Compounder Fund: The a2 Milk Company Sell Thesis - 23 May 2022

Data as of 22 May 2022

We first invested in The a2 Milk Company (ASX: A2M) for Compounder Fund’s portfolio in July 2020. Our investment thesis for the company can be found here. By April 2022, we had completely exited a2 Milk, after first selling a partial stake in July 2021. This article describes our Sell thesis for the company.

When we first invested in a2 Milk, the milk products specialist had an outstanding track record of growth and we saw a long runway for expansion of its business in two key areas: (1) The large and growing global infant formula market, particularly in China, and (2) the liquid milk markets of Australia, New Zealand, and the USA, where the company had low market share. We thought that with the positive qualities we saw in a2 Milk – discussed in our investment thesis – the company would be able to take advantage of the opportunities that were present. But after our investment, a2 Milk’s business turned sour because of COVID-19.

In the early days of the pandemic, a2 Milk’s management was initially optimistic about the company’s growth prospects. For example, in the company’s annual report for FY2020 (COVID-19 first started spreading throughout the world in early-2020, which was the second half of a2 Milk’s FY2020), management wrote that the pandemic “had a modest positive impact on revenue and earnings for the year.” Management also guided for “strong revenue growth” for FY2021. But in reality, a2 Milk’s growth curdled after FY2020 as COVID-19 strengthened its grip on the world.

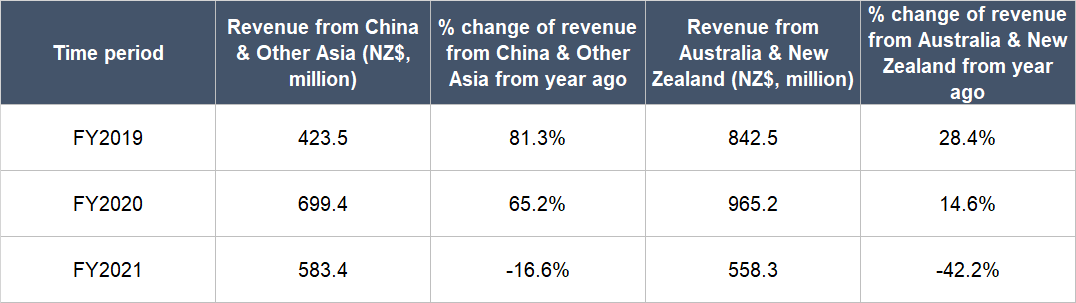

The company has two important geographical segments, China & Other Asia, and Australia & New Zealand. The former predominantly houses a2 Milk’s revenues that come from the sale of its Chinese-label infant formula products in mother and baby stores in China, as well as cross-border e-commerce sales in the country for its English-label infant formula products. Meanwhile the latter consists mostly of infant formula products that are sold within (unsurprisingly) Australia and New Zealand.

In FY2021, a2 Milk’s business in the China & Other Asia geography was negatively affected by inventory problems. Inventory levels were too high, as management built up inventory to prevent COVID-related supply chain problems but misjudged the level of end-consumer demand. There was also heightened competitive pressure from domestic infant formula brands. Meanwhile, a2 Milk’s sales in Australia & New Zealand depend partly on reseller channels where buyers would purchase a2 Milk’s products in Australia and resell them back in China. The emergence of COVID-19 and the resultant restrictions in human mobility to combat the spread of the virus caused deep disruptions in the reseller channels in the same fiscal year. There were also inventory problems in the Australia & New Zealand geography that were similar to those faced in China & Other Asia. Table 1 below shows a2 Milk’s revenues from the China & Other Asia and Australia & New Zealand geographies from FY2019 to FY2021 – note the sharp double-digit-percentage declines seen in FY2021.

Table 1; Source: a2 Milk annual reports and earnings updates

In an October 2021 investor presentation, a2 Milk’s management laid out their medium-term goal to achieve NZ$2.0 billion in revenue around five years or more from FY2021. For perspective, a2 Milk ended FY2021 with NZ$1.2 billion in revenue. So if the goal of NZ$2.0 billion is achieved by FY2026, it would represent annualised growth of less than 11%. In contrast, a2 Milk’s revenue compounded at 58% annually from FY2014 to FY2020. The revenue target of NZ$2.0 billion would also be merely 16% higher than a2 Milk’s current peak-revenue, achieved in FY2020, of NZ$1.7 billion. Moreover, management’s medium-term goal for the EBITDA (earnings before interest, taxes, depreciation, and amortisation) margin was in the “teens” percentage range. The EBITDA margin can be loosely associated with the free cash flow margin, and a2 Milk’s average free cash flow margin for FY2018 to FY2020 was significantly higher at 23.6%.

a2 Milk’s performance for the first half of FY2022 (the six months ended 31 December 2021) showed continued declines. Revenues from China & Other Asia and Australia & New Zealand fell by 6.0% and 11.0%, respectively. Although the revenue outlook for the second half of FY2022 has improved, management does not see higher earnings, indicating further margin pressure.

Typically, we’re happy to stay invested with a company if we think most of its problems are temporary. On the surface, the reseller channel disruptions for a2 Milk should be temporary, since normality should resume once COVID-19 becomes endemic. Inventory mismanagement is also a solvable problem, and a2 Milk’s management has been taking steps in the right direction, with improvements seen in the pricing situation for a2 Milk’s products in the affected areas. But crucially, management’s own view of a2 Milk’s future growth pales in comparison to what the company has achieved in the past, as we discussed earlier.

Given what we now know about a2 Milk’s performance since FY2020, and management’s growth projections, we think that the company is no longer the same high-growth and high-margin company that we had invested in initially. We had got our initial analysis on a2 Milk’s future growth prospects badly wrong. We thought it would be tasty, but it ended up leaving a bad taste in our mouth. a2 Milk’s stock price reflected its worsening fundamentals, falling from around A$19 in early July 2020 when we first invested, to around A$5 when we exited in early April 2022. Given the big decline in a2 Milk’s stock price, someone reading this might ask: “Couldn’t you have sold a2 Milk earlier?” It’s a valid question. Our response will be something we shared in Compounder Fund’s Owner’s Manual:

“And on the topic of selling stocks, we will typically sell a stock in Compounder Fund’s portfolio if we find that the investment thesis is completely broken, or we have made a big mistake in our analysis. But we will be very slow to sell. The slowness is by design – it strengthens our discipline in holding onto the winners in Compounder Fund. Holding onto the winners will be a very important contributor to Compounder Fund’s long run performance.”

With our analysis of a2 Milk being wrong, we eventually decided to sell – after holding on for some time – and redeploy the capital in other companies that we think have brighter growth prospects and thus, return potential.

And here’s an important disclaimer: None of the information or analysis presented is intended to form the basis for any offer or recommendation; they are merely our thoughts that we want to share. Compounder Fund does not own shares in any other companies mentioned in this article. Holdings are subject to change at any time