Compounder Fund: Block Sell Thesis - 11 Jul 2025

Data as of 10 July 2025

We first invested in Block (NASDAQ: XYZ) for Compounder Fund’s portfolio in July 2020. Our investment thesis for the company can be found here. Back then, the company was still named Square – the name-change to Block happened in December 2021. In late-March this year, we completely exited Block. This article describes our Sell thesis for the company.

When we invested in Block, the company had two business units that it called the Seller Ecosystem and Cash App Ecosystem, respectively. Through the Seller Ecosystem, Block provided software, hardware, and financial services that help merchants collect payments, run their businesses better, and obtain financing. The Cash App Ecosystem consisted of a suite of financial services for individuals to send and receive funds, spend, and invest (the assets that individuals could invest in via Cash App included Bitcoin). At the time of our investment, Block had impressive historical growth in GPV (gross payment volume); the GPV metric was important for Block because the majority of the company’s ex-Bitcoin revenue back then depended on transaction-based services. Block also reported tremendous growth in Cash App monthly active users (MAUs); the growing user base provided the fuel for Cash App’s revenue growth. But as time progressed after our investment in Block, growth in the company’s GPV and Cash App MAUs deteriorated.

From 2021 to 2024, Block’s GPV for the Square business (the Seller Ecosystem business unit changed its name to Square when the company changed its name from Square to Block) compounded at just 14.2% per year from US$152.8 billion to US$227.7 billion. This severely lagged the growth in payment volumes for peers of the Square business such as Toast and Shift 4 over the same period. Toast’s payment volume grew by 40.8% per year from US$57.0 billion to US$159.1 billion while Shift 4’s payment volume increased by an even faster annual pace of 52.3% from US$46.7 billion to US$164.8 billion.

When we sold Block, the latest guidance for Square’s GPV in 2025 was for high-single-digit growth in the first quarter, increasing to low-double-digit growth in the fourth quarter. For Toast, GPV was expected to increase in the low-to-mid 20-percentage range in 2025 (if its take rate, defined as gross profit as a percentage of GPV, is assumed to remain constant); for Shift4, its growth in GPV (termed end-to-end payment volume) was expected to be between 21% and 33%.

Square’s GPV growth in 2024 was just 8.6%, so management’s expectation is for GPV growth to reaccelerate in 2025. But we have doubts over management’s plan to achieve this. In Block’s 2024 fourth-quarter shareholder’s letter (the company’s latest earnings update before we exited the position), management shared one of their strategies to grow Square’s GPV:

“Our strategy is to bring our ecosystems together with a focus on neighborhoods. Block by block, we will build a new “neighborhood network” that connects sellers, buyers, staff, and artists, each positively reinforcing the other. Square and Cash App are already stitched into the fabric of local communities. The neighborhood is where our core products naturally intersect, fueling local economies and strengthening the financial health of those within them. As the world becomes more global and uniform, people will seek out authentic, local, real-life interactions. We’re going to help sellers provide it and help buyers find it.”

We don’t think this solves the problem of lacklustre GPV growth. We think it’s more important for management to improve the feature-set within Square to attract more merchants; having more merchants is what can move the needle in Square’s GPV growth.

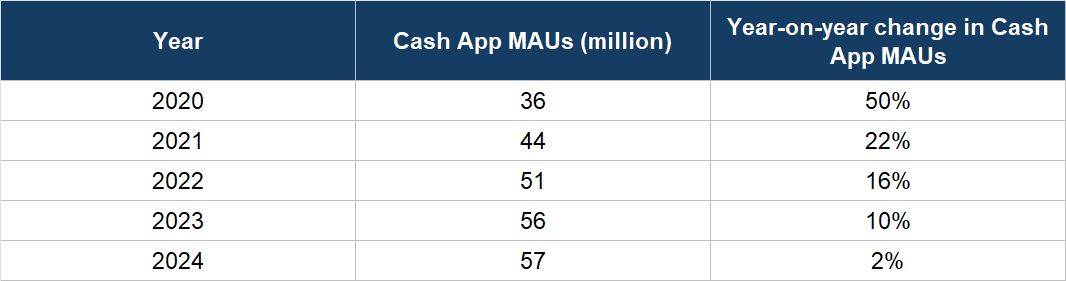

Coming to Cash App’s MAUs, the trend in the metric’s growth rate is shown in Table 1 below; note the rapid deceleration in 2023 and 2024.

Table 1; Source: Block annual report

The apparent saturation in Cash App’s MAUs at less than 60 million is a big worry for us because it is much tougher for the business unit to achieve healthy revenue growth with a stagnant user base as compared to a user base that is growing at say 15% or more. We also think we had made a mistake in our initial analysis of Cash App’s growth potential – we thought Cash App will only reach saturation with a much larger number of MAUs than what it has currently.

We applaud management’s understanding of stock-based compensation’s (SBC’s) deleterious effects on shareholder value when used inappropriately; this is especially so in the current environment where many companies routinely tout their profitability metrics after adding back SBC. In the company’s 2022 fourth-quarter earnings conference call, Jack Dorsey, the company’s leader and cofounder, commented on the topic (emphasis is ours):

“While Adjusted EBITDA margin is one of the key profit disclosures we’ve focused on in the past, we recognize it excludes certain expenses like stock based compensation which is a real, meaningful ongoing cost of operating our business. It isn’t a cash expense but it’s a real expense, so we are going to include it in how we assess our investments and performance, and to do so, we are developing better signals around it.

As a result, we are shifting our focus to an Adjusted Operating Income margin. With this metric, profit margins will include certain non-cash expenses, like stock based compensation and depreciation and amortization.”

But we’re concerned with the headwinds we see to Block’s future growth, which are the lacklustre growth in Square GPV and the inability to enlarge Cash App’s MAUs.

We made our initial investment in Block at an average price of US$127 per share, but sold at a much lower average price of US$55. The big decline in Block’s stock price might lead someone reading this to ask: “Couldn’t you have sold Block earlier?” It’s a valid question. Our response will be something we shared in Compounder Fund’s Owner’s Manual:

“And on the topic of selling stocks, we will typically sell a stock in Compounder Fund’s portfolio if we find that the investment thesis is completely broken, or we have made a big mistake in our analysis. But we will be very slow to sell. The slowness is by design – it strengthens our discipline in holding onto the winners in Compounder Fund. Holding onto the winners will be a very important contributor to Compounder Fund’s long run performance.”

Part of the capital from the sale of Compounder Fund’s Block shares was redeployed to some existing companies in the portfolio (in this case, the companies were Alphabet, Amazon, and The Trade Desk).

And here’s an important disclaimer: None of the information or analysis presented is intended to form the basis for any offer or recommendation; they are merely our thoughts that we want to share. Of all other companies mentioned in this article, Compounder Fund owns shares in Alphabet, Amazon, and The Trade Desk. Holdings are subject to change at any time.