Compounder Fund: The Trade Desk Investment Thesis - 13 Nov 2020

Data as of 12 November 2020

The Trade Desk (NASDAQ: TTD), which is based and listed in the USA, is one of the 40 companies in Compounder Fund’s initial portfolio. This article describes our investment thesis for the company.

Company description

Today, advertisers have a multitude of decisions to make when advertising digitally. For instance, they have to track their advertising returns on investment over multiple channels, choose which channels and platforms to advertise on, and how to use data to make the most of their advertising dollars.

Enter Trade Desk, which provides a self-service, cloud-based programmatic advertising platform. Trade Desk launched its platform in 2011 and initially targeted just display advertising (a type of online advertisement combining text, images, and a web-link to the advertisers’ webpage). Today, Trade Desk’s platform empowers buyers of advertisements to optimise digital advertising campaigns across advertising formats and channels, including display, video, audio, in-app, native, and social. The digital adverts that can be analysed and purchased through Trade Desk’s platform also cuts across devices, including computers, mobile devices, and connected televisions (connected televisions, also known as CTVs, are TVs that are connected to the internet).

Some of the key features of Trade Desk’s platform include:

- Auto-optimisation that allows advertisement buyers to automate their campaigns and also supports them with computer-generated modelling and decision making.

- Advanced reporting and analytics tools to help advertisers understand and learn from their advertising campaigns.

- The ability to link digital campaigns to offline sales results or other business objectives

- Enabling advertisement buyers to license a broad selection of data from third-party vendors to further improve their digital advertising campaigns

- The Koa Artificial Intelligence predictive engine that makes recommendations for campaign optimisations

- Support for advertisement buyers to transact directly with individual digital advertising publishers

- The ability for customers to use Trade Desk’s APIs (application programming interfaces) to build their own technology on top of the company’s platform

- A solution for users to launch omnichannel programmatic media plans

At the core of Trade Desk’s platform is its bid-factor architecture that allows advertisement buyers to define desirable factors and (importantly!) the value associated with those factors. Trade Desk’s platform will then compute, in real-time, the value of digital advertising impressions based on these factors, and bid only for optimal impressions. (An impression is when a digital advertisement shows up on a user’s screen.) Impressively, the bid-factor architecture built by Trade Desk allows users of the company’s platform to create “billions of different bid permutations with only a few clicks.” All of these result in better targeting, more efficient spending, and improved campaign results for advertisement buyers.

The ability to bid intelligently and quickly for digital advertising space that Trade Desk’s platform gives advertisement buyers is important to them. You may not know this, but when you visit a webpage, watch a video, use a mobile app, or use a CTV, there is often a behind-the-scenes auction for advertising inventory that’s being run in about 1/10th of one second as the content loads.

To be clear, Trade Desk’s platform is not a marketplace that connects buyers and sellers of digital advertising. Trade Desk’s primary role is to help advertisement buyers get the most out of their advertising dollars by helping them purchase the right ads at the right prices.

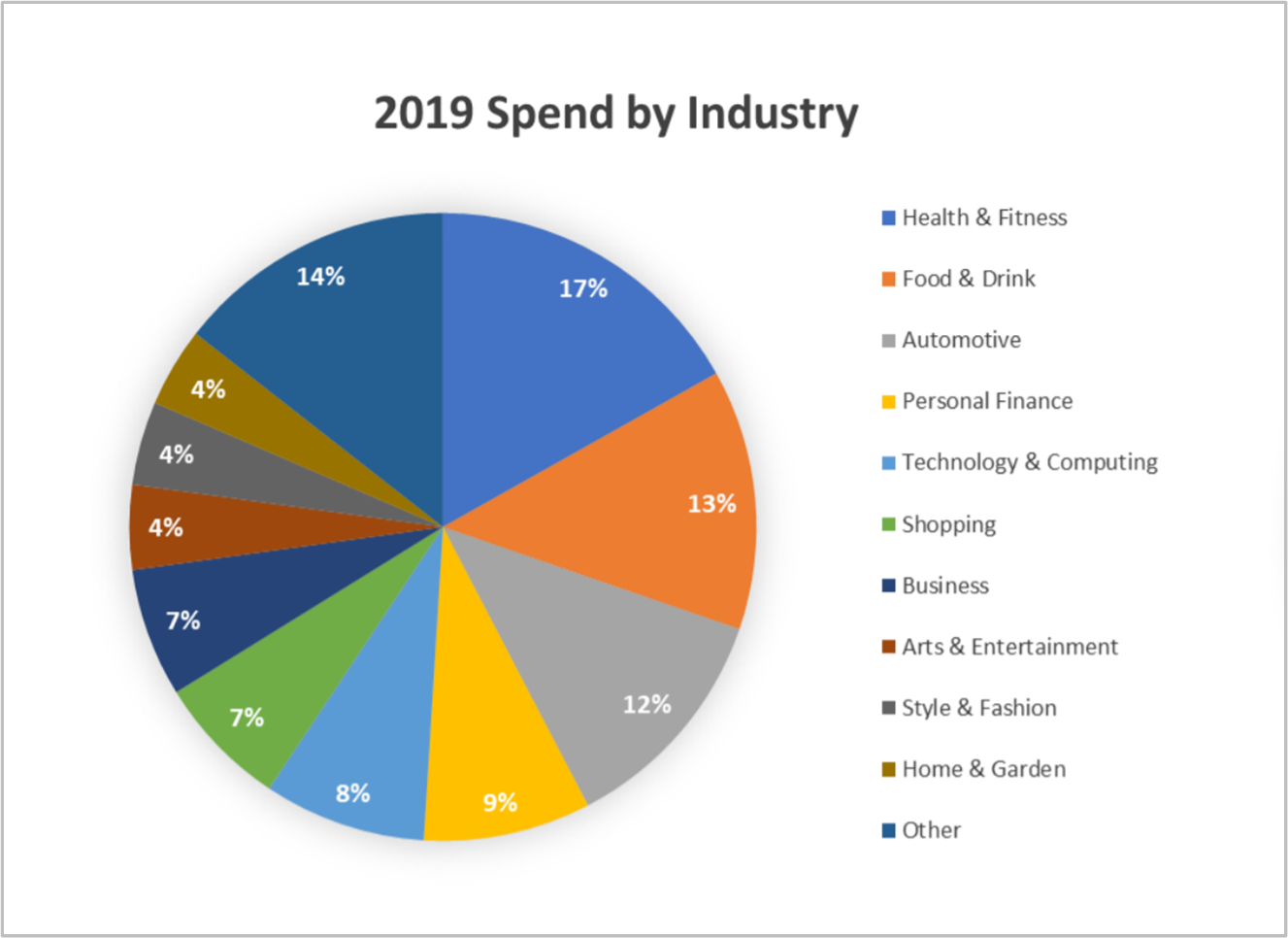

Trade Desk’s clients are mostly advertising agencies and other service providers for advertisers. But Trade Desk is diversified in terms of the end-industries that its programmatic advertising platform serves. Companies from all kinds of industries – from health & fitness to technology & computing, and from arts & entertainment to business – depend on Trade Desk for their digital advertising needs.The chart below shows the breakdown of the advertising-spend by industry that took place on Trade Desk’s platform in 2019.

Source: Trade Desk investor presentation

From a geographical perspective, Trade Desk is currently concentrated in the USA. The country accounted for an estimated 86% of Trade Desk’s total revenue of US$516.1 million in the first nine months of 2020.

Investment thesis

We have laid out our investment framework in Compounder Fund’s website. We will use the framework to describe our investment thesis for Trade Desk.

1. Revenues that are small in relation to a large and/or growing market, or revenues that are large in a fast-growing market

As we described earlier, Trade Desk’s business is in the programmatic advertising space. The company’s IPO prospectus, released in the second half of 2016 (Trade Desk was listed in September 2016), contains a succinct and compelling description of why programmatic advertising is likely to be a fast-growing market:

“In 2015, approximately [US]$639.6 billion was spent on global advertising (including approximately [US]$237.2 billion on TV advertising and approximately [US]$51.1 billion on display advertising), according to IDC, and approximately [US]$14.2 billion was transacted in the programmatic advertising spot market via realtime marketplaces, according to Magna Global. We [the use of “we” refers to Trade Desk] aim to power every agent of every advertiser in both the spot and forward markets, including upfront purchases, for programmatic advertising.

We also believe that the efficiency of programmatic advertising will lead to a greater percentage of every advertising dollar ending up in the pocket of publishers. Publishers can now generate revenue without the large sales forces that were required in the past. Higher revenue yields and lower operating costs make it possible for publishers to increase their investment in creating high quality content.

Programmatic advertising is currently a small portion of total global advertising spend. Largely because of the price discovery benefits, we believe eventually a vast majority of advertising will be transacted programmatically.”

We agree with Trade Desk’s train of thought that programmatic advertising has solid advantages over more primitive forms of advertising, and so is likely to eventually take a massive share of the global advertising market over time. Trade Desk’s IPO prospectus also mentioned that the global programmatic advertising market was expected to grow from US$14.2 billion in 2015 to US$36.8 billion by 2019, according to Magna Global.

For perspective, around US$3.6 billion in advertising spending took place on Trade Desk’s programmatic advertising platform for the 12 months ended 30 September 2020. Meanwhile, the company earned US$732.1 million in revenue for the same period. These numbers are small when compared to the estimated size of the global programmatic advertising market in 2019. Importantly, we expect this market to grow at a healthy clip in the future, as we shared earlier.

2. A strong balance sheet with minimal or a reasonable amount of debt

Trade Desk has a pristine balance sheet. As of 30 September 2020, the company had US$577.3 million in cash and short-term investments, but just US$72.0 million in debt. For the sake of conservatism, we also note that Trade Desk had US$205.4 million in operating lease liabilities. But the company’s cash and short-term investments still significantly outweigh the sum of its debt and operating lease liabilities (US$277.4 million).

Moreover, Trade Desk has already been generating positive free cash flow for a number of years and even managed to do so in the first nine months of 2020, despite the presence of COVID-19. There will be more on Trade Desk’s free cash flow later.

3. A management team with integrity, capability, and an innovative mindset

On integrity

Trade Desk’s most important leader is one of its co-founders, Jeff Green. The 43 year-old Green is currently Trade Desk’s CEO and has been so since 2009, the year of the company’s founding. The other co-founder of Trade Desk is Dave Pickles, 42, who has been the company’s chief technology officer since May 2010. We appreciate the fact that Green and Pickles have already been leading Trade Desk for 10 years or more despite their current young age.

We think that Green and Pickles’ compensation structure at Trade Desk demonstrates integrity. In 2019, their total compensation were US$12.14 million and US$4.26 million, respectively. These aren’t small sums. But importantly, 63.6% of Green’s total compensation for the year came from restricted stock awards (RSAs) and stock options that both vest over a four-year period. For Pickles, 65.0% of his total compensation also came from the same type of RSAs and stock options as Green’s. What these numbers mean is that the lion’s share of Green and Pickles’ total compensation for 2019 depend on multi-year changes in Trade Desk’s stock price, which is in turn driven by the company’s business performance. So, the interests of Green and Pickles are well-aligned with Trade Desk’s other shareholders.

Another thing we appreciate is that Green and Pickles have significant skin in the game. As of 29 February 2020, they controlled a total of 5.665 million Trade Desk shares (5.278 million for Green, and 387,608 for Pickles). At Trade Desk’s 12 November 2020 stock price of US$742, their shares are collectively worth more than US$4.2 billion.

We note that 96% of Green’s Trade Desk shares are of the Class B variety. Trade Desk has two share classes: (1) Class B, which are not traded and hold 10 voting rights per share; and (2) Class A, which are publicly traded and hold just 1 vote per share. As a result, Green controlled 55.0% of Trade Desk’s voting power (as of 29 March 2020) despite holding just 11.5% of the company’s total shares. A manager having significant control over the company can potentially be bad for shareholders. This concentration of Trade Desk’s voting power in the hands of Green means that we need to be comfortable with him at the company’s helm. We are.

We also note that Trade Desk will be holding a special shareholders’ meeting on 7 December 2020 to vote on the removal of the company’s dual share class structure in five years. Green himself supports the move. Whether Trade Desk ends up with just a single share class or not does not matter to us – what matters is whether Green stays on as CEO.

On capability and ability to innovate

We rate Jeff Green and Dave Pickles highly on this front. There are a few things we want to discuss.

First, Green has an impressive history of innovation and entrepreneurship, even before his Trade Desk days. In 2004, he co-founded AdECN, the world’s first online advertising exchange, which was acquired by Microsoft in 2007. At Microsoft, he met Pickles, and together, they pioneered the development of programmatic advertising.

Second, Trade Desk has an impressive multi-year record of (1) growing its customer-count, (2) retaining its customers, (3) driving growth in the advertising spending that takes place on its platform, and (4) increasing its spending per customer. These dynamics are illustrated in the table below (note the much higher year-on-year growth rates in advertising spending compared to the growth rates in the customer count – this signals stronger spending per customer over time):

Source: Trade Desk IPO prospectus, annual reports, and quarterly earnings updates

Third, Trade Desk has a long history of successful innovation and we credit Green, Pickles and the other leaders in the company for this. For example, we mentioned earlier that when Trade Desk first launched its programmatic advertising platform in 2011, it could only work on display advertising. But over time, Trade Desk has successfully expanded the platform’s repertoire – in 2019, 79% of the advertising spending that happened on Trade Desk’s platform were for mobile, video, audio, native, and social advertisements.

In another instance, Green and Pickles have architected a platform that can perform at massive scale. And impressively, that scale is growing. Trade Desk commented in its IPO prospectus (released in the second half of 2016) that its platform provides “access to over 200 billion ad impressions per day, reaching over 180 million devices per day on a global basis.” In Trade Desk’s 2019 annual report, the company shared that the daily ad impressions has ballooned to 790 billion while the devices it can reach is now 819 million. This scale is not easy to achieve. Here’re Green’s comments on the matter that was shared in an excellent 2017 article on Trade Desk written by Amit Chowdhry for Forbes:

“We are considering over 9 million ad opportunities every single second – which is massive. For instance, Google gets about 63,000 searches per second (according to InternetLiveStats.com). So that’s less than 1% of the ad opportunities of the rest of the Internet. And to make it even more mathematically challenging, we have to consider quadrillions of permutations for each advertiser as we consider each opportunity. We have to consider the many thousands of advertisers we power when we look at millions of ads for each. I think our engineers have accomplished one of the most difficult and impressive achievements in the history of the Internet. Like most technological achievements, the tough stuff doesn’t get much air time because it’s so nuanced and difficult to explain.”

In yet another example, here’s Trade Desk describing, in an October 2020 regulatory filing, the success it has experienced for its innovative Unified ID initiative and the improvements it’s currently driving in this area:

“In 2018, we launched Unified ID, enabling the digital advertising ecosystem to utilize our cookie footprint to increase their own cookie coverage across the open internet and level the playing field with large walled gardens, thereby furthering the market’s independence from the world’s largest advertising platforms. To date, our Unified ID has been adopted by nearly every major supply-side platform and many others in the ad ecosystem.

Today, we are building on our success with Unified ID, in collaboration with the Interactive Advertising Bureau, to create an upgraded identity solution for the open internet that no longer relies on cookies or other advertising identifiers. This initiative, based on our long-term perspective on identity and privacy, is consistent with a range of investments we have made to move the industry forward and build trusted standards and practices – whether they concern fraud management, supply chain transparency or objective measurement.”

Fourth, there are signs that Green has built a good corporate culture at Trade Desk. Glassdoor is a platform that allows employees to rate their companies anonymously. Currently, 69% of Trade Desk-raters on Glassdoor will recommend the company to a friend. Meanwhile Green has a 91% approval rating, far higher than the average Glassdoor CEO rating of 69% in 2019.

4. Revenue streams that are recurring in nature, either through contracts or customer-behaviour

Trade Desk earns revenue primarily by charging a platform fee that’s based on a percentage of a customer’s total advertising spend. The company also generates revenue from providing data and other value-added services and platform features.

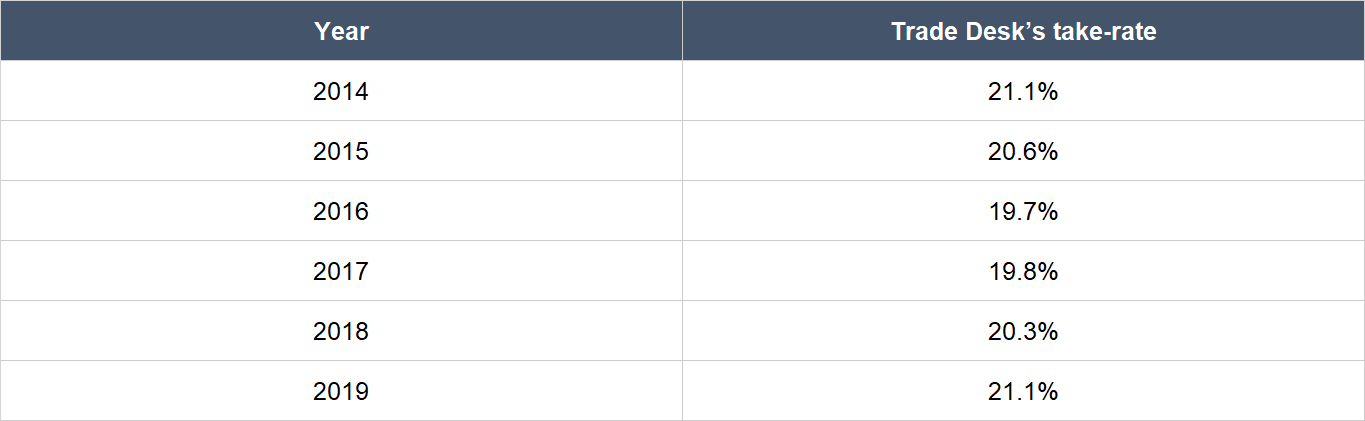

Advertising is often an essential and ongoing investment for many businesses. By taking a cut of advertising spending that takes place on its platform, we believe that Trade Desk has a high level of recurring revenue because of customer behaviour. Lending weight to our view are three things we’ve discussed about the company earlier: (1) Its client retention rate of more than 95% going back to at least 2014, (2) the rise in its customer count over time, and (3) the growth in spending per customer it has experienced. Another thing is the stable take-rate (revenue as a percentage of advertising spend) of around 20% that Trade Desk has enjoyed. This is shown in the table below:

Source: Trade Desk annual reports

But none of the above mean that Trade Desk’s customers will not reduce their advertising spend over the short run when economic conditions are tough. The current COVID-19 pandemic illustrates this dynamic clearly: Trade Desk’s revenue fell by 12.9% in the second quarter of 2020. This said, our eyes are fixed on the long-term opportunity with Trade Desk and we think the company does have strong recurring revenue over the long run.

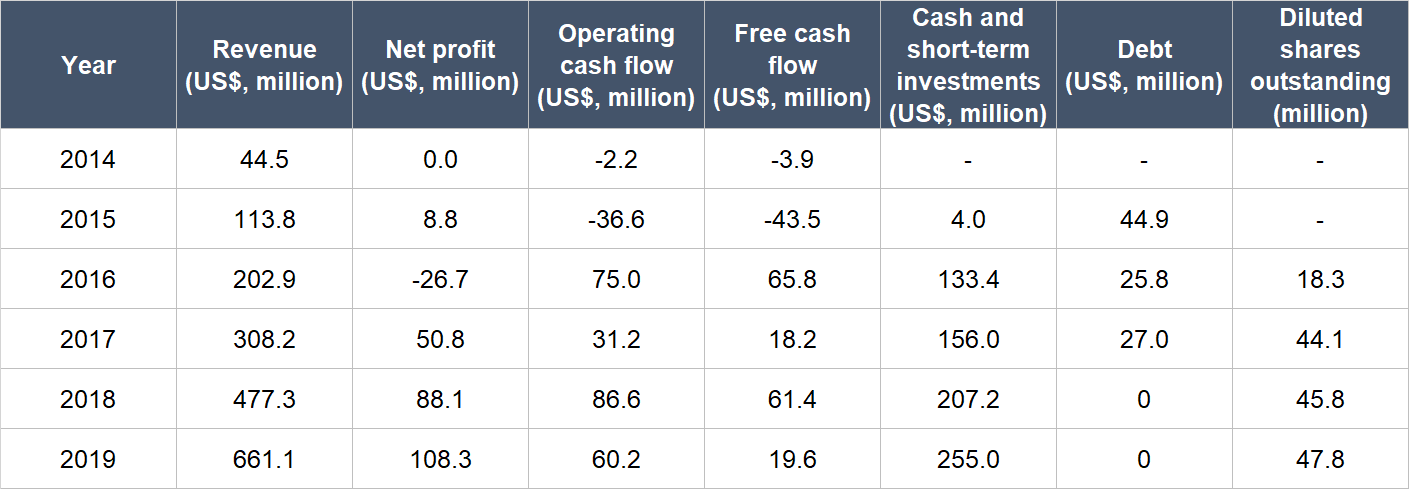

5. A proven ability to grow

The table below shows Trade Desk’s key financials since 2014 (they are the earliest data we can find, since the company was listed only in September 2016)

Source: Trade Desk annual reports

Some important things to highlight from the numbers above:

- Revenue has compounded at an impressive rate of 71.5% annually from 2014 to 2019. Growth has slowed in more recent years, but 2019’s performance was still strong at 38.5%.

- Trade Desk has started to generate a net profit consistently since 2017, and the company clocked in a decent net profit margin of 16.4% in 2019.

- Operating cash flow and free cash flow have both been consistently positive since 2016. There are some ebbs and flows in both financial numbers, but it’s nothing we’re concerned with.

- The balance sheet has been strong since 2016, with Trade Desk’s debt being either zero or significantly lower than its cash and short-term investments.

- At first glance, Trade Desk’s diluted share count appeared to increase significantly by 141% from 2016 to 2017 (we only started counting from 2016 since Trade Desk was listed in the month of September during the year). But the number we’re using is the weighted average diluted share count. Right after Trade Desk got listed, it had a share count of around 38.2 million. From 2017 to 2019, Trade Desk’s weighted average diluted share count increased by only 4.2% per year, so we don’t think the company has been diluting shareholders.

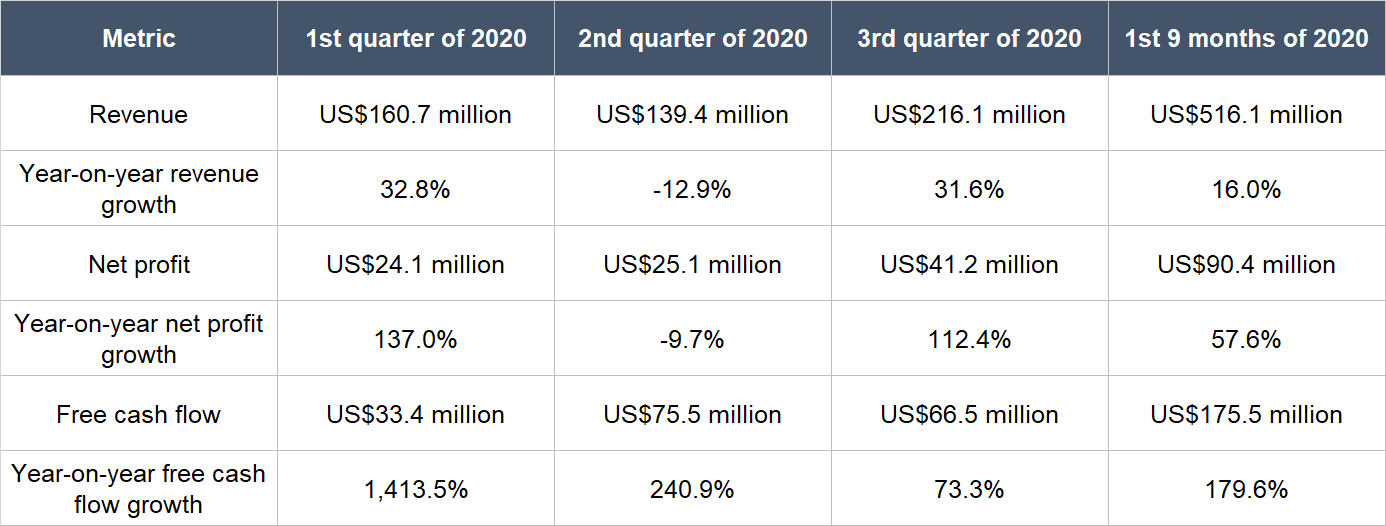

2020 has been an odd year for Trade Desk so far. The company experienced robust growth in the first quarter of the year but then saw its revenue fall by 12.9% in the second quarter (as we mentioned earlier) because of the economic challenges posed by COVID-19. During the third quarter, Trade Desk returned to strong growth again. The table below shows the year-on-year changes in Trade Desk’s revenue, net profit, and free cash flow for the first three quarters of 2020. There was also only mild dilution in the period, with Trade Desk’s weighted average diluted share count rising by just 2.1% in the first nine months of 2020 compared to a year ago.

Source: Trade Desk quarterly earnings updates

During Trade Desk’s 2020 third-quarter earnings conference call, Jeff Green also shared a very positive note on the long-term growth prospects of the company:

“In this environment, marketers have come to more fully appreciate the power of data-driven advertising. And as that happens, we are becoming indispensable. We developed closer relationships with the biggest brands and the agencies in the world, and we are winning more business with both new and existing customers. In addition, we continue to see rapid growth in key channels, such as Connected TV, which grew more than 100% year over year.

This was a very encouraging quarter, not only in terms of our revenue and market share growth, but also what it signals about our growth opportunity moving forward.”

Speaking of Trade Desk’s future growth, we want to point out the China opportunity. Trade Desk officially launched its programmatic advertising platform in China during the first half of 2019. The company has partnerships with some of China’s largest technology companies, including Alibaba, Baidu, and Tencent. The early signs are promising. Green shared during Trade Desk’s 2020 third-quarter earnings conference call that China is the company’s fastest-growing geography at the moment. The opportunity for Trade Desk in China could be immense, given that the country currently has more than 940 million internet users – this means there’s a massive potential audience for programmatic advertising.

6. A high likelihood of generating a strong and growing stream of free cash flow in the future

We think Trade Desk aces this criterion for a few reasons:

- First, there is a high likelihood, in our view, that Trade Desk’s revenue can continue to grow at a high double-digit rate in the years ahead, driven by the growing adoption of programmatic advertising by advertisers and Trade Desk’s strong position in the space.

- Second, Trade Desk has already been generating free cash flow for a few years. Moreover, the company’s free cash flow margin (free cash flow as a percentage of revenue) in the first nine months of 2020 reached an impressive 34.0%. This is even more remarkable given the current backdrop of COVID-19 posing tough challenges for economies around the world, including the USA. We think it’s likely that Trade Desk will produce strong free cash flow margins in the years ahead on average (the margin could be weak in any given year).

Valuation

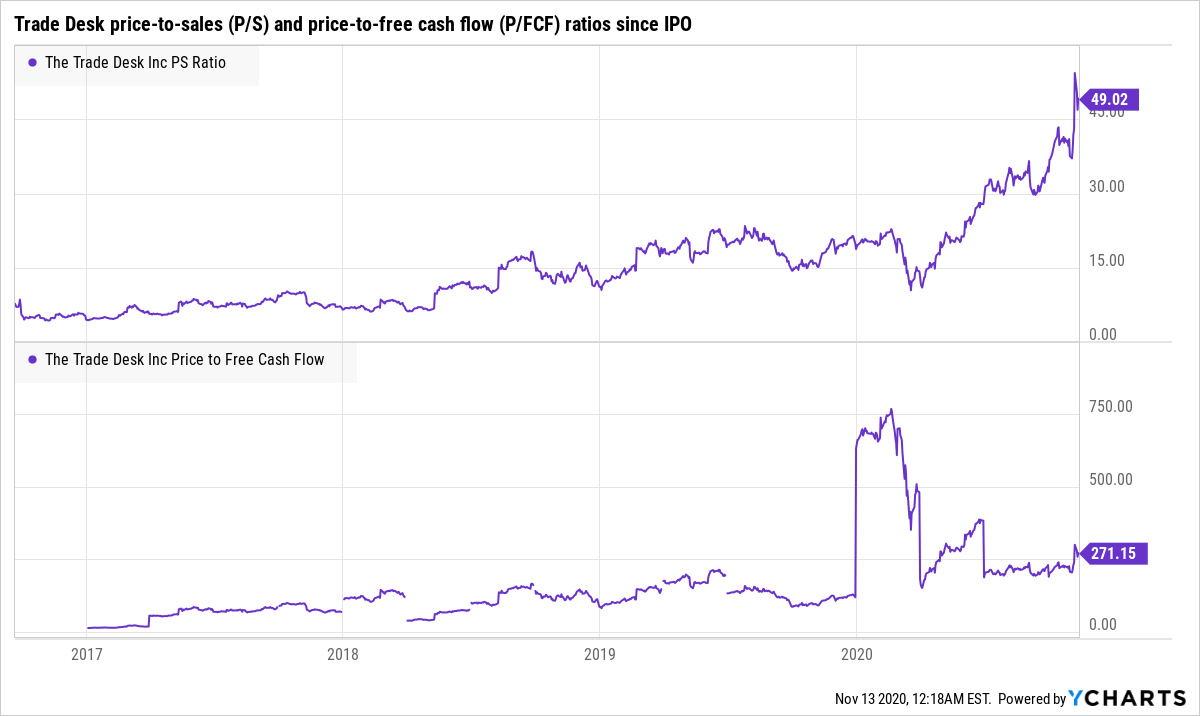

We completed our purchases of Trade Desk shares with Compounder Fund’s initial capital in late July 2020. Our average purchase price was US$437 per Trade Desk share. At our average price and on the day we completed our purchases, the company’s shares had trailing price-to-sales (P/S) and price-to-free cash flow (P/FCF) ratios of around 30 and 415, respectively.

We like to keep things simple in the valuation process. In Trade Desk’s case, we think the P/S and P/FCF ratios are appropriate metrics to gauge the value of the company. This is because Trade Desk already has a few years of history in producing positive free cash flow. Plus, the company’s recent free cash flow margin (34% for the first nine months of 2020) is robust. And when free cash flow is light, the price-to-sales (P/S) ratio will be useful.

The P/S ratio of 30 and P/FCF ratio of 415 are high – and that’s a risk. These ratios are also high relative to their own histories: The chart below shows Trade Desk’s P/S and P/FCF ratios from its IPO to 12 November 2020.

But we think Trade Desk has years of rapid growth ahead of it. Programmatic advertising is so much better than other forms of advertising (see the simple chart below for an idea on the advantages that programmatic advertising on CTVs have over traditional advertising on linear TV) and Trade Desk is at the forefront of all the action. So, we’re comfortable with paying up for Trade Desk’s shares as we think there’s a good chance it could grow into its valuation.

Source: Trade Desk investor presentation

Source: Trade Desk investor presentation

For perspective, Trade Desk carried P/S and P/FCF ratios of 49 and 273, respectively, at the 12 November 2020 stock price of US$742.

The risks involved

We see four main risks with our investment in Trade Desk.

1. An extended period of economic contraction, for whatever reason, is probably the biggest threat to Trade Desk’s growth. In the current context, there’s the presence of COVID-19 as the biggest potential driver for any future global economic pain. We mentioned earlier that COVID-19 took its toll on advertisers in the second quarter of 2020, leading to a decline in revenue for Trade Desk in the quarter. Although Trade Desk’s business did return to strong growth in the third quarter, many countries in the world – the USA included – are currently grappling with another surge in COVID-19 infections. This could lead governments around the world to introduce new measures to curb the spread of the virus, potentially resulting in negative impacts to the economy and in turn, the advertising budgets of companies.

2. Key-man risk is another risk we’re watching. We think Jeff Green has been a phenomenal leader at Trade Desk and he has been a key reason for the company’s success thus far. Should he leave Trade Desk for any reason, we’ll be keeping an eye on the leadership transition. The good thing is that Green is still young at 43, so he can likely continue leading the company in the years ahead.

3. We’re also mindful of valuation risk. We can’t ignore that Trade Desk has lofty P/S and P/FCF ratios. We’re comfortable with paying up for Trade Desk’s shares, but if there are any slowdowns in Trade Desk’s growth – even if they are temporary – there could be a painful fall in its share price. This is a risk we’re comfortable taking on as long-term investors.

4. Lastly, there’s the risk of competition. It’s possible that other companies could come up with a better mousetrap than Trade Desk’s offerings. It’s worth noting that both Facebook and Alphabet (parent of the search engine Google) depend on digital advertising for the sheer majority of their revenues and they have substantially more financial might than Trade Desk. The good thing here is that Trade Desk has been growing impressively for a number of years.

Summary and allocation commentary

To sum up Trade Desk, the company has:

- A large addressable market – programmatic advertising – that is likely to grow in the years ahead (this is because programmatic advertising has many advantages over traditional forms of advertising)

- A pristine balance sheet with significantly more cash and short-term investments than debt

- A young, highly capable, and innovative CEO/co-founder in Jeff Green, who also has a compensation-structure that is well-aligned with the interests of the company’s shareholders

- A high level of recurring revenue because of customer behaviour

- A strong multi-year track record of revenue growth and producing positive profit and free cash flow

- A high likelihood of generating strong free cash flow in the future

There are important risks to note for Trade Desk, such as the potential for its business to be hurt in the event of an extended period of economic contraction; key-man risk; deep-pocketed competitors; and the company’s current high valuation.

After weighing the pros and cons, we initiated a 2.5% position – a medium-sized allocation – in Trade Desk with Compounder Fund’s initial capital. We’re attracted to Trade Desk’s potential for strong growth in the years ahead and also the fact that it is currently profitable and producing positive free cash flow. But our enthusiasm is tempered by the company’s high valuation.

And here’s an important disclaimer: None of the information or analysis presented is intended to form the basis for any offer or recommendation; they are merely our thoughts that we want to share. Of all the companies mentioned in this article, Compounder Fund also currently owns shares in Alphabet, Facebook, and Microsoft. Holdings are subject to change at any time.