most consistent daily sales platform, the premium destination for brand building and the platform that offers the highest return throughout a product’s entire life cycle. Notably, the synergy with JD Food Delivery is starting to bear fruit, contributing an incremental 2% to 3% to ad revenue in Q4. We remain confident in sustaining our advertising revenue momentum in 2026…

…In Q4, JD Food Delivery loss rate over GMV narrowed significantly compared to a quarter ago while maintaining the scale momentum. More importantly, the strategic synergies with our core retail business are deepening. Beyond the strong user momentum mentioned earlier, both cohorts cumulative cross-selling rate and shopping frequency trended upward in Q4. Additionally, total active merchants have increased by over 270%, which was also partially contributed by the high-quality restaurants that onboarded our platform.”

It’s similar with Alibaba (note: food delivery is part of the company’s quick commerce business):

[From Alibba’s 2025 second-quarter earnings conference call]

“At the same time, we will not look at the stand-alone profitability of quick commerce delivery. If combined with the incremental benefits to our e-commerce business, we believe quick commerce will bring sustained positive economic value to the overall platform while maintaining price competitiveness.”

[From Alibaba’s 2025 third-quarter earnings conference call]

“Quick commerce is having a very significant effect in terms of enhancing user engagement as well as driving transactions in relevant categories. So that, of course, has a positive impact on CMR. So the main thing that we need to do in this next phase is to better integrate and achieve synergies across conventional e-commerce and quick commerce so as to more fully realize that impact.”

We think this means that JD.com’s and Alibaba’s leaders are likely to accept relatively lower profit margins for on-demand food delivery. This dynamic could cap Meituan’s margin-potential at a materially lower level than prior to their aggressive subsidies.

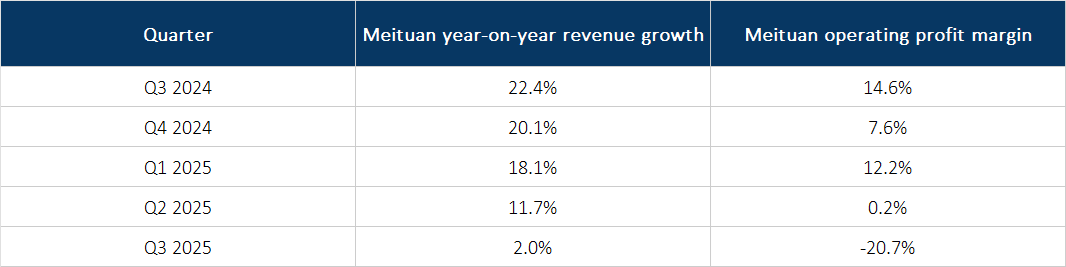

We also thought Meituan had significant competitive advantages in the on-demand delivery market, especially with its dominant market share at the time of our investment and in the subsequent years since (65% in 2024, for example). But the bruising fight with JD.com and Alibaba has led to Meituan’s revenue growth grinding to a halt and operating profit margin collapsing, as shown in Table 2. Meituan’s management has refused to engage in a price war, so the lower revenue growth rates are not surprising. But Meituan’s operating profit margin also crumbled in tandem. This suggests that Meituan’s actual competitive advantage in on-demand delivery is much weaker than our initial assessment. Given this, and our worry that the long-term economics of Meituan’s business has severely eroded, we decided to part ways with the company.

Table 2; Source: Meituan quarterly earnings updates

We made our initial investment in Meituan at an average split-adjusted price of HK$189 per share and sold at an average price of HK$97. Part of the capital from the sale of Compounder Fund’s Meituan shares was redeployed to some existing companies in the portfolio (in this case, the companies were Amazon, MercadoLibre, Shinhan Financial Group, and Tencent).

Note: JD.com entered the on-demand food delivery market only in early-2025, in conjunction with its aggressive subsidies, whereas Alibaba has long been competing with Meituan.

And here’s an important disclaimer: None of the information or analysis presented is intended to form the basis for any offer or recommendation; they are merely our thoughts that we want to share. Of all other companies mentioned in this article, Compounder Fund owns shares in Amazon, MercadoLibre, Shinhan Financial Group, and Tencent. Holdings are subject to change at any time.