Compounder Fund: Salesforce Investment Thesis - 29 Jan 2021

Data as of 26 January 2021

Salesforce (NASDAQ: CRM), which is based and listed in the USA, is one of the 40 companies in Compounder Fund’s initial portfolio. This article describes our investment thesis for the company.

Company description

Founded in 1999, Salesforce is one of the pioneers of delivering software subscription services over the cloud. Today, this model is popularly known as software as a service, or SaaS, and Salesforce is a global leader in cloud-based customer relationship management (CRM) software.

Salesforce’s software products help businesses to: (1) Manage and track their marketing processes and their customers’ experiences; (2) onboard and track their sales leads; and (3) manage customer service operations for their existing customers. The company offers three separate software platforms to manage each of these three processes: (1) Marketing and Commerce Cloud; (2) Sales Cloud; and (3) Service Cloud. Salesforce also combines the three platforms into its Customer 360 Platform, which unites sales, service, marketing, commerce, integration, analytics and more to give companies a single source of truth about their customers.

The better organisation of data, sales tracking, and forecasting that Salesforce provides leads to better business results for its customers. The average Salesforce customer experiences a 44% increase in lead volume, 37% increase in win-rate, 37% increase in sales volume, and a 45% increase in customer retention.

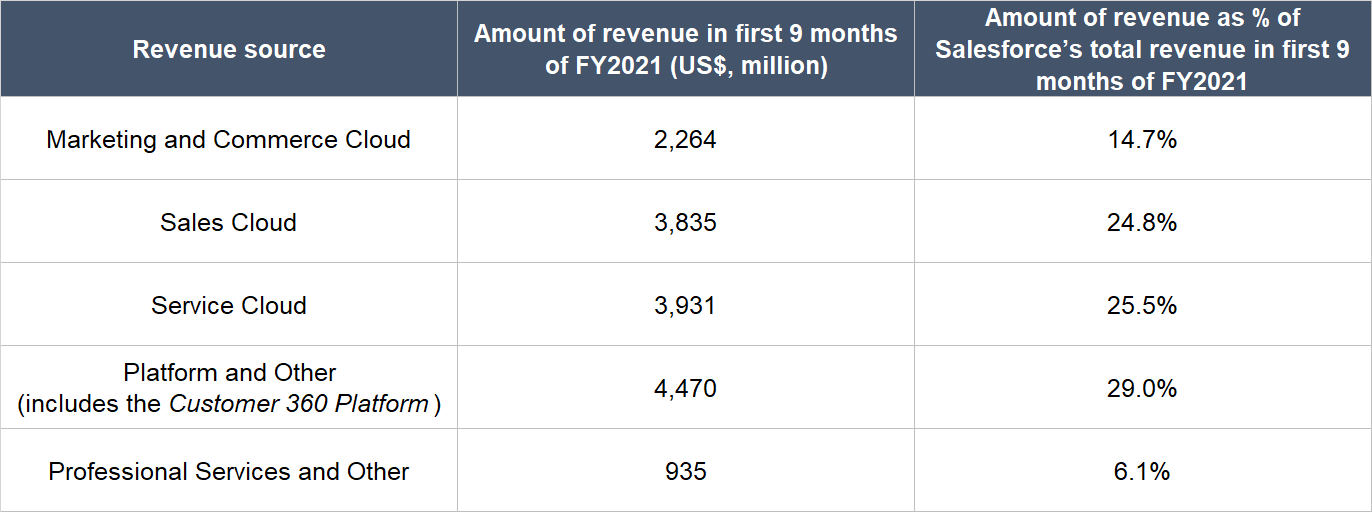

In the first nine months of its fiscal year ending 31 January 2021 (FY2021), Salesforce earned US$15.44 billion in revenue. This revenue can be split into the following categories:

Source: Salesforce quarterly earnings update

From a geographical perspective, 69.5% of Salesforce’s total revenue for the first nine months of FY2021 came from the Americas, 21.1% from Europe, and the remaining 9.4% from the Asia Pacific region.

Investment thesis

We have laid out our investment framework in Compounder Fund’s website. We will use the framework to describe our investment thesis for Salesforce.

1. Revenues that are small in relation to a large and/or growing market, or revenues that are large in a fast-growing market

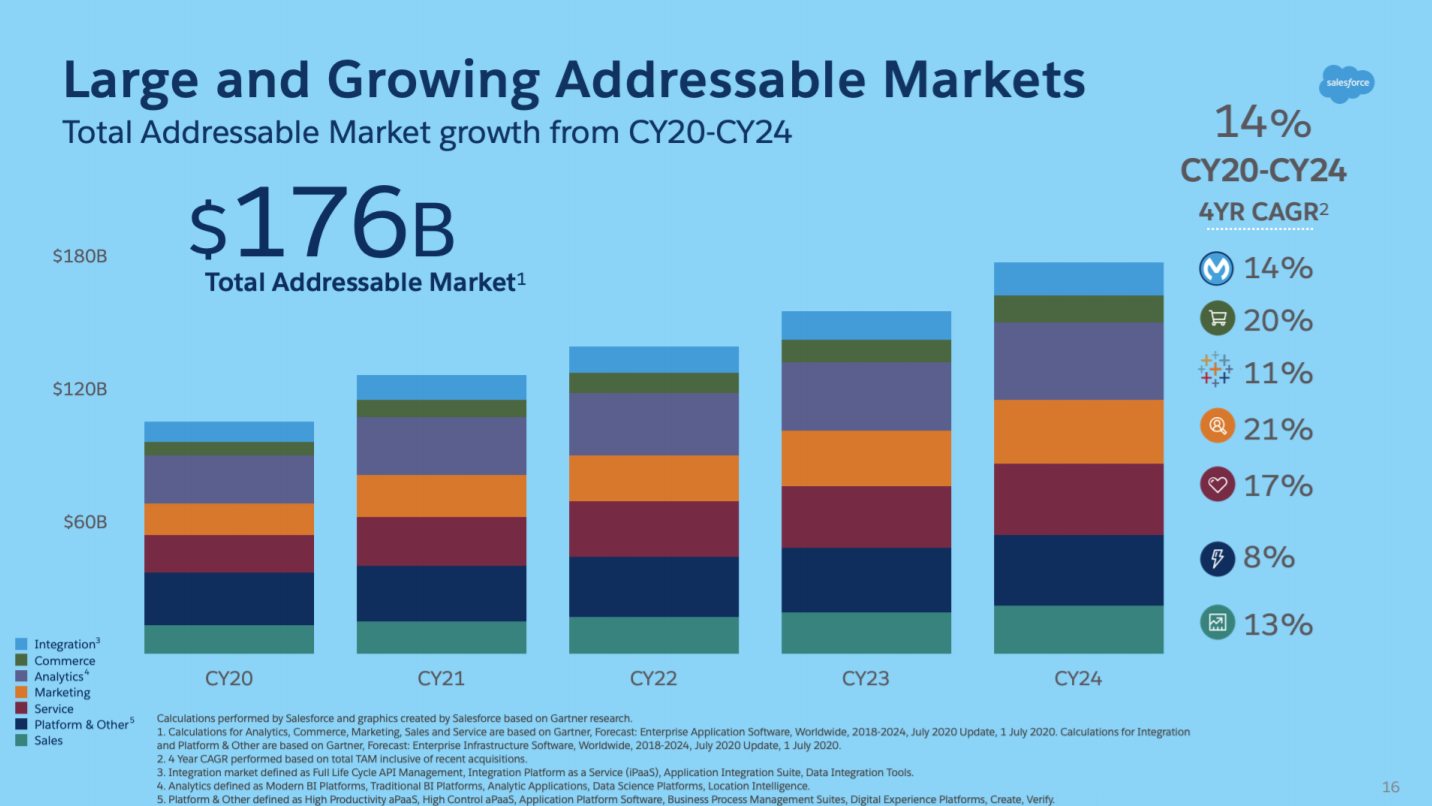

Salesforce’s revenue of US$20.29 billion in the 12 months ended 31 October 2020 is already significant. It is not a small company. But the market opportunity is much higher. Based on Salesforce’s estimates using data from Gartner’s research, its addressable market is projected to increase from around US$100 billion in 2020 to US$176 billion by 2024, as shown in the chart below.

Source: Salesforce FY2021 second-quarter earnings presentation

So it’s clear that Salesforce is operating in a large and fast-growing market and this gives plenty of room to run for the company.

We also want to highlight that Salesforce has a penchant for growing its addressable market over time. In its IPO prospectus (Salesforce was listed in 2004), Salesforce stated that the CRM software market it was participating in was just US$7.1 billion in 2002, according to a July 2003 report by market researcher IDC. The company first exceeded US$7 billion in annual revenue in FY2017 and today, Salesforce’s revenue is more than US$20 billion.

2. A strong balance sheet with minimal or a reasonable amount of debt

Salesforce exited the third quarter of FY2021 with a robust balance sheet. As of 31 October 2020, the company had a total of US$9.49 billion in cash and marketable securities and just US$2.67 billion in total debt (which are all long-term debt). But the picture will soon change.

In December 2020, Salesforce announced that it would be acquiring Slack, an enterprise communications platform provider, with both cash and shares. Based on Salesforce’s 30 November 2020 share price, Slack will be bought at an enterprise value of US$27.7 billion, and around US$15.4 billion of the price-tag will be paid by Salesforce in cash. To help finance the Slack deal, Salesforce has already put in place a loan facility of US$10 billion.

When the Slack acquisition is completed (which is expected to be in the second quarter of FY2022), Salesforce’s balance sheet should have significantly higher debt than cash and marketable securities. But we’re not worried. The company has a long history of generating positive and growing free cash flow as we’ll show later. For some perspective now, Salesforce produced US$3.69 billion in free cash flow in FY2020 and even with COVID-19 around in the first nine months of FY2021, Salesforce’s free cash flow still came in at US$2.07 billion.

3. A management team with integrity, capability, and an innovative mindset

On integrity

Salesforce’s most important leader is its 55-year old co-founder Marc Benioff. He is Salesforce’s chairperson and CEO and has been in these roles since 1999 (the year of the company’s founding) and November 2001, respectively. We appreciate the fact that Benioff is still relatively young, but already has more than two decades of experience leading Salesforce.

In FY2020, Benioff’s total compensation was US$25.97 million. This is a hefty sum, but is merely a rounding error when compared to Salesforce’s free cash flow of US$3.69 billion for the year. More importantly, 77% of Benioff’s total compensation (US$20 million) came from stock-based awards that we think are sensibly structured. Benioff’s stock-based awards consist of three components:

- There are performance-based restricted stock units (PRSUs) that vest over three years. The amount of PRUSs to be vested depends on Salesforce’s stock price performance, relative to the NASDAQ 100 index, over the same period. For example, if Salesforce’s stock price performance is among the 30-worst performing stocks in the NASDAQ 100 over the three-year vesting period, none of the PRSUs that are granted will vest; and if Salesforce’s stock price performance is within the top 40-best performing stocks in the NASDAQ 100 over the three-year vesting period, then more than 100% of the PRSUs that are granted will vest (the percentage is capped at 200% if Salesforce’s stock price performance is at the 99th percentile).

- There are restricted stock units (RSUs) that vest over a four-year period.

- There are stock options that also vest over a four-year period.

The three components of Benioff’s stock-based awards effectively bind his compensation to Salesforce’s long-term stock price movement, which is in turn tethered to Salesforce’s long-term business performance. So we think that Benioff’s interests are well-aligned with that of Salesforce’s other shareholders.

Speaking of alignment of interests, Benioff controlled 29.04 million Salesforce shares as of 30 October 2020 (the date of his latest regulatory filing). This is just over 3% of Salesforce’s current total share count of 915 million, which seems like a tiny stake. But it’s still huge in absolute monetary terms – based on Salesforce’s 26 January 2021 share price of US$226, Benioff’s shares are worth a cool US$6.57 billion. We like our companies to have leaders who are major shareholders themselves, and Benioff looks to us to have significant skin in the game.

On capability and ability to innovate

We think Benioff shines in this area, and there are a few things we want to discuss.

First, as mentioned earlier, Salesforce is one of the pioneers – if not, the pioneer – of the SaaS movement. When Benioff co-founded Salesforce, he based the company on three big ideas: First, that software should be delivered over the internet; second, that software should be bought by users on a subscription basis; and third, that philanthropy must be an important part of the company’s culture (there will be more on the philanthropy later). The first two ideas combined is what is known as the SaaS model today.

While the SaaS business model is widely accepted currently, Benioff did not have it easy when he started. In fact, at the beginning, not a single venture capitalist that Benioff met in Silicon Valley wanted to invest in his company. Back then, the venture capitalists probably did not understand the power of the SaaS business model, how it would: (1) Simplify the onboarding of customers; (2) give the software provider the ability to update and improve its software on the go; and (3) enable users to scale their use of the software quickly and seamlessly. Being one of the first SaaS companies around, there was hardly any precedent for venture capitalists to study to imagine what the future for Salesforce could look like: The idea of people paying a monthly fee for something (software-subscriptions delivered over the cloud) that they could just get a perpetual license for (the traditional way of delivering software to users) probably seemed unthinkable to the venture capitalists.

In our minds, the fact that Benioff was one of the first few individuals in the technology world to recognise the would-be importance of the SaaS model speaks volumes about his ability to innovate.

Second, Salesforce has a long history, under Benioff’s leadership, of introducing new products over time. The company does not rest on its laurels and Benioff once described Salesforce’s attitude of relentless innovation as “changing the engines on a 747 in mid-flight.” The chart below shows Salesforce’s history of product introductions from the company’s founding to 2016:

Source: Salesforce 2016 investor presentation

Here are some highlights from the major innovations shown in the chart:

- AppExchange, introduced in 2005, is a platform for third-party software developers to build apps and offer it to Salesforce customers. At the end of FY2018, AppExchange had facilitated over five million app installs, and 95% of the Fortune 100 companies had used one or more apps from the platform.

- The Salesforce1 Platform, introduced in 2013, is an app development platform that included built-in social networking features, and the software-configuration to be used on mobile devices. Notably, Veeva Systems, another of Compounder Fund’s holdings, uses the Salesforce1 platform to power much of its CRM software service.

- Salesforce Einstein, launched in 2016, provides a set of artificial intelligence (AI) tools that are accessible across Salesforce’s products. Einstein delivers customer insights and is currently generating over eighty billion predictions per day, up from ‘just’ one billion daily predictions in FY2019.

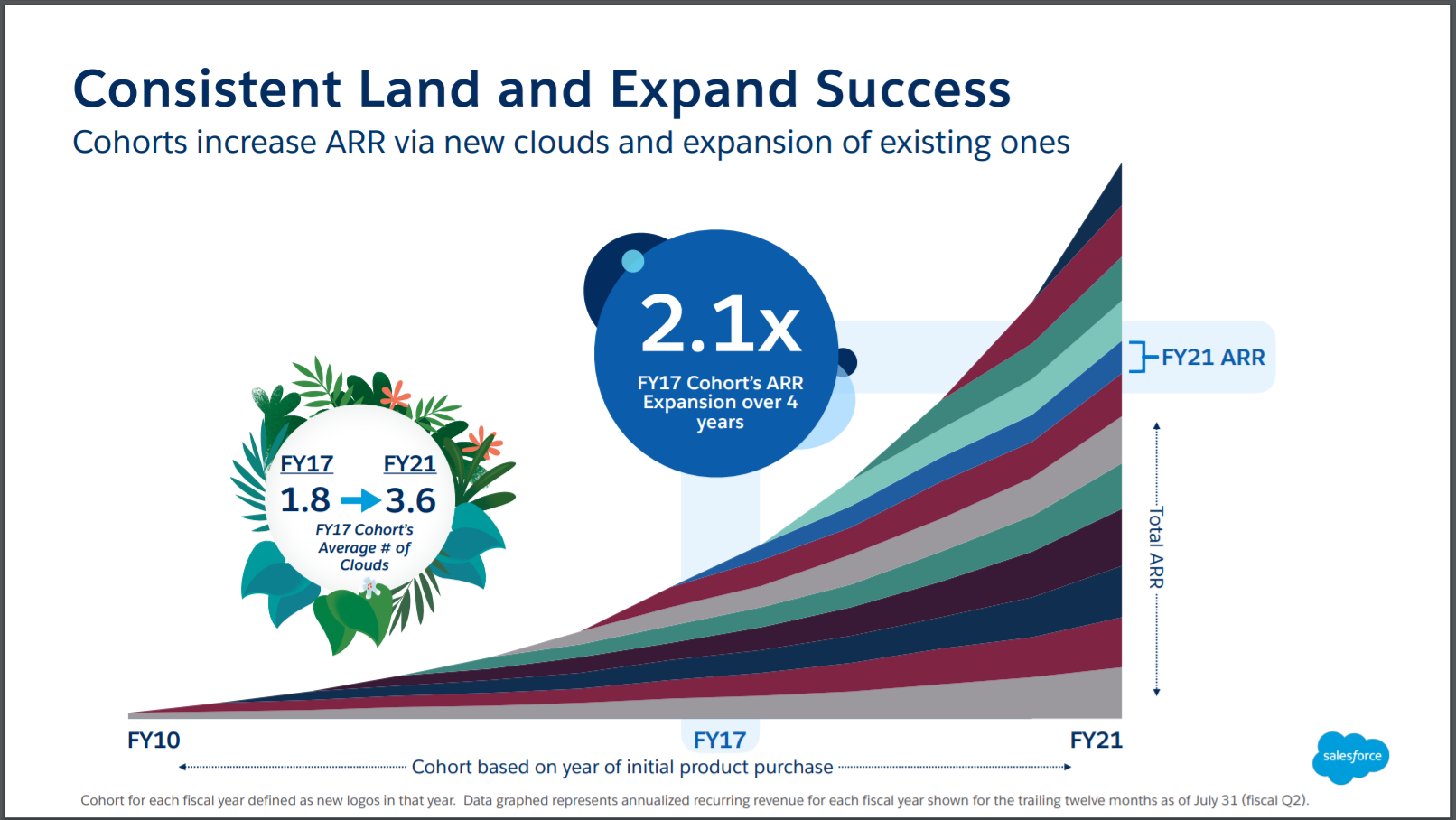

Third, Salesforce has produced solid growth in annual recurring revenue (ARR) in its customer-cohorts over many years, demonstrating the success of its land-and-expand strategy. This is illustrated in the chart below, which shows the changes in the total ARR among its customer-cohorts from FY2010 to FY2021. In the chart, each coloured-slice represents a customer-cohort. The lowest slice (light grey in colour) is the cohort of customers that joined Salesforce in FY2010 and you can see that the slice gets thicker over time, showing that the total ARR the company earns from the FY2010 cohort has grown as the years go by. The chart also shows how the FY2017 cohort grew their ARR by 2.1 times by FY2021.

Source: Salesforce 2020 investor presentation

Fourth, Benioff has successfully led Salesforce to meet ambitious growth targets while also increasing the company’s already-leading-market-share in the global CRM software market. In a 2017 investor presentation, when Salesforce’s revenue for FY2017 was US$8.4 billion, the company’s management shared a target to hit US$20-US$22 billion in revenue by FY2022. Based on Salesforce’s results for the first nine months of FY2021, the company has achieved trailing revenue of US$20.29 billion. Benioff is now targeting revenue of more than US$50 billion by FY2026, which will represent annual growth of around 19% from FY2021.

The chart below shows the market share gains achieved by Salesforce from 2015 to 2019. The company was already the leader in the global CRM applications market in 2015 and grew its market share to 18.4% in 2019.

Source: Salesforce FY2021 first quarter earnings presentation

Fifth, we think Benioff has built a great culture at Salesforce. To expand on this point, we need to take a trip down memory lane. A few years before he co-founded Salesforce, Marc Benioff was the youngest vice president at technology giant Oracle. Despite enjoying a successful career that came with a fantastic salary and lavish perks, he was burnt out. Benioff’s then-boss, Oracle founder and multi-billionaire, Larry Ellison, suggested a sabbatical. Benioff took up the offer and visited India. After his trip, Benioff decided to build a company not just for profit, but to also serve a greater purpose.

Benioff’s desire to serve a greater purpose manifested in Salesforce’s 1-1-1 philanthropy model, which sees the company devote 1% of its equity, 1% of its product, and 1% of its employees’ time to societal causes. Salesforce shared in its FY2021 second quarter earnings presentation that to-date, it has given US$392 million in grants, provided its products to more than 49,000 non-profit organisations for free or at a discount, and its employees have collectively volunteered more than 5.2 million hours globally.

Having a greater purpose has probably helped Salesforce to create happy and motivated employees. According to the Great Place To Work organisation, 92% of Salesforce employees say that it is a great place to work, compared to just 59% for a typical company. Meanwhile, on the Glassdoor platform, Salesforce has a 4.4-star rating (out of five), 90% of Salesforce raters will recommend the company to a friend, and Benioff has a 97% approval rating (in 2019, the average Glassdoor CEO rating was just 69%).

4. Revenue streams that are recurring in nature, either through contracts or customer-behaviour

The lion’s share of Salesforce’s revenue comes from subscriptions. In the first nine months of FY2021, 93.9% of the company’s total revenue of US$15.44 billion came from subscriptions to its cloud-based software products. In fact, subscriptions have never accounted for less than 90.9% of Salesforce’s annual revenue going back to at least FY2007. A typical subscription term for Salesforce’s software products is one to three years and is non-cancelable.

But just having a subscription model and non-cancelable subscription terms does not equate to having recurring revenues. If your business has a high attrition rate (the rate of customers leaving after their contracts expire), you’re constantly filling a leaky bucket. That’s not recurring income.

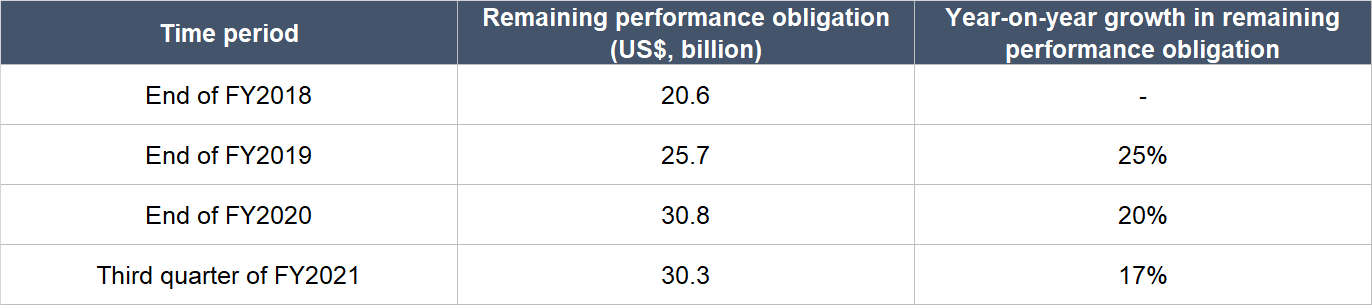

There are four reasons why we think Salesforce does not have to deal with a leaky bucket. First, the attrition rate for Salesforce’s core services in FY2018, FY2019, and FY2020 were less than 10% in each year. Second, the company has produced excellent revenue growth and high free cash flow margins for a long time, as we’ll show later. Third, we mentioned earlier that Salesforce has a long history of producing growing ARR among its customer cohorts. Fourth, Salesforce’s remaining performance obligation (RPO) has increased at a strong clip in recent years as the table below shows. RPO is effectively contracted revenue that will be recognised by Salesforce in the future; it includes contracts that customers have already paid for or will pay for in the future.

Source: Salesforce annual reports

We also want to highlight that Salesforce has a diversified revenue stream, which we think strengthens the recurring nature of the company’s business. No single customer accounted for more than 5% of Salesforce’s revenues in FY2018, FY2019, and FY2020.

5. A proven ability to grow

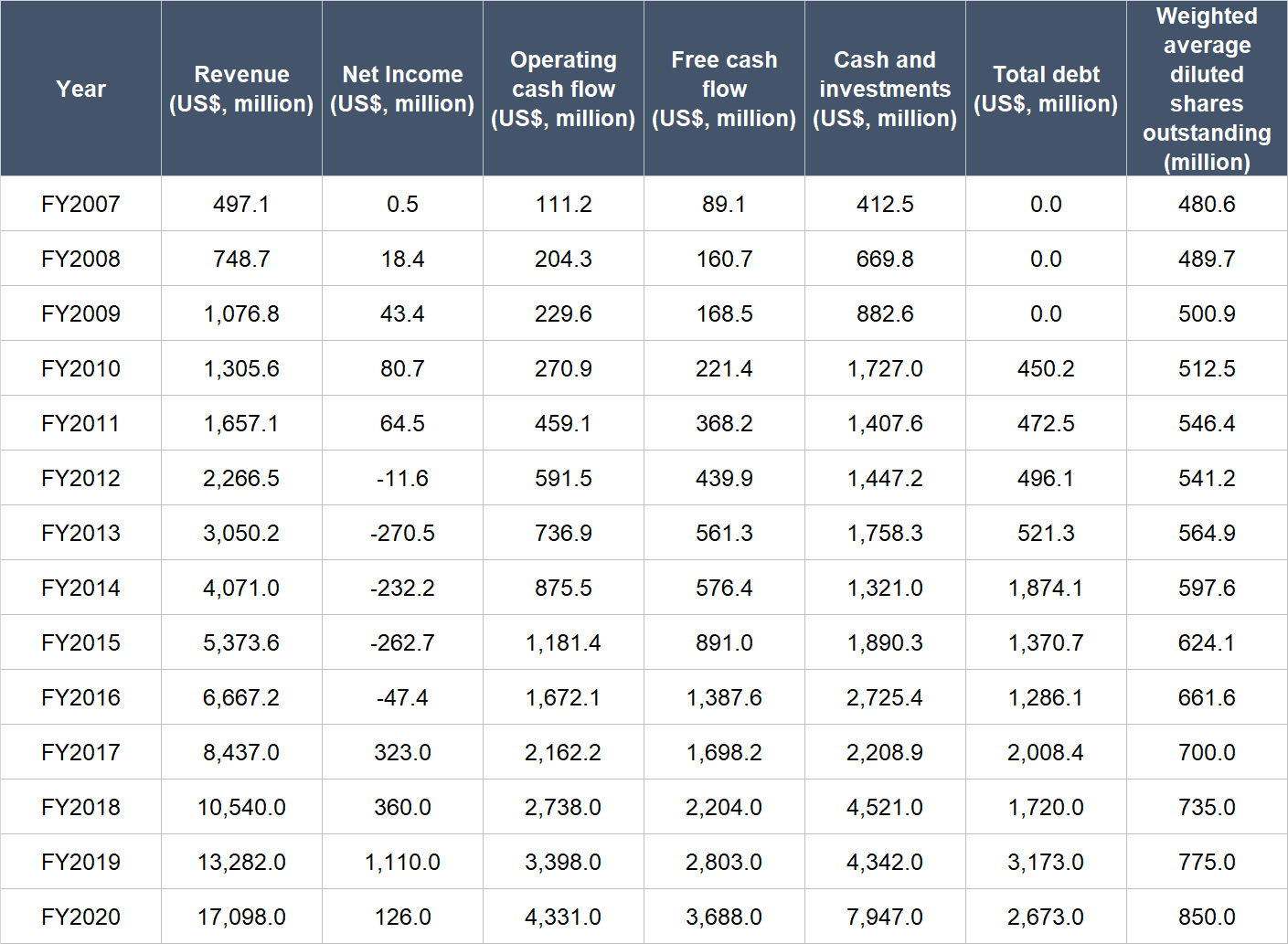

The table below shows Salesforce’s important financial numbers from FY2007 to FY2020 (we chose FY2007 as the starting point to observe how the company fared during the Great Financial Crisis period):

Source: Salesforce annual reports

A few key points about Salesforce’s financials:

- Revenue grew in each year we studied and compounded at an impressive annual rate of 31.3%. More importantly, the growth was not front-loaded. Salesforce’s revenue increased by 26.0% per year from FY2015-FY2020, and was up by 28.7% in FY2020.

- Net income was erratic from FY2007 to FY2020, but we’re not focused on this metric – we’re more concerned with Salesforce’s cash flows, and this is where the company shines.

- Operating cash flow and free cash flow were both consistently positive and growing for the entire time frame we’re looking at. From FY2007 to FY2020, Salesforce’s operating cash flow and free cash flow compounded at excellent annual rates of 32.5% and 33.2%, respectively. The nearer-term growth of the two financial numbers has been equally strong too for the FY2015-FY2020 period (29.7% per year for operating cash flow and 32.9% per year for free cash flow).

- Salesforce’s balance sheet was strong throughout, with cash & investments outweighing debt in all years except for FY2014. There was a net-debt position of US$533 million for the year, but it looked very manageable compared to Salesforce’s free cash flow.

- Salesforce has been diluting shareholders, with its weighted average diluted share count having increased annually by 4.5% and 6.4% for the FY2007-FY2020 and FY2015-FY2020 time periods. But the increase in Salesforce’s weighted average diluted share count has been much lower than the growth in its revenue and free cash flow, so we don’t think the dilution is a problem.

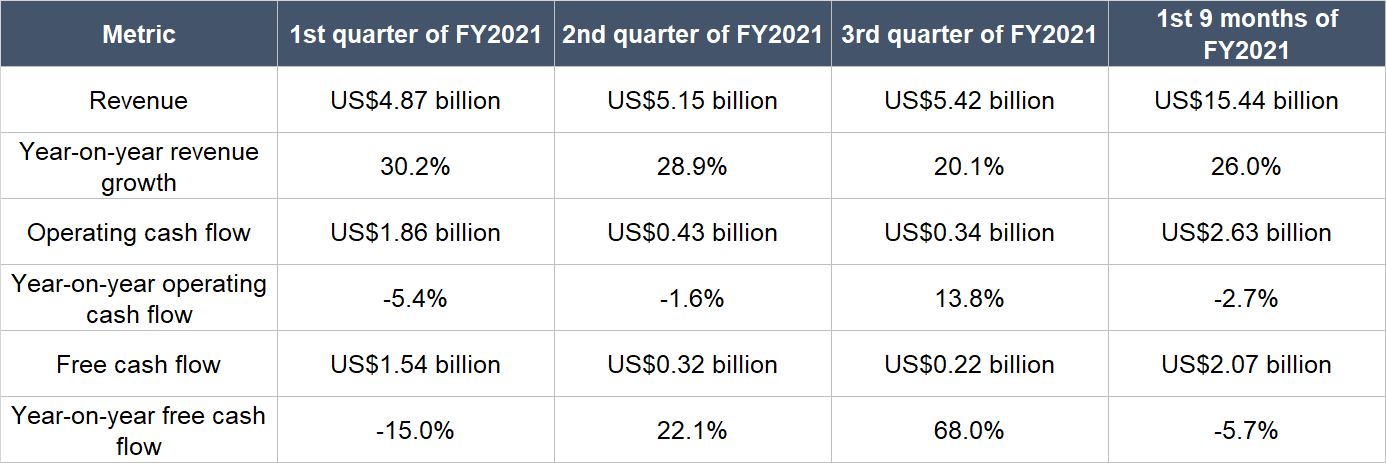

The table below shows the changes in Salesforce’s revenue, operating cash flow and free cash flow in the first three quarters of FY2021. The company has continued to produce impressive top-line growth despite the presence of COVID-19. And although operating cash flow and free cash flow did not grow during the period, the two important financial numbers were still robust. While we’re firmly focused on the long run growth of Salesforce (and we think the future is bright!), we also want to highlight that the company’s current remaining performance obligation as of 31 October 2020 (current RPO represents revenue that will be recognised over the next 12 months) stands at US$15.3 billion, up 20% year-on-year. This sets Salesforce up well for FY2022.

Source: Salesforce quarterly earnings updates

6. A high likelihood of generating a strong and growing stream of free cash flow in the future

There are two reasons why we think Salesforce excels in this criterion.

First, there’s still significant room to grow for Salesforce. Earlier, we showed that its estimated total addressable market in 2024 (US$176 billion) is more than eight times higher than its current trailing revenue (US$20.29 billion). More importantly, Salesforce is a highly innovative company. It was one of the pioneers of the SaaS business model more than 20 years ago – a model which has become so important in the world today – and its business continues to grow at a robust pace. We won’t be surprised at all if Salesforce is able to grow its total addressable market in the years ahead.

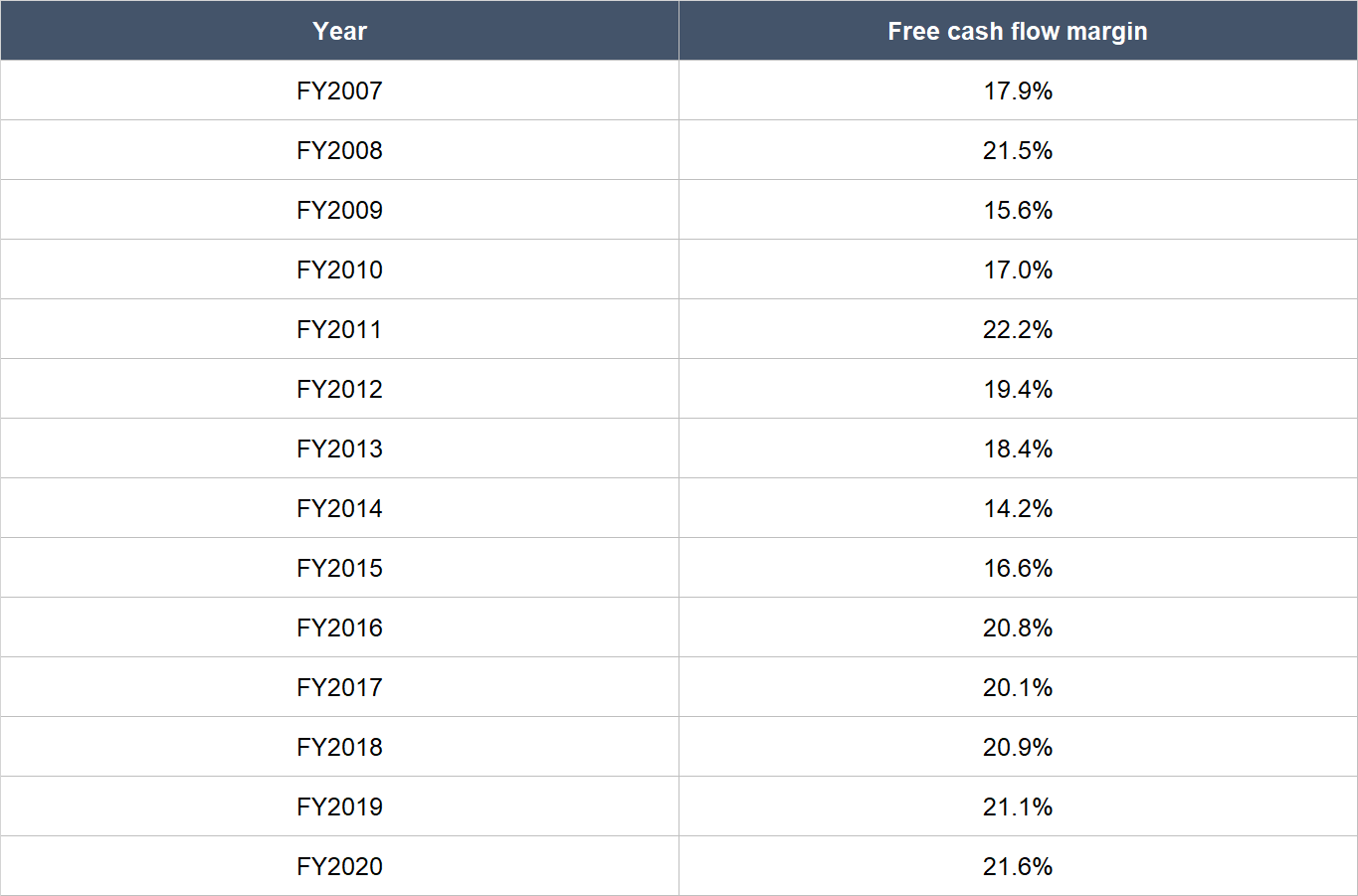

Second, Salesforce has been generating strong and growing free cash flow for years, as we’ve shown earlier. The table below illustrates the company’s free cash flow margin (free cash flow as a percentage of revenue) going back to FY2007. The company’s average free cash flow margin for FY2015-FY2020 was an impressive 20.9%. Despite the presence of COVID-19 in the first nine months of FY2021, Salesforce’s free cash flow margin was still a respectable 13.4% for the period.

Source: Salesforce annual reports

Valuation

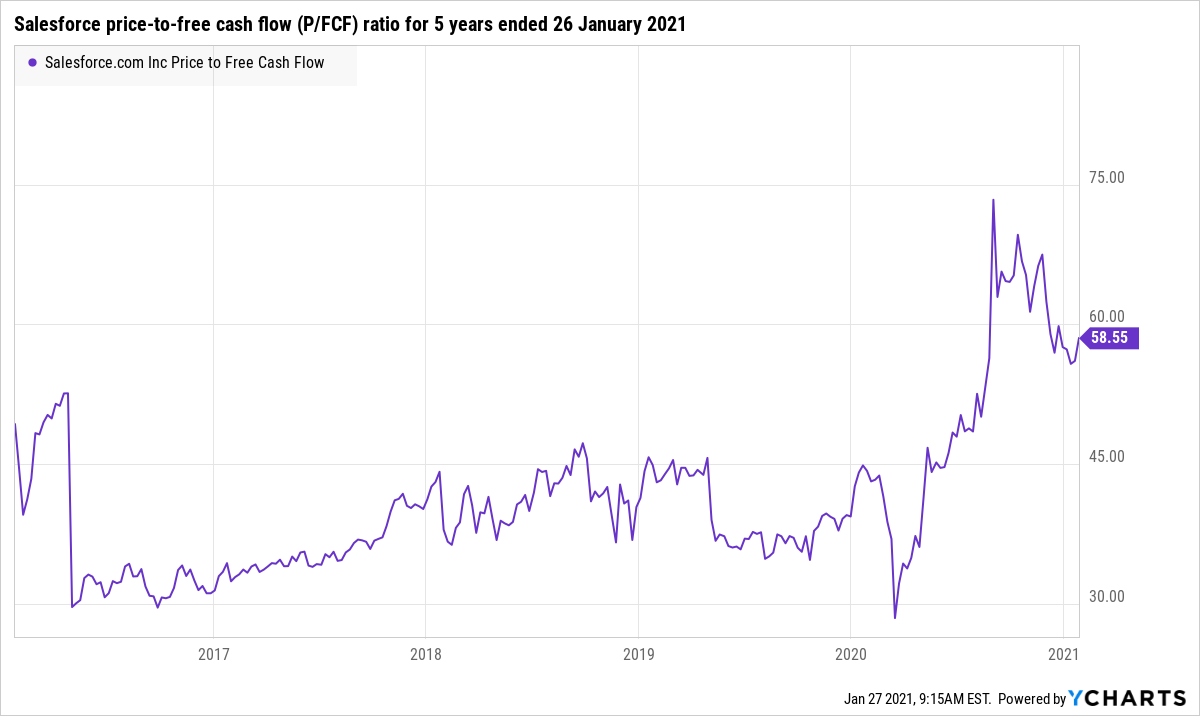

We completed our purchases of Salesforce shares with Compounder Fund’s initial capital in late July 2020. Our average purchase price was US$191 per Salesforce share. At our average price and on the day we completed our purchases, the company’s shares had a trailing price-to-free cash flow (P/FCF) ratio of around 51.

We like to keep things simple in the valuation process. In Salesforce’s case, we think the P/FCF ratio is an appropriate metric to gauge the value of the company. This is because Salesforce already has a long history of producing positive and growing free cash flow.

The P/FCF ratio of 51 is high in and of itself – and that’s a risk. This ratio is also high relative to its own history: The chart below shows Salesforce’s P/FCF ratio for the five years ended 26 January 2021:

But Salesforce has a huge total addressable market that is likely to grow in the future. The company also has a long history of solid growth, so we think there’s a high probability that Salesforce can continue to take advantage of its market opportunity to increase the scale of its business. Because of these, we’re happy to pay up for Salesforce as we think there’s a good chance it could grow into its valuation.

For perspective, Salesforce carried a P/FCF ratio of around 59 at the 26 January 2021 share price of US$226.

The risks involved

We see five major risks to our investment in Salesforce.

1. Key-man: We think Marc Benioff’s presence has been a critical reason for Salesforce’s success. He has a fierce innovative streak and has proven that he can lead the company to execute strongly. If he leaves Salesforce for whatever reason, we will be concerned with the leadership transition. The good thing is that Benioff is still relatively young at 55, so he likely still has plenty of gas left in the tank to continue leading Salesforce.

2. Competition: We showed earlier that Salesforce counts other software behemoths such as Oracle and Microsoft as competitors. Both have revenues that are much higher than Salesforce’s, so they do have strong financial firepower. But we’re comforted by Salesforce’s growing market share, which we take to be a sign that Salesforce is more than able to hold its own against the competition. In FY2020, 90% of the Fortune 500 companies were customers of Salesforce, and we think this is another demonstration of the company’s strength.

3. Capital allocation: Salesforce has been aggressive when it comes to acquisitions and has in fact depended on acquiring other software companies to help fuel its growth. According to Crunchbase, Salesforce has made at least 66 acquisitions in its history. Recent examples include the acquisitions of 13 companies in FY2017 for a total of US$4.4 billion, Mulesoft for US$6.4 billion in May 2018, Tableau for US$14.8 billion in August 2019, ClickSoftware Technologies for US$1.4 billion in October 2019, and of course, the soon-to-be-completed purchase of Slack for US$27.7 billion that we mentioned earlier. These are not trivial sums when compared to the scale of Salesforce’s business. Salesforce also often uses its shares as currency when making acquisitions, and this has resulted in dilution for its shareholders. But to the credit of Benioff and his team, we think the acquisitions, in aggregate, have been great and are beneficial to Salesforce’s long-term growth. The dilution is also not a problem, as we had discussed earlier. But there’s no guarantee that future acquisitions by Salesforce will turn out well. We’re watching the company’s capital allocation decisions.

4. Data security: Because of the nature of Salesforce’s business, it handles plenty of sensitive and proprietary data of its customers. If Salesforce were to suffer any data breaches, it could lead to a severe loss of customer-confidence and hurt its future growth prospects.

5. High valuation: We’re comfortable with paying up for Salesforce’s shares. But if the company’s growth falters – even if it’s temporary in nature – there could be painful falls in its share price.

Summary and allocation commentary

To sum up Salesforce, the company has:

- A large market opportunity relative to its current revenue; management has also been adept at growing Salesforce’s addressable market over time

- A robust balance sheet currently; even though the picture will soon change with the impending acquisition of Slack, we’re not worried since Salesforce has a long history of generating strong free cash flow

- A top-notch leader in Marc Benioff, who not only possesses integrity, but is also highly capable and innovative

- High levels of recurring revenues from subscriptions due to its SaaS business model

- An excellent long-term track record of growth in revenue, operating cash flow, and free cash flow, all the while maintaining a strong balance sheet

- A high chance of being able to generate higher free cash flow in the future.

There are risks involved with Salesforce, as it is with all companies. The key ones we’ve identified include key-man risk; the presence of competitors with fat wallets; the risk that Salesforce’s future acquisitions may turn out to be poor capital allocation decisions; reputational-risk in the event that Salesforce suffers from a data breach; and the company’s high valuation.

After weighing the pros and cons, we initiated a 2.5% position – a medium-sized allocation – in Salesforce with Compounder Fund’s initial capital. We appreciate all the company’s strengths and think that the company has a high probability of being able to take advantage of the large addressable market that it’s seeing. But at the same time, our enthusiasm is tempered slightly by Salesforce’s penchant for making acquisitions to boost growth. It’s not easy to acquire well.

And here’s an important disclaimer: None of the information or analysis presented is intended to form the basis for any offer or recommendation; they are merely our thoughts that we want to share. Of all the other companies mentioned in this article besides Salesforce, Compounder Fund also owns shares in Microsoft and Veeva Systems. Holdings are subject to change at any time.