Compounder Fund: Upstart Investment Thesis - 23 Aug 2021

Data as of 20 August 2021

Upstart (NASDAQ: UPST), which is based and listed in the USA, is a company in Compounder Fund’s portfolio that we invested in for the first time in August 2021. This article describes our investment thesis for the company.

Company description

Upstart was founded in 2012 by its co-founders – Dave Girouard, Anna Counselman, and Paul Gu – because they wanted to use technology to improve society’s access to affordable credit. Today, Upstart offers a cloud-based lending software platform to banks. To be clear, Upstart is not a bank. What it does is to provide its platform to banks.

There are currently 25 banks using Upstart’s platform and the company calls such banks its bank partners. Upstart aggregates consumer demand for loans and connects consumers to its bank partners that then originates the loans. Upstart’s lending software platform is provided to banks via the cloud. It handles all user interactions, such as rate inquiries, loan offer presentations, identity verification, loan servicing, and more. The platform is powered by Upstart’s proprietary artificial intelligence (AI) models that support fraud detection and borrower verification. Most importantly, these AI models also assess the risk of a loan and help banks better price loans and offer loans to more people. Upstart’s lending software platform is designed for seamless integration into a bank’s existing technology systems. It is also configurable, with each bank partner able to control its own credit policy and lending-parameters on Upstart’s platform.

Historically, Upstart has focused on the unsecured personal loan market and only entered the auto loans market in June 2020. In the 12 months ended 30 June 2021, Upstart’s bank partners originated 660,899 Upstart-powered loans with a total loan value of US$6.68 billion. The vast majority of these loans are unsecured personal loans. The unsecured personal loans that flow through Upstart’s platform typically have three to seven-year terms and range from US$1,000 to US$50,000, with annual percentage rates (APRs) of 6.5% to 35.99%. These loans also typically come with a monthly repayment schedule and do not have a prepayment penalty.

Consumers can discover Upstart-powered loans through Upstart’s website (Upstart.com) either directly or via loan-aggregator websites. Credit Karma is an important loan-aggregator website for Upstart. Traffic from there accounted for 49% and 52% of Upstart’s total loan originations, respectively, for the first half of 2021 and the whole of 2020. Consumers can also discover Upstart-powered loans through the websites of Upstart’s bank partners. But the lion’s share of borrowers today are still referred to Upstart’s bank partners via Upstart.com. One particularly important bank partner of Upstart is Cross River Bank. The innovative community bank, which is based in New Jersey, USA, originated 60% of Upstart’s loans in the first half of 2021. The self-same percentage for the whole of 2020 was 67%.

An Upstart-powered loan can either be retained by the bank partner that originated the loan or be purchased by Upstart, which then (1) immediately resells the loan to institutional investors, (2) holds the loan for a period of time before selling it to institutional investors, or (3) retains it. When Upstart was listed in the US stock market in December 2020, there were around 100 institutional investors in its network. This has since expanded to more than 150 today. In 2020, 21% of Upstart-powered loans were retained by the originating bank, while 77% and 2% of the loans were distributed to institutional investors and held by Upstart, respectively. No numbers are given, but Upstart has revealed that its bank partners have, over the past few years, generally increased the percentage of Upstart-powered loans that they retain (the percentage does fluctuate from quarter to quarter). This is a healthy dynamic for Upstart. The company explained in its 2020 annual report:

“In general, banks can fund loans at lower rates due to the lower cost of funds available to them from their deposit base than is otherwise available in the broader institutional investment markets. Accordingly, loans retained by the originating bank generally carry lower interest rates for borrowers, which leads to better conversion rates and faster growth for our platform.”

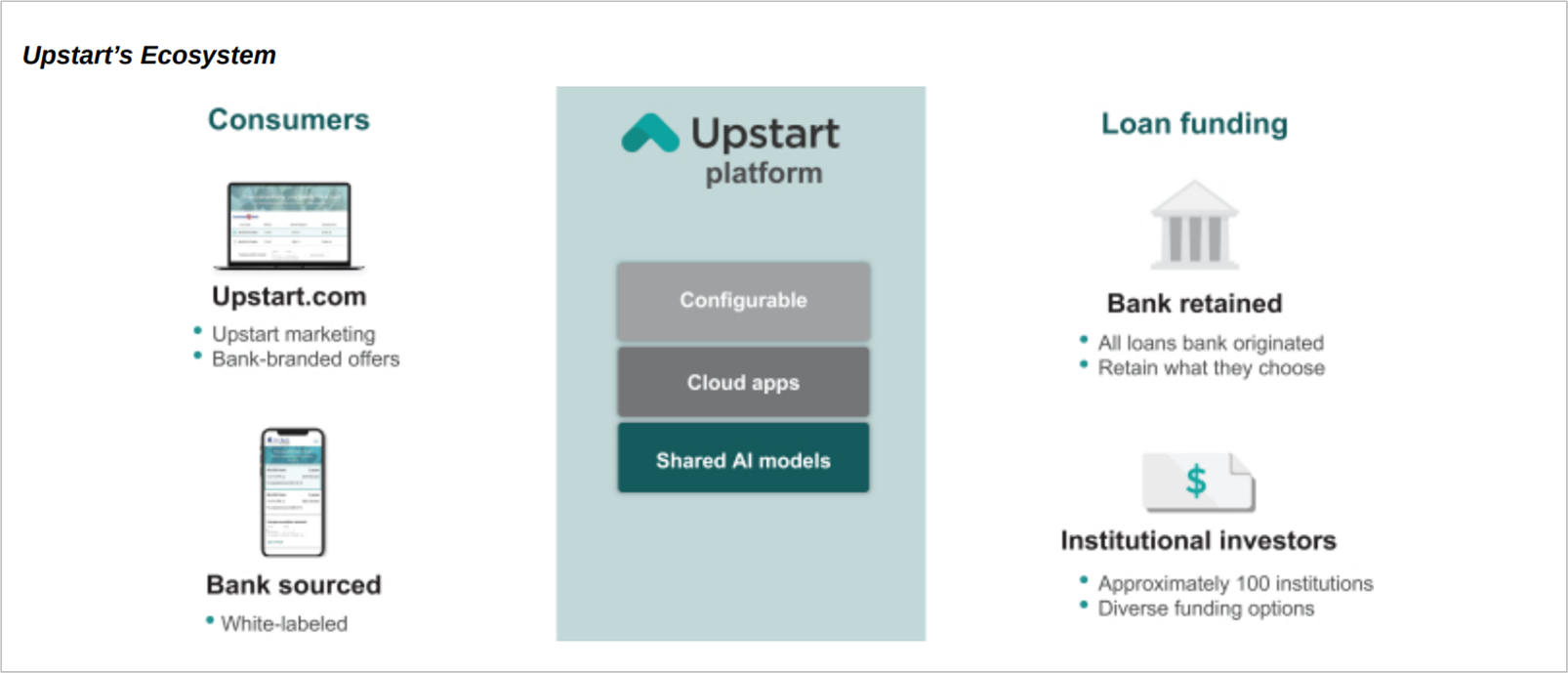

The chart below, taken from Upstart’s IPO prospectus published in December 2020, shows the entire Upstart ecosystem and how the company interacts with consumers, banks, and institutional investors.

Source: Upstart IPO prospectus

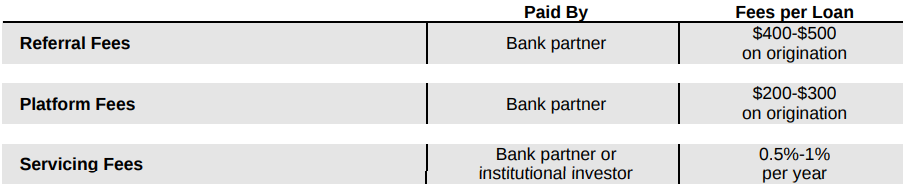

Upstart’s revenue comes from a few sources:

- Upstart charges its bank partners a referral fee each time it refers a borrower who obtains a loan

- Bank partners pay Upstart a platform fee each time they originate a loan with Upstart’s platform

- An annual servicing fee is charged to the holder of Upstart-powered loans (the holders can be either the originating bank partners or institutional investors)

- Interest income and securitisation activities

The first three sources of revenue are known as fee revenue and they are either dollar or percentage-based. The table below shows the fees earned by Upstart from an average-sized loan based on the company’s rates as of 30 September 2020:

Source: Upstart IPO prospectus

The following table illustrates the revenue earned by Upstart from each source for the 12 months ended 30 June 2021. It’s clear that Upstart’s fee revenue makes up the overwhelming majority of the company’s business.

Source: Upstart regulatory filings

For a geographical perspective, we believe that Upstart currently only does business in the USA.

Investment thesis

We have laid out our investment framework in Compounder Fund’s website. We will use the framework to describe our investment thesis for Upstart.

1. Revenues that are small in relation to a large and/or growing market, or revenues that are large in a fast-growing market

Earlier in the “Company description” section of this article, we mentioned that (1) Upstart has 25 bank partners currently, (2) these banks originated US$6.68 billion worth of loans in the 12 months ended 30 June 2021, and (3) an overwhelming share of these loans are unsecured personal loans. Meanwhile, the USA had around 5,200 deposit-taking financial institutions in 2019, and the country’s personal loan and auto loan markets currently have annual loan volumes of around US$84 billion and US$635 billion, respectively. Moreover, the total annual US consumer credit volume is around US$4.2 trillion.

All the numbers mentioned in the paragraph just above show clearly that Upstart has tremendous room for growth in the USA to win more bank partners and power more loan originations with its AI-driven lending platform. Crucially, we also think that Upstart is in a great position to expand its market share in the years ahead. There are a few reasons why.

First, Upstart’s AI-powered lending platform has clear advantages over the traditional lending process which uses antiquated methods to assess risk. The FICO score, which has been largely unchanged since its invention more than 30 years ago in 1989, is used by more than 90% of lenders in the USA for loan approval and to determine the interest rates for loans. Although the FICO score is seldom the sole input, bank credit models are still simple, commonly containing only eight to 15 variables. Even the more sophisticated models incorporate up to just 30 variables. As a result, credit risk is often assessed poorly and individuals suffer. Upstart explained this in its IPO prospectus (emphasis is ours):

“Unfortunately, because legacy credit systems fail to properly identify and quantify risk, millions of creditworthy individuals are left out of the system, and millions more pay too much to borrow money…

…Many borrowers suffer from the effects of inaccurate credit models. Many are approved for a loan that they ultimately will be unable to repay, negatively impacting both the consumer and the lender. Many others may be declined for a loan that they could have successfully repaid if given the opportunity – again doing harm to both consumer and lender. According to an Upstart retrospective study completed in December 2019, four out of five Americans who have taken out a loan have never defaulted, yet less than half of Americans have access to prime credit. Even consumers with high credit scores tend to pay too much for loans because the rates they pay effectively subsidize the losses from borrowers who default.”

Upstart’s AI lending models help improve all these problems. The company’s models incorporate more than 1,000 variables over 10 million repayment events that together account for 15 billion or more cells of data. This stands in stark contrast to the simplistic models that banks typically use. More importantly, the higher sophistication leads to better outcomes. A study by Upstart conducted a few years ago – which was also reported by the Consumer Financial Protection Bureau (CFPB), a regulatory body for financial products in the USA – found that the company’s platform approved 27% more borrowers than high-quality traditional lending models and these approved-loans also come with a 16% lower APR (annual percentage rate).

Second, the AI models that power Upstart’s cloud-based lending software platform are constantly getting better. In fact, the company has been improving its models for eight years and counting. Examples of the rapid progress that Upstart has made with its AI models from 2014 to 2020 are shown in the chart below (increase the “zoom” on your browser window for a better view).

Source: Upstart 2020 annual report

The improvements in Upstart’s AI models have led to tangible benefits for its business over the past few years and these can be seen in the following table. It shows the impressive growth in (1) Upstart-powered loans from 2017 to the first half of 2021, (2) the percentage of Upstart-powered loans that are fully automated, and (3) Upstart’s conversion rate. The conversion rate for any particular time frame is defined as the number of loans transacted (in other words, the number of Upstart-powered loans originated by the company’s bank partners) divided by the number of rate inquiries received. We think the conversion rate is an important metric for Upstart because it’s a proxy for the level of access to credit that Upstart can bring to consumers as a result of improvements to its AI models. The growth in the percentage of fully automated loans is even more impressive given that fraud rates in Upstart-powered loans have been kept really low (around 0.4% or less since the first quarter of 2017).

![]()

Source: Upstart IPO prospectus, annual report, and quarterly earnings update

One other important trait about Upstart’s AI models is that they are able to learn from each new loan that the company’s platform facilitates.

Third, only a small handful of the 5,200 financial institutions that are currently in the USA have the necessary financial and technological resources to successfully build their own AI-lending models. This makes Upstart an important partner for smaller financial institutions in the USA. Upstart explained in its IPO prospectus:

“The largest four U.S. banks spend an estimated [US]$38 billion on technology and innovation annually. These four banks may attempt to build AI lending models over time, once general market acceptance has been achieved. However, outside the largest four banks, there are approximately 5,200 FDIC insured institutions that are at risk of falling behind. Despite holding over [US]$8 trillion in deposits, we believe these banks, particularly small to medium-sized banks, have outdated technology and lack the technical resources of larger banks to fund the digitization process.”

Fourth, Upstart’s AI-powered lending platform provides a great experience for two of its key constituents: Consumers and banks. For consumers, they get to enjoy better access to credit and lower interest rates. As we mentioned earlier, a study by Upstart found that the company’s platform approved 27% more borrowers than high-quality traditional lending models and these approved-loans also come with a 16% lower APR. There’s more. Upstart provides a great digital experience too. When a consumer applies for an Upstart-powered loan (either from Upstart.com or from the websites of Upstart’s bank partners), there’s only one single streamlined application process and a firm loan offer is provided. Moreover, around 70% of Upstart-powered loans in 2020 – up from 0% in late 2016 (this is another example of improvements Upstart has made to its AI models) – were instantly approved with no document upload or phone call required. It’s also worth noting that more than half of the Upstart-powered loans that were distributed in 2020 were from applications made through mobile devices. In an increasingly mobile-driven world, having a mobile-friendly experience is important for a company’s growth – and we think it’s clear that consumers enjoy Upstart’s mobile experience. For banks, Upstart provides a number of important benefits:

- As mentioned earlier, Upstart provides smaller banks and other types of lending institutions with a cost-effective way to compete technologically with banks that have much larger financial firepower. The AI models that Upstart provides to banks are also delivered in the form of a simple cloud application, which makes it easy to use.

- Consumers looking for loans that end up at Upstart.com are being referred to the company’s bank partners. These banks therefore enjoy higher loan volume and customer flow.

- Using data from late 2017, Upstart compared its credit models with those of several large US banks and found that its models could lower these banks’ loss rates by nearly 75% while keeping approval rates constant.

- Upstart also helps banks produce a great consumer experience. The company mentioned in its December 2020 IPO prospectus that the lending programs of its bank partners have Net Promoter Scores (NPS-es) of 79, much higher than the benchmark scores for the largest US banks. The NPS ranges from -100 to +100 and it measures the willingness of customers to recommend a company’s product or service to others and can be a gauge of customer loyalty and satisfaction.

Fifth, Upstart has a significant head start in AI-powered lending. As we mentioned earlier, Upstart has been training its AI-models for lending for eight years and counting. What’s fascinating is that even today, not many companies are competing with Upstart. In a wonderful May 2021 interview, Upstart’s co-founder Paul Gu, who currently heads the product and data science teams at the company, said:

“The biggest surprise has been – I expected there to be a lot more people trying to build what we’re building. It just seemed to me like such an incredible opportunity to create value for lenders and such an incredible opportunity to create value for consumers. It’s almost like banging-your-head-on-the-table-obvious that this is probably the best application for AI that you could have, period. Just in terms of the combination of all the kinds of pieces are there: The high volumes of data, the high economic opportunity, the real-time decision making, and at the same time, there’s this enormous, enormous, enormous, market. One of the oldest industries, most profitable industries, the source of almost all the profits in the consumer financial system.

And yet here we are, 10 years almost since I dropped out of college [to co-found Upstart] – actually it has been more than 10 years. And almost we see so little, so little, happening in this direction outside of what we’re building at Upstart. I’ve just been surprised by I think the level of inertia and maybe some of the kind of institutional barriers to innovating in this direction. But we hope that’s starting to change now with some of the success we’ve had.”

This head start and seeming lack of current competition is important. Earlier, we talked about how Upstart’s AI models learn with each new loan that the company facilitates. We think this creates a positive flywheel: Upstart’s AI models get better with each new Upstart-powered loan, leading to more demand for Upstart-powered loans from consumers and bank partners, resulting in even better AI models for the company. The end result is that it is going to become harder and harder for any competitor to catch up with Upstart over time. Upstart explained the challenges involved with creating AI credit models in its 2020 annual report:

“Our AI models are central to our value proposition and unique position in the industry. Our models incorporate more than 1,000 variables, which are analogous to the columns in a spreadsheet. They have been trained by more than 10.5 million repayment events, analogous to rows of data in a spreadsheet.

These elements of our model are co-dependent; the use of hundreds or thousands of variables is impractical without sophisticated machine learning algorithms to tease out the interactions between them. And sophisticated machine learning depends on large volumes of training data. Over time, we have been able to deploy and blend more sophisticated modeling techniques, leading to a more accurate system. This co-dependency presents a challenge to others who may aim to short-circuit the development of a competitive model. While incumbent lenders may have vast quantities of historical repayment data, their training data lacks the hundreds of columns, or variables, that power our model.”

In September 2017, Upstart became the first company to receive a no-action letter from the CFPB. We think this is another good example of the quality of Upstart’s AI-powered lending software platform. The purpose of the no-action letter is to reduce potential regulatory uncertainty – in relation to the Equal Credit Opportunity Act (ECOA) – for companies that are offering innovative consumer-finance products that can benefit consumers. The ECOA prohibits discrimination on the basis of race, color, religion, national origin, gender, and more, for consumers who are seeking credit. Upstart’s first no-action letter expired in November 2020 and the CFPB then issued a new letter which will expire in November 2023. When Upstart’s 2020 annual report was published in March this year, there were no other lending platforms that had received a similar no-action letter from the CFPB.

2. A strong balance sheet with minimal or a reasonable amount of debt

As of 30 June 2021, Upstart has US$506.3 million in cash on its balance sheet while having just US$6.1 million in total debt. This is a robust balance sheet, in our view.

It also helps that Upstart has already been generating free cash flow for a few years. This is something we’ll discuss in greater detail in the “A proven ability to grow” sub-section of this article.

3. A management team with integrity, capability, and an innovative mindset

We mentioned earlier that Upstart’s co-founders are Dave Girouard, Anna Counselman, and Paul Gu and that Gu is currently still an important leader at the company (he leads Upstart’s product and data science teams – he is in essence, Upstart’s AI whiz). The same goes for Girouard and Counselman. Girouard has been Upstart’s CEO since its founding while Counselman is currently in charge of managing Upstart’s operations and human capital. Meanwhile, Upstart’s chief financial officer, Sanjay Datta, joined the company as CFO nearly five years ago in December 2016. We appreciate the fact that despite their relatively young ages – Girouard is 55, Datta is 47, Counselman is 40, and Gu is just 30 – all the aforementioned members of Upstart’s management team each have years of experience leading the company.

On integrity

When Upstart released its latest regulatory filing in April this year that discussed the compensation structure for its management team, the company was still classified as an “emerging growth company.” As a result, the company was not required to share details on how its leaders were compensated. What we do know is that Girouard, Gu, and Datta were the company’s three highest-paid executives in 2020. Girouard’s total compensation was US$8.76 million, consisting mostly of option awards (92%). Gu and Datta’s compensation were US$1.84 million and US$1.85 million, respectively, and they were also mostly in the form of option awards (61% and 60%). These sums, while high, do not seem egregious to us.

Another positive point on the integrity of Upstart’s leadership team is the skin in the game that Girouard, Gu, and Datta have. The table below shows the number of Upstart shares they control as of 15 March 2021 (this includes options that were exercisable within 60 days of the date) and the monetary values of these shares based on Upstart’s 20 August 2021 share price of US$194. With stakes in Upstart that are worth hundreds of millions to a few billion dollars, we think that the interests of Upstart’s leaders are well aligned with those of the company’s other shareholders.

Source: Upstart 2020 proxy filing

On capability and innovation

We have a tonne of respect for Upstart’s management team – in particular Dave Girouard and Paul Gu – when it comes to capability and innovation. In the “Revenues that are small in relation to a large and/or growing market, or revenues that are large in a fast-growing market” sub-section of this article, we discussed a number of things. They include the advantages that Upstart’s AI models have over traditional credit models, the constant improvement in Upstart’s AI models, the great user experience that Upstart provides to both consumers and banks, and the head start that Upstart has in the AI-powered lending space. These did not spontaneously happen – they occurred because of the great work of Upstart’s leaders.

There are a few other positive things about Upstart’s management team that we want to discuss. First, we want to dig a little deeper into the quote from Paul Gu’s May 2021 interview that we shared earlier. He said that it was blindingly obvious to him and his Upstart co-founders that AI could deliver a massive positive impact in the lending market and thus result in the creation of a great business. But he was surprised that very few others saw the same thing. Dave Girouard also shared something similar in an interview – conducted soon after Upstart’s IPO in December 2020 – with venture capital firm First Round, which was an early investor in Upstart:

“When it comes to lending, I think the whole world sort of came to the conclusion that it’s kind of a commodity — anybody can lend if you have money and some basic analytics. And if you do it well, you’ll make some profits, and if you don’t, you probably won’t. But for whatever reason, people didn’t seem to believe that you could apply modern cloud computing and data science to create a dramatically better product.

People would say, ‘Yeah, is your lending model really going to be any better?’ It’s almost like everything they’ve learned about computer science and the potential of the software, they threw out the window when they looked at a lending-related business and said, ‘Nah, that’s just a human instinct business. All the software and data in the world won’t make a difference.’ I feel like that’s the way some in the industry to this day still think about it…

…To be honest, we went through times when either for the press or VCs, it wasn’t worth talking to Upstart because the winners had already won. And then when the world figured out the winners hadn’t won, it still wasn’t really worth talking to Upstart because the industry kind of looked like a disaster, frankly. And we just didn’t seem to be able to convince most of the world that it really was something very different. And I think we felt that way for years.”

From our vantage point, Gu and Girouard’s comments show that Upstart’s management team has a unique view about the world. Having a unique worldview is a trait we prize when we study a company’s leaders because we believe it’s not something that can be easily replicated by others. And this gives such a company a significant competitive advantage.

The second thing we want to talk about comes from the same May 2021 interview that Gu did. It relates to why Upstart’s co-founders chose to start with unsecured personal loans instead of other types of consumer loans such as mortgages or auto loans. We thought it demonstrates the clear and impressive thought process that Upstart’s management team had when choosing the first type of consumer loan product for the company to tackle. Gu said (emphasis is ours):

“The first is, if you want to demonstrate the efficacy of machine learning applied to something that’s been done for a very long time by many many companies, many banks, you want to apply it in a place where it’s going to matter the most, and be the hardest. And that’s in unsecured personal loans. If you think about every other asset class – car loans, home loans – they’re backed by something. Even credit cards are backed by the further utility of being able to continue to use your credit card in the future. When you give someone $20,000 and say “please pay me back,” you’re really backed by nothing. What that means is you really have to be very good at making a decision about who you’re going to lend to and who you’re not going to lend to, or else you will very soon be out of business. And that meant that if we could do a better job underwriting the risk here using AI, we would be able to generate incredible economic gains for both the lender and the consumer. So that’s what we were able to do.

The second reason is that from the consumer’s perspective, the unsecured personal loan, by its very nature, is the most flexible kind of loan. It can be used for any purpose. It’s not something that you can only get at specific moments in your life when you’re buying a car or a house. It’s something that you really can get at any time for any reason. And in that sense, it sort of forms the broadest product and is the most natural starting place.

And we always felt that if we did those first and second things, it would be much easier to go from personal loans to other types of loan products – which we’re now doing – than the other way around where you start with something really safe and really limited. It would be very hard to get out of that box and go to other spaces.”

Third, we find Girouard to be a thoughtful CEO who seems to have built a great corporate culture at Upstart. Glassdoor is a website that allows a company’s employees to rate it anonymously. Upstart currently has a 4.1-star rating out of 5 at Glassdoor, and 84% of Upstart-raters would recommend a friend to work at the company. Girouard also has an excellent 98% Glassdoor-approval rating as CEO, far higher than the average Glassdoor CEO approval rating of 69% in 2019. The interview that Girourd did with First Round also gives great insight on the impressive way he has built and currently leads Upstart (link here again). Here’re some quotes from him from the interview that we find memorable and helped us to size him up as a CEO:

“With Upstart, I’ve had this view that I’m trying to build this thing that’s going to be around long after I’m gone. So I feel like decisions should be made as far down in the company as they can. I should be doing things that only the CEO can do. If I have to do people’s jobs for them, I always ask them why that is. If I have to make a decision that I think somebody on my staff should be able to make, it makes me wonder why that is.

And it doesn’t mean that I’m looking to just kick back and read TechCrunch or the First Round Review. Rather it’s that I want to be thinking about how the company is operating. The management by exception construct is that I’m trying to build this engine that just runs really well. I want to be observing it in motion, and I want to say, ‘Did that happen the way it’s supposed to happen?’

That machine requires incredible talent at the executive level. It requires good direction and coordination. And it always has to grow and mature and get better at what it does. I want the people who work for me to feel stretched and to be in a place where many of them could take my role, and the company really wouldn’t miss a beat.

Somebody came to me just a few weeks back, and said, ‘Hey, I’d like to put some money towards X. I’m not sure if Upstart’s really up for putting money towards X, but I think we should. Dave, can you approve this?’ And I was like, ‘I don’t want to approve this. There’s plenty of other people that could say yes to this. You don’t need to ask me.’

Don’t get me wrong — if I don’t like something that we’re doing, trust me, I can be very difficult. I’m not passive in any sense. It’s just that my ideal scenario is that I have an amazing team that’s doing the right things. I’m helping, advising, judging, and occasionally breaking a tie, but ultimately the company is a well-oiled machine that knows how to do what it does.”

Fourth, we appreciate the ambitious nature of Upstart’s management team. The company has publicly stated that it sees a vast opportunity to bring its AI-lending software platform from personal loans to many other types of loan products, such as auto loans, credit cards, mortgages, student loans, point-of-sale loans and HELOCs (home equity lines of credit). We believe this ambition greatly increases the chances that Upstart will continue to find significant room to grow in the years ahead. It also helps that Upstart has managed to successfully tackle the hardest type of consumer loan product, the unsecured personal loan. Upstart has begun making inroads into the auto loans market, as we mentioned earlier. It’s still early days, but the company’s progress is promising. During Upstart’s 2021 second quarter earnings conference call, Girouard said (emphasis is ours):

“We started in January, offering our auto refinance product in a single state, then expanded to 14 states by the end of Q1 and have now expanded to 47 states, covering more than 95% of the U.S. population. We’ve also improved our funnel conversion rate about 100% since the beginning of the year despite expanding from states with minimal funnel friction to those with the most. This is critical because funnel efficiency is the primary way we’ll scale up auto loan originations, just as we’ve done historically with personal loans. Upstart-powered banks have now originated more than 2,000 auto refinance loans in 40 different states. And these loans are beginning to provide the repayment data that is the fuel to our AI models. And lastly, we now have our first five banks and credit unions signed up for auto lending on our platform.”

4. Revenue streams that are recurring in nature, either through contracts or customer-behaviour

In the “Company description” section of this article, we broke down Upstart’s sources of revenue. 96.4% of the company’s revenue in the 12 months ended 30 June 2021 came from referral fees, platform fees, and servicing fees.

The servicing fees naturally recur so long as Upstart is servicing an active loan that is held by a bank partner or institutional investor. We believe that both the referral fees and platform fees are also recurring in nature. This is because consumers request for loans all the time, and the fees are earned each time Upstart refers a loan to its bank partners or each time a loan is originated through Upstart’s platform.

But none of the above mean that banks will not reduce their appetite for originating loans when economic conditions are tough. Even if consumers want loans, Upstart would not be able to earn revenue if its bank partners are not keen to originate loans. Upstart’s business suffered in the second quarter of 2020, which was the height of the COVID-19 outbreak. The onset of the pandemic led to a rapid rise in unemployment in the USA, which in turn led to a reduction in loan originations by Upstart’s bank partners and a temporary pause in loan-funding from institutional investors. As a result, Upstart saw a massive sequential decline of 86% in the number of transacted loans from the first quarter of 2020 to the second quarter. This said, our eyes are fixed on the long-term opportunity with Upstart and we think the company does have strong recurring revenue over the long run. As it stands, Upstart’s business has returned to growth and we’ll discuss this in greater detail in the “A proven ability to grow” sub-section of this article.

5. A proven ability to grow

Upstart has a short history as a public-listed company (its IPO was only in December 2020) so we don’t have much financial data to study for the company. But we like what we see. The table below shows the key annual financial figures for Upstart that we can obtain:

Source: Upstart IPO prospectus and 2020 annual report

A few key things to highlight from Upstart’s historical financials:

- Revenue has compounded at an excellent annual rate of 69.3% from 2017 to 2019. Upstart’s revenue growth decelerated in 2020 – to a still excellent 42.2% – largely because of the severe decline in transacted loans that happened in the second quarter of the year. We mentioned this in the “Revenue streams that are recurring in nature, either through contracts or customer-behaviour” sub-section of this article. For more perspective, Upstart’s transacted loans and revenue declined in the second quarter of 2020 by 71% and 47%, respectively, compared to the same quarter a year ago. These numbers make Upstart’s overall revenue growth in 2020 even more impressive.

- Our focus is not on Upstart’s net income at the moment, but on its cash flow. Nonetheless, we appreciate the fact that the company produced a profit in 2020 and that its net income margin has been trending in the right direction (-13.5% in 2017, -12.4% in 2018, -0.3% in 2019, and 2.6% in 2020).

- The company produced positive operating cash flow and free cash flow in each year for the whole period we looked at. There’s no clear trend of growth in Upstart’s cash flows yet, but we’re not worried. Upstart operates an asset-light software business. Because of this, we believe that Upstart will benefit from operating leverage as its business scales, leading to stronger free cash flow over time.

- The company’s balance sheet was not the strongest in 2018 and 2019 as there was more debt than cash in both years. But the situation changed in 2020, and as mentioned earlier in the “A strong balance sheet with minimal or a reasonable amount of debt” sub-section of this article, Upstart ended the second quarter of 2021 with a robust balance sheet that had US$500 million in net cash.

- We usually look at changes in a company’s share count over time to determine if there has been egregious shareholder dilution in the past. In the case of Upstart, we did not look at its share count since the company was listed only in December 2020. We do note that Upstart had a share count of 72.46 million right after its listing and we will be comparing Upstart’s future share counts with this number. Ultimately, what we want is to see Upstart produce business growth that significantly outweighs increases in its share count, if any.

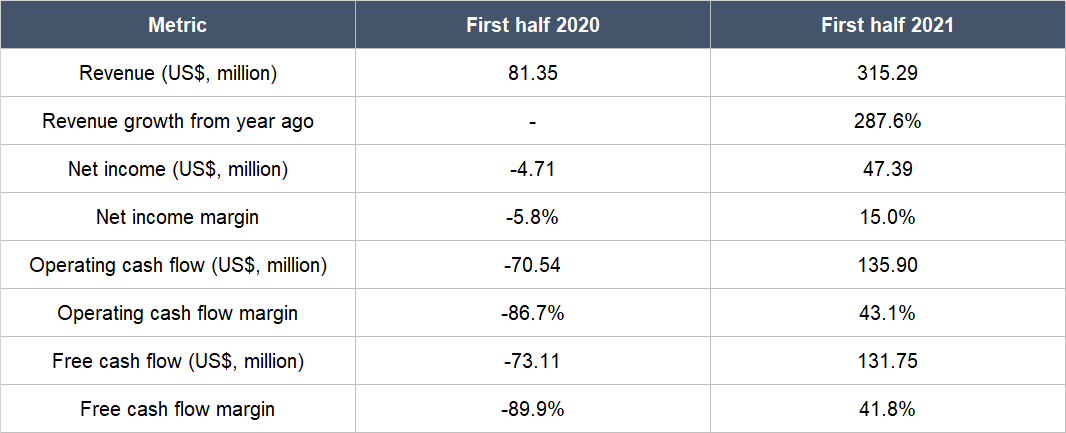

Upstart has reported its results for the first half of 2021 and its revenue growth has accelerated significantly from the growth rate seen in 2020. This is shown in the table below. It also shows that there were impressive improvements during the first half of this year in Upstart’s net income, net income margin (net income as a percentage of revenue), operating cash flow, operating cash flow margin (operating cash flow as a percentage of revenue), free cash flow, and free cash flow margin (free cash flow as a percentage of revenue).

Source: Upstart quarterly earnings updates

6. A high likelihood of generating a strong and growing stream of free cash flow in the future

We showed in the “A proven ability to grow” sub-section of this article that Upstart had already been producing positive free cash flow in each year from at least 2017.

During the first half of 2021, its free cash flow margin was an outstanding 41.8%. We don’t expect such a high free cash flow margin to be sustainable over the long run, but we believe that Upstart can still produce a robust free cash flow margin in the future. This is because the company is an asset-light software business at its core.

Valuation

Our initial purchases of Upstart shares were completed around the middle of August 2021. Our average purchase price was US$195 per share. At our average price and on the day we completed our purchases, Upstart’s shares had a trailing price-to-free cash flow (P/FCF) ratio and trailing price-to-sales (P/S) ratio of around 85 and 39, respectively. We like to keep things simple in the valuation process. In Upstart’s case, we think the P/FCF and P/S ratios are appropriate metrics to gauge the value of the company. For the P/FCF ratio, it is because Upstart has been producing free cash flow for a number of years, and its free cash flow margin has increased markedly in the first half of 2021. For the P/S ratio, it’s useful when Upstart’s free cash flow is light because it is reinvesting into its business for future growth.

The P/FCF and P/S ratios of 85 and 39 are high and that’s a risk. But we’re willing to pay a premium for a few reasons. First, Upstart has been growing its revenue at a rapid clip over the past few years and yet still has huge consumer loan markets to conquer. Second, we believe that Upstart has a high chance of being able to continue growing at this rapid clip in the years ahead. Third, we think that Upstart can command strong free cash flow margins when it’s at a more mature state.

For perspective, Upstart carried P/FCF and P/S ratios of around 84 and 39 at its 20 August 2021 share price of US$194.

The risks involved

We see a few key risks that could upend our investment in Upstart.

In our view, Dave Girouard and Paul Gu have been instrumental in Upstart’s past growth and they will continue to have an outsized influence on the company’s future growth. Because of this, we think there’s key-man risk with Upstart. We will be concerned if Girouard and/or Gu were to leave the company for any reason.

There’s also significant customer-concentration risk. We mentioned in the “Company description” section of this article that Cross River Bank originated 67% and 60% of Upstart’s loans in 2020 and the first half of 2021, respectively. So it’s not a surprise to note that Cross River Bank accounted for 63% and 62% of Upstart’s total revenue for the same periods.. There’s another unnamed bank that’s an important customer of Upstart: It made up 18% of Upstart’s total revenue in 2020 and 23% in the first half of 2021. The good thing is that Upstart has been signing up more bank partners – the number has increased from 10 as of 30 September 2020 to 25 today. And according to Girouard’s comment in Upstart’s 2021 second-quarter earnings conference call, there’s a “robust and growing list of lenders in [Upstart’s] pipeline for the second half of 2021.” As Upstart’s number of bank partners increases over time – which is likely to happen, in our view, given the benefits that Upstart’s AI-powered lending software platform can provide – we believe the level of customer-concentration should decrease. There are already signs of this happening. Cross River Bank accounted for 83% of Upstart’s revenue in 2017, which is much higher than the 60% seen for the first half of 2021.

We’re watching another form of concentration risk: This time with suppliers. In the “Company description” section of this article, we wrote that loan-aggregator website Credit Karma accounted for 49% and 52% of Upstart’s total loan originations, respectively, for the first half of 2021 and the whole of 2020. Any changes to the business direction of Credit Karma could thus severely hurt Upstart’s business. But there are two things that give us comfort for now:

- Upstart makes up a large chunk of Credit Karma’s revenue (Upstart pays customer-acquisition fees to Credit Karma), so it’s likely that the latter would not want to rock the boat.

- The fastest growing channel for Upstart are consumers that come directly to the company for loans. If this continues, Credit Karma’s importance to Upstart will steadily decrease over time.

Although Upstart’s AI models have incorporated data generated since the onset of the COVID-19 pandemic, the development of the models and the bulk of the data gathered for them have largely occurred during a period of sustained economic growth in the USA. This means that Upstart’s AI models have yet to be battle-tested against a prolonged recession in the USA and it is a risk. There’s a possibility that Upstart’s AI models will fail to properly assess credit risk in the next long-drawn economic downturn for the country. If so, Upstart’s future business-growth could be severely stunted as prospective and current bank partners, along with institutional investors that invest in Upstart-powered loans, may lose confidence in the company’s AI-powered lending software platform. But we think the chances are high that Upstart’s AI models will be able to handle the challenges that are thrown their way. During Gu’s May 2021 interview that we referenced earlier, he explained how Upstart’s AI models handled the COVID-19 pandemic with aplomb (emphasis is ours):

“Lending of course, we always talk a lot about the economic cycle. When times are good, everybody seems to be lending. When times are bad, no one wants to be lending. When times are good, everyone is worried about when times are bad. One of the things we’ve always believed is that this fascination with the economic cycle and the focus on when the bad part of the cycle is coming, is a symptom of an approach to lending that is not particularly robust or predictive. It means that lenders aren’t really able to predict very well the individual consumer’s level of risk. What they are really just doing is saying ‘Overall, times are good now and we assume right now we are going to get a 5% default rate. When times are bad, that 5 is going to change to 10.’ It’s almost like a throwing-paint-against-the-wall approach. When the seasons change, everything just goes from good to bad.

Our belief has always been that the variation between individual borrowers far outweighs the variation between macroeconomic periods. And it’s very clear that’s the case when you actually zoom into the data and you see that even in the toughest economic climates, the vast majority of people in low-risk buckets still end up repaying their loans. The most interesting question is actually which individuals are actually in the low-risk buckets and not which period are you in.

And going back to the past year – a very interesting time. Not only was there a turn in the economic cycle but a very unusual one. And essentially what we saw was that – we saw certainly a lot of changes to consumer behaviour. But in aggregate we actually saw that the loan performance of the entire ecosystem across all our bank partners and capital markets partners – the returns that they were expecting to earn, they pretty much across the board consistently achieved or beat over the course of the last year in spite of the pandemic.

Having said that, I think a lot of that does have to do with some of the unique circumstances that happened here, which is another piece of what we really built into our model. And that’s about being able to respond to the macroeconomic changes, on really a dime. When unemployment rates started going up in Q2 of 2020, that was a time where it was really important to be able to respond very quickly and precisely to the changes in the unemployment rates.

You wanted to be able to know in which sectors, occupations, etc, there was extra unemployment risk that you needed to be modelling in and how to model it relative to traditional norms. You wanted your model to handle that because the alternative was getting a group of people sitting around the table and do some back-of-the-envelope math and take a blunt cut to your credit box. So it means that you’re either going to still be taking on too much risk or essentially just stop running your business during this challenging time. What we found was that we were able to continue approving a significant number of people for loans and have those people pay back because they were the right people to lend to.On the reverse side, as things started normalising, again you want that system that can respond very dynamically to updating macroeconomic data and that’s a system that we built and it worked incredibly well over the last year.”

The last important risk we’re keeping our eyes on is valuation risk. We think Upstart’s business is likely to grow at a rapid clip for many years and so it deserves its premium valuation. But if there are any hiccups in Upstart’s business – even if they are temporary – there could be a painful fall in the share price. This is a risk we’re comfortable taking as long-term investors.

Summary and allocation commentary

To summarise Upstart, it has:

- A massive market to grow into in the form of the entire consumer loan market.

- A robust balance sheet with significantly more cash than debt.

- A management team that has an excellent multi-year track record with execution and innovation.

- High levels of recurring revenues through annual servicing fees and usage-based platform and referral fees.

- A history of impressive revenue growth; the company has also been generating positive operating cash flow and free cash flow for a number of years.

- A good chance of being able to produce strong free cash flow in the future.

As it is with every company, there are risks to note for Upstart. The main ones we’re watching include key-man risk; Upstart’s heavy reliance on Cross River Bank for revenue and Credit Karma for customer-acquisition; the possibility that Upstart’s AI models will handle the next recession poorly; and the company’s high valuation.

After weighing the pros and cons, we decided to initiate a position of around 0.6% in Upstart in the middle of August 2021. Our initial position in Upstart can be considered to be a small-sized allocation. We appreciate all the strengths we see in Upstart’s business, but our enthusiasm is currently tempered by the company’s high valuation and the fact that the company’s AI models have yet to prove itself in a prolonged recession for the US economy.

And here’s an important disclaimer: None of the information or analysis presented is intended to form the basis for any offer or recommendation; they are merely our thoughts that we want to share. Of all the other companies mentioned in this article, Compounder Fund does not own shares in any of them. Holdings are subject to change at any time.