Compounder Fund: Zoom Video Communications Investment Thesis - 24 Sep 2020

Data as of 21 September 2020

Zoom Video Communications Inc (NASDAQ: ZM) is one of the 40 companies in Compounder Fund’s initial portfolio. This article describes our investment thesis for the company.

Company description

Zoom, which is based and listed in the USA, provides a video-first communications platform. In Zoom’s own words, it “connect[s] people through frictionless video, phone, chat, and content sharing. and enable[s] face-to-face video experiences for thousands of people in a single meeting across disparate devices and locations.”

The cornerstone of Zoom’s platform is the Zoom Meetings product, which can be set up and used on your laptop, desktop, tablet or mobile devices. Zoom Meetings can be integrated with tools from other major software providers; can support tens of thousands of video participants in a single meeting; and can allow one-to-one, one-to-many, and many-to-many conversations. Anyone can use Zoom Meetings for free, but will have to pay for a subscription for additional features. Paying subscribers can enjoy features such as longer group meetings, a higher number of participants per meeting, and more.

In addition to Zoom Meetings, Zoom’s other products include:

- Zoom Phone: A cloud-based PBX (private branch exchange) phone system that enables users to receive and make calls on their connected devices.

- Zoom Chat: A chat function within Zoom Meetings and Zoom Phone that also allows the sharing of audio files, images, and other content.

- Zoom Rooms: A software-based conference room system, utilising off-the-shelf hardware, that helps companies turn their physical meeting rooms into online video conferencing rooms.

- Zoom Conference Room Connector: Helps businesses bring their traditional video conferencing hardware systems to the cloud.

- Zoom Video Webinars: Software that empowers users to broadcast live videos featuring up to 100 panelists and 10,000 view-only attendees.

- Zoom for Developers and Zoom App Marketplace: Enables other software developers to integrate Zoom’s products with other software applications.

- Zoom for Home: A hardware product launched in July this year, Zoom for Home is a device that can be easily set up at home for high-quality video conferencing to support remote work.

In the fiscal year ended 30 January 2020 (FY2020), Zoom earned US$622.7 million in revenue. The Americas accounted for 81% of this, with EMEA (Europe, Middle East and Asia) taking up 11% and the remaining 8% belonging to the APAC (Asia Pacific) region.

Investment thesis

We have laid out our investment framework in Compounder Fund’s website. We will use the framework to describe our investment thesis for Zoom.

1. Revenues that are small in relation to a large and/or growing market, or revenues that are large in a fast-growing market

In its IPO prospectus (Zoom listed on 18 April 2019), Zoom reported that the market segments it serves would represent a US$43.1 billion opportunity in 2022, according to market intelligence provider International Data Corporation (IDC). IDC defines Zoom’s market as Unified Communications and Collaboration; within this, Zoom addresses the Hosted / Cloud Voice and Unified Communications, Collaborative Applications, and IP Telephony Lines segments.

But Zoom believes that it addresses a broader opportunity than is captured by IDC. Zoom’s management believes that users can greatly expand the use-cases of Zoom’s video communication tool throughout their organisation after they experience its benefits. We agree with Zoom’s leaders. In particular, the current COVID-19 pandemic, and the ensuing restriction on human movement to fight the spread of the disease, has demonstrated that video communication tools can have a wide range of use cases. In Zoom’s earnings conference call for the second quarter of FY2021, CEO Eric Yuan commented:

“My golly, if I talk about new usage, it probably can speak for four or five minutes. I’ll give you several. Like, you see the problem next, you can use Zoom for the virtual property tour. During the last 10 weeks, we have closed over 50% of the newly launched properties in Singapore over Zoom.

And also, the CSK, a corporate law firm in Florida, to have virtual trial by jury. And also, like Source Coast Community services, which is the, you know, largest and the mental health service provider in California also use Zoom to offer mental health. And mental health, it’s become a very big problem. A lot of new users like that.

So, every day, I feel very, very excited to see so many new use cases.”

In other examples, Zoom is now also being used for education, telemedicine, and fitness classes.

But even if we use just IDC’s estimate of Zoom’s 2022 market opportunity of US$43.1 billion, Zoom still only accounts for a fraction of that. Zoom’s revenue in the 12 months ended 31 July 2020 was US$1.35 billion; for the whole of FY2021, Zoom has projected revenue of around US$2.4 billion. We believe that Zoom is well-equipped to grab significantly more market share – by winning new customers and increasing revenue per customer – and at the same time, expand its market.

We also want to highlight the international expansion opportunity. Zoom’s international business is growing rapidly. Revenue from outside the Americas accounted for 31.6% of Zoom’s total revenue in the second quarter of FY2021, up from just 19% in FY2020.

2. A strong balance sheet with minimal or a reasonable amount of debt

As of 31 July 2020, Zoom had zero debt and US$1.48 billion in cash, cash equivalents, and short-term marketable securities. This is a rock-solid balance sheet. Zoom has operating lease liabilities, but these were just US$63.1 million.

In addition, Zoom has already been generating positive free cash flow for a number of years, unlike many other software-as-a-service companies. We’ll discuss Zoom’s cash flow in greater detail later.

3. A management team with integrity, capability, and an innovative mindset

On integrity

Eric Yuan, who is currently 50, founded Zoom in 2011 and has been leading the company as CEO since. We appreciate the fact that Yuan is still relatively young (in the business world) but already has nearly a decade of experience leading Zoom.

Zoom has opted not to share details about its compensation structure for its key leaders because of its status as an “emerging growth company.” But we still think that what we know about Zoom’s compensation structure demonstrates integrity. Here are a few data points:

- Yuan’s total compensation in FY2020 was only US$320,826 while that of CFO Kelly Steckelberg was just US$408,533.

- Chief Revenue Officer Ryan Azus’s total compensation was a princely sum of US$28.6 million, but 98% of this came from new-hire-related restricted stock units given by Zoom (Azus joined the company in August 2019). The restricted stock units vest over four years and on the condition that Azus remains an employee of Zoom.

- Yuan was granted stock option awards in September 2018 that vest over a four year period.

Notably, Yuan and Steckelberg controlled 45.53 million and 1.08 million Zoom shares, respectively, as of 31 March 2020. At Zoom’s 21 September 2020 share price of US$468, Steckelberg’s stake is worth US$508 million while Yuan’s is valued at a staggering US$21.3 billion. We think these large ownership stakes also help put Zoom’s management team in the same boat as the company’s other shareholders such as Compounder Fund.

One thing we want to highlight is that all of Eric Yuan’s Zoom shares are of the Class B variety. Zoom has two share classes: (1) Class B, which are not traded and hold 10 voting rights per share; and (2) Class A, which are publicly traded and hold just 1 vote per share. Yuan held 34.4% of Zoom’s voting power as of 31 March 2020, so he has significant control over the company. This concentration of Zoom’s voting power in the hands of Yuan means that we need to be comfortable with him at the company’s helm. We are.

On capability and ability to innovate

We rate Eric Yuan highly on this front, and there are a few things we want to discuss.

First, we think that Yuan has led Zoom to build a video conferencing platform that is loved by consumers due to its user-friendly interface and great user experience. We can testify to this as regular Zoom users. But more importantly, there’s also Zoom’s strong net promoter score (NPS). In 2018 and 2019, Zoom’s NPS was over 70 in both years. The NPS ranges from -100 to +100 and it measures the willingness of customers to recommend a company’s product or service to others and can be a gauge of customer loyalty and satisfaction. For perspective, the average NPS for software companies in the US is just 41, according to the Temkin Group.

Second, it’s perhaps no surprise to realise that Zoom’s products are well-loved if you read the company’s IPO prospectus. Yuan included a letter in the document that contained an unusual declaration of wanting to make the world a happier place. He wrote:

“Life is about the pursuit of happiness. The greatest, most sustainable happiness comes from making others happy. Delivering happiness is what we do at Zoom.

Ten years ago, I was an engineering leader at a major technology company. I would visit customers, and they would tell me how unhappy they were with the technology in the videoconferencing market. This made me unhappy. There had to be something better – something designed for modern video communications, something that would deliver happiness. I knew that we would have to start from scratch to do it right.

This experience underlies the Zoom happiness philosophy. Our focus is to keep both our customers and our employees happy. The sum of their joy is greater than its parts. Our customers and our employees make each other happy. We live this philosophy every day. We take care of our customers and employees. We built a video-first communications platform that is scalable, user friendly and reliable. We respond to our customers’ emails (quickly), talk with them face-to-face on Zoom, really listen to them and build the features and products they ask for (also quickly).

Happiness delivers results. In 2018, our average customer Net Promoter Score was over 70, demonstrating that our high-quality, easy-to-use platform is making customers happy. We have consistently earned high scores across customer review sites, including Gartner Peer Insights, TrustRadius and G2 Crowd. And let’s not forget our employees. Zoom has received multiple awards from Glassdoor based on high ratings and reviews from our employees.”

We think Yuan’s devotion to delivering happiness for Zoom’s customers is a simple but unreplicable competitive advantage for the company. It is a unique way of looking at the world, and one that we think is near-impossible to replicate by competitors, since it comes directly from Yuan’s mind. Yuan also places great emphasis on making his employees happy, which we love. We think happy employees lead to greater productivity, lower employee turnover, and the ability to attract talented individuals, which makes everyone happier – and off the flywheel goes. For perspective, here’s some data:

- Yuan received Glassdoor’s award as the number one CEO of a large company in 2018

- Zoom was ranked second in Glassdoor’s Best Places to Work in the large company category in 2019.

- Currently, 96% of Zoom-raters on Glassdoor will recommend the company to a friend. Meanwhile, Yuan has a 98% approval rating as CEO, far higher than the average Glassdoor CEO rating of 69%.

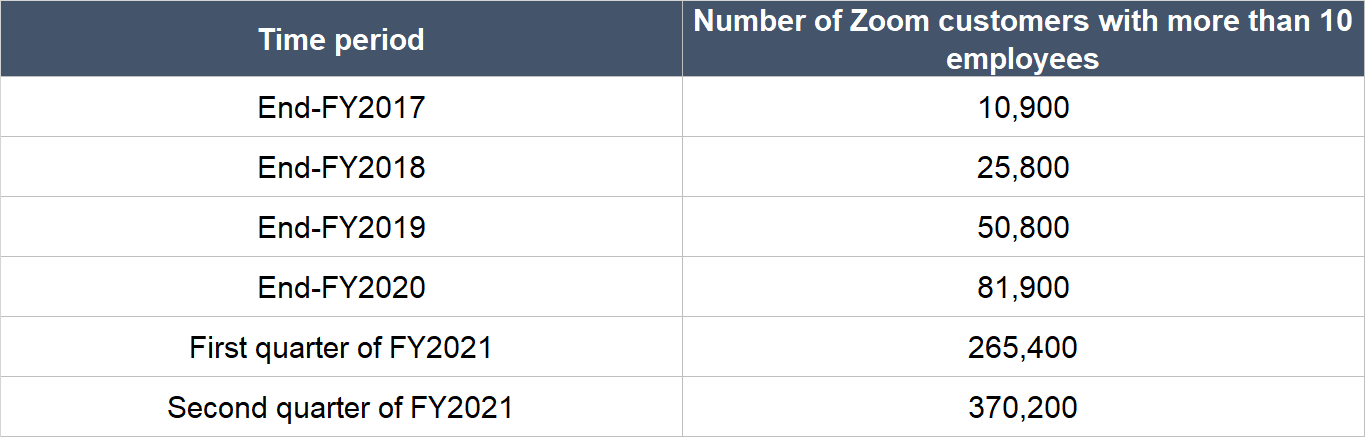

Third, Zoom has executed brilliantly with the land-and-expand strategy. The strategy starts with the company landing a customer with an initial use case, and then expanding its relationship with the customer through more users and/or more use cases. The success can be illustrated through (1) Zoom’s impressive growth in the number of customers with more than 10 employees, and (2) the strong net dollar expansion rates (NDERs), for customers with more than 10 employees, enjoyed by the company. The table below shows Zoom’s customer numbers over the past few years:

Source: Zoom IPO prospectus, FY2020 annual report, and Q1 & Q2 FY2021 earnings update

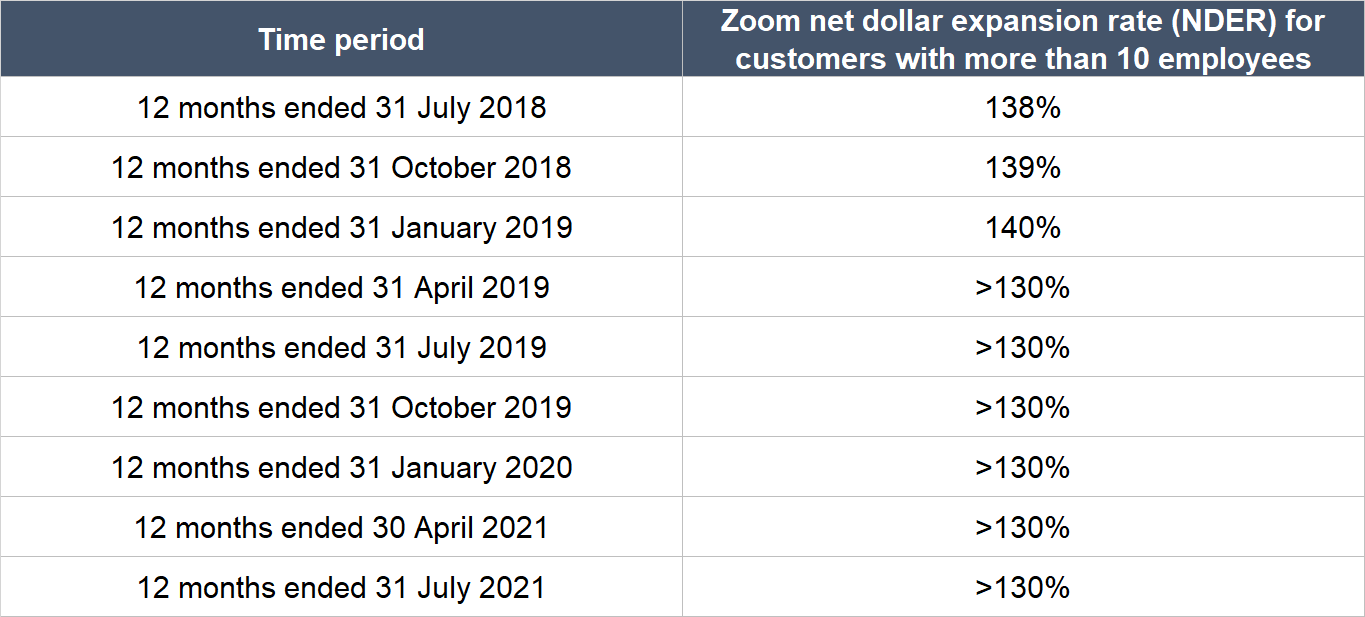

The NDER metric is a very important gauge of the health of a SaaS (software-as-a-service) company’s business. It effectively measures the change in revenue from the entire cohort of Zoom’s customers with more than 10 employees from a year ago compared to today; the NDER includes positive effects from upsells as well as negative effects from customers who leave or downgrade. Anything more than 100% indicates that Zoom’s customers with over 10 employees, as a group, are spending more. Impressively, Zoom’s trailing-12-months NDER has been more than 130% for nine consecutive quarters as of the second quarter of FY2021.

Source: Zoom IPO prospectus and quarterly earnings updates

We also want to shine a spotlight on Zoom’s excellent execution with its unique sales model. The company drives viral enthusiasm among a small group of users within an organisation (with the help of free-use of Zoom Meeting and an excellent overall “it just works” experience that users enjoy with the company’s products) that then leads to widespread adoption. In FY2019, Zoom had 344 customers that contributed more than US$100,000 in revenue and collectively, they accounted for 30% of Zoom’s revenue for the year. Of these 344 customers, 55% started their relationship with Zoom with at least one free user prior to subscribing.

Fourth, Yuan had the foresight to build a video-first, cloud-native video conferencing platform for Zoom, unlike competing tools which tacked on video capabilities to aging, pre-existing conference call or chat tools. As mentioned earlier, the idea for Zoom came when Yuan grew frustrated with his experience of interacting with unhappy customers while working at a “major technology company.” This company is Cisco, and the videoconferencing product Yuan worked on was Webex. We are attracted to companies that are built because their founders saw a big problem that needed fixing – to us, it’s a sign of entrepreneurial drive and innovation in the companies’ leaders. And Yuan embodies this. He cared deeply about his customers’ experience (this is also related to the second point we discussed earlier about Yuan’s devotion to customer happiness) and wanted to build a better solution.

Fifth, Zoom has performed admirably during the current COVID-19 pandemic. Here’re some highlights:

- In the first half of 2020, the number of daily meeting participants on Zoom peaked at over 300 million in April, up from 10 million in December 2019. Being able to meet this incredible spike in demand was a huge achievement for Zoom.

- In the first quarter of 2020, with the best of intentions, Zoom opened its platform to over 100,000 K-12 schools in 25 countries and millions of people around the world. But Zoom failed to fully consider the security and privacy implications, especially for users who lack the relevant technical support in such areas. There was a lot of bad press as a result. Zoom quickly launched a transparent 90-day initiative to improve the security and privacy features of its products and the project was completed recently. Yuan has learnt from the experience and security and privacy will continue to be an important focus for Zoom in the future.

- Zoom provided a one-time bonus (equivalent to two-weeks’ pay) in the height of the COVID-19 crisis for all non-commissioned employees to offset costs associated with any disruption to life caused by the pandemic.

- The company’s not pulling back on investments for growth. In May 2020, Zoom announced that it will be setting up two research & development-focused engineering centres in the USA (one in Greater Phoenix, Arizona, and the other in Pittsburgh, Pennsylvania). The two centres will hire a total of 500 software engineers in the next few years. Zoom’s also expanding its hiring plans for the rest of 2020 to meet the new opportunities it’s seeing in the current environment. For perspective, Zoom ended the second quarter of FY2021 with over 3,400 employees, up more than 30% from 2,532 at the end of FY2020.

Sixth, Zoom is not resting on its laurels and regularly releases new products. In July, the company introduced the Zoom for Home hardware product, as already mentioned. In the same month, Zoom also launched Zoom HaaS (Hardware as a Service), which could help increase adoption of the Zoom Room and Zoom Phone products by lowering friction around hardware purchases; through Zoom HaaS, customers can subscribe for phone and meeting room hardware. In a video interview with Stanford Business School earlier this year (conducted through Zoom, of course!), Eric Yuan also mentioned that his team is working on new projects for Zoom that include real-time language translation and features powered by artificial intelligence sensors. Ultimately, Yuan’s goal is to make video communication even better than face-to-face meetings. To get there, plenty of innovation on Zoom’s part will be needed.

4. Revenue streams that are recurring in nature, either through contracts or customer-behaviour

Zoom’s revenue comes from subscriptions to its video conferencing software products, which are recurring in nature. Of course, just having a subscription business is not enough if subscribers do not renew. But in the case of Zoom, it’s clear that subscribers love to renew and even spend more: Earlier, we shared Zoom’s impressive net dollar expansion rates for customers with more than 10 employees.

5. A proven ability to grow

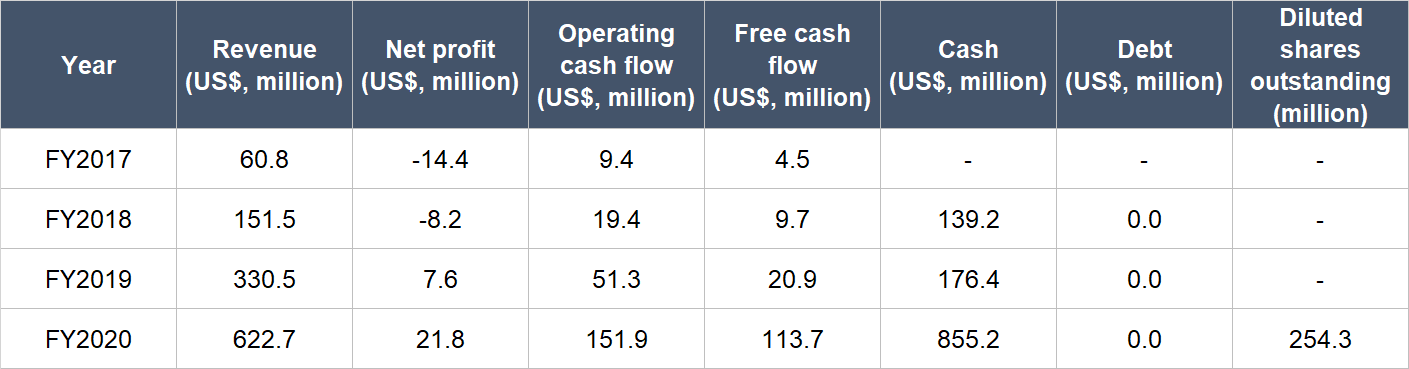

Zoom has a short history as a public-listed company (its IPO was only in April 2019) so we don’t have much financial data to study for the company. But we like what we see. The table below shows the key financial figures for Zoom that we can obtain:

Source: Zoom IPO prospectus and FY2020 annual report

A few key things to highlight from Zoom’s financials:

- Zoom’s revenue has compounded at an incredible annual rate of 117.1% from FY2017 to FY2020. FY2020’s growth rate was slower, but was no slouch at all at 88.4%.

- The company started generating a profit in FY2019.

- Zoom’s operating cash flow and free cash flow were not only positive in every year from FY2017 to FY2020, but they also both grew rapidly. Moreover, the free cash flow margin (free cash flow as a percentage of revenue) in FY2020 was decent at 18.3%.

- Zoom raised US$448 million from its April 2019 IPO and a further US$100 million in a concurrent private placement. Both actions helped strengthen the company’s balance sheet. But even before the IPO, Zoom was already in a strong financial position with millions in cash and zero debt.

- The date of Zoom’s IPO was in the first quarter of FY2020. So there’s no prior useful data on the company’s share count that can tell us if Zoom has been diluting shareholders.

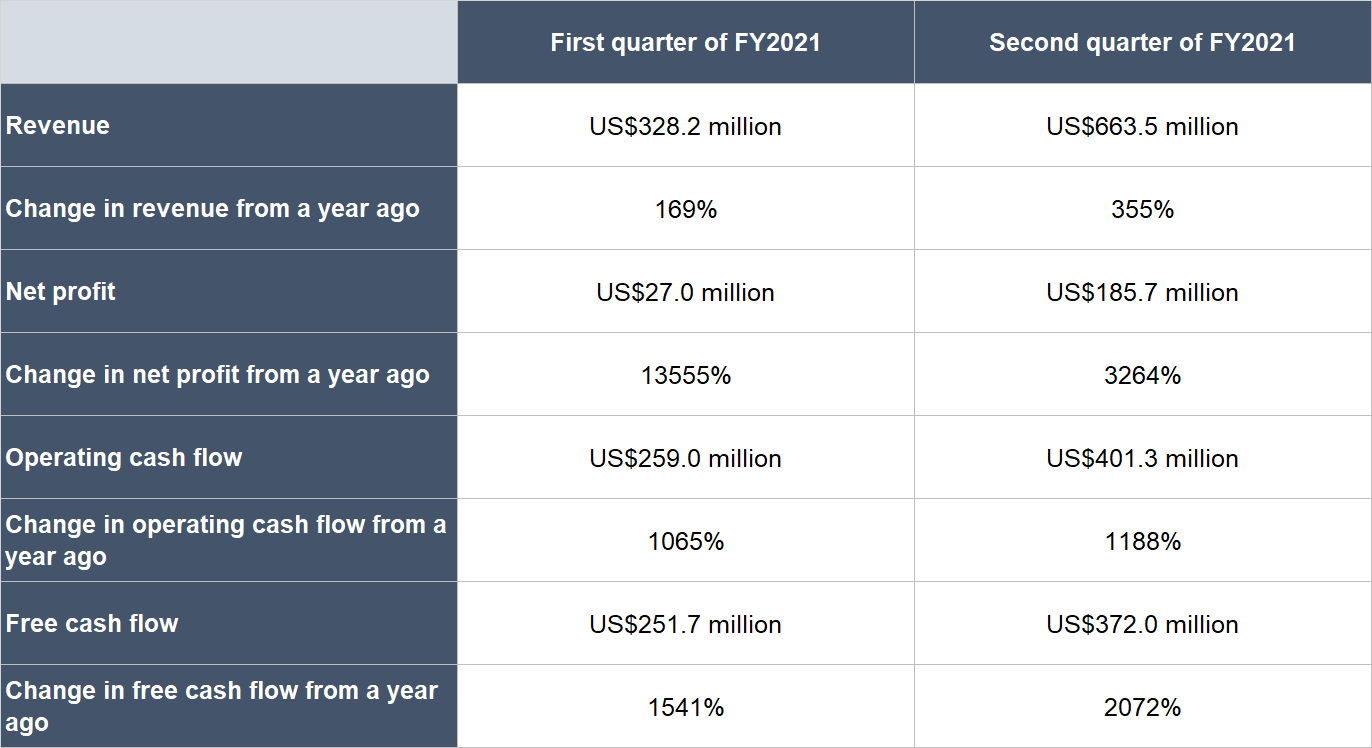

COVID-19 has been a massive tailwind for Zoom. The pandemic even helped Zoom to become a verb – people now tend to say “I’ll Zoom you” instead of “let’s chat on Zoom”. This has led Zoom to produce stunning growth in the first half of FY2021 as shown in the table below. In fact, Zoom’s performance in the second quarter of FY2021 is one of the best quarters we’ve ever seen for a public-listed software company.

Source: Zoom earnings updates

A few other things we want to point out for Zoom’s results in the first half of FY2021:

- Zoom’s net profit margin for the period is a robust 21.5%.

- The free cash flow margin is a jaw-dropping 62.9%, but we expect this margin to fall as the year progresses.

- In the second quarter of FY2021, Zoom’s remaining performance obligation (RPO) surged by 209% from a year ago to US$1.42 billion. The RPO metric consists of unrecognised revenue that the company expects to recognise in future periods. The big jump in the RPO sets Zoom up well for future quarters.

- Zoom ended the second quarter of FY2021 with 370,200 customers with more than 10 employees, up 458% from a year ago.

- Dilution was acceptable in the context of the company’s growth, as Zoom’s diluted share count at the end of FY2021 was 296.4 million, up ‘just’ 16.5% from end-FY2020.

6. A high likelihood of generating a strong and growing stream of free cash flow in the future

We think Zoom scores highly in this criterion for two reasons.

First, we see Zoom as having a high chance of being able to grow its revenue significantly in the years ahead. Its products are well-loved by users, and it has excellent net dollar expansion rates plus a top-notch track record of winning new customers.

Second, as Zoom grows and attains economies of scale, it could result in high free cash flow margins in the future. Zoom is currently in rapid-growth mode and is investing to grow its business. Yet it still managed to achieve an incredible free cash flow margin of 62.9% in the first half of FY2021. We don’t think this high free cash flow margin of 62.9% is sustainable. But we think that Zoom could easily achieve a steady-state free cash flow margin of around 40% given its current performance and the traditionally asset-light nature of software businesses.

Valuation

We completed our purchases of Zoom shares with Compounder Fund’s initial capital in late July 2020. Our average purchase price was US$258 per Zoom share. At our average price and on the day we completed our purchases, Zoom shares had trailing price-to-sales (P/S) and price-to-free cash flow (P/FCF) ratios of around 92 and 217, respectively. We like to keep things simple in the valuation process. In Zoom’s case, we think the P/S and P/FCF ratios are appropriate metrics to value the company. This is because the company’s business has begun to gush out free cash flow, but the picture could change in the near future since Zoom is still in high-growth mode.

Optically, the valuations at our points of investment seem really high. But we still want to be a part owner of this exceptional business – as we discussed earlier, Zoom is stellar when we comb through it with our investment framework. We believe that Zoom can see very high double-digit annual revenue growth rates – in turn leading to similarly strong free cash flow growth – for years into the future. In fact, in its FY2021 second-quarter earnings update, Zoom guided for revenue of between US$2.37 billion and US$2.39 billion for the whole of FY2021, representing revenue growth of more than 280% at the low-end. Zoom also has one of the best metrics among SaaS companies, in terms of revenue growth, the net dollar expansion rate, and increase in customer numbers. All of these make us comfortable paying a large premium when investing in Zoom’s shares.

For perspective, Zoom carried P/S and P/FCF ratios of 103 and 197, respectively, at the 21 September 2020 share price of US$468.

The risks involved

We’ve identified a few big threats to our investment thesis with Zoom.

One is competition. Zoom competes with many different video conferencing products, some of which are from technology giants. These products include Microsoft Teams, Facebook Messenger Rooms, Google Hangouts, and also Cisco Webex, among others. (Compounder Fund also owns shares in Microsoft, Facebook, and the parent of Google, Alphabet.)

But we think Zoom’s products stand out from the competition. They are really easy to use, and this causes users to love Zoom (as said earlier, the company has a really high net promoter score of 70). We think it’s really difficult for a competitor to unseat Zoom. The ease-of-use found in Zoom’s products come from Eric Yuan’s devotion to making his customers and employees happy, and this cannot be easily replicated, as we mentioned earlier.

Moreover, there’s a viral dynamic to Zooom’s products – the more users the products have, the greater and faster their adoption. This is because when users want to do video calls with friends or associates, they will need to invite first-time users onto the Zoom platform. These first-timers will then get introduced to the Zoom platform and if they enjoy the experience (and they likely will) they could become hosts for Zoom meetings themselves in the future and then introduce Zoom to others.

Another risk we’re watching is Zoom’s short history in the stock market, given that its IPO was just one-and-a-half years ago in April 2019. But we are willing to back Zoom because we think its business holds promise for fast-growth for a long period of time

We also cannot ignore Zoom’s high valuation. Any hiccups in Zoom’s growth will very likely cause a significant compression in the company’s valuation multiple and result in a steep decline in its share price.

There is key-man risk too. We see Eric Yuan as the key architect for Zoom’s current success. His focus on customer satisfaction, building a scalable and user-friendly service, and keeping employees happy, has been the cornerstone of Zoom’s rise. The company’s growth could be derailed if it loses Yuan’s leadership. The good thing is that Yuan is young in the business world at just 50 years old. And based on recent media appearances, he has tremendous energy and enthusiasm to continue leading the company.

The location of Zoom’s workforce is another source of risk. At the end of FY2020, Zoom had over 700 research & development employees that are based in China. There’s currently a tense relationship between China and the USA (in particular, the two countries are tussling over technology and data security) and the presence of a large R&D team in China is a risk to Zoom’s business. In its FY2020 annual report, Zoom commented that it has “a high concentration of research and development personnel in China, which could expose [the company] to market scrutiny regarding the integrity of our solution or data security features.”

Lastly, there’s a chance that a significant portion of Zoom’s growth in FY2021 thus far is attributable to a transient increase in demand because of shelter-in-place measures across the world to combat COVID-19. But our belief is that COVID-19 is a catalyst for greater and lasting adoption of video communication tools at work, in schools, at home, and more – we see the trend persisting well after the pandemic fades. For instance, some companies are exploring having their employees work completely from home permanently even after the world finds a solution to COVID-19, or have a workforce that’s distributed between the office and home. More importantly, COVID-19 has forced the large-scale adoption of video communication tools by society. We think it’s reasonable that for many use-cases, people will find video conferencing to be a better solution than what was done previously. But only time will tell.

Summary and allocation commentary

Summing up Zoom, it has:

- A widely-loved video conferencing software product

- A large market opportunity that is poised for growth as new use-cases for video conferencing develop over time

- A rock-solid balance sheet with no debt

- An incredible leader in Eric Yuan who has a fanatical focus on delivering happiness for both customers and employees, and who has significant skin in the game

- Sensible compensation for management

- A subscription business that is highly recurring in nature

- An exceptional track record of growth

- A high likelihood of being able to produce strong free cash flow in the future.

Zoom does have a premium valuation, so we’re taking on valuation risk. There are also other risks to note, such as Zoom’s short listing history; the presence of big-tech competitors; key-man risk; a high concentration of R&D employees in China; and the danger of Zoom’s current growth potentially being the result of a temporary increase in demand.

After weighing the pros and cons, we initiated a 1.0% position – a small allocation – in Zoom with Compounder Fund’s initial portfolio. We think Zoom is an exceptional business and we do want a piece of the action. But our enthusiasm is somewhat tempered by the company’s high valuation.

And here’s an important disclaimer: None of the information or analysis presented is intended to form the basis for any offer or recommendation; they are merely our thoughts that we want to share.